Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

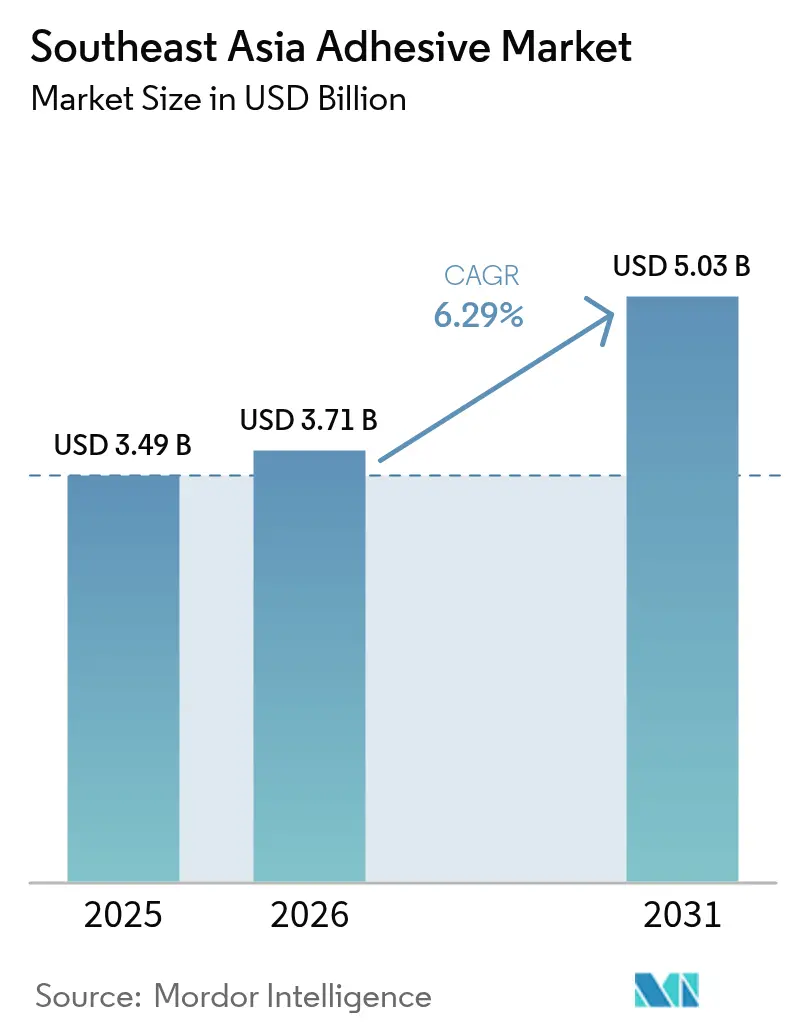

| Base Year Market Size (2025) | USD 3.49 Billion |

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.03 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

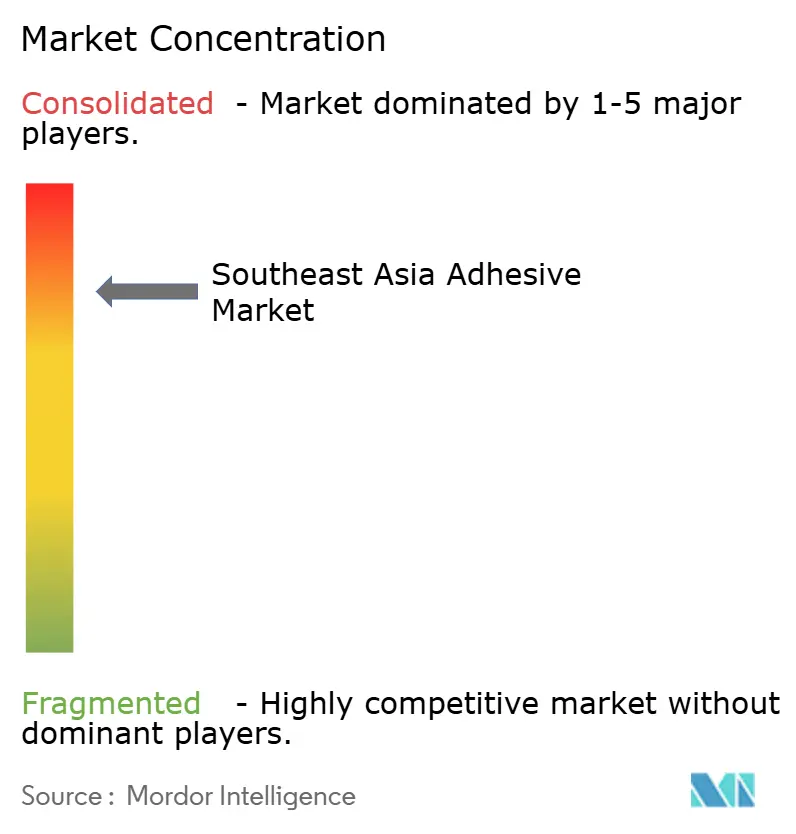

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Adhesive Market Analysis by Mordor Intelligence

The Southeast Asia Adhesive Market size is projected to expand from USD 3.49 billion in 2025 and USD 3.71 billion in 2026 to USD 5.03 billion by 2031, registering a CAGR of 6.29% between 2026 to 2031. Manufacturing localization, tighter volatile-organic-compound (VOC) caps, and an expanding electric-vehicle (EV) battery supply chain are reshaping demand patterns across Indonesia, Thailand, and Vietnam. Water-borne chemistries already dominate architectural coatings and pressure-sensitive tapes, while polyurethane (PU) systems are scaling quickly in automotive and electronics because they combine structural integrity with thermal conductivity. Feedstock swings acrylic-acid spot prices moved from USD 1,290 to USD 1,457 per metric ton between mid-2025 and February 2026, have accelerated backward-integration plans among regional producers. Competitive intensity remains moderate as multinationals such as Henkel and Sika expand technical-service hubs, yet local formulators are carving share in construction and woodworking with lower-cost water-based emulsions.

Key Report Takeaways

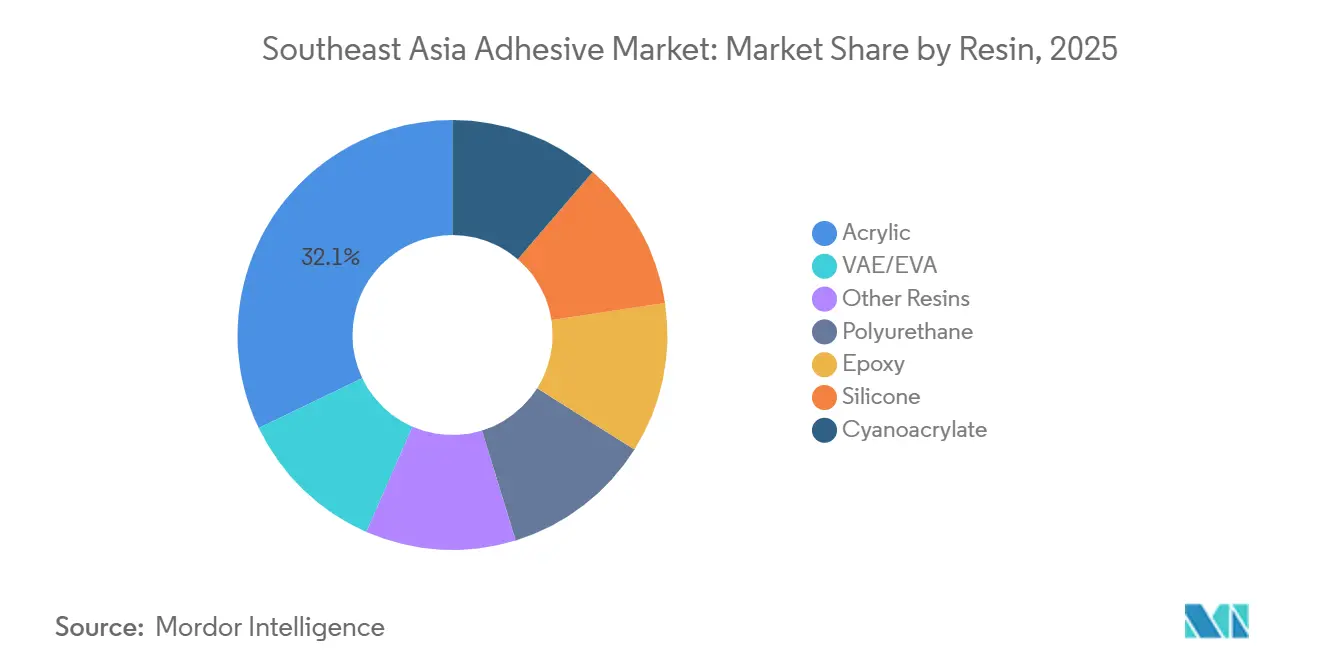

- By resin, acrylic led with 32.12% of Southeast Asia adhesives market share in 2025, while polyurethane is projected to expand at a 6.59% CAGR through 2031.

- By technology, water-borne accounted for 42.15% of the Southeast Asia adhesives market share in 2025, while UV-cured is set to grow at a 6.49% CAGR through 2031.

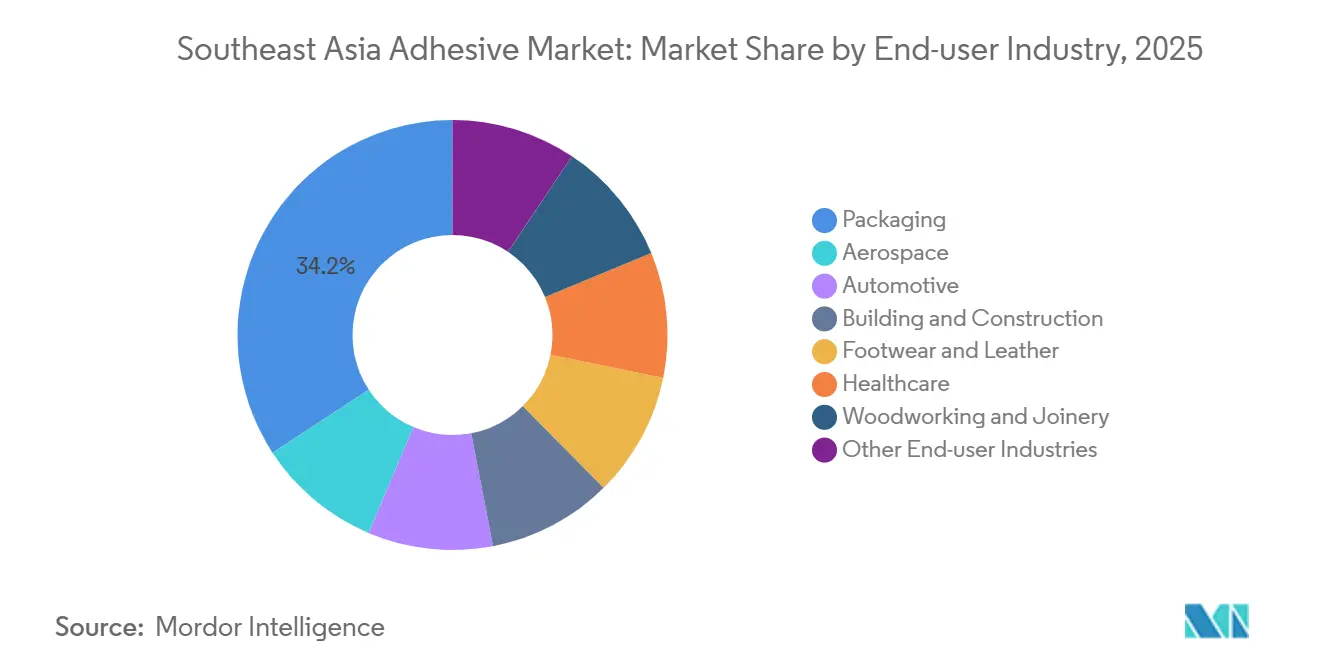

- By end-user industry, packaging captured 34.22% of the Southeast Asia adhesives market share in 2025, while automotive is forecast to post a 6.33% CAGR through 2031.

- By geography, Indonesia commanded 28.26% of the Southeast Asia adhesives market share in 2025, whereas Vietnam is projected to advance at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Adhesive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-driven surge in flexible and sustainable packaging | +1.2% | Indonesia, Thailand, Vietnam, Philippines | Short term (≤ 2 years) |

| Expansion of hygiene and medical disposables manufacturing | +0.9% | Vietnam, Thailand, Malaysia | Medium term (2-4 years) |

| Regulatory push toward low-VOC water-borne and reactive systems | +0.8% | Singapore, Malaysia, with spillover to Indonesia and Thailand | Medium term (2-4 years) |

| EV-battery manufacturing investments in Thailand and Indonesia | +1.4% | Thailand, Indonesia | Medium term (2-4 years) |

| Localization incentives for water-based raw-material production | +0.7% | Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Surge in Flexible and Sustainable Packaging

Parcel traffic increased by 533% year-on-year in custom e-commerce cartons handled by Alibaba’s regional logistics arm, driving converters to adopt hot-melt and water-borne adhesives that bond recycled corrugated board without affecting repulpability. Lintec introduced a low-temperature hot-melt adhesive in March 2025, which reduces energy consumption during application by 20% and complies with Alliance for Beverage Cartons recyclability standards. Henkel’s Technomelt E-COM series eliminates the need for pre-heating ovens on high-speed case-sealing lines, reducing downtime by 15% in Indonesia and Thailand. Additionally, brand owners transitioning to mono-material polyethylene pouches are boosting demand for solvent-free laminating adhesives. However, bio-based tackifiers, which are 20-30% more expensive than petrochemical-derived alternatives, are creating margin pressures for formulators without renewable feedstock integration.

Expansion of Hygiene and Medical Disposables Manufacturing

Kimberly-Clark completed a 40% capacity expansion at its Vietnam nonwovens facility in late 2025, emphasizing the region’s importance in adult-incontinence and feminine-care exports. Mitsui Hygiene Materials Thailand began large-scale production of superabsorbent-polymer cores in early 2026, requiring hot-melt pressure-sensitive adhesives with peel strengths exceeding 2 N/25 mm while avoiding skin irritation. Regulatory concerns over residual styrene are driving a gradual shift toward metallocene-polyolefin backbones. Vietnam’s Ministry of Health implemented ISO 10993 biocompatibility testing for adhesive ingredients in January 2026, extending approval timelines by three months. While aging demographics and rising disposable incomes support long-term growth, input-cost inflation and certification fees are tempering near-term volumes.

Regulatory Push Toward Low-VOC Water-Borne and Reactive Systems

Amendments to Singapore’s Environmental Public Health Act banned adhesives containing more than 0.1% formaldehyde starting January 2026, necessitating reformulation of solvent-borne contact cements. Hong Kong imposed a 50 g/L VOC cap on construction adhesives, effectively phasing out neoprene-based products. Thailand is considering adopting VOC limits aligned with EU Directive 2004/42/EC by 2027, potentially impacting 30% of current solvent volumes. Water-borne systems now account for 42.15% of the technology mix, but high humidity extends open times, slowing furniture production throughput. Reactive polyurethane (PU) and epoxy adhesives, which cure through crosslinking rather than solvent evaporation, are gaining market share. However, their short pot life and the high cost of metering equipment limit adoption among smaller manufacturers.

EV-Battery Manufacturing Investments in Thailand and Indonesia

CATL’s first 6.9 GWh lithium-ion cell plant in Karawang, Indonesia, began trial production in March 2026, driving demand for thermally conductive PU gap fillers with thermal conductivity ratings exceeding 3 W/m-K. A second 6.9 GWh production line is scheduled for Q3 2026 under the PT CATIB joint venture. Sunwoda is investing USD 1 billion in Thailand’s Eastern Economic Corridor to supply Japanese and European automakers. Henkel’s TEROSON adhesives, which pass 1,000-cycle thermal-shock tests required by UN 38.3 transport regulations, are preferred by several cell manufacturers. Huntsman’s SHOKLESS PU, launched in 2025, bonds aluminum battery trays without primers, reducing assembly time by 25%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and hazardous-chemical regulations | -0.6% | Singapore, Malaysia, Thailand, with gradual adoption in Indonesia and Vietnam | Medium term (2-4 years) |

| Volatile petrochemical feedstock prices | -0.9% | Regional, with acute impact on Indonesia, Thailand, and Vietnam | Short term (≤ 2 years) |

| Shortage of skilled applicators for advanced chemistries | -0.4% | Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Hazardous-Chemical Regulations

Singapore’s formaldehyde ban and Hong Kong’s 50 g/L VOC ceiling have added USD 50,000-150,000 in non-recurring engineering costs per SKU and extended product launches by up to nine months[1]Singapore Ministry of Sustainability and the Environment, “Environmental Public Health Act Amendments,” sso.agc.gov.sg. Thailand’s proposed VOC regulations require third-party testing, which smaller compounders may find unaffordable. Malaysia is considering classifying certain isocyanate adhesives under Schedule 1 poisons, necessitating closed-loop systems and annual audits. While end-users are exploring water-borne or reactive alternatives, longer cure times and weaker bonding on low-energy plastics are slowing adoption. Inventory depletion of legacy stock is causing a short-term decline before re-engineered products reach commercial scale.

Volatile Petrochemical Feedstock Prices

Acrylic-acid spot prices fluctuated between USD 1,290 and USD 1,457 per ton from mid-2025 to February 2026 due to outages at Chinese oxidation units and disruptions in Middle Eastern propane supplies. Propylene contract prices surged by 14.3% in January 2026, compressing hot-melt adhesive margins by 200-300 basis points. Ethylene prices increased by EUR 50 per ton in early 2026, leading to higher costs for vinyl acetate and EVA. Packaging converters resisted price hikes, forcing formulators to hedge through long-term supply agreements with crackers, despite lead times of 18-24 months. New cracker facilities in Indonesia and Vietnam, expected by 2028, may stabilize input costs, but near-term volatility remains a challenge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Gains on Thermal Management Needs

The Southeast Asia adhesives market for polyurethane resins is anticipated to grow at a CAGR of 6.59% through 2031, driven by the need for thermally conductive gap fillers with ratings exceeding 3 W/m-K in EV battery modules. Acrylic resins held a 32.12% revenue share in 2025, supported by their application in pressure-sensitive tapes and architectural coatings requiring UV resistance in equatorial climates. Epoxy resins dominate high-margin applications like semiconductor die-attach, while silicones are expanding in façade sealants due to their ±50% movement capability. Cyanoacrylates are increasingly used in medical device bonding, as their sub-10-second fixture times help reduce assembly delays.

The resin market is becoming more fragmented as converters focus on specialized performance rather than cost alone. Polyurethane is gaining prominence due to its role in automotive lightweighting, while bio-based hot-melts, such as those made with lignin or polyvinyl alcohol, are emerging in plywood applications, achieving bond strengths of 1.2 MPa in trials conducted by Kasetsart University. Companies with diverse portfolios and strong technical support are securing projects that demand a combination of thermal management, chemical resilience, and regulatory compliance. Fluctuating acrylic-acid prices are encouraging backward integration, though the high capital expenditure is driving smaller regional players toward toll manufacturing or joint ventures.

By Technology: UV-Cured Technology Accelerates in Electronics

Water-borne technology accounted for a 42.15% share of the Southeast Asia adhesives market in 2025, driven by its low odor and ease of cleanup. UV-cured technology is projected to grow at a CAGR of 6.49% through 2031, as smartphone and PCB manufacturers adopt LED lamps that cure acrylate oligomers in under two seconds. Solvent-borne adhesives are declining due to VOC regulations, but remain dominant in synthetic leather bonding due to their instant tack. Reactive polyurethane and epoxy adhesives are gaining traction in structural automotive components, achieving full strength within 24 hours without the need for ovens.

Hot-melts remain widely used for case sealing at 150-180 °C, though their reliance on EVA makes them vulnerable to vinyl-acetate price fluctuations. Lintec’s low-temperature hot-melt grade, which operates at 130 °C, reduces energy consumption by 20% and extends equipment lifespan. The technology landscape is becoming polarized, with commodity applications favoring cost-efficient water-borne or hot-melt solutions, while specialty segments adopt UV-cured or reactive chemistries to meet stringent durability and productivity requirements.

By End-user Industry: Automotive Adhesives Ride EV Wave

Packaging led the market in 2025 with a 34.22% revenue share, but the automotive sector is expected to grow at a CAGR of 6.33% through 2031, driven by the shift to EV manufacturing in Thailand and Indonesia. Facilities such as CATL’s twin 6.9 GWh plants in Indonesia and Sunwoda’s USD 1 billion pack facility in Thailand require adhesives for bonding aluminum trays, encapsulating prismatic cells, and sealing coolant manifolds. The building and construction sector remains the second-largest end-user, with Sika set to double its Bekasi mortar capacity in 2024 to support high-rise projects. Vietnam’s footwear production, which shipped 1.2 billion pairs in 2025, is accelerating the adoption of water-based polyurethane dispersions to comply with EU REACH solvent regulations.

Healthcare demand is rising as Kimberly-Clark and Mitsui expand nonwoven capacity, requiring skin-friendly hot-melts. Woodworking adhesives are benefiting from Indonesia’s furniture exports, relying on polyvinyl-acetate emulsions. The aerospace commands premium epoxy films for composite wings. The growing divergence between high-volume commodity applications and specialized, regulation-intensive niches is widening margin differentials across product lines.

Geography Analysis

Indonesia contributed 28.26% of 2025 revenue to the Southeast Asia adhesives market, anchored by construction, automotive parts, and battery cells. In March 2025, Avian Brands allocated USD 17 million to Dextone Lemindo to enhance water-based emulsion capacity and improve order lead times. Government tax holidays for monomer plants and abundant nickel reserves support future growth, though feedstock price fluctuations remain a concern.

Vietnam is the fastest-growing geography at a 6.72% CAGR through 2031. In May 2026, Nitto Denko expanded its capacity by adding 197 million polarized-film units and 19.6 million m³ of optical adhesives to cater to Samsung and LG production lines. Meanwhile, tesa’s EUR 55 million Hai Phong plant and Deli Group’s USD 270 million adhesive-tape hub underscore strong foreign direct investment[2]Nitto Denko Corporation, “Vietnam Optical Adhesives Capacity Add,” nitto.com. Hanoi’s move to implement EU-style VOC regulations by 2028 is anticipated to drive early adoption of water-borne and UV adhesive systems.

Thailand holds a strategic middle ground as an ASEAN automotive base. Sunwoda’s battery-pack complex and AICA’s acquisition of a 51% stake in silicone-sealant producer ADB strengthen local supply chains. In October 2024, tesa relocated its regional headquarters to Bangkok, integrating logistics and technical support to enhance market responsiveness. Malaysia and Singapore focus on high-value electronics chemistries, as demonstrated by Henkel’s electronic-adhesives lab in Singapore Science Park, launched in January 2026 as the largest in Southeast Asia. The Philippines and the rest of the region remain secondary but could attract labor-intensive footwear and garment assembly operations as wages in Vietnam increase.

Competitive Landscape

The Southeast Asia adhesives market shows high concentration. Multinational companies such as Henkel, Sika, H.B. Fuller, and 3M operate compounding and service hubs across Indonesia, Thailand, and Vietnam. Henkel’s Singapore lab, capable of handling 50 concurrent semiconductor projects, reflects a shift toward underfills and thermal-interface materials that deliver gross margins exceeding 50%. Local firms, such as Avian Brands and Macroadhesive, capitalize on shorter lead times and lower fixed costs to secure construction and woodworking accounts.

Strategic moves emphasize supply-chain security. UPM’s mid-2026 coating-line expansion in Johor Bahru localizes label-stock adhesive production and reduces shipping costs. Sika opened a Singapore mortar plant in January 2025, doubling tile-adhesive output to meet high-rise construction demand. Additionally, South Korean resin companies are exploring greenfield investments in Vietnam, which could reduce Northeast Asia’s price leverage by 5-8%.

Technology support is an emerging differentiator. Adhesive formulators that provide integrated solutions, including dispensing equipment, on-site audits, and technician training, are capturing market share in reactive and UV-cured niches where skill shortages limit growth. White-space opportunities exist in bio-based hot-melts for flexible packaging and thermally conductive silicone gels for power modules, addressing the flammability and thermal-cycling limitations of traditional solvent or epoxy chemistries.

Southeast Asia Adhesive Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

3M

Sika AG

Pidilite Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: UPM announced the establishment of a new slitting and distribution terminal near Hanoi. The facility was expected to become operational by mid-2026 to support the significant presence of electronics and durables manufacturers in the area.

- March 2025: Hindustan Adhesives Limited approved funding of IDR 5.1 billion to acquire a 51% stake in PT Bagla Group Indonesia. The acquisition aimed to enhance the company's regional presence and expand its operations in Indonesia's processing and wholesale trade sectors.

Southeast Asia Adhesive Market Report Scope

Adhesives, often known as glues, cement, mucilages, or pastes, are non-metallic agents applied to one or both surfaces of two distinct items, effectively binding them. Adhesives are employed to bond a wide array of materials, including metals, plastics, glass, and wood.

The Southeast Asia adhesives market is segmented by resin, technology, end-user industry, and geography. By resin, the market is segmented into acrylic, polyurethane, epoxy, silicone, cyanoacrylate, VAE/EVA, and other resins. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot-melt, and UV-cured. By end-user industry, the market is segmented into packaging, aerospace, automotive, building and construction, footwear and leather, healthcare, woodworking and joinery, and other end-user industries. The report also covers the market sizes and forecasts for adhesives in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin

| Acrylic |

| Polyurethane |

| Epoxy |

| Silicone |

| Cyanoacrylate |

| VAE/EVA |

| Other Resins |

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-Melt |

| UV-Cured |

By End-user Industry

| Packaging |

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Woodworking and Joinery |

| Other End-user Industries |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Resin | Acrylic |

| Polyurethane | |

| Epoxy | |

| Silicone | |

| Cyanoacrylate | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-Melt | |

| UV-Cured | |

| By End-user Industry | Packaging |

| Aerospace | |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the size of the Southeast Asia adhesives market?

The Southeast Asia adhesives market is valued at USD 3.71 billion in 2026 and is forecast to reach USD 5.03 billion by 2031.

Which resin type is growing fastest through 2031?

Polyurethane resin is projected to grow at a 6.59% CAGR through 2031, driven by EV battery and lightweight automotive applications.

How are VOC regulations affecting adhesive demand in the region?

Stringent VOC caps in Singapore, Hong Kong, and pending rules in Thailand are accelerating the shift toward water-borne and reactive systems, though reformulation costs temporarily slow uptake.

Which country will lead regional growth through 2031?

Vietnam is expected to log the highest CAGR at 6.72% as electronics, footwear, and furniture manufacturers ramp investment.

Page last updated on: