Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

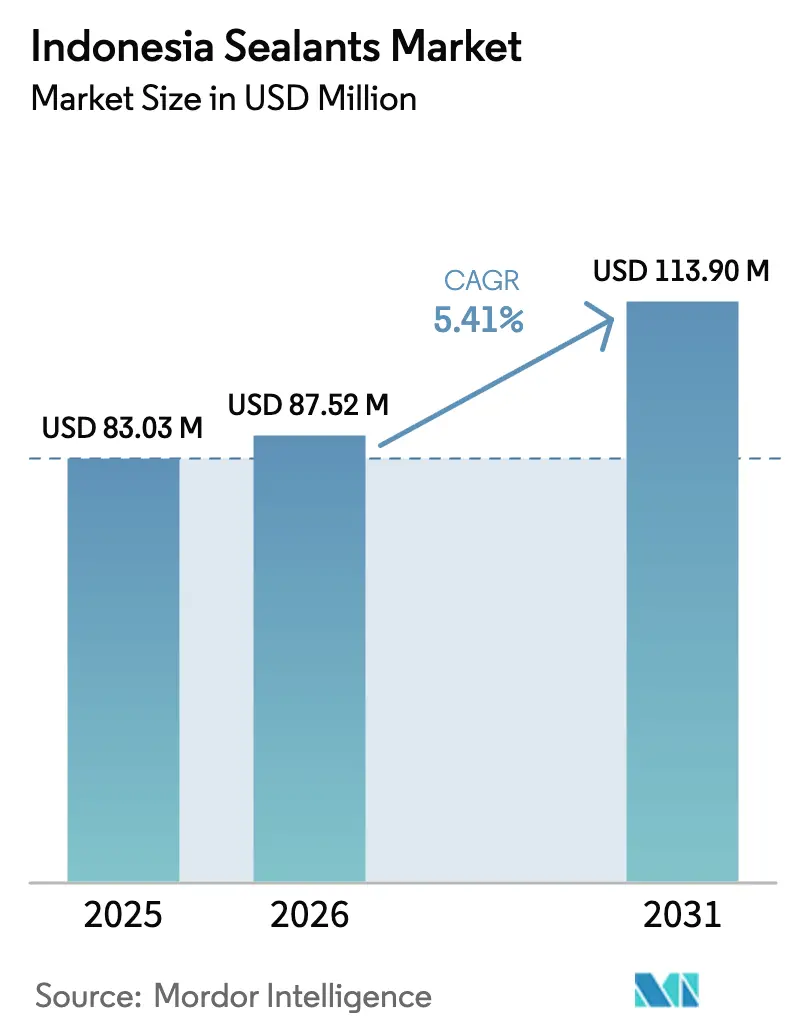

| Base Year Market Size (2025) | USD 83.03 Million |

| Market Size (2026) | USD 87.52 Million |

| Market Size (2031) | USD 113.90 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Sealants Market Analysis by Mordor Intelligence

The Indonesia Sealants Market size is expected to grow from USD 83.03 million in 2025 to USD 87.52 million in 2026 and is forecast to reach USD 113.90 million by 2031 at 5.41% CAGR over 2026-2031. In Indonesia, a surge in residential and industrial construction, coupled with investments in electric vehicle assembly in West Java and a shipbuilding revival in Sulawesi, is driving the adoption of weather-proofing, structural, and marine-grade formulations. Multinational brands are ramping up local production to meet mandatory SNI certification and tropical-performance testing. Meanwhile, a draft regulation on low-VOC emissions set for the 2026–2031 period is pushing demand toward waterborne acrylic and alpha-silane chemistries. Additionally, while low-cost imports from China are putting pressure on commodity prices, there is a noticeable shift toward differentiated products, bolstered by technical services and local validation.

Key Report Takeaways

- By resin, silicone captured 44.22% of 2025 demand, the largest Indonesia sealants market share, while acrylic is projected to grow the fastest at a 5.83% CAGR (2026-2031).

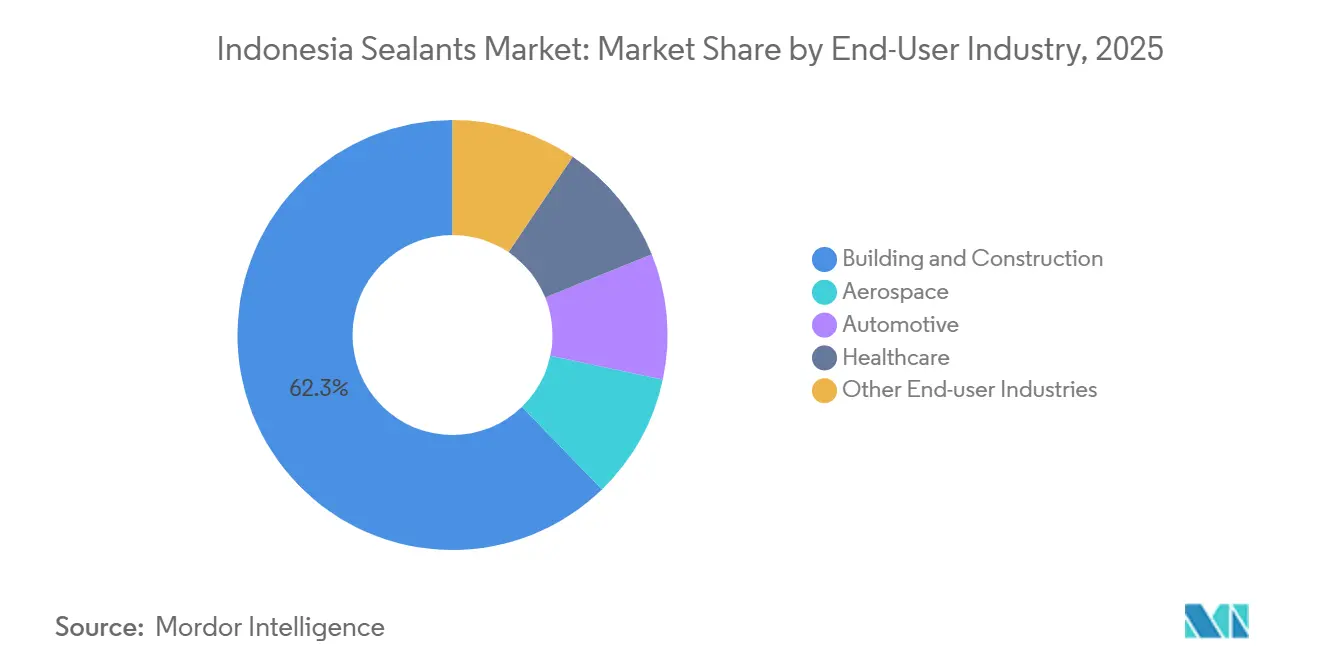

- By end-user industry, building and construction accounted for 62.25% of 2025 revenue, the dominant end-user in the Indonesia sealants market, whereas healthcare is forecast to expand at a 6.12% CAGR (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM automotive line-expansion in West Java | +1.2% | West Java (Subang, Purwakarta, Karawang), spillover to Greater Jakarta | Medium term (2-4 years) |

| Growing demand for tropical-climate weather-seal retrofits | +1.5% | National, concentrated in coastal Java, Sumatra, Sulawesi | Short term (≤ 2 years) |

| Eco-friendly low-VOC siloxane push (2027 draft MoEF rule) | +0.8% | National, early adoption in Jakarta, Surabaya, Bandung | Long term (≥ 4 years) |

| Sulawesi shipbuilding corridor fueling marine-grade uptake | +0.9% | Sulawesi (North, Central, South), Kalimantan ports | Medium term (2-4 years) |

| E-commerce logistics hubs needing high-movement floor joints | +0.7% | Greater Jakarta, Surabaya, Semarang, Batam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Automotive Line Expansion in West Java

By March 2026, BYD's electric-vehicle plant in Subang will have neared completion. With a target for annual production capacity, the plant is expected to influence the demand for silicone thermal-interface materials and polyurethane structural sealants. In June 2025, IMAS and GAC Aion inaugurated a scalable facility in Purwakarta, with a notable portion of their components sourced locally. These initiatives are projected to boost the forecast CAGR for the period 2026–2031 by creating a consistent demand for battery-housing gaskets, lightweight body bonding, and cabin air-tightening sealants. Wacker's expansion of specialty silicones capacity in the Asia-Pacific region ensures a steady supply for Indonesian OEM tiers. As the industry transitions from internal combustion engines to battery packs, certain engine-bay applications have diminished. However, this shift has created opportunities for more valuable electrification joints, elevating quality standards in Indonesia's sealants market.

Tropical-Climate Weather-Seal Retrofits

In Indonesia, where humidity levels consistently range from 70% to 90% and annual rainfall can peak at 6,000 mm, sealants experience reduced lifespans[1]Jozef Švajlenka and Hermawan Hermawan, “Building Envelope and Microclimate Variables,” Sustainability, mdpi.com. This climatic hurdle has spurred a steady demand for retrofitting in areas such as glazing, façade joints, and sanitary grades. In recent years, as the building sector has expanded, developers, acutely aware of humidity challenges, have emphasized mitigation strategies, particularly in high-occupancy projects. By 2024, Sika had broadened its retail footprint, a strategic move in tune with Indonesia's growing trend of do-it-yourself sealant replacements. Although SNI-mandated tropical durability testing can extend product approval by four to eight weeks, showcasing resilience against hydrolytic and fungal stress is becoming a pivotal branding edge. With the e-commerce boom, there is an escalating demand for warehouses, amplifying the need for flexible, forklift-resistant floor-joint sealants. These sealants must endure the challenges posed by heavy machinery and the country's pronounced moisture fluctuations.

Low-VOC Siloxane Reformulation Push

Presidential Regulation 110/2025 introduces a carbon-economic-value framework, targeting a reduction in construction-chemical VOCs by 2027. This regulation encourages formulators to adopt waterborne acrylics and alpha-silane hybrids. In March 2025, BASF and Sika launched their Baxxodur EC 151 hardener, which is designed to significantly reduce VOCs in epoxy systems, highlighting a pathway to early compliance. Regulation 7/2024 has increased costs for import permits on ozone-depleting substances and HFCs, impacting solvent and foam systems. This development is steering Indonesia's sealants market toward a preference for silicone and hybrid chemistries. In Jakarta and Surabaya, early adopters are specifying low-emission grades to meet green-building certification standards, further promoting the localization of waterborne dispersion supplies within the supply chain.

Sulawesi Shipbuilding Corridor Stimulus

Indonesia's shipyards, which annually build vessels and conduct repairs, are fueling a strong demand for marine polysulfide, polyurethane, and silicone joints. In July 2025, PT Dok dan Perkapalan Air Kantung and PT PAL signed a cooperation pact to modernize facilities, underscoring policy support for domestic vessel production. Research on the design of service life indicates that sealed 70 mm concrete covers can delay corrosion onset by over 60 years in tropical marine environments. Regulations from classification societies, coupled with TKDN local-content certificates, enhance the localization of specialty sealants. This move ensures a sustained volume for suppliers boasting certified marine products during the forecast period of 2026–2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising inflow of low-cost PRC imports | -0.9% | National, acute in Greater Jakarta, Surabaya, Medan | Short term (≤ 2 years) |

| Prolonged SNI certification for aerospace-grade sealants | -0.5% | National, most acute for specialty/high-performance segments | Medium term (2-4 years) |

| Skilled applicator shortage outside Java | -0.6% | Eastern provinces (Sulawesi, Kalimantan, Papua, Maluku) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Inflow of Low-Cost Chinese Imports

In July 2025, Indonesia saw a surge in imports of caulking compounds and adhesive preparations from China, with the latter offering substantial discounts over local brands. These imports, including toluene di-isocyanate and silicone polymers, enabled aggressive under-pricing, thereby tightening profit margins for Indonesia's commodity-grade sealant suppliers. In 2025, Henkel restructured its Southeast Asia distributorship, underscoring how global entities recalibrated their market strategies to combat budget-friendly competitors while enhancing their premium service image. Despite the introduction of carbon-levy mechanisms under Regulation 110/2025, aimed at penalizing high-emission imports to bridge the cost gap, the immediate pricing pressures still cast a slight shadow on growth during the forecast period of 2026–2031.

Certification and Skilled-Labor Gaps

In Indonesia, securing SNI approval for specialty aerospace and military sealants takes 12 to 24 months. This lengthy process includes ISO 9001 audits and tropical durability testing, causing delays in bringing these low-volume, high-margin products to market. Outside Java, a shortage of certified applicators limits the use of two-component polyurethane and epoxy systems, which require careful mixing and surface preparation. Although BIM mandates have clarified designs for more than 100 government projects, the real-world success of these designs hinges on the skill level of the workforce. As a result of these prolonged certification processes and labor challenges, Indonesia's sealants market faces a tempered growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Dominance Amid Acrylic Acceleration

In 2025, silicone secured a commanding 44.22% revenue share in Indonesia's sealants market, primarily due to its exceptional ultraviolet (UV) stability and adhesion. These attributes are critical for the archipelago's humid, high-rainfall climate. Conversely, acrylic grades are projected to register the highest compound annual growth rate (CAGR) of 5.83% during the forecast period of 2026–2031. This trend is attributed to a growing preference among contractors for cost-effective, low-volatile organic compound (VOC) solutions for residential retrofits, a shift catalyzed by Regulation 110/2025.

Silicone's elastic recovery and biocide-friendly formulation ensure that façade and sanitary joints can withstand daily wet-dry cycles, with a lifespan of 10 to 15 years. Simultaneously, the demand for acrylic roof and wall fillers in Indonesia is increasing, driven by government housing subsidies that encourage repainting and leakage repairs. In the automotive sector, polyurethane plays a critical role in bonding and securing joints in warehouse flooring, where tensile adhesion exceeding 1.5 megapascal (MPa) is essential. This segment is also benefiting from the rapidly expanding West Java Electric Vehicle corridor. Furthermore, hybrid alpha-silane technologies, developed at Wacker’s Asian facilities, combine the flexibility of silicone with the adhesion strength of polyurethane. These advancements offer tin-free alternatives, aligning with future VOC regulations.

By End-User Industry: Construction Pre-eminence with Healthcare Upswing

In 2025, residential and industrial projects propelled the building and construction sector to dominate, capturing 62.25% of the market's value. These projects consistently require glazing sealants, expansion-joint fillers, and bathroom silicones. From 2026 to 2031, the emergence of new automotive plants is expected to elevate the demand for batteries, body-in-white, and cabin sealing. Additionally, marine yards in Sulawesi are supporting specialty orders.

Healthcare, with a robust 6.12% CAGR (2026-2031), is the fastest-growing consumer in the market. As Indonesia's pharmaceutical landscape expands, hospitals are increasingly adopting ISO-class clean-room sealants. By 2031, a significant surge in the sealants market for Indonesian healthcare facilities is anticipated, driven by the growth of cold-chain warehouses for biologics. While the aerospace sector faces limited volumes due to certification challenges, naval maintenance is gaining momentum at PT PAL Indonesia's upgraded docks.

Geography Analysis

In Indonesia, the construction boom in Greater Jakarta and the rising electric vehicle (EV) sector in West Java are driving the nation's demand for high-performance silicones and polyurethanes. These materials are crucial for applications ranging from building facades to battery packs and clean-room floors. Sika's expansive megasite in Bekasi not only anchors regional distribution but also ensures prompt aftermarket replenishment, reinforcing its critical role in Indonesia's sealants market.

Sulawesi, home to numerous shipyards, is experiencing the fastest growth. These shipyards require marine-grade joints that can withstand saltwater and UV fluctuations. A collaboration between PT PAL and PT DAK has modernized these local shipyards, underscoring the demand for classification-approved sealants. This emphasis has notably increased the market share of certified polysulfides within Indonesia's sealants sector.

Sumatra and Kalimantan, while showcasing potential with their untapped demand from the mining and agro-industrial sectors, face challenges due to a shortage of skilled applicators for two-component systems. However, with focused training initiatives, there is a promising opportunity to penetrate the lucrative polyurethane and epoxy markets. Research indicates that silicone sealants, especially around glazing and concrete joints, can significantly extend the lifespan of sealed 70 mm covers, preventing corrosion for up to six decades[2]Hilmy Mochamad and Herry Prabowo, “Service Life Design for Infrastructure,” scitepress.org. This is particularly beneficial in coastal regions vulnerable to chloride ingress.

Competitive Landscape

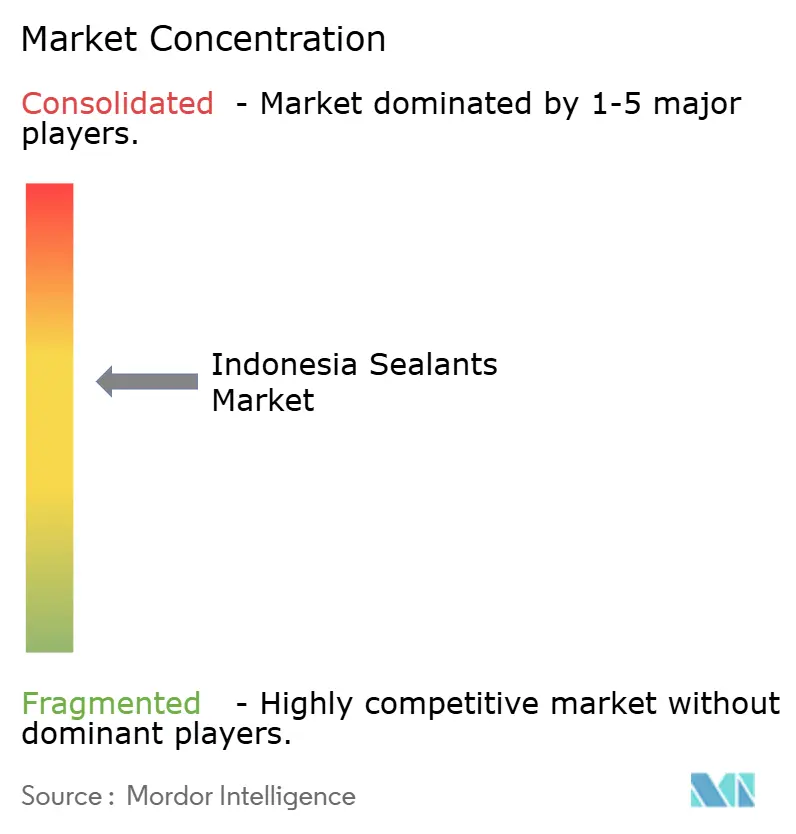

The Indonesian sealants market is moderately consolidated. Factors such as SNI timelines, validation in tropical labs, and the provision of on-site application training influence competitive intensity. Suppliers who invest in BIM-integrated technical services enjoy elevated specification rates in government projects. In contrast, brands lacking local ISO-accredited testing encounter delays in market entry.

Indonesia Sealants Industry Leaders

Sika AG

3M

Dow

Henkel AG & Co. KGaA

DEXTONE INDONESIA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Saint-Gobain completed a USD 1.025 billion acquisition of Fosroc, expanding its construction-chemicals and sealant portfolio in Indonesia.

- May 2024: Dow secured six honors at the SEAL Business Sustainability Awards for Silastic SST 2650 self-sealing silicone and DOWSIL 991 high-performance sealant to underscore environmental and application excellence.

Indonesia Sealants Market Report Scope

A sealant is a flexible or rigid substance applied to joints, gaps, or surfaces to block the passage of fluids, air, dust, or heat, effectively preventing leaks and protecting against environmental damage. It is widely used in construction, automotive applications, and DIY projects due to its durability, adhesion, and flexibility, with common types including silicone and polyurethane.

The Indonesian sealants market is segmented by resin and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts are done based on value (USD).

By Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms