Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

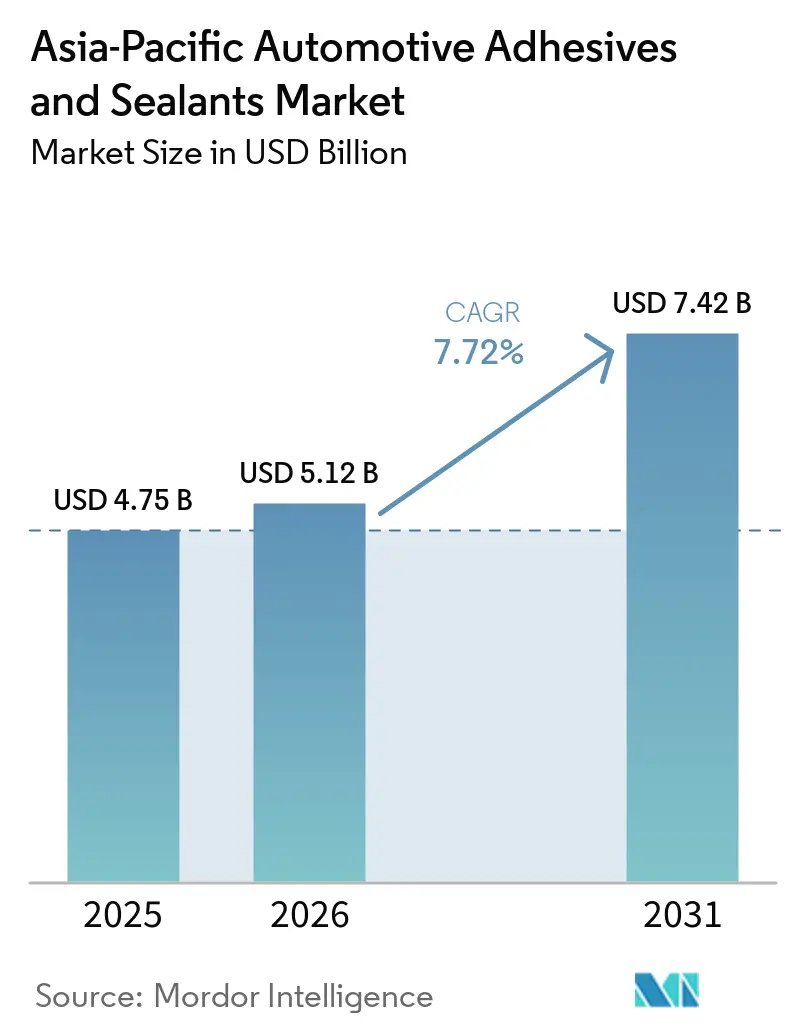

| Base Year Market Size (2025) | USD 4.75 Billion |

| Market Size (2026) | USD 5.12 Billion |

| Market Size (2031) | USD 7.42 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Adhesives And Sealants Market Analysis by Mordor Intelligence

The Asia-Pacific Automotive Adhesives and Sealants Market size is projected to be USD 4.75 billion in 2025, USD 5.12 billion in 2026, and reach USD 7.42 billion by 2031, growing at a CAGR of 7.72% from 2026 to 2031. Automakers are increasing the use of adhesives per vehicle as multi-material body-in-white designs replace traditional spot-welded steel structures. This change is driven by the implementation of China VI B emission limits and the alignment of Corporate Average Fuel Economy (CAFE) targets. The rapid growth in battery-electric vehicle (BEV) production is further boosting demand for thermal-interface and gasketing materials capable of dissipating heat at levels exceeding 1.5 W/m·K. Simultaneously, countries such as Indonesia, India, and Thailand are localizing electric vehicle (EV) assembly, leading to a rise in demand for polyurethane and silicone sealants that comply with strict flammability and dielectric standards. Global suppliers are introducing isocyanate-free, bio-based, and debondable adhesive grades that improve recyclability and reduce lifecycle emissions without compromising lap-shear strength. Fluctuations in feedstock prices and a shortage of skilled labor for robotic dispensing remain key challenges to broader adoption in tier-two plants across ASEAN.

Key Report Takeaways

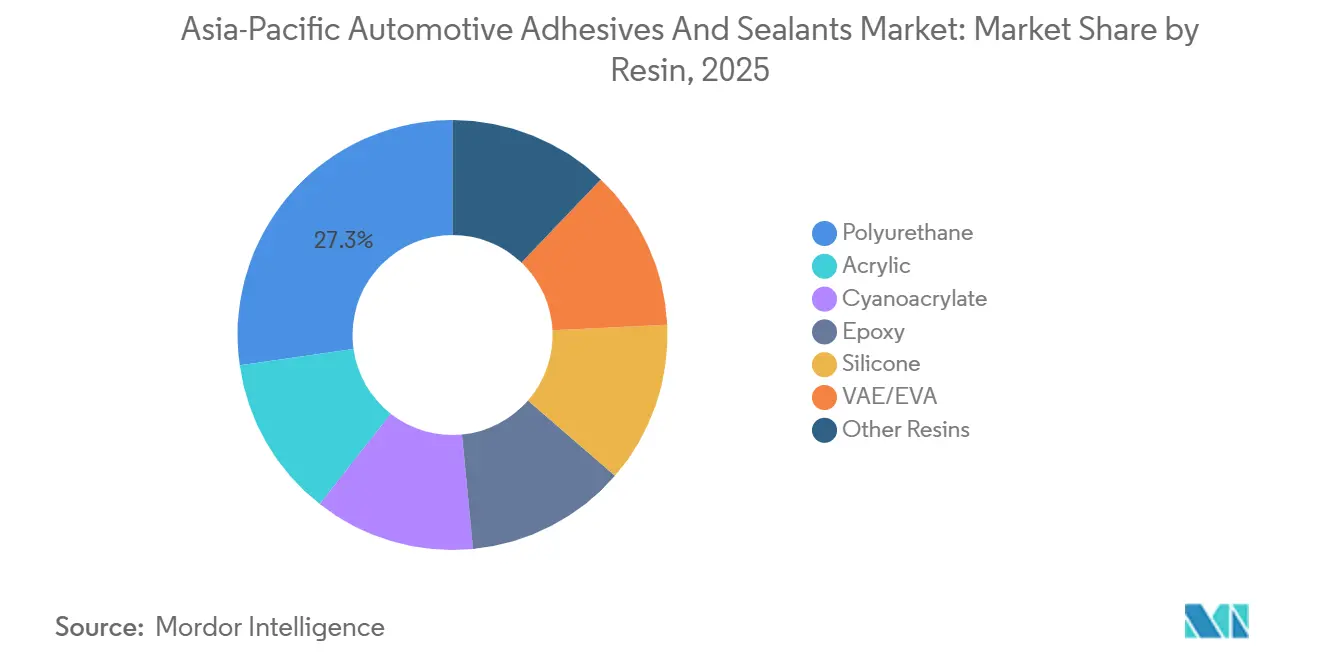

- By resin, polyurethane led with 27.25% of the Asia-Pacific Automotive Adhesives & Sealants market share in 2025, while VAE/EVA is projected to expand at a 6.55% CAGR through 2031.

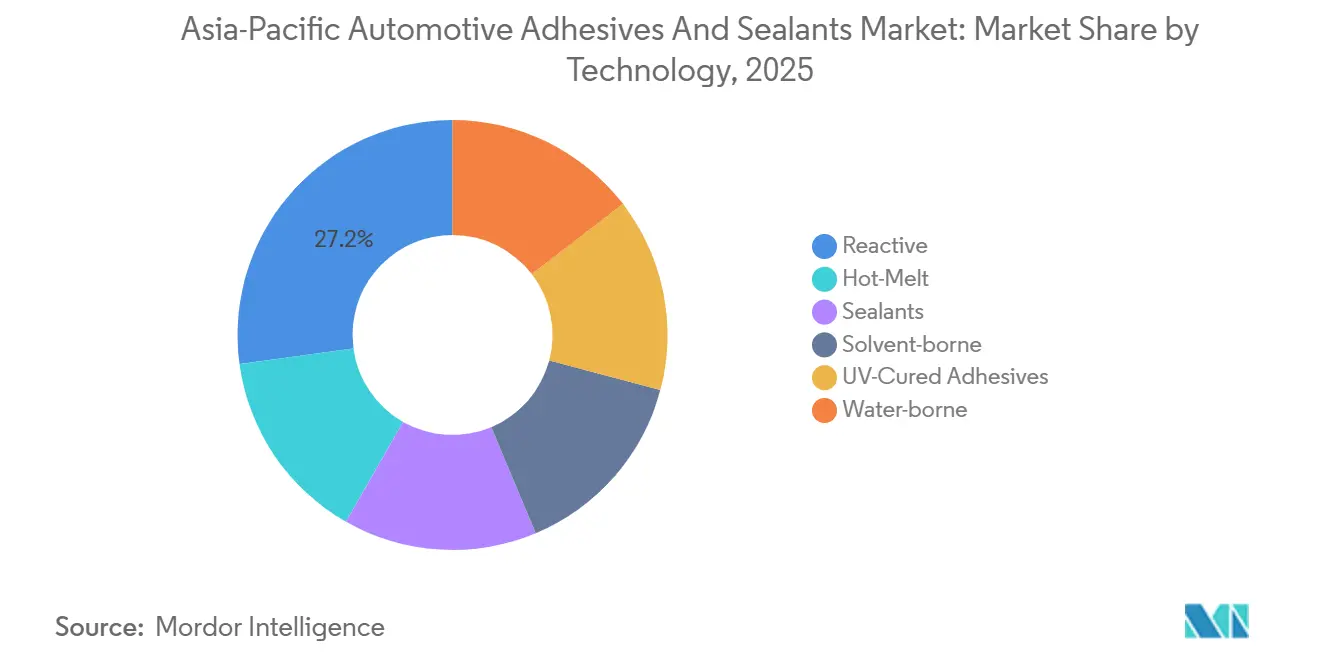

- By technology, reactive systems held 27.16% revenue share in 2025; hot-melt platforms record the swiftest trajectory at an 8.53% CAGR over 2026-2031.

- By geography, China dominated with 53.66% of regional sales in 2025, whereas Indonesia is forecast to post the fastest 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Automotive Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM preference for multi-material body-in-white designs | +1.8% | China, Japan, South Korea; spillover to India and Thailand | Medium term (2-4 years) |

| Weight-reduction mandates under China VI and CAFE norms | +1.5% | China (national); Japan and South Korea (voluntary CAFE-equivalent) | Short term (≤ 2 years) |

| Uptick in EV battery pack gasketing demand | +1.6% | China, India, Indonesia; early adoption in Thailand and Malaysia | Medium term (2-4 years) |

| Start-ups commercializing bio-based polyurethane chemistries | +0.7% | Global, with pilot deployments in Japan and South Korea | Long term (≥ 4 years) |

| Emergence of low-surface-energy composite adhesives | +0.6% | Japan, South Korea, China (premium OEMs); niche in India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Preference for Multi-Material Body-in-White Designs

Automakers in the region are integrating steel, aluminum, magnesium, and carbon-fiber-reinforced polymers within single structures to reduce curb weight by 8-12%. This change has increased adhesive usage from approximately 15 kilograms to over 25 kilograms per vehicle[1]Sika AG, “Investor and Media Conference Fast Forward,” sika.com. ArcelorMittal’s multi-phase integration process for Chinese sedans combines ultra-high-strength steel with aluminum closures, a pairing unsuitable for resistance spot-welding due to the risk of galvanic corrosion. In 2025, Seres adopted magnesium die-cast subframes, specifying epoxy structural adhesives that achieve lap-shear strength exceeding 10 megapascals (MPa) without requiring surface pretreatment. Japanese tier-one suppliers report that silyl-modified-polymer sealants, which cure at ambient temperatures, reduce cycle times by eliminating the need for bake ovens. These advancements are embedding adhesives more deeply into high-volume platforms scheduled for launch between 2027 and 2030.

Weight-Reduction Mandates Under China VI and CAFE Norms

China’s implementation of China VI B standards in January 2026 will reduce particulate matter thresholds by 30% and nitrogen oxide (NOx) limits by 50%, while real-driving-emissions testing will enhance enforcement. Additionally, original equipment manufacturers (OEMs) must achieve a fleet average of 3.3 liters per 100 kilometers (L/100 km) by 2030, driving the substitution of steel with adhesive-bonded aluminum and composites that eliminate the need for energy-intensive heat tunnels. Hyundai and Kia are following a similar approach, using reactive hot-melts on tailgates and hoods to reduce weight by 3-5 kilograms per closure. Japan’s Stage 4 regulations, effective in 2026, extend lightweighting requirements to vans and mini-trucks, increasing supplier demand for qualified one-component polyurethanes.

Uptick in EV Battery-Pack Gasketing Demand

Battery electric vehicle (BEV) charge rates exceeding 3C are raising pack temperatures, leading to the adoption of thermal-interface adhesives with conductivity levels of 1.5-3 watts per meter-kelvin (W/m·K), which are replacing traditional gap fillers. Henkel’s LOCTITE SI 54861 silicone gasket, certified to UL94-V0 and offering over 200% elongation, has become standard for Chinese battery top covers[2]H.B. Fuller Co., “2025 Investor Day,” hbfuller.com . In India, EV adhesive revenue is projected to grow from USD 94.3 million in 2024 to nearly USD 2 billion by 2034, supported by Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) II subsidies. Debondable chemistries that soften under controlled heat are being piloted by Japanese recyclers, enabling pack disassembly without shredding.

Start-Ups Commercializing Bio-Based Polyurethane Chemistries

Henkel introduced Technomelt PUR 6260 ECO in November 2025, featuring 60% castor-oil and recycled polyol content while meeting lap-shear strength requirements of greater than or equal to 3 megapascals (MPa). DIC is expanding its waterborne polyurethane capacity in Guangdong and increasing epoxy resin production by 59% at its Chiba plant, with completion expected by July 2029, supported by a JPY 3 billion (USD 0.01 billion) government grant. Although bio-based grades carry a 15-20% cost premium, carbon-border-adjustment regulations are accelerating fleet-wide trials among multinational OEMs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in isocyanate and epoxy feedstock prices | -0.9% | China, Japan, South Korea (primary production hubs); cascades to ASEAN | Short term (≤ 2 years) |

| OEM push toward mechanical fastening for ease-of-repair | -0.5% | India, Indonesia, Thailand (nascent collision-repair networks) | Medium term (2-4 years) |

| Stringent VOC caps in Japan and South Korea | -0.4% | Japan, South Korea, and the indirect influence on China's coastal cities | Short term (≤ 2 years) |

| Skill gap in robot-dispensing programming at Tier-2 plants | -0.3% | Indonesia, Thailand, Malaysia (tier-two supplier clusters) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Isocyanate and Epoxy Feedstock Prices

Unplanned methylene diphenyl diisocyanate (MDI) outages and fluctuations in crude oil prices caused spot-market variations through 2025, reducing the margins of smaller ASEAN formulators by 200-300 basis points. The epoxy market weakened in early 2026, leading some suppliers to delay research and development initiatives and capacity expansion plans. DIC’s new Chiba epoxy unit, subsidized to ensure domestic supply, highlights the significant capital investment required to manage raw material risks. While silyl-modified polymer alternatives help reduce isocyanate exposure, they remain limited by thermal-aging constraints above 120°C.

OEM Push Toward Mechanical Fastening for Ease of Repair

Collision-repair networks in India and Indonesia often lack access to infrared ovens and surface preparation tools, prompting automakers to reintroduce clips and rivets for non-structural panels. This hybrid approach reduces adhesive consumption by 10-15% per vehicle and has influenced Tesla Shanghai’s battery-pack assembly, which incorporated mechanical fasteners in 2025 to streamline warranty-related repairs. H.B. Fuller Company’s 2024 acquisition of ND Industries reflects the expectation that fastener-adhesive hybrids will continue to play a role in cost-sensitive market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Dominates, VAE/EVA Accelerates

Polyurethane is expected to account for 27.25% of the Asia-Pacific Automotive Adhesives & Sealants market share in 2025, driven by its 400% elongation and moisture-curing properties, which are suitable for mixed-substrate joints. Henkel’s thermal-conductive polyurethane grades, offering thermal conductivity of 1.2-3.4 watts per meter-kelvin (W/m·K), are widely used in bonding electric vehicle (EV) modules. Epoxy adhesives are utilized in under-hood applications requiring resistance to temperatures up to 180°C, while silicone adhesives are preferred for high-voltage battery packs due to their dielectric strength exceeding 10 kilovolts per millimeter (kV/mm).

Vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne systems, though currently smaller in market share, are projected to grow at a compound annual growth rate (CAGR) of 6.55% through 2031. Their cost-effectiveness and compliance with volatile organic compound (VOC) regulations make them suitable for applications such as headliners and door panels in India. These adhesives help original equipment manufacturers (OEMs) meet Japan’s in-cabin formaldehyde limit of 100 micrograms per cubic meter (µg/m³) without requiring ultraviolet (UV) lamp investments. The market for VAE/EVA adhesives is expected to expand significantly, supported by increased regional production capacity from domestic suppliers.

By Technology: Reactive Systems Hold Ground, Hot-Melt Gains

Reactive one- and two-component systems are projected to retain a 27.16% revenue share in 2025, owing to their ability to deliver lap-shear strength of greater than or equal to 15 megapascals (MPa) across a temperature range of -40°C to +120°C. Sika has reported strong demand for these systems in both global and regional automotive platforms in Asia.

Hot-melt adhesives are anticipated to grow at a CAGR of 8.53% through 2031, marking the fastest growth among all technologies. Their ability to achieve handling strength within 15 seconds makes them suitable for high-mix production lines in countries like Thailand and Malaysia. The market for hot-melt adhesives is expected to expand as solvent-borne alternatives are phased out due to stricter VOC regulations. UV-cured adhesives remain a premium option, primarily used in windshield and panoramic roof assembly, where lamp-line-of-sight constraints limit broader adoption.

Geography Analysis

China accounted for 53.66% of regional revenue in 2025, driven by the production of over 25 million passenger vehicles and the early adoption of multi-material designs influenced by China VI B emissions regulations. Sika expanded its operations with new plants in Xi’an and Suzhou; however, a sluggish real estate sector led to a 5.2% decline in its Chinese sales in local currency during 2025. Despite this, outbound Chinese OEM projects valued at CHF 19 billion (USD 24.05 billion) have increased export demand for adhesives meeting global specifications.

Japan and South Korea are focusing on UV-cured and bio-based chemistries, though strict VOC limits have raised capital expenditures for tier-two suppliers. DIC’s JPY 3 billion (USD 0.01 billion) subsidy-supported epoxy expansion, scheduled for completion by 2029, is expected to enhance supply security and boost technology exports to ASEAN countries. Hyundai and Kia have adopted reactive hot-melts for global platforms to meet voluntary fuel-efficiency targets aligned with China’s CAFE standards.

Indonesia is leading regional growth with a 6.72% CAGR, supported by a 230% year-on-year increase in BEV sales during Q1 2024. Sika doubled its Bekasi plant capacity in 2024 and initiated water-borne adhesive trials across its Java facilities. India follows with consistent annual adhesive demand growth of 8-10%, highlighted by Pidilite’s USD 36 million Punjab facility, which aims for a 200,000-ton capacity by 2027. Thailand’s 20.65% rebound in passenger car sales in November 2025 and Malaysia’s high-throughput hot-melt production lines further underscore the growth potential in the ASEAN region.

Competitive Landscape

The Asia-Pacific automotive adhesives & sealants market is moderately fragmented. Five major global companies, Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, 3M, and Dow, account for an estimated 55-60% of tier-one Original Equipment Manufacturer (OEM) specifications in the Asia-Pacific Automotive Adhesives & Sealants market. Sika’s “Fast Forward” initiative plans to close several smaller Chinese plants by 2027, targeting annual savings of CHF 150-200 million (USD 189.94-253.25 million), reflecting cost pressures even for established players. Arkema’s USD 150 million acquisition of Dow’s flexible-packaging laminating-adhesive line has added solvent-free and bio-based assets, which are projected to generate USD 30 million in Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) within five years.

H.B. Fuller Company expanded its market presence with the 2024 acquisition of ND Industries, positioning itself to address the increasing demand for hybrid fastener-adhesive solutions in cost-sensitive interior applications. Regional competitors such as Pidilite, DIC, and Shanghai Huitian are gaining traction in the aftermarket and tier-two segments by developing low-surface-energy and Volatile Organic Compound (VOC)-compliant products tailored to local regulatory requirements. Huntsman’s SHOKLESS polyurethane foam for Electric Vehicle (EV) batteries and the opening of its 11,000 m² innovation hub in 2024 highlight the significant Research and Development (R&D) investments required to compete in high-margin e-mobility segments. Opportunities for growth remain in areas such as debondable adhesives for recycling and primer-less bonding solutions for polypropylene and carbon fiber.

Asia-Pacific Automotive Adhesives And Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

Dow

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Henkel AG & Co. KGaA introduced Loctite MS 9650, an isocyanate-free silyl-modified polymer adhesive, designed for bonding multiple substrates in automotive production. This product targets the growing demand for adhesives and sealants in the Asia-Pacific automotive industry, particularly in India and Southeast Asia.

- June 2025: Sika AG has upgraded its Suzhou plant to focus on high-viscosity polyurethane technologies for advanced bonding and sealing, prioritizing local-for-local supply. This development aligns with the growing demand for automotive adhesives and sealants in the Asia-Pacific region.

Asia-Pacific Automotive Adhesives And Sealants Market Report Scope

Automotive adhesives and sealants are chemical compounds used to bond components, fill gaps, and seal joints in vehicles. They act as an alternative to mechanical fasteners, aiding in weight reduction, improving structural integrity, and enhancing durability. These compounds prevent leaks, reduce noise and vibration (Noise, Vibration, and Harshness - NVH), and ensure effective stress distribution, which is critical for the assembly of modern lightweight and electric vehicles.

The Asia-Pacific automotive adhesives and sealants market is segmented by resin, technology, and geography. By resin, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into hot-melt, reactive, sealants, solvent-borne, UV-cured adhesives, and water-borne. The report also covers the market size and forecasts for automotive adhesives and sealants in 9 countries across the region. The market sizes and forecasts are provided in terms of value (USD).

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Hot-Melt |

| Reactive |

| Sealants |

| Solvent-borne |

| UV-Cured Adhesives |

| Water-borne |

By Geography

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Singapore |

| South Korea |

| Thailand |

| Rest of Asia-Pacific |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Hot-Melt |

| Reactive | |

| Sealants | |

| Solvent-borne | |

| UV-Cured Adhesives | |

| Water-borne | |

| By Geography | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - In the automotive industry, both the OEM and after market adhesive and sealants applications are considered under the scope.

- Product - All adhesive and sealant products used in automotive industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, UV Cured Adhesives, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms