Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

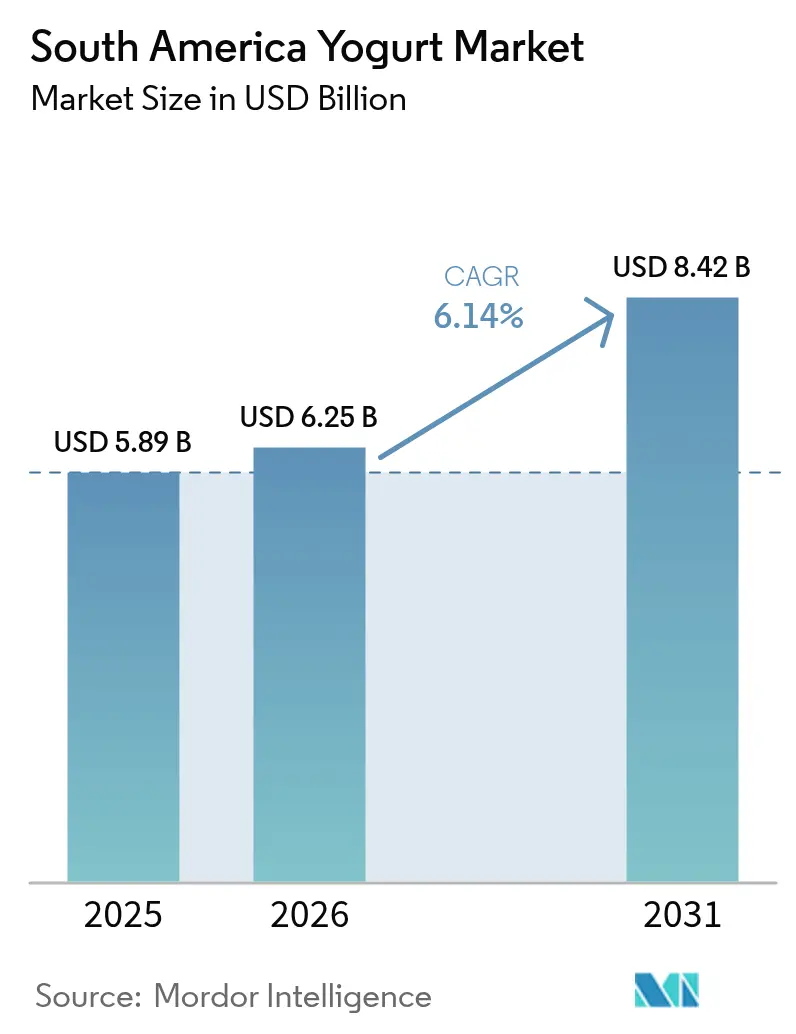

| Base Year Market Size (2025) | USD 5.89 Billion |

| Market Size (2026) | USD 6.25 Billion |

| Market Size (2031) | USD 8.42 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Yogurt Market Analysis by Mordor Intelligence

South American Yogurt Market size market size in 2026 is estimated at USD 6.25 billion, growing from 2025 value of USD 5.89 billion with 2031 projections showing USD 8.42 billion, growing at 6.14% CAGR over 2026-2031. The market's expansion is driven by multiple factors, including health-conscious consumer preferences, expanding cold chain infrastructure, and flexitarian dietary shifts. The growing urban population and rising disposable incomes have significantly influenced consumption patterns, while sustainability concerns have created a strategic need for manufacturers to diversify their product portfolios. The market encompasses traditional, Greek-style, and flavored yogurts, with major dairy companies expanding their production capacities to meet demand. While the trend toward natural and organic variants, innovative packaging solutions, and new flavor combinations continues to shape market dynamics, challenges persist in the form of volatile milk prices and import tariffs on probiotic cultures. These challenges particularly affect small and medium enterprises striving to maintain profit margins while meeting consumer demands for premium offerings. The increasing adoption of yogurt as a breakfast option and healthy snack alternative further supports market growth across South America.

Key Report Takeaways

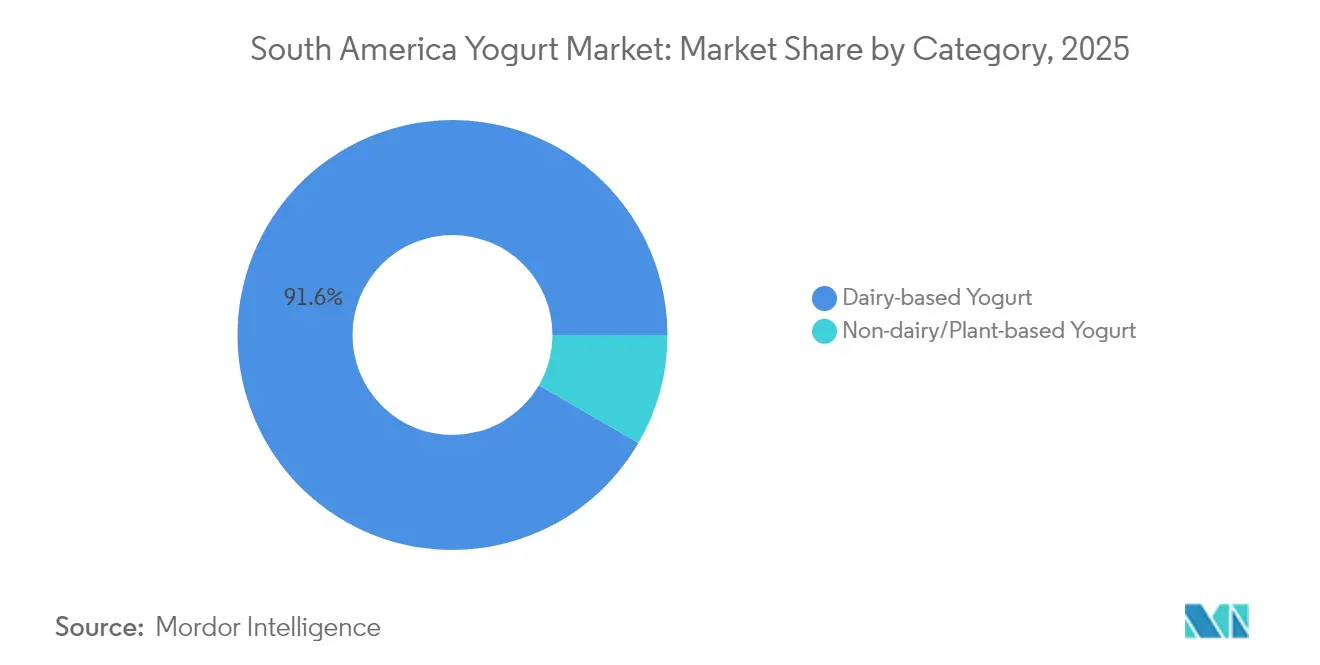

- By category, dairy-based yogurt led with a 91.62% share in 2025 in the South America yogurt market; plant-based yogurt is projected to expand at a 7.05% CAGR through 2031.

- By product form, spoonable/set yogurt held 67.55% of the South America yogurt market; while drinkable yogurt is poised for a 8.05% CAGR to 2031.

- By flavor profile, plain/natural accounted for 41.60% of the South America yogurt market in 2025; flavored posted the fastest 7.58% CAGR.

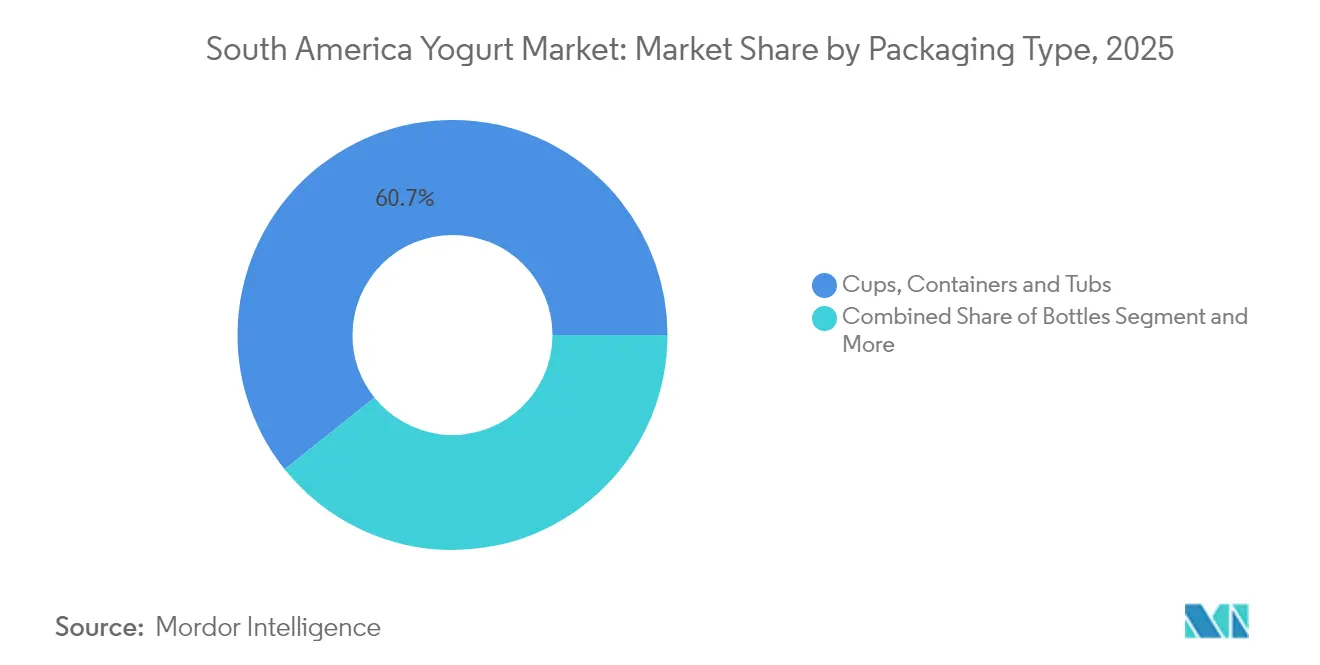

- By packaging type, cups, containers and tubs led with a 60.74% share in 2025 in the South America yogurt market; tetra packs and pouches posted the fastest 7.63% CAGR.

- By distribution channel, off-trade captured 55.20% revenue in 2025 in the South America yogurt market; on-trade are growing at a 6.44% CAGR.

- By geography, Brazil captured 62.55% of the South America yogurt market share in 2025 and Columbia is projected to record the highest CAGR at 8.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of South America Yogurt Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for functional probiotic dairy products | +1.8% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Flavor innovation using local fruits accelerating yogurt uptake | +1.2% | Brazil, Peru, Colombia | Short term (≤2 years) |

| Growth of convenience-pack drinkable yogurts | +1.5% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Cold-chain retail expansion enabling premium greek yogurt | +1.7% | Brazil, Colombia, Argentina | Long term (≥4 years) |

| Surge of flexitarians fueling plant-based yogurt | +1.0% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Growing health consciousness among consumers and increasing awareness of probiotic benefits | +1.4% | Brazil, Colombia, Argentina, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional probiotic dairy products

The functional probiotic yogurt segment is experiencing significant growth across South America, primarily driven by increasing consumer awareness of gut health benefits and immune system support. This trend is particularly evident where urban middle-class consumers demonstrate willingness to pay premium prices for products with scientifically backed health claims. The market's development is supported by regulatory frameworks, such as ANVISA in Brazil, which has established specific guidelines requiring manufacturers to provide evidence of health benefits and strain viability. This creates a competitive advantage for companies with strong research and development capabilities. In response to growing demand and the rising prevalence of digestive health issues, manufacturers are expanding their product lines and launching innovative offerings. For example, LALA introduced LALA Gold in November 2024, a premium product line featuring high-protein yogurt variants in both drinkable and spoonable formats, containing real fruit, active probiotics, and no added sugar, with protein content ranging from 20 to 25 grams per serving. As consumer interest in functional foods continues to grow and regulatory frameworks evolve, the market is expected to maintain its growth trajectory, offering opportunities for both established manufacturers and new entrants.

Flavor innovation using local fruits accelerating yogurt uptake

The incorporation of indigenous South American fruits into yogurt products is driving market growth while providing manufacturers with competitive advantages. Companies are developing varieties featuring regional fruits like açaí, guaraná, berries and passion fruit to appeal to local taste preferences and meet consumer demand for authentic flavors. The integration of these fruits enables manufacturers to differentiate their products in an increasingly competitive market landscape. Major manufacturers like Danone and Nestlé have launched products combining traditional yogurt with indigenous fruits from the Amazon region. These ingredients not only offer distinct flavors and high antioxidant content but also allow manufacturers to command premium prices while reducing transportation costs and supporting regional agricultural communities. This trend continues to expand, as demonstrated by Yasso's April 2024 launch of new frozen Greek yogurt bars featuring real fruit flavors: Strawberry Chocolate Crunch, Strawberries and Cream, and Creamy Mango. The success of these fruit-based innovations has encouraged other manufacturers to explore similar product developments, leading to increased diversification in the yogurt market.

Cold-chain retail expansion enabling premium Greek yogurt

The expansion of cold-chain retail infrastructure in South America has enabled the distribution and storage of premium Greek yogurt products across major urban centers. Supermarket chains and specialty stores are increasingly allocating dedicated shelf space for Greek yogurt due to growing consumer demand for protein-rich dairy products. The improved cold storage facilities and temperature-controlled transportation networks allow manufacturers to maintain product quality and extend shelf life, benefiting both international Greek yogurt brands entering markets in Brazil, Argentina, and Chile and local dairy companies launching their own Greek yogurt product lines. According to the Global Cold Chain Alliance, in Latin America, 40% of the food demand is driven by exports, 20% by imports for domestic consumption, and 40% by local production and distribution[1]Source: The Global Cold Chain Alliance (GCCA), "LATIN AMERICAN COLD CHAIN MARKETPLACE CONTINUES TO EXPAND," www.gcca.org . Countries like Brazil and Mexico are investing in modern cold storage facilities and logistics networks to support this market development. This ongoing investment in cold chain infrastructure positions South America as a significant growth market for premium dairy products, particularly yogurt.

Surge of flexitarians fueling plant-based yogurt

The increasing number of flexitarians in South America is driving the growth of plant-based yogurt consumption. Consumers are adopting semi-vegetarian diets while maintaining occasional meat consumption, influenced by health consciousness, environmental concerns, and lactose intolerance. Major retailers in Brazil and Argentina are expanding their plant-based yogurt offerings, while local manufacturers are developing products using regional ingredients like coconut, almonds, and soy to meet this growing demand. This dietary shift is particularly evident among urban, educated consumers who are reducing their animal product consumption without completely eliminating it. According to World Population Review, Brazil's population includes approximately 14% vegetarians and 2% vegans, indicating significant market potential for plant-based yogurt products[2]Source: World Population Review, "Country Ranking-Veganism by Country," worldpopulationreview.com. As this dietary trend continues to evolve, the South American plant-based yogurt market is expected to witness sustained growth and innovation in product development.

Restraints Impact Analysis of South America Yogurt Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile milk prices compressing dairy-based yogurt margins | –1.2% | Brazil, Argentina, Uruguay | Short term (≤2 years) |

| Import tariffs on probiotic cultures raising SME costs | –0.8% | Brazil, Argentina, Peru | Medium term (2-4 years) |

| Short shelf life and spoilage risk | –0.9% | Higher impact in rural areas region-wide | Short term (≤2 years) |

| High competition from traditional dairy products and local fermented beverages | –0.7% | Colombia, Peru, regional markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile milk prices compressing dairy-based yogurt margins

The South American yogurt market faces significant challenges due to fluctuating milk prices, which directly affect production costs and profit margins. Brazil and Argentina, the region's largest dairy producers, experience frequent price volatility in raw milk due to weather conditions, feed costs, and economic instability. These price variations force yogurt manufacturers to either absorb the increased costs or pass them on to consumers, potentially affecting demand. Additionally, the region's complex dairy supply chain and limited cold storage infrastructure contribute to higher operational costs. The situation is particularly challenging for small and medium-sized yogurt producers who have limited bargaining power with milk suppliers and restricted ability to hedge against price fluctuations.

Short shelf life and spoilage risk

The inherent perishability of yogurt products presents significant challenges across South America, where ambient temperatures and inconsistent cold chain infrastructure accelerate product degradation. Traditional yogurt maintains quality for only 20-30 days under ideal refrigeration conditions, with this window shrinking dramatically when temperature control is compromised. This short shelf life creates substantial logistical challenges, particularly for distribution to rural areas and smaller retail outlets where refrigeration may be intermittent. These constraints increase operational costs for manufacturers, who must invest in preservation technologies and temperature-controlled supply chains to maintain product quality and safety standards. Addressing these cold chain infrastructure gaps remains crucial for expanding market reach and ensuring consistent product quality across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

South America Yogurt Market Segment Analysis

By Category:

Plant-based disrupts traditional dairy dominanceDairy-based yogurt maintains its commanding position with 91.62% market share in 2025, benefiting from established consumer preferences and cultural traditions across South America. The dairy segment's dominance is reinforced by extensive distribution networks and price advantages, with production costs approximately 30% lower than plant-based alternatives. Brazil's dairy industry, which produces approximately 25.7 billion liters of milk annually, provides a stable supply base for conventional yogurt production despite occasional price volatility as per the U.S. Dairy Export Council.

Plant-based yogurt is experiencing explosive growth at 7.05% CAGR (2026-2031), driven by increasing flexitarian dietary patterns and sustainability concerns. This segment faces persistent challenges in sensory attributes, with research indicating that unexpected sourness and texture issues remain barriers to broader adoption. The Good Food Institute reports that despite challenges in the broader plant-based market, innovations in taste and texture are steadily improving consumer acceptance, with manufacturers increasingly targeting the flexitarian demographic rather than exclusively vegans

By Product form:

Convenience drives drinkable format growthIn the product form segmentation, spoonable/set yogurt maintains market leadership with 67.55% share in 2025, appealing to traditional consumption patterns and versatile usage occasions. This segment benefits from its established position as a breakfast staple and snack option across South American households, supported by innovations in premium offerings, particularly Greek-style products that deliver higher protein content and creamier textures. The segment's dominance is further reinforced by its widespread retail presence and consumer familiarity with traditional yogurt formats.

Drinkable yogurt is emerging as the market's growth driver, expanding at 8.05% CAGR (2026-2031) and steadily increasing its market share. This growth is driven by urbanization and busier lifestyles across South American metropolitan areas, where consumers prioritize on-the-go nutrition. The development of ambient yogurt technology has enhanced market penetration in tropical climates and areas with limited refrigeration infrastructure, particularly benefiting younger demographics and rural regions previously constrained by cold chain limitations.

By Flavor profile:

Local ingredients enhance premium positioningPlain/natural yogurt commands a significant 41.60% market share in 2025, maintaining its position as a market leader in South America. This dominance stems from its dual role as both a standalone product and a versatile ingredient in regional cuisine. The segment particularly resonates with health-conscious consumers who prefer lower sugar options and individuals who choose to personalize their yogurt with fresh ingredients at home. The minimal processing and absence of artificial additives in plain yogurt align with the growing consumer preference for clean-label products.

Flavored yogurt demonstrates stronger growth potential with a projected CAGR of 7.58% during 2026-2031. The segment's expansion is fueled by ongoing innovation in flavor profiles and formulations, particularly through the incorporation of indigenous South American fruits. According to research from the London School of Economics, these native ingredients not only provide unique sensory experiences but also offer enhanced functional benefits through their high antioxidant content. This strategic use of local ingredients enables manufacturers to command premium prices while reinforcing regional identity in their product offerings.

By Packaging type:

Innovation extends reach beyond urban centersCups, containers, and tubs maintain their dominance in the yogurt packaging market, holding a 60.74% market share in 2025. This traditional format's success stems from consumer familiarity and versatility across yogurt varieties, with ongoing evolution in materials and design, including sustainable alternatives to address environmental concerns. Manufacturers continue to invest in research and development to enhance the functionality and eco-friendliness of these conventional packaging formats.

The market is witnessing a significant shift with tetra packs and pouches growing at 7.63% CAGR (2026-2031). These formats offer advantages in convenience, shelf life, and reduced refrigeration needs, enabling market expansion beyond urban areas. The ambient yogurt technology, featuring 4-6 month shelf life without refrigeration, particularly appeals to younger consumers seeking portable options while addressing distribution challenges in regions with limited cold chain infrastructure. The adoption of these innovative packaging solutions is expected to accelerate as manufacturers focus on meeting evolving consumer preferences and expanding their market reach.

By Distribution channel:

Foodservice momentum challenges retail dominanceOff-trade channels maintain market leadership with 55.20% share in 2025, driven by established consumer shopping habits and home consumption preferences. This segment includes supermarkets, hypermarkets, convenience stores, and online retail platforms. The off-trade segment's dominance stems from its broad product selection, competitive pricing through bulk purchasing, and integrated shopping experiences where consumers can purchase yogurt with other groceries. However, this channel shows moderate growth potential due to market maturity and evolving consumer preferences toward experiential consumption.

The on-trade segment demonstrates robust growth potential with a 6.44% CAGR (2026-2031), exceeding the market's overall growth rate. This expansion stems from the growing foodservice sector, including restaurants, cafes, hotels, and institutional catering services. These establishments increasingly incorporate yogurt into their menus as a healthy option and ingredient for smoothies, desserts, and breakfast items. The on-trade channel serves as a primary platform for introducing new yogurt varieties, reflecting the increasing consumer interest in experiential dining across South America.

Geography Analysis

Brazil Yogurt Market

Brazil commands a 62.55% share of the South American yogurt market in 2025, supported by its large population and established dairy industry. The country's milk production is projected to reach 25.4 MMT in 2025, representing a 1.6% growth according to USDA. While the South Region exhibits above-average dairy product consumption, the North and Central West regions show lower consumption patterns. The Brazilian National School Feeding Programme (PNAE) has become a key market driver by mandating 30% of its budget for family farmer products, creating new yogurt distribution channels in underserved areas.

Colombia Yogurt Market

Colombia emerges as the region's fastest-growing market with an 8.55% CAGR (2026-2031), driven by increasing disposable incomes, urbanization, and health consciousness. However, recent health taxes on high-sugar products have led to a decrease in food processing production during 2024, prompting manufacturers to develop lower-sugar alternatives, particularly in premium segments. The market shows strong demand for high-protein and functional yogurt products.

South America Yogurt Market

Argentina's yogurt market faces challenges from economic instability and currency devaluation, affecting both production costs and consumer purchasing power. Chile benefits from free-trade agreements, enabling efficient import of specialized cultures and packaging materials, which supports the development of premium niche brands and export opportunities. Peru's market growth is primarily sustained by domestic demand and private investment, contributing to the region's diverse yogurt market landscape.

Competitive Landscape

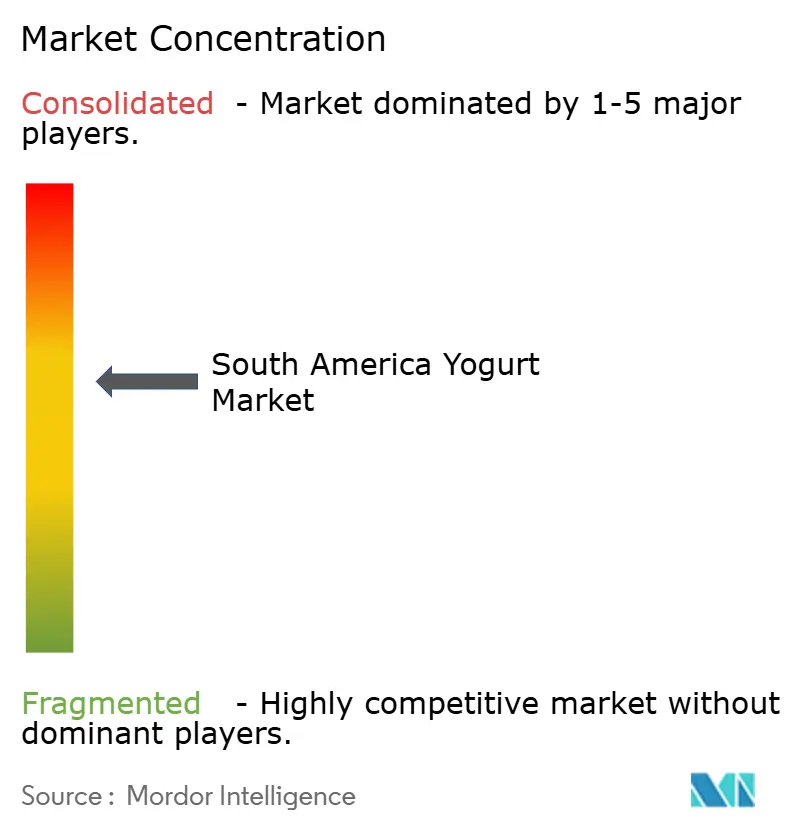

The South American yogurt market demonstrates moderate concentration, featuring a mix of global dairy corporations and established regional players. Multinational companies like Danone, Nestlé, and Lactalis utilize their extensive research and development capabilities and global supply chains to drive innovation, while regional leaders such as Grupo Lala, Alpina, and Gloria maintain strong market positions through their understanding of local preferences and robust distribution networks.

Companies are increasingly investing in premium and functional offerings, particularly in probiotic innovations and plant-based alternatives. Danone has prioritized South America for growth, expanding its Essential Dairy and Plant-Based portfolio with high-protein and children's products. In January 2024, SystemBiotech introduced a yogurt product enriched with psychobiotics, targeting mental health through gut-brain axis modulation.

The market presents significant opportunities in ambient yogurt technologies for rural distribution and affordable functional products targeting the expanding middle class. Emerging companies are differentiating themselves through local ingredient sourcing and sustainability initiatives, addressing evolving consumer preferences while creating new market segments. These market dynamics are expected to drive product innovation and market expansion in the coming years, particularly in underserved regions and consumer segments.

South America Yogurt Industry Leaders

-

Danone SA

-

Nestlé SA

-

Grupo Alpura

-

Schreiber Foods Inc.

-

Fonterra Co-operative Group

- *Disclaimer: Major Players sorted in no particular order

South America Yogurt Market Companies Covered in this Report

- Danone SA

- Nestle SA

- Grupo Alpura

- Schreiber Foods Inc.

- Fonterra Co-operative Group

- Chobani LLC

- General Mills, Inc.

- Groupe Lactalis S.A..

- Yakult Honsha Co. Ltd.

- Emmi Group

- Grupo Lala

- Laticinios Bela Vista

- Alpina Productos Alimenticios

- Sigma Alimentos (Santa Clara)

- FAGE International S.A

- Conaprole

- Tirol Alimentos

- Grupo Gloria

- Colun

- Lacteos Los Andes

Recent Industry Developments in South America Yogurt Market

- April 2025: Danone launched a new line of açaí and guaraná flavored probiotic yogurts in Brazil, leveraging locally-sourced ingredients to appeal to health-conscious consumers while supporting regional agricultural communities.

- October 2024: Laticínios Bela Vista launched a new line of plant-based yogurt alternatives in Brazil, responding to growing flexitarian consumer trends with oat and coconut-based formulations.

- June 2024: FAGE International S.A. entered the Brazilian market with its premium Greek yogurt products, initially focusing on major urban centers through import distribution channels.

- May 2024: Gloria, the Peruvian dairy company, introduced its 'Gloria Zerolacto' product line to serve lactose-intolerant consumers. The new range encompasses lactose-free milk, yogurt, and cheese products, addressing the evolving dietary requirements of consumers.

South America Yogurt Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the South America yogurt market as retail and food-service sales of spoonable and drinkable fermented dairy and plant-based yogurts whose fermentation is driven by Streptococcus thermophilus and Lactobacillus species. Frozen yogurt, kefir, buttermilk, and probiotic drinks packaged as beverages fall outside this scope.

Scope exclusion: Products labeled "fermented milk" or "yogurt drink" with viscosity below 1 Pa.s are excluded.

Segments Covered in This Report

-

By Category

- Dairy-based Yogurt

- Non-dairy/Plant-based Yogurt

-

By Product Form

- Spoonable/Set Yogurt

- Drinkable Yogurt

-

By Flavor Profile

- Plain/Natural

- Flavored

-

By Packaging Type

- Cups, Containers and Tubs

- Bottles

- Tetra Packs and Pouches

- Others

-

By Distribution Channel

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Other Distribution Channels

- On-trade

-

Off-Trade

-

By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed dairy processors, chilled-aisle buyers, cold-chain logistics providers, and nutritionists across Brazil, Argentina, Chile, Colombia, and Peru. The conversations validated penetration rates of Greek and plant-based lines, corroborated retail price ladders, and clarified planned line extensions that shape our forecast assumptions.

Desk Research

We began by collating dairy supply and utilization balances from FAO, milk output and herd data from Brazil's IBGE and Argentina's INDEC, tariff-coded import-export flows from UN Comtrade, and retail sell-out indices from Euromonitor Passport. Company 10-Ks, quarterly presentations, and trade association releases (e.g., ABIA, Camara Argentina de la Industria Lactea) helped us benchmark market shares and average selling prices. Subscription resources such as D&B Hoovers and Dow Jones Factiva supplied hard-to-find financial splits and news on capacity moves. These sources illustrate the wider pool consulted; many additional public and paid references informed data checks and context building.

Market-Sizing & Forecasting

A top-down demand pool was built by reconstructing yogurt consumption from national milk availability, trade adjustments, and typical milk-to-yogurt conversion yields, which were then cross-checked with sampled ASP x volume estimates from leading suppliers. Key variables in the model include per-capita milk intake, urban refrigerated shelf space, median yogurt retail price per kilogram, household disposable income, and probiotic claim share of new launches. Gaps in bottom-up inputs were bridged using weighted regional averages agreed upon during expert calls. Forecasts to 2030 employ multivariate regression that links the above drivers plus GDP growth to historical volume trends before applying scenario-tested price trajectories.

Data Validation & Update Cycle

Outputs pass three filters: variance tests versus historical series, peer value comparisons, and senior analyst review. We refresh models annually and trigger interim updates when currency shocks, dairy policy changes, or material M&A alter market dynamics. A final pre-publication sweep ensures clients receive the latest view.

How Mordor Intelligence's South America Yogurt Market Size Compares to Other Published Estimates

Published estimates diverge because firms choose different geographies, product mixes, and price bases. Our disciplined scope, yearly refresh, and twin-track modeling keep our baseline tightly linked to observable dairy flows and shelf prices.

Key gap drivers include competitors merging yogurt drinks with probiotic beverages, applying Latin America rather than South America geography, or inflating totals by using shipped rather than sold volumes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.89 B (2025) | Mordor Intelligence | - |

| USD 5.81 B (2024) | Global Consultancy A | Uses 2024 base and excludes Peru, leading to slightly lower pool |

| USD 8.80 B (2024) | Industry Data Service B | Combines yogurt with fermented milk and covers Caribbean markets |

| USD 9.23 B (2024) | Research Portal C | Adds probiotic drinks, so value overstates core yogurt sector |

The comparison shows that once differing scopes and product inclusions are stripped away, Mordor's balanced, transparent baseline offers decision-makers the most reproducible starting point for strategic planning.

Key Questions Answered in the Report

What is the current South American Yogurt market size?

The market stands at USD 6.25 billion in 2026 and is projected to reach USD 8.42 billion by 2031.

Which country holds the largest South American Yogurt market share?

Brazil leads with roughly 62.55% of regional revenue, supported by its large population and dairy base.

What is driving the rapid growth of plant-based yogurt in South America?

Flexitarian dietary shifts and steadily improving taste and texture are propelling plant-based options at an 7.05% CAGR.

Why are drinkable yogurts outpacing spoonable formats in growth?

On-the-go lifestyles and ambient-processing advances make drinkable yogurts more convenient for urban consumers.

How are volatile milk prices affecting the South American Yogurt industry?

Price swings squeeze smaller dairies’ margins, accelerating consolidation and prompting larger players to diversify formats.

Page last updated on: