Mining Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

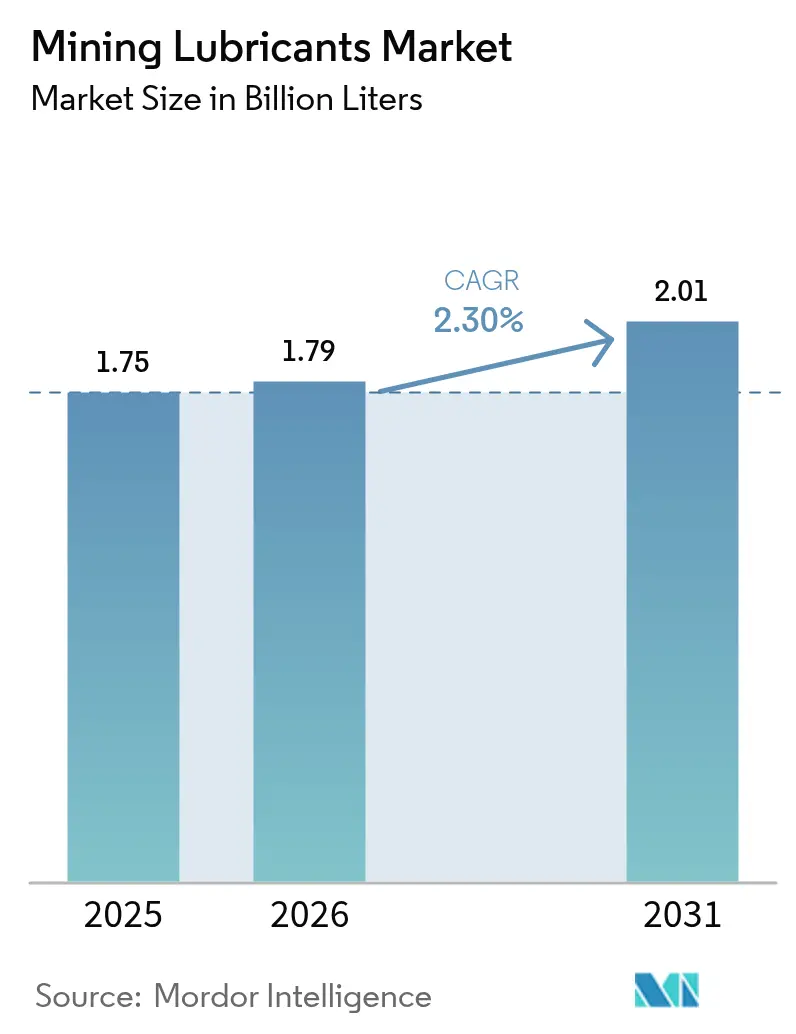

| Market Volume (2026) | 1.79 Billion liters |

| Market Volume (2031) | 2.01 Billion liters |

| Growth Rate (2026 - 2031) | 2.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

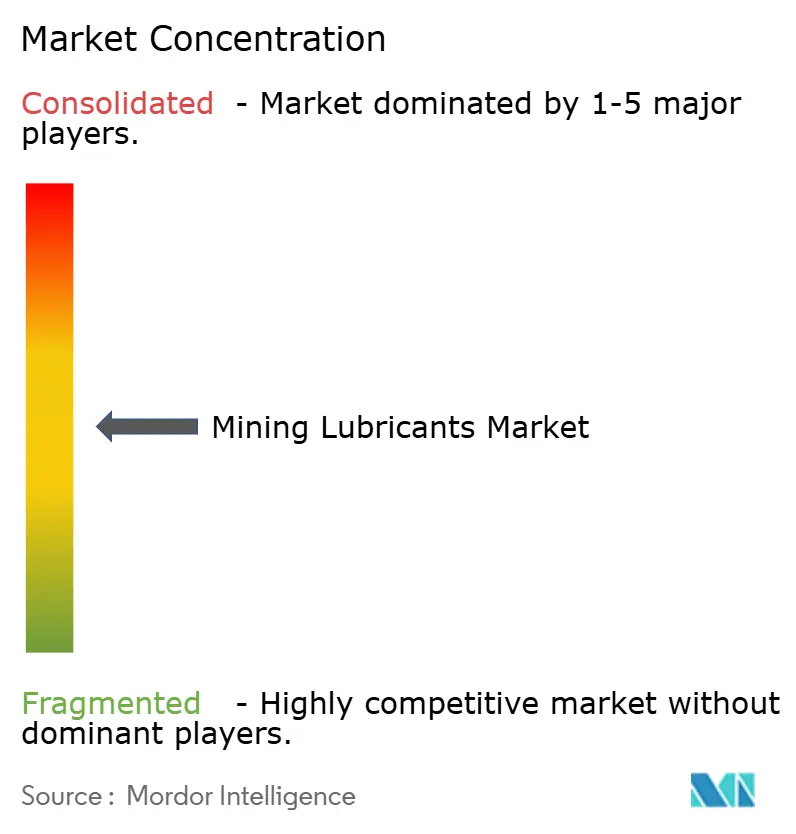

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining Lubricants Market Analysis by Mordor Intelligence

The Mining Lubricants Market size was valued at 1.75 billion liters in 2025 and estimated to grow from 1.79 billion liters in 2026 to reach 2.01 billion liters by 2031, at a CAGR of 2.30% during the forecast period (2026-2031). This steady trajectory reflects rising mining output balanced by wider use of efficient centralized lubrication systems, longer drain intervals, and premium synthetic formulations that moderate volumetric consumption. Demand is anchored in autonomous haulage fleets that require always-on, sensor-guided lubrication, while environmental rules in fragile biomes accelerate the adoption of biodegradable oils. Coal-rich mine expansions in Asia-Pacific and North America underpin baseline volumes, but real-time condition monitoring that cuts unnecessary changeouts tempers growth. Competitive strategies therefore tilt toward value-added services, predictive maintenance support, and higher-performance fluids over pure volume sales.

Key Report Takeaways

- By base stock, mineral oil commanded 66.58% of the mining lubricants market size in 2025, whereas synthetic oils record the quickest 3.03% CAGR to 2031.

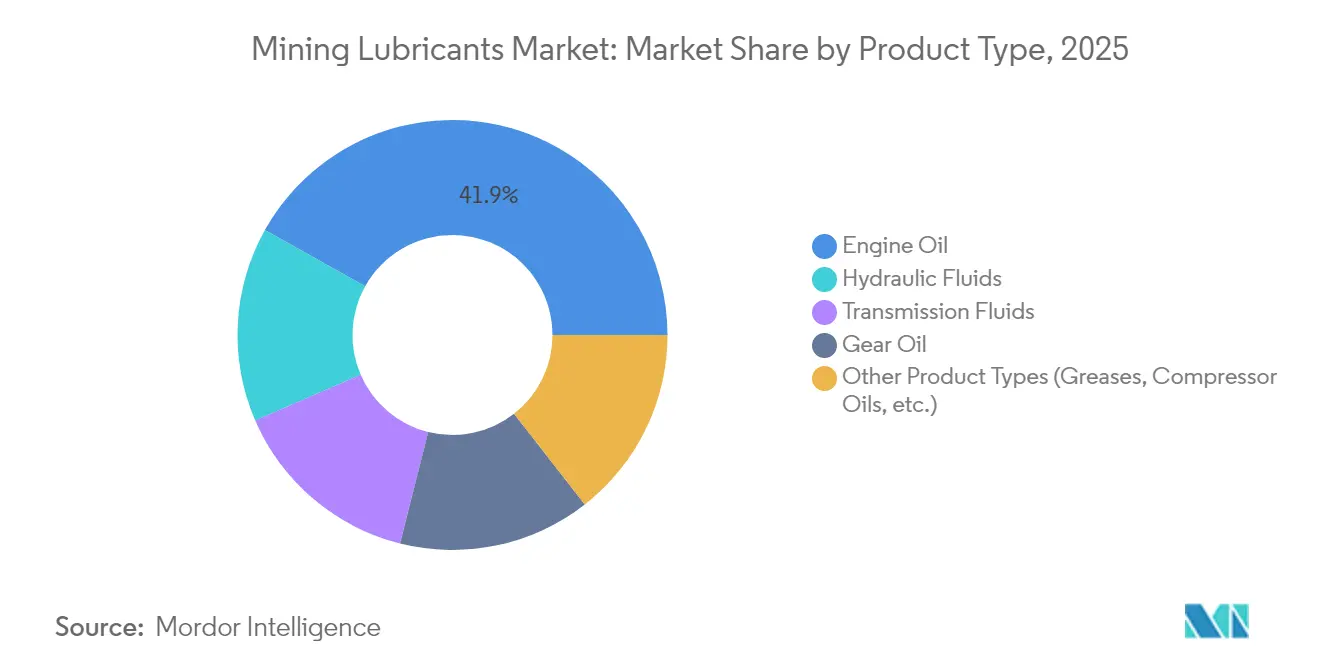

- By product type, engine oil led with 41.88% revenue share in 2025, while hydraulic and transmission fluids together advance at a 2.91% CAGR over the same period.

- By geography, Asia-Pacific held 39.28% of the mining lubricants market share in 2025; the region is projected to post the fastest 3.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mining Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of coal-rich mining activities | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rapid capacity additions in hard-rock mines | +0.6% | Global, concentrated in Australia, Chile | Medium term (2-4 years) |

| Modern, high-horsepower equipment boosting lube intensity | +0.5% | Global, led by North America, Australia | Long term (≥ 4 years) |

| Autonomous haulage requiring smart centralized lubrication | +0.4% | North America, Australia | Long term (≥ 4 years) |

| Environmental push for biodegradable lubricants in fragile biomes | +0.3% | Global, emphasis on Arctic, rainforest regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Coal-Rich Mining Activities

Coal mine expansions extend fleet operating hours and raise lubricant loads as producers in Australia, China, India, and the United States keep thermal-coal output stable despite decarbonization pressure. Australia doubled mining-sector investment to lift iron ore and coal capacity, reinforcing volume demand for heavy-duty engine oils and greases used in draglines and haul trucks[1]Reserve Bank of Australia, “Statement on Monetary Policy—Mining Investment Trends,” rba.gov.au. Canadian oil-sands production climbed to 1.9 million b/d in late-2024, and debottlenecking projects raised upgrader capacity to 600,000 b/d, spurring lubricant needs for extreme-temperature and high-contamination conditions. Bigger equipment in coal pits relies on high-performance lubricants with longer service intervals to cut unscheduled stoppages. Yet global coal demand uncertainties tied to power-sector decarbonization may cap the longevity of this driver.

Rapid Capacity Additions in Hard-Rock Mines

New copper, gold, and rare-earth pits deploy automated, high-pressure equipment operating deeper underground, intensifying lubricant complexity. Operators install sensor-laden hydraulic shovels and high-ratio gearboxes that necessitate synthetic oils with superior thermal stability. Liebherr’s zero-emission excavation roadmap, targeting fossil-free systems by 2030, illustrates the shift to electric and hybrid drive trains that still depend on tailored lubricants for transmissions and bearing sets. Predictive-maintenance platforms feed real-time friction and temperature data to optimize change intervals, reducing waste while safeguarding uptime. As hard-rock expansions proliferate in Chilean copper belts and Western Australian goldfields, specialized lubricants that manage high loads and temperature spikes command premium pricing.

Modern, High-Horsepower Equipment Boosting Lube Intensity

Ultra-class haul trucks now exceed 4,400 hp, exemplified by Cummins’ QSK95 engine, amplifying sump volumes and operating temperatures. MTU’s Series-4000 engines deliver 15% productivity gains and 12% fuel savings but demand oils with heightened oxidation resistance. Higher horsepower drives adoption of synthetic lubricants that retain viscosity and film strength under thermal shock. Equipment builders increasingly specify semi-synthetic or full-synthetic formulations, accelerating premiumization of the mining lubricants market. The need to maintain emission-compliant combustion also raises detergent and dispersant requirements in engine oils, reinforcing the technology gulf between conventional mineral fluids and advanced synthetics.

Autonomous Haulage Requiring Smart Centralized Lubrication

Driverless trucks and drills rely on automated, centralized lubrication units fitted with IoT sensors that meter precise dosages during operation. These systems remove workers from hazardous zones, enhance consistency, and allow lubrication while equipment runs, reducing downtime. Data analytics platforms analyze vibration, load, and oil-condition metrics to predict lube replenishment, extending component life and aligning service with production schedules. As mines roll out autonomous fleets in Australia’s Pilbara and Nevada’s gold belts, demand shifts toward longer-life greases and oils capable of functioning for months without manual checks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility inflating base-oil costs | -0.4% | Global | Short term (≤ 2 years) |

| Group-II base-oil supply tightness from refinery rationalization | -0.3% | Global, acute in Europe, Asia | Medium term (2-4 years) |

| Longer drain-intervals from real-time condition monitoring | -0.5% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Inflating Base-Oil Costs

Lubricant producers face margin pressure when crude prices spike since Group-II base stocks track petroleum benchmarks. Shell’s conversion of a German hydrocracker to 300,000 t/y of Group-III base oils improves regional supply resilience and trims carbon emissions by 620,000 t/y, but cost pass-throughs to mine operators remain inevitable[2]Shell Global, “Shell Converts German Hydrocracker to Base Oil Production,” shell.com. Miners offset volatility by adopting condition-based maintenance that cuts oil use, pressuring suppliers to balance pricing with value-added technical support. Premium synthetics partially hedge margin swings through higher per-liter value.

Longer Drain Intervals from Real-Time Condition Monitoring

Inline viscometers such as Cambridge Applied Systems’ SPL571 constantly measure oil degradation, allowing operators to extend drains safely and cut lubricant purchases. Predictive platforms that integrate vibration and ferrography analytics help mines avert failures and optimize oil life, with savings sometimes exceeding USD 1 million per shovel annually. While these gains elevate demand for high-performance formulations able to survive longer cycles, they also structurally curb volumetric sales, compelling suppliers to focus on service contracts and performance guarantees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Stock: Synthetic Oils Erode Mineral Dominance

Mineral oils retained 66.58% mining lubricants market share in 2025 owing to cost advantages and established supply. Synthetic variants, however, accelerate at a 3.03% CAGR to 2031 as high-horsepower machinery, deeper pits, and ambient extremes outstrip mineral capabilities. The synthetic slice of the mining lubricants market size benefits from stable viscosity, oxidation resistance, and extended drains that reduce service downtime. Chevron’s heavy-duty synthetic and semi-synthetic rollout underscores OEM endorsement for longer-life fluids that deliver fuel efficiency gains. Bio-based lubricants remain a niche but grow where environmental permits require stringent biodegradability, particularly in Arctic, Amazon, and island mines.

The premium nature of synthetics narrows the cost differential versus mineral alternatives as drain intervals stretch, improving lifecycle economics. Coupled with autonomous haulage, synthetics’ superior film retention lowers bearing failures, justifying higher upfront price and tilting procurement toward performance-based contracts that reward uptime.

By Product Type: Engine Oils Lead, Specialized Fluids Accelerate

Engine oils captured 41.88% of the mining lubricants market size in 2025 because almost all haul trucks, loaders, and shovels run high-output diesel engines. Rising horsepower and tighter NOx limits require formulations with elevated detergent, anti-wear, and soot-control properties. Cummins’ 4,400-hp QSK95 powerplant specifies low-SAPS synthetics, illustrating OEM demand for premium oils that safeguard turbocharger bearings and control liner polishing.

Hydraulic fluids and transmission oils record the briskest 2.91% CAGR to 2031 as equipment complexity escalates. Tele-remote drills and electric-drive trucks use high-precision hydraulic and gear systems that need fluids with shear-stable viscosity improvers, water-tolerance, and copper-corrosion inhibitors. Greases for centralized systems rise alongside autonomous haulage, with calcium-sulfonate complexes favored for water-wash resistance. Bio-hydraulic oils gain share in environmentally sensitive zones where spill penalties rise.

Geography Analysis

Asia-Pacific’s 39.28% mining lubricants market share in 2025 reflects massive mineral output in Australia, Indonesia, and India. Ongoing investment keeps iron-ore and coal exports flowing from the Pilbara and Kalimantan, sustaining demand despite China’s property slowdown. The Reserve Bank of Australia noted a doubling of mining capital expenditures that underpin lubricant volumes. Shell’s grease plant in Thailand tripled to 15,000 t/y, becoming Southeast Asia’s largest and anchoring regional supply. ExxonMobil’s 20,000 b/d base-oil expansion in Singapore supplies advanced EHC grades and bolsters feedstock security. While China’s import pull eases, India’s urban growth helps compensate, anchoring a 3.68% CAGR through 2031.

North America remains technologically advanced, with autonomous fleets in Canadian oil sands and US copper pits pushing uptake of IoT-linked lubrication. Shell-Whitmore’s joint venture offers turnkey reliability solutions spanning greases, oils, and automated delivery hardware, enhancing operational uptime for mine operators. Record 1.9 million b/d oil-sands production in 2024 and upgrader capacity hikes translate into steady lubricant demand across extreme cold operations. Environmental scrutiny encourages biodegradable fluids in regions adjacent to waterways, fostering niche synthetic and bio-oil uptake.

Europe’s smaller mining footprint limits volume but leads in environmental compliance, driving early adoption of EU Ecolabel-certified lubricants. Shell’s German base-oil project will meet 40% of domestic demand and 9% of EU requirements, easing Group-III supply tightness and cutting emissions. Scandinavian and Iberian mines fit advanced condition monitoring that extends drain intervals, underscoring the shift from litres sold to uptime delivered. The region’s focus on circularity and carbon cuts positions high-performance synthetics and bio-oils for growth despite sluggish overall mining output.

Competitive Landscape

The mining lubricants market features moderate fragmentation. Shell, BP (Castrol), ExxonMobil, TotalEnergies, and Chevron leverage vertical integration from base-oil refining to finished-lube blending and on-site technical services. Shell’s Whitmore venture widens rail and haulage coverage with combined grease know-how and distribution reach. BP’s review of its Castrol unit signals portfolio reshaping toward e-mobility fluids and high-margin industrial lubes. TotalEnergies expands its Quartz heavy-duty range with biodegradable variants targeting EU mines.

Technology is the chief battleground: IoT-enabled condition-monitoring platforms, cloud-based oil analytics, and biodegradable formulations create differentiation. Suppliers bundle lubricant supply with vibration analysis, training, and inventory management, shifting contracts from commodity purchases to performance guarantees. Base-oil security shapes cost leadership; ExxonMobil’s Singapore expansion and Shell’s German project both insulate operations from Group-II/III tightness, stabilizing margins and supporting premium product rollout. New entrants focusing on bio-based oils carve out specialized niches but face scale barriers in global distribution.

Mining Lubricants Industry Leaders

ExxonMobil Corporation

BP p.l.c.

Chevron Corporation

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Shell Lubricants has completed the acquisition of a 100% equity stake in Raj Petro Specialities Pvt. Ltd. from the Brenntag Group. This transaction enhances Shell Lubricants' market presence by serving customers in sectors such as mining, while also facilitating the realization of new synergies and economies of scale across the lubricants value chain.

- March 2023: ExxonMobil announced an investment of approximately INR 900 crore (USD 110 million) to establish a lubricant manufacturing facility in the Isambe Industrial Area of Raigad, under the Maharashtra Industrial Development Corporation. The plant is expected to commence operations by the end of 2025.

Global Mining Lubricants Market Report Scope

The Mining Lubricants market report include:

| Mineral Oil |

| Other Base Stocks (Synthetic Oils, Bio-based, etc.) |

| Engine Oil |

| Gear Oil |

| Hydraulic Fluids |

| Transmission Fluids |

| Other Product Types (Greases, Compressor Oils, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Base Stock | Mineral Oil | |

| Other Base Stocks (Synthetic Oils, Bio-based, etc.) | ||

| By Product Type | Engine Oil | |

| Gear Oil | ||

| Hydraulic Fluids | ||

| Transmission Fluids | ||

| Other Product Types (Greases, Compressor Oils, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Mining Lubricants Market size?

The market stood at 1.79 billion liters in 2026 and is projected to reach 2.01 billion liters by 2031.

Which region leads the mining lubricants market?

Asia-Pacific leads with 39.28% market share and is forecast to grow at a 3.68% CAGR through 2031.

Which base stock segment is growing fastest?

Synthetic oils expand at a 3.03% CAGR as high-horsepower and autonomous equipment demand longer-life, high-performance fluids.

Why are drain intervals lengthening in mining applications?

Real-time condition monitoring and predictive maintenance systems provide precise oil-health data, enabling safe extension of drain intervals and reducing lubricant waste.

Page last updated on: