South America Surfactants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

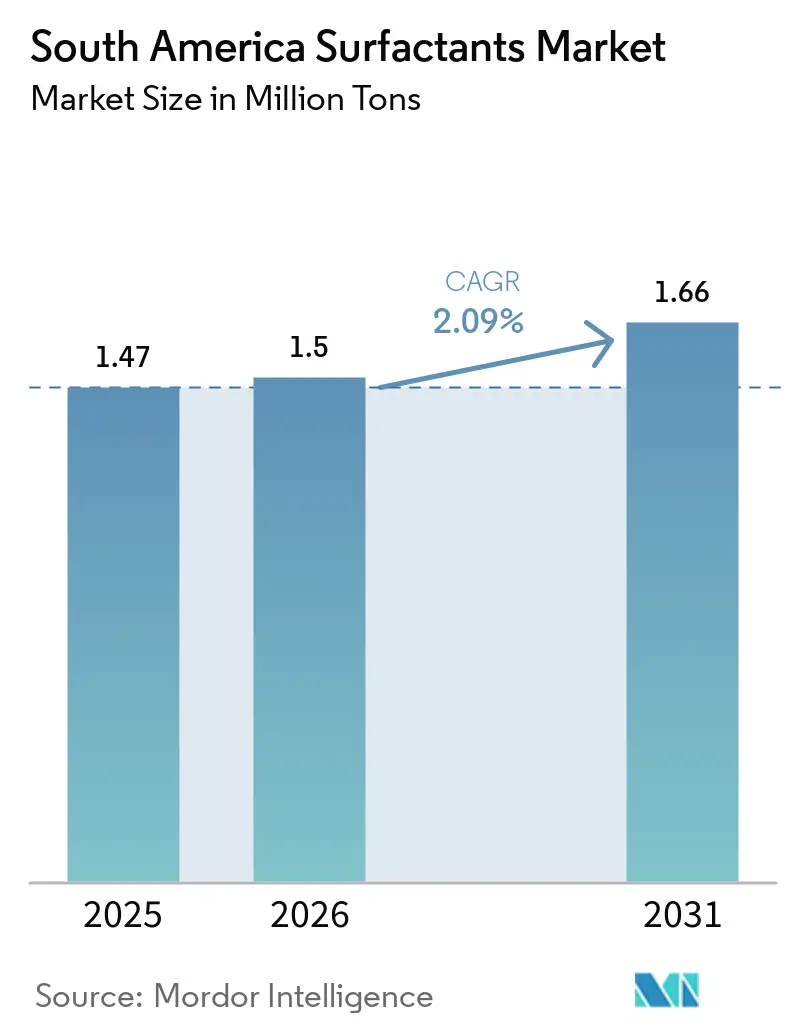

| Base Year Market Size (2025) | 1.47 Million tons |

| Market Volume (2026) | 1.5 Million tons |

| Market Volume (2031) | 1.66 Million tons |

| Growth Rate (2026 - 2031) | 2.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Surfactants Market Analysis by Mordor Intelligence

The South America Surfactants Market size is expected to grow from 1.47 million tons in 2025 to 1.5 million tons in 2026 and is forecast to reach 1.66 million tons by 2031 at 2.09% CAGR over 2026-2031. Specialty demand associated with lithium-ore flotation in Chile and Argentina is increasing anionic collector volumes. At the same time, volatility in crude-linked linear alkylbenzene sulfonate (LAS) feedstock is compressing detergent margins in Brazil and Argentina. Regulatory challenges, particularly Brazil’s January 2027 cap on alkylphenol ethoxylate (APEO) content, are prompting reformulations toward alcohol ethoxylates, cocamidopropyl betaine, and methyl ester sulfonate (MES). Additionally, bio-based tax credits under Brazil’s National Program for Green Chemistry are enhancing the cost competitiveness of oleochemical production routes, supporting steady capacity expansions in Bahia, São Paulo, and Mato Grosso. Furthermore, stricter agrochemical application standards and the expansion of soybean cultivation in Matopiba are driving increased demand for nonionic adjuvants, contributing to incremental growth in the South America surfactants market.

Key Report Takeaways

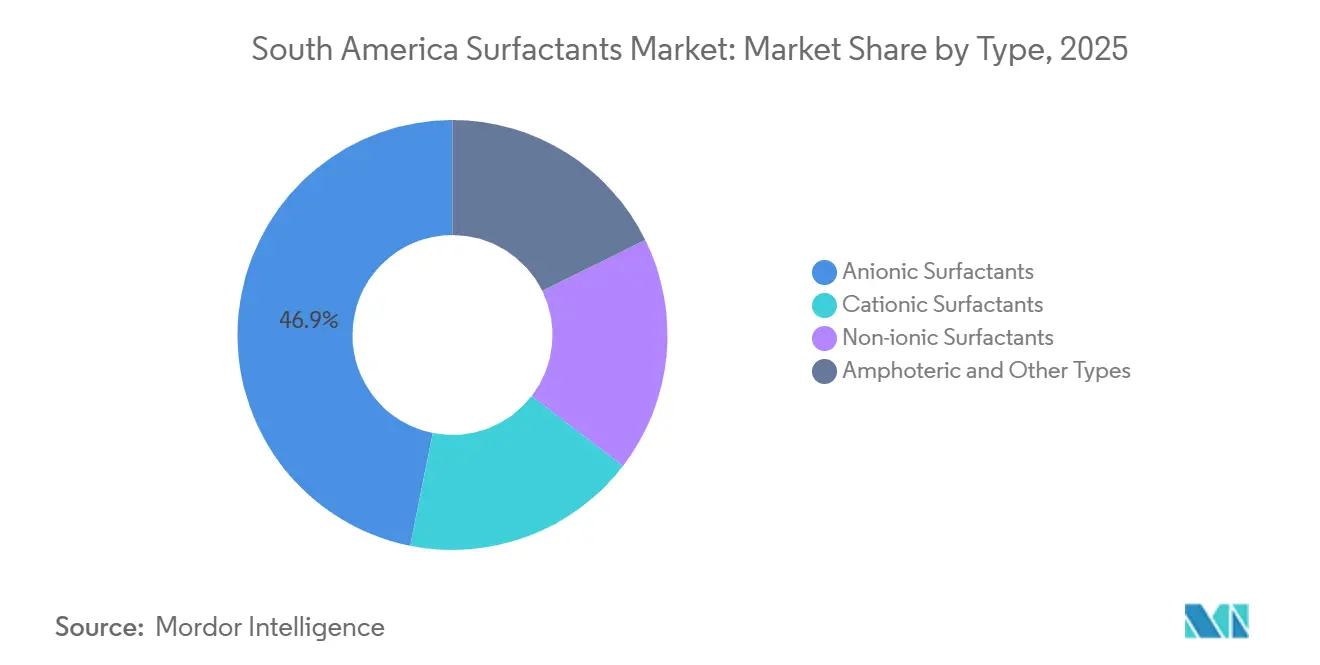

- By type, anionic surfactants held 46.85% of the South America surfactants market share in 2025, whereas amphoteric and other types are expected to advance at a 3.05% CAGR through 2031.

- By origin, synthetic grades accounted for 78.28% of the South America surfactants market share in 2025, while bio-based surfactants are expected to advance at a 3.16% CAGR through 2031.

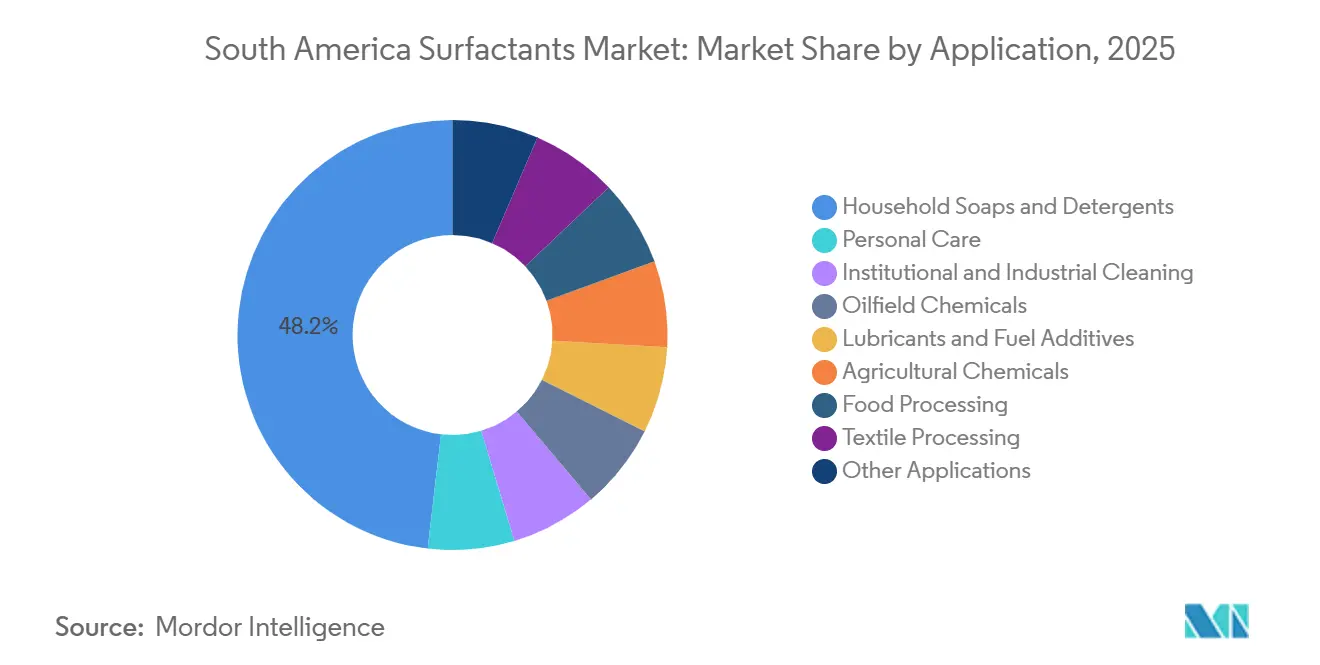

- By application, household soaps and detergents absorbed 48.17% of the South America surfactants market share in 2025, while personal care is expected to advance at a 2.95% CAGR through 2031.

- By geography, Brazil commanded 49.73% of the South America surfactants market share in 2025 and is projected to post a 2.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Surfactants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing personal and home-care consumption boom | +0.5% | Brazil, Colombia, Argentina | Medium term (2–4 years) |

| Accelerating agrochemical capacity additions | +0.4% | Brazil, Argentina, Paraguay border zones | Short term (≤ 2 years) |

| Bio-based surfactants favoured by oleochemical feedstock growth | +0.3% | Brazil (Northeast, Central-West), Argentina | Long term (≥ 4 years) |

| Lithium-ore flotation chemicals demand spike | +0.2% | Chile (Atacama), Argentina (Jujuy, Salta) | Medium term (2–4 years) |

| Brazilian "green-chem" tax incentives | +0.2% | Brazil (federal + state programs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Personal- and Home-Care Consumption Boom

Latin America’s cosmetics and personal-care sales totaled USD 24.74 billion in 2024, with Brazil alone contributing USD 9.83 billion. This growth highlights a shift toward premium products, such as liquid body washes and shampoos, over traditional bar soaps. Mild amphoteric surfactants like cocamidopropyl betaine command a 30-50% price premium over commodity LAS, ensuring price stability even amid fluctuations in crude-derived feedstock costs. Brazil’s liquid laundry detergent retail value reached USD 697.81 million in 2024, driven by urban adoption of front-loading washing machines that favor alcohol ethoxylate and Alcohol Ethoxy Sulfate (AES) systems. In Argentina, powder detergents remain dominant due to high inflation limiting appliance upgrades. Colombia and Peru exhibit mixed adoption of detergent formats across urban and rural areas, complicating distributor inventory management.

Accelerating Agrochemical Capacity Additions

Brazil’s pesticide-treated cropland expanded by 6.1% between 2023 and 2024, reaching 85 million hectares. BRANDT Consolidated invested USD 15 million in an adjuvant plant in Rondonópolis to supply alcohol-ethoxylate blends for soybean and corn crops. Argentine formulators depend on imports due to delayed greenfield investments, but revised spray-drift guidelines are driving demand for low-foam, high-temperature-stable nonionics. Brazilian regulators plan to phase out alkylphenol ethoxylates in crop-protection products by 2027, shifting demand toward fatty-amine ethoxylates and alcohol ethoxylates that meet ISO 14001 standards.

Bio-Based Surfactants Favored by Oleochemical Feedstock Growth

Brazil increased fatty-acid distillation capacity by 8% in 2024 through its integrated soybean-crushing and palm-oil chains, providing MES and fatty-alcohol feedstocks at competitive costs. Federal Law 14.754/2023 offers a 25% tax credit on capital expenditures for renewable surfactant lines verified under ASTM D6866. Indorama Ventures’ Oxiteno division processed 80,000 tons of renewable fatty alcohols in 2024, a 12% year-on-year increase, driven by demand from personal-care and institutional-cleaning segments. Argentina has potential through soybean oil, but peso devaluation and a lack of incentives hinder near-term capacity expansion.

Lithium-Ore Flotation Chemicals Demand Spike

Chile produced 234,000 metric tons of lithium carbonate equivalent in 2024, with Argentina adding 40,000 metric tons as Salta and Jujuy projects ramped[1]U.S. Geological Survey, “2025 Mineral Commodity Summary – Lithium,” usgs.gov. Anionic collectors like sodium oleate and secondary alkane sulfonate, dosed at 200-500 g/t, are essential for spodumene ore flotation at pH 9-11. Norquim’s 5,000-t/y collector plant in Antofagasta began supplying brine-resistant blends in 2024. Emerging direct-lithium-extraction circuits could add 1,500-2,000 tons of incremental surfactant demand by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening APEO and phosphorus effluent laws | -0.3% | Brazil (federal), Argentina (Buenos Aires, Córdoba) | Medium term (2–4 years) |

| Crude-oil price volatility hitting LAB feedstock | -0.4% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Regional macro-economic instability | -0.3% | Argentina, Brazil, Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening APEO and Phosphorus Effluent Laws

Brazil’s Conselho Nacional do Meio Ambiente (CONAMA), 498/2024 limits industrial effluent alkylphenol content to 10 µg/L and restricts detergent nonylphenol ethoxylate (NPE) to 0.1% by mass starting January 2027[2]CONAMA, “Resolution 498/2024 on APEO Limits,” gov.br. Argentina has added PFAS compounds to its POPs inventory and will ban PFAS-containing surfactants in firefighting foams by December 2026. Reformulating to alcohol ethoxylates and amine oxides increases raw material costs by 8%-12%, a challenge for tender-driven institutional channels.

Crude-Oil Price Volatility Hitting LAB Feedstock

Brent crude prices rose from USD 78/bbl in January 2025 to USD 95/bbl in March 2025, increasing Brazilian Linear Alkylbenzene (LAB) spot values by 22% and compressing detergent-formulator margins by up to 4 percentage points. Petrobras adjusts costs quarterly based on Brent prices and USD/BRL exchange rates, exposing buyers to currency and crude price fluctuations. Argentina’s reliance on imported LAB, priced in dollars, further amplifies cost sensitivity due to peso devaluation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Anionic Surfactants Dominance Meets Amphoteric Premiumization

Anionic surfactants accounted for 46.85% of 2025 volume, with LAS dominating due to its prevalence in powder detergents. AES and AOS contributed additional volume through liquid detergent and shampoo applications. LAS price volatility, linked to kerosene-derived linear alkylbenzene, is prompting a shift toward MES in Brazil’s Northeast, where localized oleochemical feedstocks narrow cost differences to less than USD 100/t compared to LAS. Specialty sub-segments, such as secondary alkane sulfonates in lithium flotation and sulfosuccinates in ultra-mild cleansers, offer niche but profitable opportunities.

Amphoteric surfactants and other types are projected to grow at a 3.05% CAGR through 2031, driven by personal-care brands emphasizing mildness and the phase-out of APEO co-surfactants by 2027. Nonionics, primarily alcohol ethoxylates, are transitioning from alkylphenol ethoxylates to straight-chain C12-C14 alcohol ethoxylates derived from Brazil’s oleochemical industry. Regulatory pressures and premiumization trends are gradually reshaping the South America surfactants market by type.

By Origin: Synthetic Surfactants Scale Versus Bio-Based Surfactants Momentum

Synthetic surfactants held a 78.28% share in 2025, supported by refinery-integrated LAB and ethylene-oxide value chains in Brazil and Argentina. Braskem’s Triunfo cracker ensures a steady EO supply for Oxiteno’s alkoxylation units. However, bio-based surfactants are expected to grow at a 3.16% CAGR through 2031, driven by MES capacity in Bahia, Alkyl Polyglucoside (APG) scale-up in São Paulo, and pilot biosurfactant fermenters by Croda and Evonik.

Bio-based alcohol ethoxylates benefit from 80,000 tons per year of renewable feedstocks processed by Oxiteno in 2024. Despite elevated costs, biodegradability and enzyme compatibility are driving adoption in institutional cleaning. Synthetic surfactants continue to dominate, but bio-based products are capturing incremental growth and higher margins.

By Application: Household Soaps and Detergents Anchor Volume, Personal Care Drives Growth

Household soaps and detergents accounted for 48.17% of 2025 demand, with LAS-rich powder detergents dominating in top-loading machines. However, urban households are shifting toward liquid detergents requiring alcohol-ethoxylate and AES blends, reducing powder detergent share by 2.1 percentage points in São Paulo in 2024.

Personal care is projected to grow at a 2.95% CAGR through 2031, supported by higher per-capita spending (USD 92 in Brazil in 2024) and the influence of digital-native brands. Institutional and industrial cleaning is transitioning to alcohol-ethoxylate systems due to regulatory changes, while agrochemical adjuvants benefit from expanding soybean acreage. Oilfield services remain niche but offer high value per ton, with Petrobras piloting rhamnolipids in pre-salt reservoirs. Other applications, including textiles, lubricants, and food processing, contribute to the market’s diversified end-use portfolio.

Geography Analysis

Brazil accounted for 49.73% of regional volume in 2025 and is expected to grow at a 2.30% CAGR through 2031. Federal tax incentives, integrated feedstock chains, and a large consumer base support both commodity and specialty segments. Bahia’s Camaçari hub anchors ethylene-oxide and LAB production, while Mato Grosso’s soybean expansion drives agrochemical nonionics. Liquid laundry detergent sales in São Paulo rose 8.3% year-on-year in 2024, while powder detergent volumes declined by 2.1%, reflecting a shift toward AES and alcohol ethoxylates. Regulatory tightening on APEO effluents poses challenges, but Brazil’s scale mitigates compliance costs.

Argentina faces challenges from 211% inflation and a 54% peso devaluation in 2024, which reduced real wages and delayed capital investments. YPF’s Ensenada LAB unit operates at 75% capacity, necessitating imports and exposing buyers to exchange-rate risks. The agrochemical adjuvant market, valued at ARS 3 billion (USD 3.4 million), remains price-sensitive, limiting the adoption of premium nonionics. A lack of green-chemistry incentives further restricts MES and APG capacity expansion.

Chile’s surfactant demand is driven by lithium-mining flotation chemicals, with Norquim’s Antofagasta plant supporting high-salinity brine operations. Emerging direct-lithium-extraction processes could boost specialty surfactant demand. Colombia and Peru hold minor shares, with Colombia’s rising GDP per-capita supporting personal-care adoption and Peru’s Talara basin sustaining oilfield-chemical demand. Paraguay, Uruguay, and Ecuador rely on imports from Brazil due to limited domestic production.

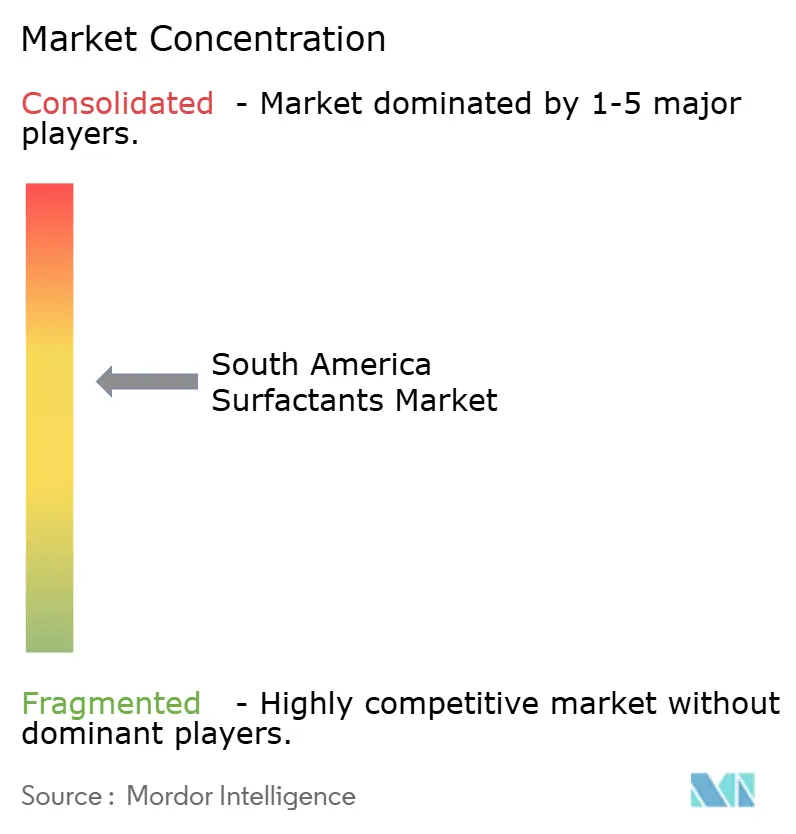

Competitive Landscape

The South America surfactants market is moderately concentrated, with BASF, Dow, Indorama Ventures Public Company Limited, Stepan Company, and Clariant as the leading players. Global companies often use tolling or joint ventures; for example, BASF partners with Deten Química for LAS supply, while Clariant outsources alcohol-ethoxylate production to Oxiteno. Mid-sized firms like Stepan Company and TENSAC focus on niche products such as amine oxides and agrochemical nonionics, leveraging formulation expertise to maintain margins.

Opportunities include lithium-flotation collectors resilient above pH 11, biosurfactants for Petrobras’ enhanced-oil-recovery pilots, and domestic APG capacity to reduce reliance on European imports. Localization of technology is increasing, as evidenced by Evonik’s 2024 methionine-derivative line in Argentina. Patent activity remains limited, indicating that logistics integration and feedstock security are more critical than proprietary molecules for competitive advantage in the South America surfactants market.

South America Surfactants Industry Leaders

BASF

Dow

Indorama Ventures Public Company Limited

Clariant

Stepan Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Brazilian government enacted an expanded tax relief regime for the country's chemical and petrochemical producers, reducing levies on key inputs by over 60%. This measure supported the surfactants market by alleviating cost pressures caused by rising feedstock prices influenced by the Middle East conflict.

- August 2025: Nouryon announced a 20% capacity expansion for sodium chlorate production in South America. This expansion was aimed at supporting the growing Brazilian pulp industry, which drives demand for surfactants used in pulp processing.

South America Surfactants Market Report Scope

Surfactants, or surface-active agents, are amphiphilic compounds composed of both hydrophilic (water-attracting) and hydrophobic (oil-attracting) components. These compounds reduce surface tension between liquids, solids, or gases. By coating dirt and oils, surfactants facilitate their mixing with water, enabling easy removal. This property makes them critical in applications such as cleaning agents, emulsifiers, dispersants, and wetting agents.

The South America Surfactants Market is segmented into type, origin, application, and geography. By type, the market is segmented into anionic surfactants, cationic surfactants, non-ionic surfactants, and amphoteric and other types. Anionic surfactants are further segmented into linear alkylbenzene sulfonate (LAS or LABS), alcohol ethoxy sulfate (AES), alpha-olefin sulfonate (AOS), secondary alkane sulfonate (SAS), methyl ester sulfonate (MES), sulfosuccinates, and other anionic surfactants. Cationic surfactants are further segmented into quaternary ammonium compounds and other cationic surfactants. Non-ionic surfactants are further segmented into alcohol ethoxylates, ethoxylated alkyl-phenols, fatty acid esters, and other non-ionic surfactants. By origin, the market is segmented into synthetic surfactants and bio-based surfactants. By application, the market is segmented into household soaps and detergents, personal care, institutional and industrial cleaning, oilfield chemicals, lubricants and fuel additives, agricultural chemicals, food processing, textile processing, and other applications. By geography, the market is segmented into Brazil, Argentina, Chile, Colombia, Peru, and the rest of South America. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Anionic Surfactants | Linear Alkylbenzene Sulfonate (LAS or LABS) |

| Alcohol Ethoxy Sulfate (AES) | |

| Alpha-Olefin Sulfonate (AOS) | |

| Secondary Alkane Sulfonate (SAS) | |

| Methyl Ester Sulfonate (MES) | |

| Sulfosuccinates | |

| Other Anionic Surfactants | |

| Cationic Surfactants | Quaternary Ammonium Compounds |

| Other Cationic Surfactants | |

| Non-ionic Surfactants | Alcohol Ethoxylates |

| Ethoxylated Alkyl-phenols | |

| Fatty Acid Esters | |

| Other Non-ionic Surfactants | |

| Amphoteric and Other Types |

| Synthetic Surfactants |

| Bio-based Surfactants |

| Household Soaps and Detergents |

| Personal Care |

| Institutional and Industrial Cleaning |

| Oilfield Chemicals |

| Lubricants and Fuel Additives |

| Agricultural Chemicals |

| Food Processing |

| Textile Processing |

| Other Applications |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Type | Anionic Surfactants | Linear Alkylbenzene Sulfonate (LAS or LABS) |

| Alcohol Ethoxy Sulfate (AES) | ||

| Alpha-Olefin Sulfonate (AOS) | ||

| Secondary Alkane Sulfonate (SAS) | ||

| Methyl Ester Sulfonate (MES) | ||

| Sulfosuccinates | ||

| Other Anionic Surfactants | ||

| Cationic Surfactants | Quaternary Ammonium Compounds | |

| Other Cationic Surfactants | ||

| Non-ionic Surfactants | Alcohol Ethoxylates | |

| Ethoxylated Alkyl-phenols | ||

| Fatty Acid Esters | ||

| Other Non-ionic Surfactants | ||

| Amphoteric and Other Types | ||

| By Origin | Synthetic Surfactants | |

| Bio-based Surfactants | ||

| By Application | Household Soaps and Detergents | |

| Personal Care | ||

| Institutional and Industrial Cleaning | ||

| Oilfield Chemicals | ||

| Lubricants and Fuel Additives | ||

| Agricultural Chemicals | ||

| Food Processing | ||

| Textile Processing | ||

| Other Applications | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the South America surfactants market?

The South America surfactants market size stood at 1.50 million tons in 2026 and is projected to reach 1.66 million tons by 2031.

Which country accounts for the largest surfactant demand in South America?

Brazil led with 49.73% of 2025 volume, driven by integrated feedstock supply chains and federal green-chemistry incentives.

Which surfactant type is growing fastest through 2031?

Amphoteric and other types are forecast to grow at a 3.05% CAGR through 2031.

How will bio-based products influence future demand?

Bio-based surfactant volumes are expected to advance at a 3.16% CAGR through 2031 as MES, APG, and biosurfactants gain fiscal support under Brazil’s National Program for Green Chemistry.

Page last updated on: