Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

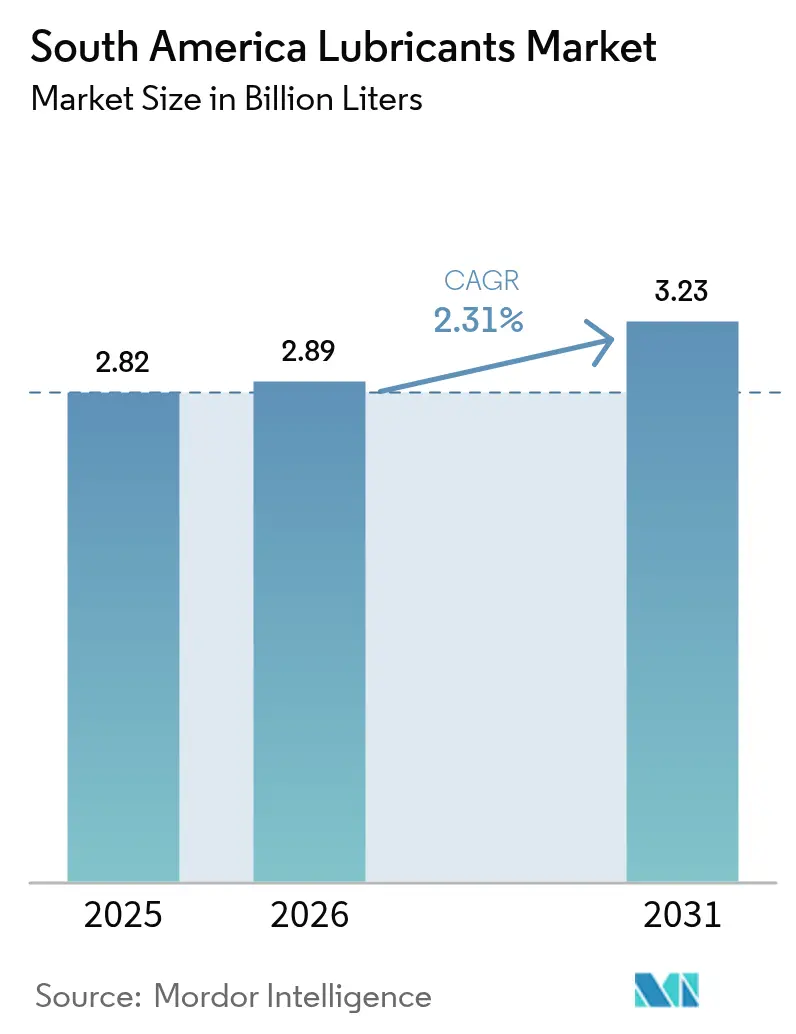

| Base Year Market Size (2025) | 2.82 Billion Liters |

| Market Volume (2026) | 2.89 Billion Liters |

| Market Volume (2031) | 3.23 Billion Liters |

| Growth Rate (2026 - 2031) | 2.31% CAGR |

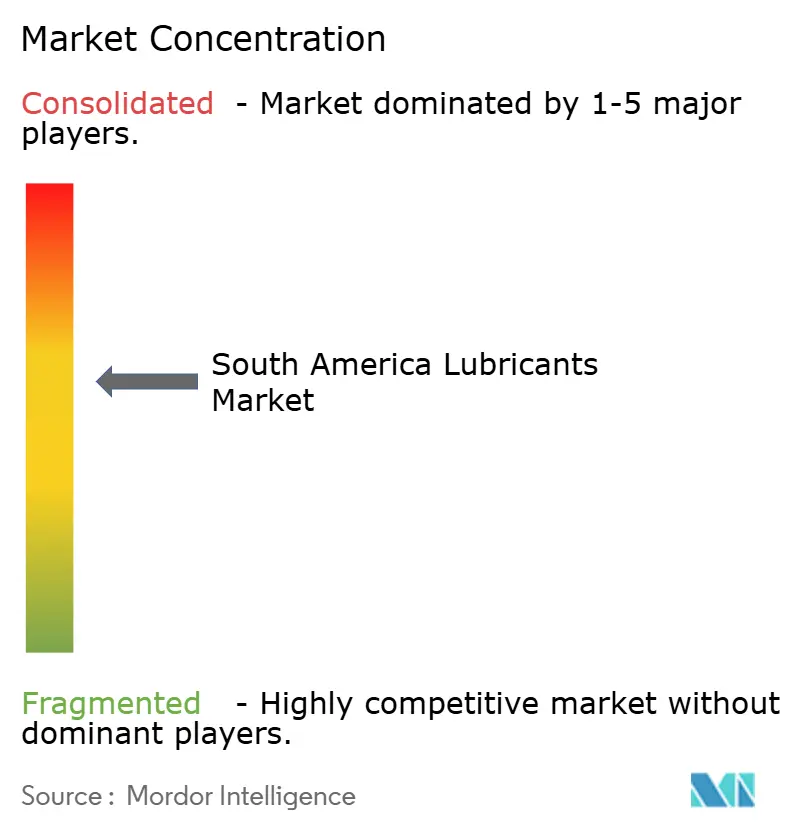

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Lubricants Market Analysis by Mordor Intelligence

The South America Lubricants Market size is expected to grow from 2.82 Billion Liters in 2025 to 2.89 Billion Liters in 2026 and is forecast to reach 3.23 Billion Liters by 2031 at 2.31% CAGR over 2026-2031. Demand is shifting toward low-SAPS synthetic lubricants as Brazil's PROCONVE P-8 emissions standards increase quality requirements. In Chile and Peru, the automation of mining fleets is driving higher consumption of long-drain gear oils, which can reduce service intervals by up to five times. Petrobras plans to invest R$33 billion in refining by 2029, including the addition of 12,000 barrels per day of Group II base-oil capacity at Reduc. This investment aims to decrease reliance on imported feedstocks and shield formulators from currency fluctuations. Hydraulic fluids are expected to benefit from Brazil's transition to B15 biodiesel in 2025, which supports bio-based formulations compatible with higher ester content. Meanwhile, the rapid adoption of electric buses in Chile and Colombia is reducing diesel-engine oil demand. However, expanding offshore drilling activities in Brazil and Guyana continue to drive demand for high-performance fluids.

Key Report Takeaways

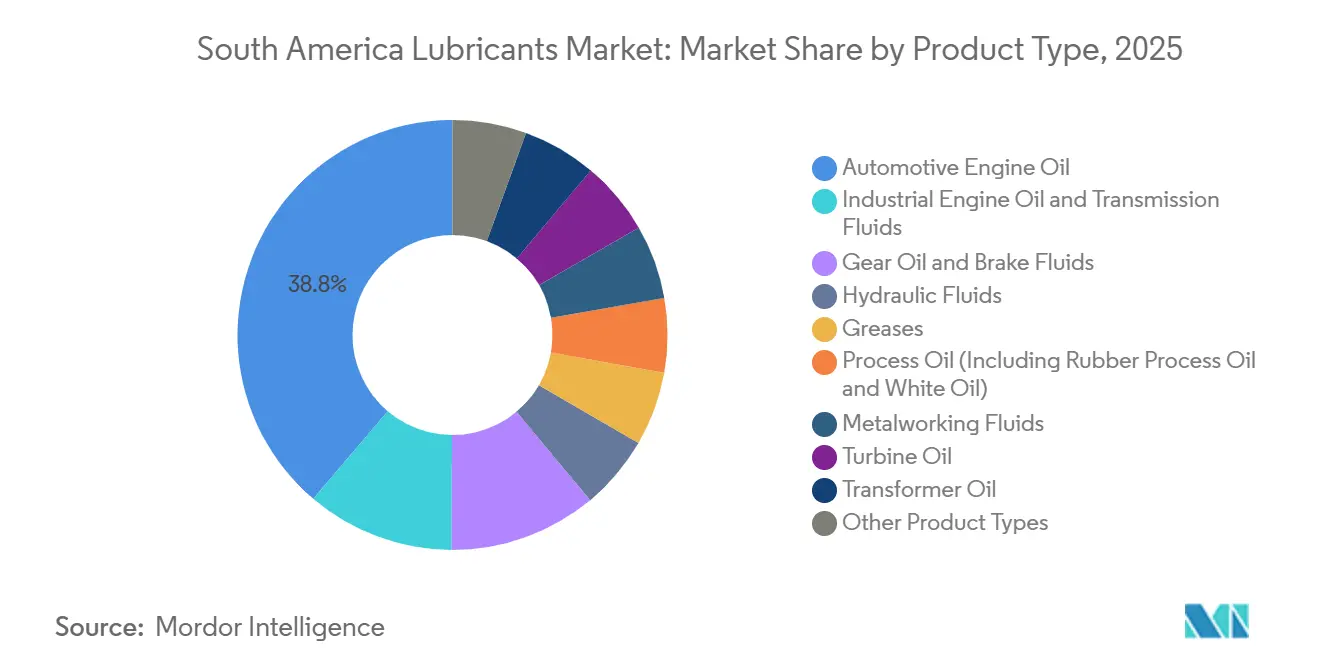

- By product type, automotive engine oil led with 39.78% of the South America lubricants market share in 2025, while hydraulic fluids are projected to record a 2.67% CAGR through 2031.

- By base-stock type, mineral oil-based lubricants accounted for 61.56% of the South America lubricants market share in 2025, whereas bio-based lubricants are forecast to advance at a 3.12% CAGR through 2031.

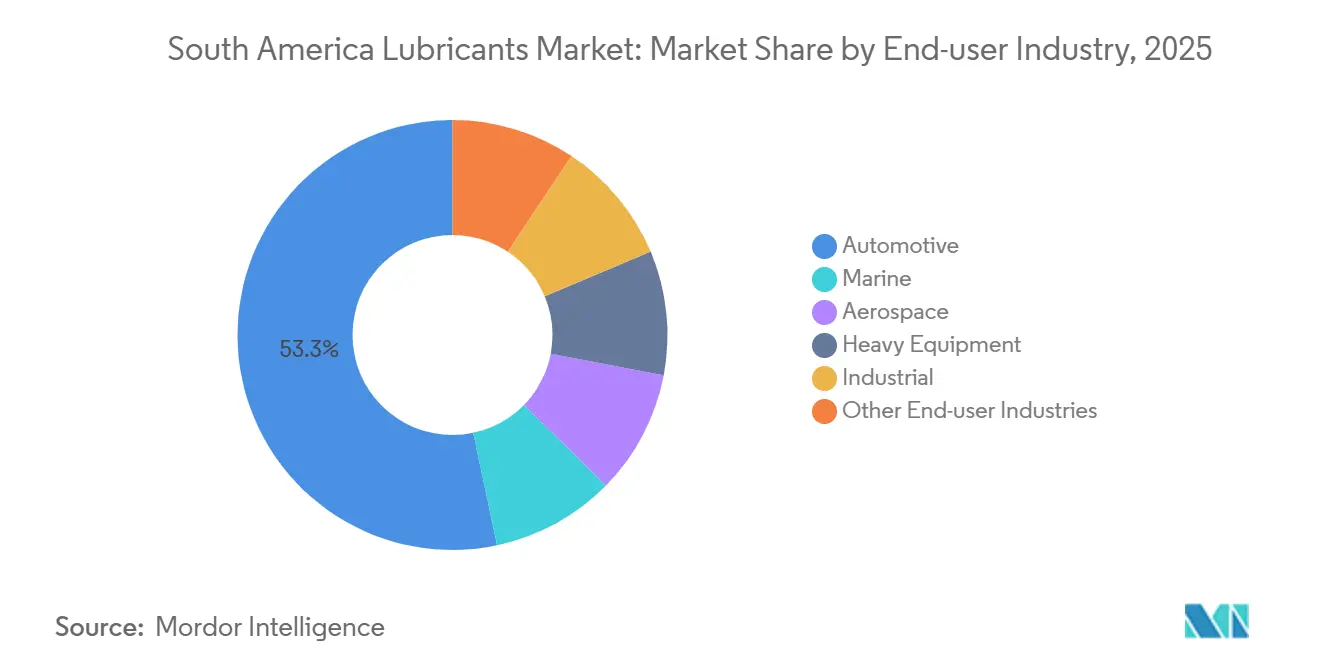

- By end-user industry, the automotive segment captured 53.32% of the South America lubricants market share in 2025; the industrial segment is set to grow at a 2.92% CAGR through 2031.

- By geography, Brazil held 47.12% of the South America lubricants market share in 2025, while Chile is projected to expand at a 2.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovering passenger-car sales boosting PCMO demand | +0.4% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Accelerated deep-water Energy and Power in Brazil and Guyana raising demand for high-performance drilling fluids | +0.3% | Brazil (Santos Basin), Guyana | Long term (≥ 4 years) |

| PROCONVE P-8 (Euro VI) phase-in driving low-SAPS engine-oil adoption | +0.5% | Brazil (national, concentrated in São Paulo, Rio de Janeiro, Minas Gerais) | Short term (≤ 2 years) |

| Surge in soybean-oil biodiesel blends spurring bio-based hydraulic fluids | +0.4% | Brazil, Argentina | Medium term (2-4 years) |

| Automation of Chile and Peru mining fleets requiring long-drain synthetic gear oils | +0.5% | Chile (Antofagasta, Atacama), Peru (Arequipa, Moquegua) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PROCONVE P-8 Phase-In Driving Low-SAPS Engine-Oil Adoption

The phase-in of the Euro VI-equivalent PROCONVE P-8 regulation is driving increased demand for low-SAPS engine oils, which are critical for safeguarding after-treatment hardware. Petrobras plans to expand Group II base-oil capacity by 2029, reducing Brazil's 74% dependency on imports and stabilizing costs that had risen during the 2024-2025 period of currency fluctuations. This enhanced domestic supply will also enable Brazilian blenders to export compliant products to Mercosur countries, considering similar standards. In 2025, FUCHS inaugurated a 50,000-ton Sorocaba plant to cater to this premium segment, emphasizing the rapid shift toward higher-quality lubricants[1]FUCHS Group, “Grand Opening of Sorocaba Plant,” fuchs.com. The combination of local feedstock availability and new blending facilities strengthens the outlook for synthetic passenger-car and heavy-duty oils in the South America lubricants market.

Accelerated Deep-water Energy and Power in Brazil and Guyana Raising Demand for High-Performance Drilling Fluids

Petrobras approved new FPSOs for the Búzios field and awarded an USD 800 million integrated-drilling contract to SLB in 2024, increasing the demand for synthetic-based fluids capable of withstanding 150 °C reservoir temperatures. Exxon Mobil achieved production of 650,000 barrels per day in Guyana by late 2025, utilizing advanced muds with high-pressure stability. These fluids, which can cost up to four times more than mineral-based formulations, remain a small portion of total well costs, prompting operators to prioritize performance over price. TotalEnergies increased its operated stake in the Lapa field to 48% in 2025, further driving demand for specialty lubricants. Continued offshore investments provide a multi-year growth trajectory for the South America lubricants market.

Surge in Soybean-Oil Biodiesel Blends Spurring Bio-Based Hydraulic Fluids

Brazil transitioned to B15 biodiesel in August 2025 and is targeting B20-B25 by 2028, while Argentina aims for B15 by 2027. The higher ester content in these blends is prompting OEMs to specify HEES-grade hydraulic fluids to ensure seal compatibility. Regional blenders benefit from cost advantages due to the availability of soybean and palm oil, enabling ISO 15380 compliance without relying on imported additives. Colombia directs 44% of its palm oil production to biodiesel, enhancing feedstock availability. This local supply advantage allows producers to offer bio-based fluids at competitive prices and pursue EU Ecolabel certification for exports, accelerating the adoption of bio-based lubricants in the South America lubricants market.

Automation of Chile and Peru Mining Fleets Requiring Long-Drain Synthetic Gear Oils

Chile increased copper production by 6% in 2025 to 5.73 million tons, while Peru has a US $64 billion mining project pipeline, both incorporating autonomous haul trucks for continuous operations. Synthetic gear oils extend drain intervals from 1,000 to up to 5,000 hours, reducing downtime and delivering 20-30% annual lubricant cost savings despite 50-80% price premiums. In 2025, FUCHS partnered with REMSAC in Peru to directly service these requirements at mine sites. The reliability and compatibility of long-drain synthetics with predictive maintenance systems position them as a key growth driver in the South America lubricants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-devaluation risk inflating import cost of PAO and additive packages | -0.3% | Argentina (national), Brazil (import-dependent states) | Short term (≤ 2 years) |

| Rising penetration of electric two-wheelers eroding motorcycle-oil volumes | -0.2% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Public procurement of electric buses in Chile curbing diesel-engine-oil demand | -0.3% | Chile (Santiago, Valparaíso, Concepción), Colombia (Bogotá, Medellín) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Currency-Devaluation Risk Inflating Import Cost of PAO and Additives

In 2025, Brazil imported 74% of its base oils from the United States, and a 15-20% depreciation of the Brazilian real significantly increased the delivered costs of synthetic feedstocks. Argentina's peso devalued by over 100% against the dollar in 2024, further squeezing margins for blenders reliant on imported supplies. While Petrobras's planned Group II production stream will reduce exposure after 2028, formulators remain vulnerable in the interim. Smaller blenders without hedging mechanisms may revert to mineral oils or lose market share, potentially slowing the growth of the premium segment in the South America lubricants market.

Public Procurement of Electric Buses in Chile Curbing Diesel-Engine-Oil Demand

By August 2025, Santiago operated 3,059 electric buses, displacing approximately 120,000-150,000 liters of diesel engine oil annually. Bogotá had over 1,600 electric buses and contracted an additional 2,000 units through 2028, eliminating a similar volume of PC-11 grade oil demand. The loss of high-profile urban fleets also reduces reference accounts that lubricant suppliers rely on to secure private contracts. While electric bus drivetrains require transmission and thermal-management fluids, the per-vehicle volume is limited to 5-10 liters, dampening the outlook for commercial-vehicle lubricant categories in the South America lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hydraulic Fluids Gain Momentum

Automotive engine oil accounted for 39.78% of the market volume in 2025, supported by a substantial light-vehicle fleet. However, hydraulic fluids are anticipated to grow at the fastest rate, with a CAGR of 2.67% through 2031, driven by the increasing use of biodiesel blends and mining automation, which require ester-compatible and long-life formulations. Transmission fluids and gear oils are benefiting from synthetic advancements that extend drain intervals by three to five times in heavy equipment, a critical factor for 24-hour mining operations.

Extended-life formulations are shifting purchasing decisions from volume-based to total cost-based criteria, favoring suppliers that can validate performance data. Industrial engine oils used in generators and marine auxiliaries are also seeing growth, driven by rising electricity consumption. Specialty segments, such as metalworking fluids, are experiencing niche growth through water-based and renewable product lines, such as TotalEnergies’ Brasil Folia range[2]TotalEnergies, “Brasil Folia Metalworking Fluids,” totalenergies.com.

By Base Stock Type: Bio-Based Lubricants Leads Growth

Mineral oil-based lubricants retained a 61.56% market share in 2025 due to their lower cost. However, bio-based lubricants are leading growth, with a projected CAGR of 3.12% through 2031, supported by local soybean supply for ISO 15380 hydraulic formulations. Synthetic products, including PAO, PAG, and esters, continue to meet low-SAPS and long-drain requirements, maintaining a high-value segment within the South America lubricants market.

Petrobras plans to add 12,000 barrels per day of Group II output by 2029, providing domestic blenders with a pathway to Euro VI compliance and reducing foreign exchange exposure. Semi-synthetics remain a cost-effective option for fleets seeking partial performance improvements. The abundance of vegetable oil in the region allows local suppliers to price competitively against imported bio-esters, creating export opportunities to Europe under Ecolabel regulations.

By End-user Industry: Industrial Surges Ahead of Automotive Dominance

The automotive segment consumed 53.32% of lubricants in 2025 but is expected to lose momentum to the industrial segment, which is projected to grow at a CAGR of 2.92% through 2031. Mining is a significant driver, particularly in Chile and Peru, where copper production and project backlogs remain strong.

Marine lubricant volumes are also increasing, with Argentina’s VLSFO demand rebounding by 86% year-on-year in Q1 2025, supporting the need for cylinder and system oils for low-sulfur fuels. Additionally, heavy equipment in agriculture and construction continues to drive steady demand for hydraulic and gear oils, particularly as biodiesel mandates necessitate fluid upgrades.

Geography Analysis

Brazil accounted for 47.12% of the regional market volume in 2025, driven by vehicle production, offshore energy activities, and agribusiness machinery. Petrobras’s BRL 33 billion refining plan aims to localize premium feedstock and reduce import dependency, enabling Brazilian blenders to supply PROCONVE P-8 compliant oils to Mercosur markets. Iconic leveraged Texaco’s re-entry into fuel stations to increase lubricant volumes by 8% in 2024, highlighting the coordination between retail fuel and lubricant sales.

Chile is expected to grow at the fastest rate, with a projected CAGR of 2.88% through 2031, supported by copper production expansion and the planned retirement of coal plants, which shifts lubricant demand toward mining fleets and renewable energy infrastructure. Gulf Oil International partnered with REFAX in January 2026, aiming for a 5% market share by leveraging an established logistics network. However, Santiago’s large electric bus fleet has already reduced diesel-bus oil demand, creating a mixed outlook.

Argentina balances currency-linked cost inflation with upstream growth at Vaca Muerta. YPF’s divestment of its Brazil unit redirects capital to shale development, while new bunker hubs at San Lorenzo expand marine lubricant channels. Colombia is leveraging palm oil for biodiesel and bio-lubricants, but faces challenges in the passenger car motor oil (PCMO) segment as electric motorcycles and buses gain traction. Peru benefits from sustained lubricant demand driven by a USD 64 billion mining pipeline and direct-to-mine supply models introduced by FUCHS-REMSAC. Other South American countries offer niche opportunities for distributors targeting agricultural districts with tailored product offerings.

Competitive Landscape

The South America lubricants market is moderately fragmented, with the top five suppliers, including Petrobras, Shell, BP, TotalEnergies, and Moove, accounting for approximately 55% of the market volume in 2025. Petrobras is strengthening its upstream integration by adding Group II capacity and a 6,300-barrel-per-day re-refining unit, enhancing domestic feedstock availability and environmental credentials. Shell continues to invest heavily in offshore operations, indirectly ensuring base-oil availability for its blends.

FUCHS has invested BRL 220 million in a new plant in Sorocaba and established a 60% joint venture with REMSAC to expand its presence in mining, cement, and food industries, reflecting a focus on high-margin industrial fluids. Gulf Oil International is expanding its regional footprint through its partnership with REFAX in Chile and earlier plant acquisitions in Brazil, aiming to increase brand visibility alongside planned fuel-retail expansion.

Emerging competitors include Usiquímica, which acquired YPF’s Brazil plant and the Valvoline license, positioning itself for mid-tier dominance in the automotive segment. Technology leadership is becoming increasingly important, with ExxonMobil’s field data demonstrating three- to five-fold drain extensions in mining assets serving as a benchmark for sales strategies. Repsol launched a new global brand in 2025, aiming to double its lubricants EBITDA by 2030, signaling a focus on consolidation to improve margins. Suppliers that excel in regulatory compliance, secure local feedstock, and shift toward direct fleet service channels are well-positioned to capture a significant share of the South America lubricants market.

South America Lubricants Industry Leaders

Exxon Mobil Corporation

Shell plc

BP p.l.c

Moove NA Distribution Holdings, Inc

Petrobras

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gram Marine and LPC, in collaboration with Servi Río, successfully delivered their first marine lubricant cargo to San Lorenzo, Argentina. This milestone marked the establishment of a new supply hub for Cyclon and AVIN brands to provide premium lubricants to vessels at Argentine ports.

- May 2025: FUCHS invested over BRL 220 million (USD 39 million) to construct a new lubricant blending plant in Sorocaba, Brazil. This investment is expected to strengthen the company's position in the lubricant market and enhance supply capabilities in Latin America.

South America Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The South America lubricants market is segmented by product type, base stock type, end-user industry, and geography. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. The report also covers the market size and forecasts for lubricants in 5 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the volume of the South America lubricant market?

The South America lubricant market stands at 2.89 billion liters in 2026 and is forecast to reach 3.23 billion liters by 2031, expanding at a 2.31% CAGR from 2026.

Which product type is expected to post the fastest growth through 2031?

Hydraulic fluids are set to grow at a 2.67% CAGR through 2031 due to biodiesel adoption and mining-sector automation.

Why are bio-based lubricants expected to gain growth through 2031?

Abundant soybean and palm-oil feedstocks allow local formulators to meet ISO 15380 requirements at lower cost, driving a 3.12% CAGR through 2031 for bio-based lubricants.

Which country is forecast to be the fastest growing through 2031?

Chile leads with a 2.88% CAGR through 2031, propelled by copper-mining expansion and energy-sector transformation.

Page last updated on: