South America Olive Market Analysis by Mordor Intelligence

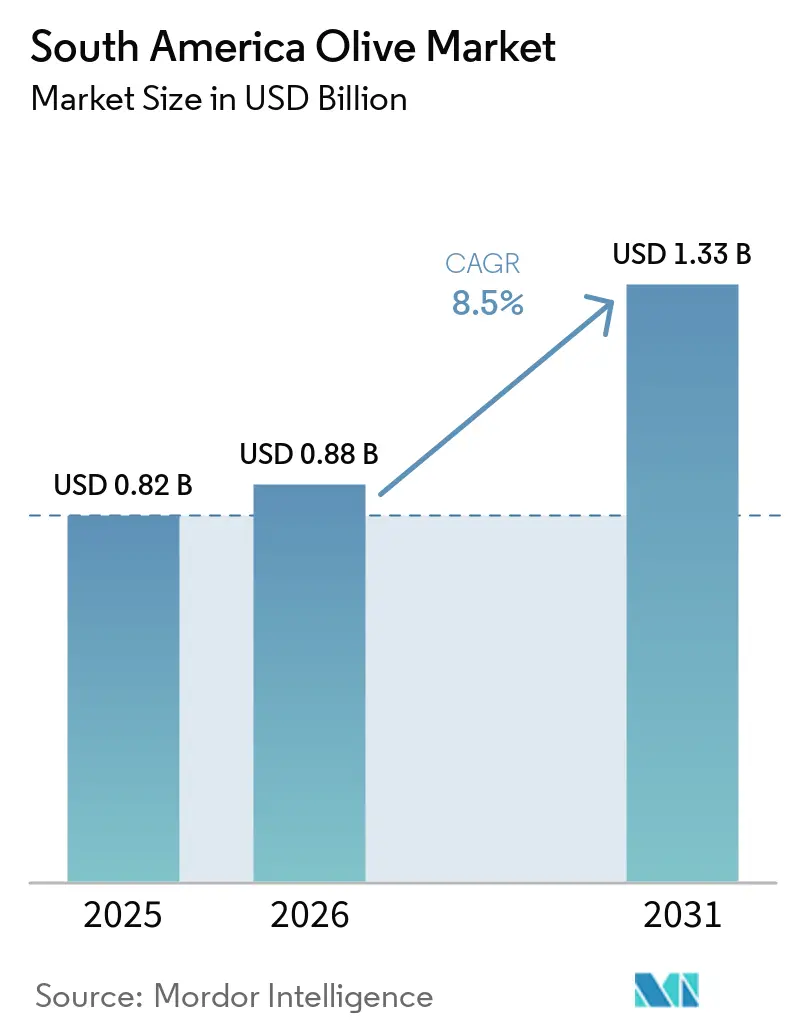

The South America olive market was valued at USD 0.88 billion in 2025 and is projected to grow from USD 0.88 billion in 2026 to USD 1.33 billion by 2031, registering a CAGR of 8.5% during 2026-2031. The market's growth is driven by increasing domestic consumption and expanding export opportunities within the region. Favorable climatic conditions facilitate consistent production cycles, ensuring a stable supply and supporting demand stability. Active regional trade flows, with neighboring markets absorbing a significant portion of the supply, further contribute to market dynamics. Governments are focusing on sustainability, quality enhancement, and sector modernization through supportive policies and industry frameworks. Additionally, the adoption of advanced agricultural practices and digital technologies is enhancing operational efficiency, optimizing resource utilization, and improving overall competitiveness in the South America olive market.

Key Report Takeaways

- By geography, Argentina accounted for the largest 38% of the South America olive market share in 2025. Whereas, Peru market size is projected to grow at the fastest 7.8% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Olive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising olive production meeting intra-regional demand | +1.8% | Argentina, Chile and Peru and spillover to Brazil demand | Medium term (2–4 years) |

| Growing demand for virgin and extra-virgin olive oil | +1.5% | Europe and North America led by Argentina and Chile | Long term (≥ 4 years) |

| Government incentives supporting orchards and drip irrigation | +1.2% | Peru, Chile and Argentina | Medium term (2–4 years) |

| Expansion of retail chains for certified table olives | +0.9% | Chile and Peru and exports to Brazil and United States | Short term (≤ 2 years) |

| Adoption of climate-resilient varieties and precision farming | +1.0% | Argentina, Chile and Peru | Long term (≥ 4 years) |

| Growth in olive-based nutraceutical products | +0.8% | North America, Europe and Asia importers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Olive Production Meeting Intra-Regional Demand

Olive production in South America is increasing in response to growing intra-regional demand. The International Olive Council reports that Argentina's table olive production reached 96,000 metric tons in 2024/25, a 17% increase compared to the previous year [1]Source: International Olive Council, “Key Figures on the World Market for Table Olives,” internationaloliveoil.org. This growth demonstrates the expansion of supply capacity as producers scale output to meet rising demand, particularly from neighboring markets. Favorable conditions and established cultivation systems have supported this production growth, solidifying South America's position as a significant supplier in olive trade.

Growing Demand for Virgin and Extra-Virgin Olive Oil

The growing demand for premium olive-based products is contributing to the expansion of the South American olive market. Increasing consumer preference for high-quality, natural, and traceable products is prompting producers to adopt improved cultivation practices and enhance quality. This focus is boosting the demand for superior-grade olives, particularly in export-driven markets. Consequently, producers in countries like Argentina and Chile are prioritizing quality differentiation and value-added production. This development enhances the olive value chain by improving price realization, increasing competitiveness, and supporting sustained market growth in the region.

Government Incentives Supporting Orchards and Drip Irrigation

Government initiatives across South America are driving the market through significant investments in irrigation infrastructure and agricultural development programs. In Peru, the government has announced a USD 24 billion investment in irrigation projects for 2025 [2]Source: Trade Council, “Peru Invests $24 Billion in Irrigation Projects,” tradecouncil.org. This initiative aims to expand agricultural land and bolster export-oriented production systems. The investment focuses on developing new farmland and improving water availability in arid regions, which are key areas for olive cultivation. These efforts enhance productivity, facilitate the adoption of efficient drip irrigation systems, and mitigate climate-related risks. Similarly, policy support in Chile and Argentina is fostering sustainable orchard expansion, collectively increasing production capacity and supporting long-term growth in the South American olive market.

Expansion of Retail Chains for Certified Table Olives

The growth of retail chains and specialty food outlets is driving demand for certified table olives by catering to changing consumer preferences for quality and transparency. According to researchers from the Universitat Politècnica de València in 2024, environmental labels and sustainability certifications on table olive products play a significant role in influencing consumer purchasing decisions. This trend is prompting producers to prioritize traceability and product differentiation, while retailers are dedicating more shelf space to premium and certified products. Consequently, branding and certification strategies are becoming increasingly important, contributing to growth in higher-value segments of the olive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climatic anomalies (El Nino and La Nina) impacting yields | -1.3% | Peru, Argentina and Chile | Short term (≤ 2 years) |

| High production costs versus imported Mediterranean olives | -0.9% | Argentina, Chile and Peru | Medium term (2–4 years) |

| Limited mechanization in hilly areas increasing losses | -0.6% | Argentina, Peru and Chile | Medium term (2–4 years) |

| Fluctuating farm-gate prices affecting smallholder profitability | -0.5% | Peru, Argentina and Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climatic Anomalies (El Nino and La Nina) Impacting Yields

Climatic anomalies, including temperature fluctuations and irregular rainfall patterns linked to El Niño and La Niña events, continue to impact the stability of olive production in South America. According to the World Meteorological Organization, an El Niño event is projected to develop from mid-2026, which is likely to influence global temperature and rainfall patterns, including critical agricultural areas. These climate variations affect precipitation distribution and increase the occurrence of extreme weather events, such as floods and droughts, across South America [3]Source: World Meteorological Organization, “WMO Likelihood Increases of El Niño,” wmo.int. This directly disrupts flowering cycles and fruit development, leading to uncertainty in yield stability and complicating harvest planning in key olive-producing regions.

High Production Costs versus Imported Mediterranean Olives

High production costs continue to be a significant restraint for the South American olive market, reducing its competitiveness compared to established Mediterranean suppliers. The region's production systems are heavily dependent on manual labor, fragmented landholdings, and lower levels of mechanization, which contribute to higher harvesting and operational expenses. Additional expenses related to irrigation, energy, and logistics further elevate the overall cost structure. In contrast, Mediterranean producers benefit from large-scale operations and advanced mechanization, resulting in lower per-unit costs. For instance, in 2024, Argentine Olive Federation indicated that rising labor and input costs continued to pressure olive producers' profit margins. As a result, exporters are increasingly focusing on premium positioning and value-added segments rather than competing on price in global markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Argentina accounted for the largest 38% of the South America olive market share in 2025. The availability of established processing, grading, and packaging infrastructure, combined with internationally recognized quality certification systems, strengthens export credibility and facilitates premium market positioning. However, climate variability, including the risk of frost, highlights the necessity for enhanced irrigation systems and the development of more resilient cultivars. Regional policy support and financing mechanisms provide operational stability, but additional investments in mechanization and cold storage are required to improve efficiency, minimize post-harvest losses, and maintain long-term competitiveness in key production regions.

Peru's market size is projected to grow at the fastest 7.8% CAGR through 2026-2031. The adoption of drip irrigation and enhanced agronomic practices is improving yield consistency in arid regions. Producers are increasingly exploring value-added opportunities, such as agritourism, to diversify income streams and reduce dependence on bulk exports. However, structural inefficiencies persist within the supply chain, particularly in farm-gate pricing, where intermediaries capture a significant share of value. Efforts to enhance transparency and provide direct market access are projected to improve producer margins and contribute to sector stability.

Chile continues to strengthen its export-oriented olive industry, benefiting from favorable climatic conditions and highly productive cultivation zones. Efficient irrigation practices and sustainability-focused initiatives are supporting long-term resource management and operational efficiency. The increasing adoption of renewable energy solutions is helping to lower production costs while aligning with environmentally conscious market demands. Producers are expanding their presence in premium retail channels and focusing on branded products, which enhances global competitiveness and reinforces Chile’s position as a reliable supplier in high-value international markets.

Competitive Landscape

The competitive landscape includes a mix of established processors and a diverse group of growers supplying raw olives. Larger companies focus on branded exports and integrated operations, while smaller producers contribute through traditional cultivation practices. The shift toward vertical integration enables companies to capture greater value across the supply chain, particularly in table olive processing, enhancing control over quality and consistency. Geographic Indication certifications support product differentiation by defining clear quality standards and origin identity, aiding premium pricing strategies in export markets.

Technological advancements are transforming competition as producers adopt precision agriculture tools and advanced quality assessment systems. Innovations in harvesting techniques, irrigation management, and digital traceability improve efficiency and product consistency. These developments enable leading players to lower operational costs and enhance margins, while smaller or less technologically advanced producers face challenges in upgrading their capabilities to remain competitive in both domestic and export markets.

Competitive intensity is rising as producers focus on brand development and premium product positioning to target higher-value segments. Companies are investing in packaging, storytelling, and origin-based marketing to differentiate their products in international markets. Strategic expansion into specialty retail channels and direct-to-consumer platforms is enhancing market reach. Success increasingly relies on the ability to integrate quality assurance, strong branding, and efficient supply chain management to sustain a competitive position.

Recent Industry Developments

- February 2026: The European Union–Mercosur trade agreement specifies that table olives exported from Mercosur countries are currently subject to a 12.8% import duty in the European Union. Under the agreement, this duty will be gradually phased out over a 7-year period.

- October 2025: The International Olive Council conducted a technical mission to Brazil aimed at strengthening cooperation, providing training, and supporting the development of the olive sector across key growing regions, enhancing production capabilities and quality standards in the country.

South America Olive Market Report Scope

Olives are small, oval-shaped fruits with a hard stone and bitter flesh that are green when unripe and bluish-black when ripe, mostly used as food and as a source of oil. The South America olive market is segmented by country (Argentina, Chile, and Peru). The report includes production analysis (area harvested, yield, and volume), consumption analysis (value and volume), import analysis (value and volume), export analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, list of key players, logistics and infrastructure, and seasonality analysis. The market forecasts are provided in terms of value (USD) and volume (metric tons) for all the above segments.

By Geography

| South America | Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | South America | Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the projected value of the South America olive sector by 2031?

It is projected to reach USD 1.33 billion, expanding at an 8.5% CAGR from 2026-2031.

Which country currently holds the largest share of regional olive revenue?

Argentina leads with the largest 38% of South America market share in 2025.

What growth rate is forecast for Peru’s olive segment through 2031?

Peru is on track for the fastest 7.8% CAGR from 2026 to 2031.

How could El Nino events influence upcoming harvests?

Warmer, wetter patterns reduce winter chill hours and increase disease pressure, which can cut yields significantly if mitigation strategies are not in place.

Page last updated on: