Market Overview

| Study Period | 2019 - 2030 |

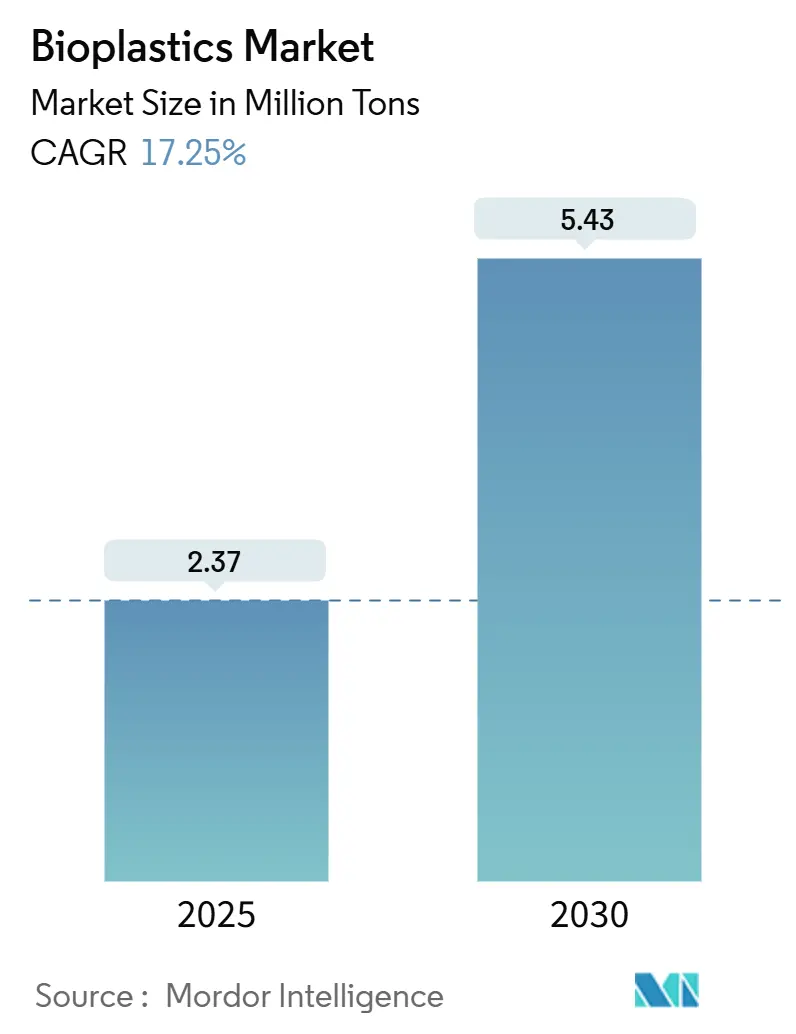

| Market Volume (2025) | 2.37 Million tons |

| Market Volume (2030) | 5.43 Million tons |

| Growth Rate (2025 - 2030) | 17.25% CAGR |

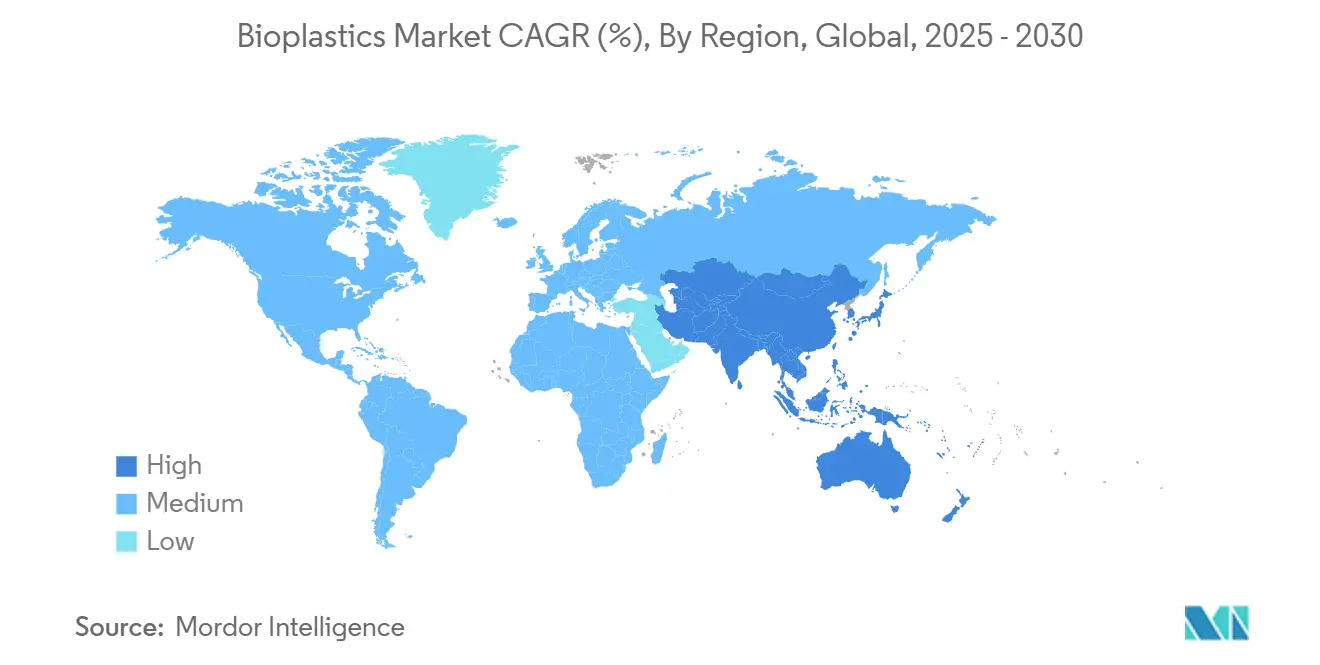

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bioplastics Market Analysis by Mordor Intelligence

The global bioplastics market size reached 2.37 million tons in 2025 and is forecast to expand to 5.43 million tons by 2030, reflecting a compelling 17.25% CAGR across 2025-2030. Rising policy pressure, stronger corporate sustainability targets, and improving feedstock flexibility collectively propel this steep trajectory, and one outcome is that brand‐owners are now budgeting for bio-based content as a line-item rather than an optional premium. A notable implication is that demand visibility is lengthening contract horizons, which underpins larger-scale capacity additions. Thus, the bioplastics industry is evolving from early-stage growth toward a more capital-intensive, industrial phase.

Key Report Takeaways

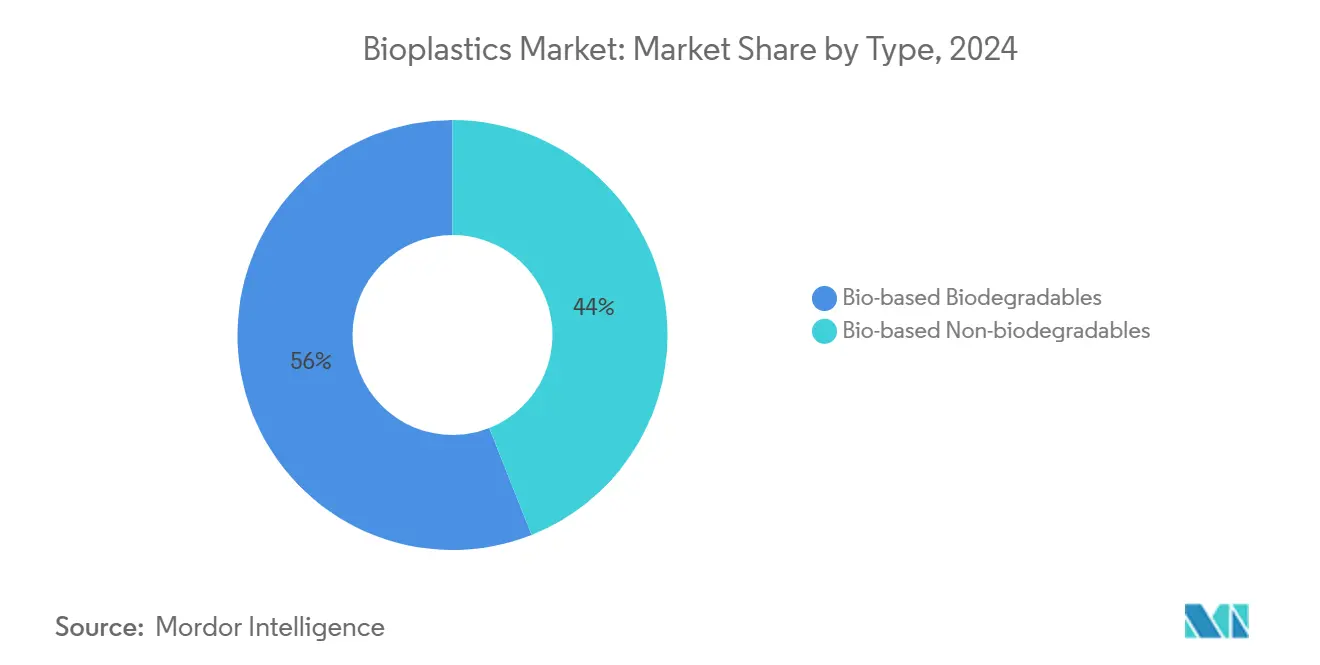

- By type, Bio-based Biodegradables accounted for the largest share, holding 56% of the total revenue in 2024, and are also expanding at a CAGR of 23.36% through 2030.

- By feedstock, sugarcane accounted for 41% of the total revenue, while cellulosic and wood waste are the fastest-growing segments with a CAGR of 24.30%.

- By processing technology, extrusion held the largest share in 2024 with 46% of the total market, while 3D printing is expanding at a CAGR of 22.80%.

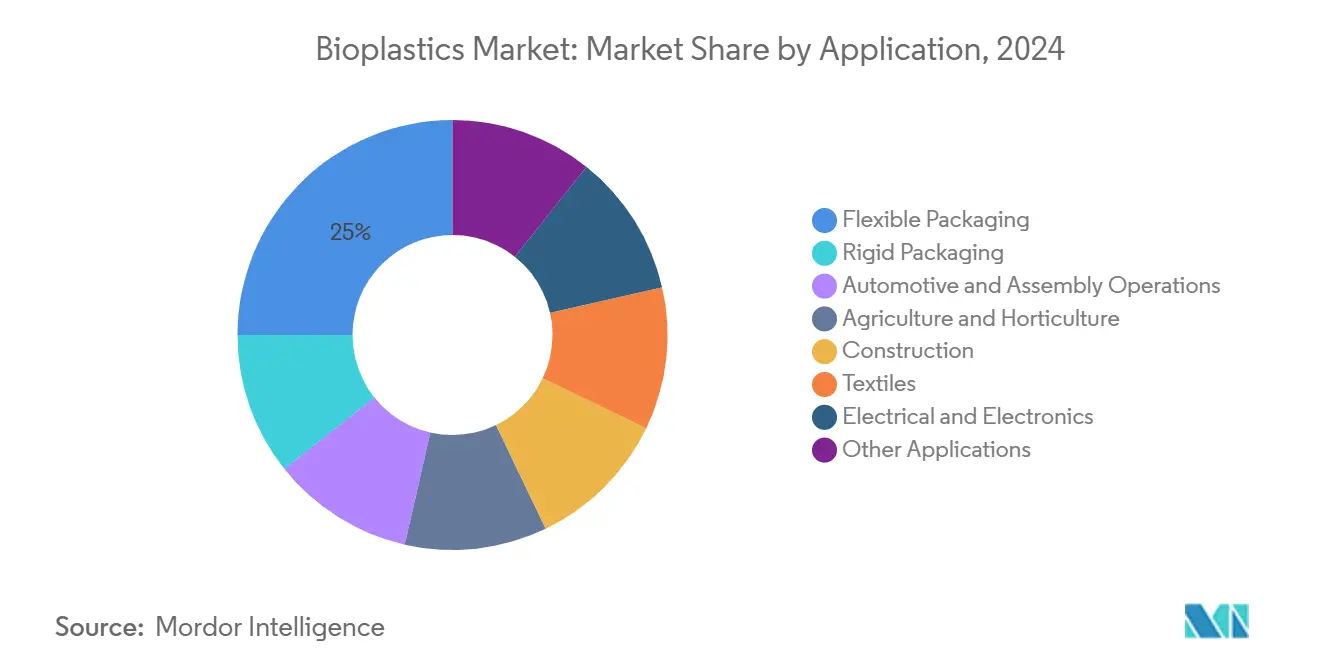

- By application, flexible packaging with a 25% share of the market in 2024, is also the fastest-growing segment with a CAGR of 24.38%.

- By geography, Asia-Pacific held the largest share in 2024 with 48% of the total market, and is growing at a CAGR of 22.47%.

Global Bioplastics Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use plastic bans | +4.2% | Europe and Asia, with spillover to North America | Short term (≤2 yrs) |

| Growing Demand in Packaging | +3.8% | Global, with a concentration in Europe and North America | Medium term (≈3-4 yrs) |

| Corporate net-zero targets | +2.5% | Global, led by multinational corporations | Medium term (≈3-4 yrs) |

| Environmental factors | +2.1% | Global, with a stronger impact in environmentally conscious markets | Long term (≥5 yrs) |

| Government procurement policies | +1.9% | Europe and India, with potential expansion to other regions | Medium term (≈3-4 yrs) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Mandate for Single-Use Plastic Bans Catalyzing Bio-Based Adoption

The PPWR takes effect in February 2025 and requires all packaging placed on the EU market to be recyclable by 2028, explicitly allowing bio-based plastics when mechanical recycling is impracticable. Producers view the rule as a demand guarantee for compostable coffee capsules, thin films, and barrier coatings where recycling economics are weak, and one immediate response has been fast-tracked certification programmes for food-contact PLA. Forward contracting for compliant material indicates that legislators are accelerating commercial timelines, and procurement teams now see regulatory alignment as a cost-avoidance strategy rather than a marketing add-on.

Growing Demand for Bioplastics in Packaging

Flexible packaging already accounts for one quarter of the overall bioplastics market size in 2024 and is projected to grow at 24.38% CAGR to 2030, making it both the largest and fastest-growing application. Brand owners cite shelf-life parity and improved sealability as decisive factors, and converters are redesigning laminates to remove aluminium layers in favour of bio-barrier coatings. This rapid uptake suggests that technical barriers once thought fundamental are now being treated as routine engineering challenges.

Corporate Net-Zero Targets Accelerating Procurement

Dow’s collaboration with New Energy Blue to source bio-ethylene from corn stover will displace roughly 1 million tons of greenhouse-gas emissions annually, demonstrating how waste-based feedstocks can help meet science-based targets. Similar moves by Braskem and SCG Chemicals in Thailand nearly double bio-PE capacity, showing that offtake security now underwrites large-scale investments. The emerging pattern is clear: corporate decarbonisation commitments are turning into binding purchase agreements that reposition bio-polymers from optional to required inputs.

Environmental Factors Encouraging a Paradigm Shift

Life-cycle assessments reveal that NatureWorks’ Ingeo PLA grades cut carbon footprints by up to 84% relative to conventional ABS, a differential large enough to impact corporate scope-3 calculations[1]NatureWorks, "NatureWorks’ Ingeo PLA Manufacturing Expansion Attracts Record Financing from Krungthai Bank PCL of Thailand," www.natureworksllc.com. Manufacturers note that such quantified performance strengthens the internal business case for transitioning to circular feedstocks. As a result, environmental metrics are becoming contract deliverables rather than marketing collateral.

Restraint Impact Analysis

| Restraints | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheaper alternatives | -3.5% | Global, with higher impact in price-sensitive markets | Short to Medium term (≤4 yrs) |

| Performance gap in high-heat applications | -2.1% | Global, particularly in the automotive and industrial sectors | Medium term (≈3-4 yrs) |

| Volatile sugarcane prices | -0.9% | Brazil, Thailand, and other sugarcane-producing regions | Short term (≤2 yrs) |

Source: Mordor Intelligence

Availability of Cheaper Alternatives

Price-sensitive buyers in developing regions still opt for petro-plastics, yet rising landfill levies and emerging carbon taxes are eroding the headline price gap. Distributors observe that when extended producer responsibility fees are included, the total landed cost difference narrows further, especially for lightweight packaging. Consequently, economic tipping points vary by jurisdiction, indicating that cost parity is as much a policy question as a technology challenge.

Performance Gap of Bio-PET vs. Petro-PET in High-Heat Applications

Bio-PET currently trails its fossil counterpart in sustained temperature resistance, limiting use in automotive under-the-hood parts. However, research and development into controlled branching of polymer chains is closing this gap, and early prototypes are now passing 120 °C stress tests. This progress implies that segment-specific engineering, rather than blanket substitution, will unlock fresh demand pools.

Segment Analysis

By Type: Bio-Based Non-Biodegradables Lead While Biodegradables Surge

Bio-based non-biodegradable plastics hold 56% bioplastics market share in 2024, largely due to Bio-PET and Bio-PE grades that fit straight into existing melt lines. Their dominance stems from performance familiarity, allowing brand owners to meet climate targets without re-engineering equipment. Nonetheless, the market shows a clear pivot toward biodegradable PLA and PHA, which log a forecast of 23.36% CAGR through 2030. As certification bodies clarify compostability standards, buyers increasingly segment applications by end-of-life outcome rather than by resin family alone.

Demand for biodegradable grades is moving fastest in food-service items, where mandated organic-waste streams favour compostable products. A practical takeaway is that material selection now factors in local waste infrastructure as much as mechanical properties. This dynamic suggests that regional policy divergences will shape future resin mixes, with certain cities prioritising composting and others doubling down on recycling.

Note: Segment shares of all individual segments available upon report purchase

By Feedstock: Cellulosic Innovations Challenging Sugarcane Dominance

Sugarcane and sugar beet supply 41% of total feedstock in 2024, offering reliable conversion routes to bioethanol and thereafter to bio-ethylene or PTA. Yet, cellulosic and wood waste inputs are climbing at 24.30% CAGR, and Origin Materials’ commercial line converting forest-sector residue to intermediates underscores that non-food biomass is viable at scale.

Stakeholders note that multi-feedstock flexibility also hedges against supply shocks; if sugar yields falter, mills maintaining both bagasse and agricultural residue routes can redirect quickly. Such optionality is becoming an investment criterion in new plant design, pointing to a more resilient supply ecosystem.

By Processing Technology: 3D Printing Disrupts Traditional Methods

Extrusion retains 46% bioplastics market size in processing technologies, given its ubiquitous role in film and sheet lines. Injection moulding follows closely for rigid goods, yet 3D printing is the headline growth story at 22.80% CAGR through 2030. A University of Birmingham team recently developed a recyclable bio-based photopolymer that can be printed, depolymerised, and reprinted, signalling a move toward closed-loop additive manufacturing[2]University of Birmingham, "Bio-based resins could offer recyclable future for 3D printing," www.birmingham.ac.uk.

Material suppliers now tailor PLA and PHA filament grades for long-run thermal stability, which reduces warping and broadens usable part geometries. This synergy between resin chemistry and printer hardware reflects a maturing ecosystem where process and material development proceed in tandem.

By Application: Flexible Packaging Leads Market Transformation

Flexible formats capture 25% bioplastics market share in 2024 and are predicted to post 24.38% CAGR, making them a double engine of scale and speed. High barrier films using micro-layer co-extrusion achieve shelf-life parity with fossil multilayers, which has convinced cautious food brands to pilot full-scale rollouts. The learning curve now focuses on seal strength under variable humidity, a hurdle that recent bio-PE blends are starting to overcome.

The application palette is broadening. UPM, Selenis, and Bormioli Pharma have launched a wood-based polymer pharmaceutical bottle, illustrating that regulated sectors are entering the fray. Such high-value niches can carry premium pricing, which in turn cross-subsidises volumes for mass-market flexible pouches.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia accounted for 48% of the global bioplastics market size in 2024 and is on track for a 22.47% CAGR, effectively solidifying its leadership position each year. Thailand’s new bio-ethylene complex, backed by Braskem and SCG Chemicals, nearly doubles regional bio-PE output and provides local converters with a stable domestic source. Financial incentives from several Asian governments accelerate plant approvals, and abundant agricultural residue streams reduce feedstock risk. These advantages encourage vertically integrated clusters that cut logistics costs and tighten supply chains.

Europe differentiates itself through stringent circular-economy regulations. The PPWR’s recyclability mandate and national plastic taxes create a price signal favoring compostable and mechanically recyclable biopolymers. Companies are responding with innovations such as Futerro’s RENEW PLA, which is fully recyclable through the LOOPLA process, offering an end-of-life route that aligns with EU objectives.

North America lags in absolute volume but shows momentum in advanced bio-polyesters and PHAs. Corporate sustainability goals, rather than national regulation, drive adoption, and the prevalence of private-sector initiatives yields a diverse portfolio of pilot plants. The

Competitive Landscape

The bioplastics industry exhibits a highly consolidated structure, with legacy petrochemical majors and pure-play biopolymer companies forming two strategic clusters. Firms like BASF and Arkema tap existing supply networks to produce drop-in resins, leveraging scale to negotiate feedstock contracts. Pure-play leaders like NatureWorks and TotalEnergies (Total Corbion) specialise in PLA and maintain focused research and development pipelines, differentiating through technical depth rather than portfolio breadth.

Bioplastics Industry Leaders

-

BASF

-

TotalEnergies (Total Corbion)

-

NatureWorks LLC

-

Eni S.p.A. (Novamont)

-

Braskem

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Braskem and SCG Chemicals established Braskem Siam Company Limited to produce bio-ethylene from bioethanol in Thailand. The venture will almost double I’m green bio-based polyethylene capacity, positioning Asia to capture incremental demand.

- May 2024: NatureWorks LLC secured USD 350 million financing from Krungthai Bank for a new Ingeo PLA facility in Thailand. The plant will deliver 75,000 tons of annual capacity and is slated for commissioning in 2025.

Global Bioplastics Market Report Scope

Bioplastics are produced from renewable sources, such as corn starch, vegetable fats and oils, woodchips, straw, recycled food waste, sawdust, and other sources. The market is segmented by type, application, and geography. By type, the market is segmented into bio-based biodegradables and bio-based non-biodegradables. By application, the market is segmented into flexible packaging, rigid packaging, automotive and assembly operations, agriculture and horticulture, construction, textiles, electrical and electronics, and other applications. The report also covers the market size and forecast for the bioplastics market in 15 countries across major regions. For each segment, the market sizing and prediction have been made based on volume (kiloton).

| By Type | Bio-based Biodegradables | Starch-based | |

| Polylactic Acid (PLA) | |||

| Polyhydroxyalkanoates (PHA) | |||

| Polyesters (PBS, PBAT, PCL) | |||

| Other Bio-based Biodegradables | |||

| Bio-based Non-biodegradables | Bio Polyethylene Terephthalate (PET) | ||

| Bio Polyethylene | |||

| Bio Polyamides | |||

| Bio Polytrimethylene Terephthalate | |||

| Other Bio-based Non-biodegradables | |||

| By Feedstock | Sugarcane / Sugar Beet | ||

| Corn | |||

| Cassava and Potato | |||

| Cellulosic and Wood Waste | |||

| Others (Algae and Microbial Oil) | |||

| By Processing Technology | Extrusion | ||

| Injection Molding | |||

| Blow Molding | |||

| 3D Printing | |||

| Others (Thermoforming, etc.) | |||

| By Application | Flexible Packaging | ||

| Rigid Packaging | |||

| Automotive and Assembly Operations | |||

| Agriculture and Horticulture | |||

| Construction | |||

| Textiles | |||

| Electrical and Electronics | |||

| Other Applications | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Netherlands | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| South Africa | |||

| Egypt | |||

| Kenya | |||

| Rest of Middle-East and Africa | |||

By Type

| Bio-based Biodegradables | Starch-based |

| Polylactic Acid (PLA) | |

| Polyhydroxyalkanoates (PHA) | |

| Polyesters (PBS, PBAT, PCL) | |

| Other Bio-based Biodegradables | |

| Bio-based Non-biodegradables | Bio Polyethylene Terephthalate (PET) |

| Bio Polyethylene | |

| Bio Polyamides | |

| Bio Polytrimethylene Terephthalate | |

| Other Bio-based Non-biodegradables |

By Feedstock

| Sugarcane / Sugar Beet |

| Corn |

| Cassava and Potato |

| Cellulosic and Wood Waste |

| Others (Algae and Microbial Oil) |

By Processing Technology

| Extrusion |

| Injection Molding |

| Blow Molding |

| 3D Printing |

| Others (Thermoforming, etc.) |

By Application

| Flexible Packaging |

| Rigid Packaging |

| Automotive and Assembly Operations |

| Agriculture and Horticulture |

| Construction |

| Textiles |

| Electrical and Electronics |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Kenya | |

| Rest of Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected bioplastics market size by 2030?

The bioplastics market size is expected to reach 5.43 million tons by 2030 under current growth assumptions.

Which region holds the largest bioplastics market share?

Asia leads with 48% market share in 2024, supported by rapid capacity expansion and favourable policy incentives.

What feedstock category is growing the fastest in the bioplastics industry?

Cellulosic and wood waste feedstocks show the fastest growth, driven by technological advances that enable conversion of non-food biomass.

Why is flexible packaging important for bioplastics demand?

Flexible packaging combines high turnover and consumer visibility, making it both the largest application segment and the fastest-growing use case.

How do corporate net-zero targets influence the bioplastics market?

Large brands lock in bio-based procurement contracts to meet decarbonisation goals, creating predictable demand that supports new plant investments.