South Africa Seed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

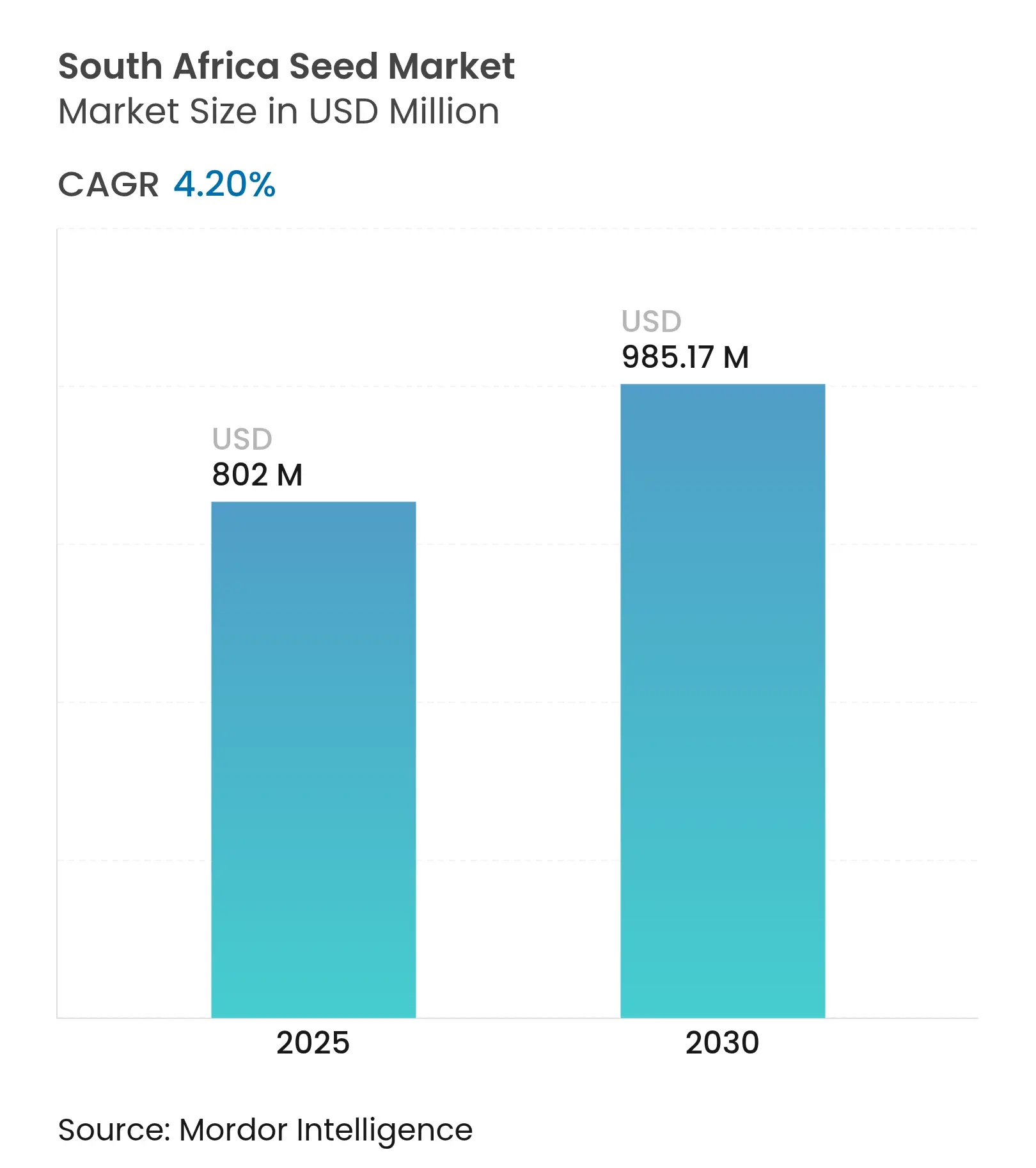

| Market Size (2025) | USD 802 Million |

| Market Size (2030) | USD 985.17 Million |

| Growth Rate (2025 - 2030) | 4.20 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

South Africa Seed Market Analysis by Mordor Intelligence

The South Africa seed market size stood at USD 802 million in 2025 and is projected to reach USD 985.17 million by 2030, reflecting a 4.20% CAGR over the forecast period. Robust adoption of advanced germplasm, early uptake of genetically modified (GM) traits, and a supportive regulatory framework have underpinned the steady expansion of the South Africa seed market. The proclamation of the Climate Change Act in March 2025 is steering investment toward climate-resilient cultivars, while precision agriculture platforms continue to raise input-use efficiency and boost yields. Regional production gains, especially in the Western Cape’s wheat belt and the summer rainfall maize-soybean zones, are supporting additional seed demand, and commercial adoption of genome-editing incentives is widening the scope for next-generation varieties. Market participants are concurrently navigating risks such as consolidation-driven price inflation, evolving pesticide regulations, and climate-induced supply-chain shocks, yet continued government and private-sector R&D spending points to sustained growth opportunities.

Key Report Takeaways

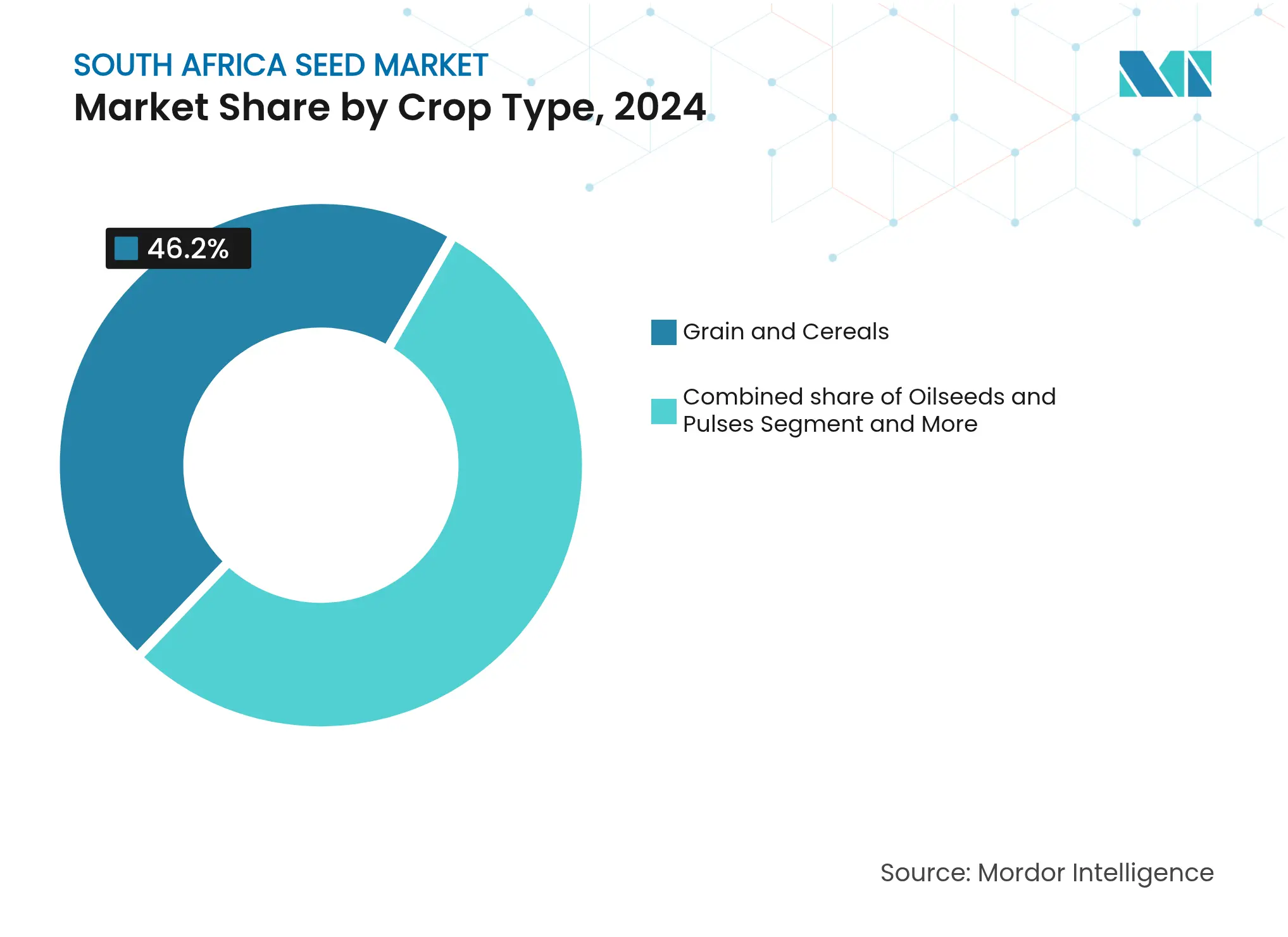

- By crop type, grains and cereals held 46.20% of South Africa seed market share in 2024, while fruits and vegetables are forecast to grow at a 9.60% CAGR through 2030.

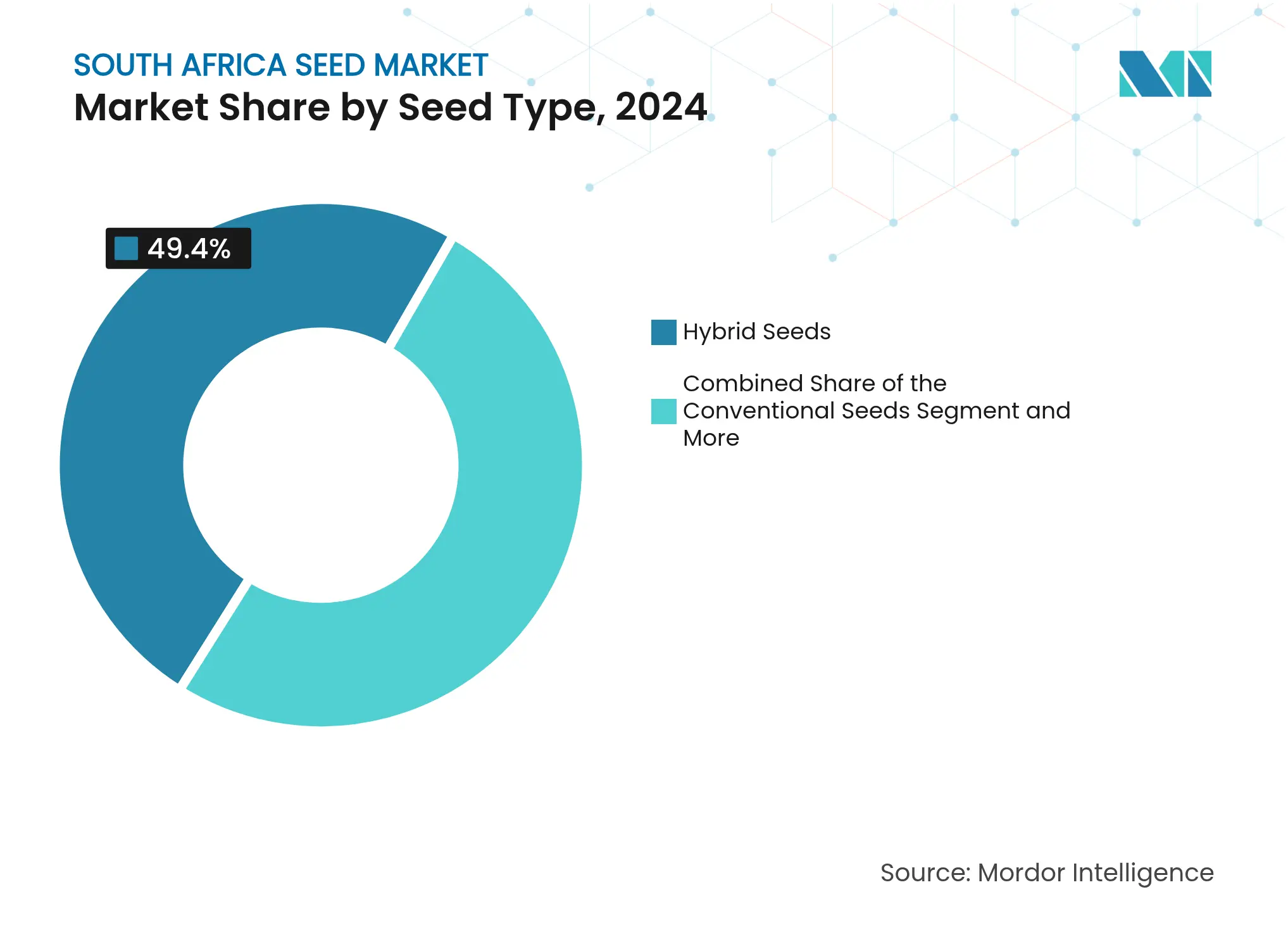

- By seed type, hybrid seeds commanded 49.40% of the South Africa seed market size in 2024; GM seeds are projected to register an 11.20% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Climate-resilient seed demand

Climate-resilient seed demand

| +1.2% | National, with a concentration in the Western Cape and summer rainfall regions | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National, with a concentration in the Western Cape and

summer rainfall regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

Federal incentives for gene-editing

Federal incentives for gene-editing

| +0.8% | National, with research hubs in Gauteng and the Western Cape | Medium term (2-4 years) | |||

Growth in cover-crop seed usage

Growth in cover-crop seed usage

| +0.6% | National, particularly the Free State and Northwest provinces | Medium term (2-4 years) | |||

Digital agriculture enables precision seeding

Digital agriculture enables precision seeding

| +0.9% | National, with early adoption in commercial farming areas | Short term (≤ 2 years) | |||

Biofuel-feedstock seed demand surge

Biofuel-feedstock seed demand surge

| +0.4% | National, with a focus on coastal and inland regions | Long term (≥ 4 years) | |||

Corporate carbon-offset native-seed projects

Corporate carbon-offset native-seed projects

| +0.3% | National, with emphasis on degraded land restoration | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Climate-Resilient Seed Demand

Recurring droughts, hotter summers, and variable rainfall underline the urgency for drought- and heat-tolerant genetics. DroughtTEGO maize retained stable yields under moderate moisture stress and delivered strong performance in optimal conditions, underscoring commercial appetite for resilient hybrids. Heat-tolerant wheat that withstands temperatures 4 °C higher than conventional checks produced 6 metric tons per hectare with only 200 mm of moisture, broadening adoption among Western Cape growers[1]Source: ICARDA Team, “Heat and Drought Tolerant Wheat Varieties,” ICARDA, icarda.org. The Agricultural Research Council’s Roots-to-Resilience program is scaling drought-tolerant sweet potato, while integration of sorghum, millet, and cowpea is strengthening food-system stability across Limpopo and Mpumalanga[2]Source: Agricultural Research Council, “Sweet Potatoes,” arc.agric.za. Together, these initiatives are widening cultivar portfolios and sustaining sales volumes across the South Africa seed market.

Federal Incentives for Gene-Editing

Minister Thoko Didiza’s February 2024 decision to maintain genome-editing oversight under the GMO Act provided regulatory certainty for Clustered regularly interspaced short palindromic repeats (CRISPR)-enabled crops. Subsequent climate legislation in March 2025 furnished tax credits for low-carbon innovations, accelerating collaboration between public breeders and private firms. South Africa’s role in the African Union Development Agency - New Partnership for Africa's Development genome-editing platform is connecting local researchers with continental talent and shared databases, shortening trait-development cycles. Patent activity exemplified by application 2024/04114 covering stacked insect- and herbicide-resistant maize signals a vibrant pipeline[3]Source: CIPC. "JUNE 2024 PATENT JOURNAL." cipc.co.za. These incentives will keep demand for high-value germplasm buoyant and broaden the South Africa seed market.

Growth in Cover-Crop Seed Usage

Soil-erosion rates that exceed natural formation by up to 50 times in exposed fields are prompting conservation-tillage adoption. Black oats are becoming a cover-crop mainstay, producing dense biomass that suppresses weeds and lifts organic-matter scores. Participatory research in Free State and North West confirmed that smallholders who adopted leguminous covers improved soil nitrogen and livestock feed availability in a single season. Educational outreach through extension agents and input alliances is driving annual double-digit volume growth in cover-crop seed orders. As regenerative practices scale, incremental gains in soil health and yield stability will reinforce long-term seed demand.

Digital Agriculture Enables Precision Seeding

IoT-enabled variable-rate seeders, drones, and satellite imagery are transforming crop-establishment practices. Farmonaut’s remote-sensing dashboards lowered planting-error zones by 30% for 1,000 clients in 2025. Red Ant Agri’s Smart Node system creates prescription maps and provides real-time feedback on seed density and depth, minimizing skips and doubles. Domestic startups such as Adagin Technologies are layering AI over machine-vision scale metrics to refine in-field decisions and maximize returns. These gains in input efficiency translate into repeat orders for traited and coated seed, reinforcing volumes in the South Africa seed market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Consolidation-driven seed-price inflation

Consolidation-driven seed-price inflation

| -0.7% | National, affecting all commercial farming regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

National, affecting all commercial farming regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

State bans on neonic-treated seeds

State bans on neonic-treated seeds

| -0.5% | National, with particular impact on cotton and maize production | Medium term (2-4 years) | |||

Trait-patent litigation costs

Trait-patent litigation costs

| -0.4% | National, affecting biotechnology companies and large-scale farmers | Medium term (2-4 years) | |||

Ryegrass anther-smut supply risk

Ryegrass anther-smut supply risk

| -0.2% | National, primarily affecting forage and pasture seed supply | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Consolidation-Driven Seed-Price Inflation

The top five multinationals now control more than half of the cross-pollinated seed supply. BASF’s announced exit from several agriculture units and Syngenta’s divestitures are reshuffling portfolios, leading to localized shortages and upward price revisions. Corteva raised average seed prices 3% in Q1 2025 even as volumes slipped 2%, illustrating market-power dynamics. Although efficiency gains could temper cost pressures, farmers are already shifting toward retained or public-domain seed lines where viable, damping growth potential. Beck's Hybrids' acquisition of a Syngenta corn seed production facility in Nebraska demonstrates ongoing asset reallocation within the industry, potentially affecting pricing dynamics across regional markets.

State Bans on Neonic-Treated Seeds

Proposed restrictions on neonicotinoid seed treatments are emerging as a significant restraint on the expansion of the seed market. Studies indicate that these chemicals can persist in cotton seedling tissues and negatively impact pollinators through environmental runoff. Although diamide-based treatments present potential alternatives, upcoming regulatory decisions are likely to influence seed-treatment volumes, particularly in maize and cotton-producing regions. In Africa, the neonicotinoid market is increasingly under regulatory scrutiny, which could drive changes in seed treatment practices. Similar restrictions in other regions on specific neonicotinoids highlight the critical need for balanced regulations in Africa that safeguard both agricultural productivity and environmental sustainability.

Segment Analysis

By Crop Type: Grains Drive Market Foundation

Grains and cereals accounted for 46.20% of the South Africa seed market share in 2024. The South Africa seed market size for grains and cereals is buttressed production jump in the 2024-25 season, reflecting favorable rainfall and better genetics. Wheat remains challenged by shrinking acreage and weather swings, yet new heat-tolerant lines are maintaining yields in the Western Cape. Wheat production faces unique challenges, with declining areas due to market deregulation and weather unpredictability, leading to increased reliance on imports despite technological advances in drought-tolerant varieties.

The fruits and vegetables segment, despite its smaller scale, shows the highest growth rate. The increasing export-oriented horticulture activities and changes in consumer dietary preferences drive seed demand, resulting in a CAGR of 9.60%. Oilseeds and pulses maintain consistent growth, with soybean production supported by 95% GM seed adoption. The implementation of precision agriculture enhances yields across grain varieties, as variable-rate application technologies improve fertilizer usage and water efficiency through data-driven methods. Financial constraints and inadequate infrastructure continue to limit widespread adoption of these technologies.

Note: Segment shares of all individual segments available upon report purchase

By Seed Type: Hybrid Technologies Lead Innovation

Hybrid seeds captured 49.40% of the South Africa seed market size in 2024, benefitting from consistent yield premiums across maize, sunflower, and vegetable classes. Yield data for hybrid onions show a 20% advantage over open-pollinated equivalents, supporting the conversion of farmers. Starke Ayres leverages marker-assisted and double-haploid breeding, while the company's Quality Assurance Laboratory accreditation by the International Seed Testing Association enables the issuance of ISTA Orange International Certificates, ensuring quality standards that support hybrid seed market confidence.

GM seeds remain the fastest-growing tier at 11.20% CAGR. Sustained regulatory clarity post-February 2024 and anticipated launches such as Bayer’s Vyconic soybeans with five herbicide tolerances are widening trait options. Conventional seeds remain relevant for smallholders and heritage conservation. Policies permitting on-farm seed saving in limited quantities help maintain biodiversity, yet commercial momentum gravitates towards high-tech categories. The segment benefits from heritage seed conservation efforts, particularly among women farmers in Limpopo province who maintain diverse maize varieties, though regulatory frameworks increasingly favor commercial seed systems.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

South Africa's seed market varies across its agro-ecological zones, with distinct regional agricultural patterns. The region's Mediterranean climate and winter rainfall patterns make it particularly suitable for wheat cultivation. The summer rainfall regions of Free State, North West, and Mpumalanga focus on maize, soybeans, and sunflower cultivation, benefiting from favorable growing conditions during the warmer months. These areas have well-developed agricultural infrastructure and established farming practices that support diverse crop production. While wheat remains a significant crop in the market, the country's low self-sufficiency necessitates substantial imports to meet domestic demand, affecting local price dynamics. This import dependency exposes the domestic market to international price fluctuations and currency exchange rate variations, influencing both farmers' planting decisions and consumer prices.

KwaZulu-Natal's leadership in sugarcane and sweet potato production drives demand for specialized cane varieties and drought-tolerant root crop seeds. Limpopo and Mpumalanga provinces have increased their cultivation of alternative crops, particularly millet and cowpea varieties adapted to semi-arid conditions. The agricultural landscape in these regions demonstrates a growing emphasis on crop diversification and climate-resilient farming practices. The adoption of these practices has led to increased demand for specialized seed varieties that can withstand challenging environmental conditions while maintaining productivity.

Climate forecasts indicate below-normal rainfall in the southwest and above-normal precipitation in coastal regions, which will influence seed selection for the 2025-26 planting season. North West, Mpumalanga, and Limpopo provinces are adopting drought-resistant crops such as sorghum, millet, and cowpea to address climate change and water scarcity challenges. This regional adaptation to climate variability has resulted in a shift toward more resilient crop varieties, particularly in areas experiencing water stress. The integration of these drought-resistant crops represents a strategic response to changing environmental conditions while maintaining agricultural productivity across different regions.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Global incumbents Bayer AG, Corteva Agriscience, and Syngenta Group collectively accounted for more than half of the commercial seed volumes in 2024, yet local champions such as Starke Ayres and Capstone Seed retain robust regional footholds. Starke Ayres’ expansion into Kenya, Namibia, and Zambia, and its quality-assurance laboratory accredited by ISTA, strengthens cross-border trust. Ag’s partnership with Bayer AG at the De Ruiter Experience Center pairs AI analytics with greenhouse seed development, accelerating time-to-market for high-value vegetable hybrids.

InteliGro’s tie-up with CropWatch layers remote-sensing insights over input advisory services, expanding seed company channels. Patent filings signal continued R&D investment; application 2024/04114 covers insect- and herbicide-resistant maize, maintaining technology flow. Barriers to entry remain moderate due to the Plant Improvement Act’s seed-quality protocols, which favor firms with robust testing infrastructure.

Emerging disruptors include biotechnology startups and precision agriculture companies, while established players pursue strategic acquisitions and partnerships to maintain competitive advantages. The regulatory framework under the Plant Improvement Act requires seed testing and quality compliance, creating barriers to entry while ensuring market standards that benefit established companies with robust quality assurance systems.

South Africa Seed Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bayer introduced Vyconic soybean seed with five herbicide tolerances, targeting 2027 commercialization.

- February 2025: Advanta Seeds launched new okra varieties aimed at enhancing agricultural productivity in South Africa, reflecting ongoing developments in the seed market focused on improving crop yields and meeting local demand.

- March 2024: Syngenta Vegetable Seeds secured exclusive licensing for Emerald Seed Company’s onion genetics.

Table of Contents for South Africa Seed Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Climate-resilient seed demand

- 4.2.2Federal incentives for gene-editing

- 4.2.3Growth in cover-crop seed usage

- 4.2.4Digital agriculture enables precision seeding

- 4.2.5Biofuel-feedstock seed demand surge

- 4.2.6Corporate carbon-offset native-seed projects

- 4.3Market Restraints

- 4.3.1Consolidation-driven seed-price inflation

- 4.3.2State bans on neonic-treated seeds

- 4.3.3Trait-patent litigation costs

- 4.3.4Ryegrass anther-smut supply risk

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value and Volume)

- 5.1By Crop Type

- 5.1.1Grains and Cereals

- 5.1.2Oilseeds and Pulses

- 5.1.3Fruits and Vegetables

- 5.1.4Other Crops

- 5.2By Seed Type

- 5.2.1Conventional Seeds

- 5.2.2Hybrid Seeds

- 5.2.3GM Seeds

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1Bayer AG

- 6.4.2Corteva Agriscience

- 6.4.3Syngenta Group

- 6.4.4Limagrain Zaad South Africa Ltd (Groupe Limagrain)

- 6.4.5BASF SE

- 6.4.6Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.7Sakata Seed Corporation

- 6.4.8East-West Seed Group

- 6.4.9Capstone Seed Group

- 6.4.10Starke Ayres Pty Ltd (Plennegy Group)

- 6.4.11Barenbrug South Africa Pty Ltd (Royal Barenbrug Group)

- 6.4.12DLF Seeds South Africa Pty Ltd

7. Market Opportunities and Future Outlook

South Africa Seed Market Report Scope

A seed is a mature ovule containing an embryo, along with stored nutrients and a protective outer covering, called the seed coat used for crop production. The South Africa Seed Market is segmented by the Crop Type (Grain and Cereal, Pulse, Vegetable, Oilseed, and Other Crop Types) and the Types of Seeds (Conventional Seeds, Hybrid Seeds, and GM Seeds). The report offers market size and forecast in value USD for all the above segments.