Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.29 Billion |

| Market Size (2031) | USD 13.43 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

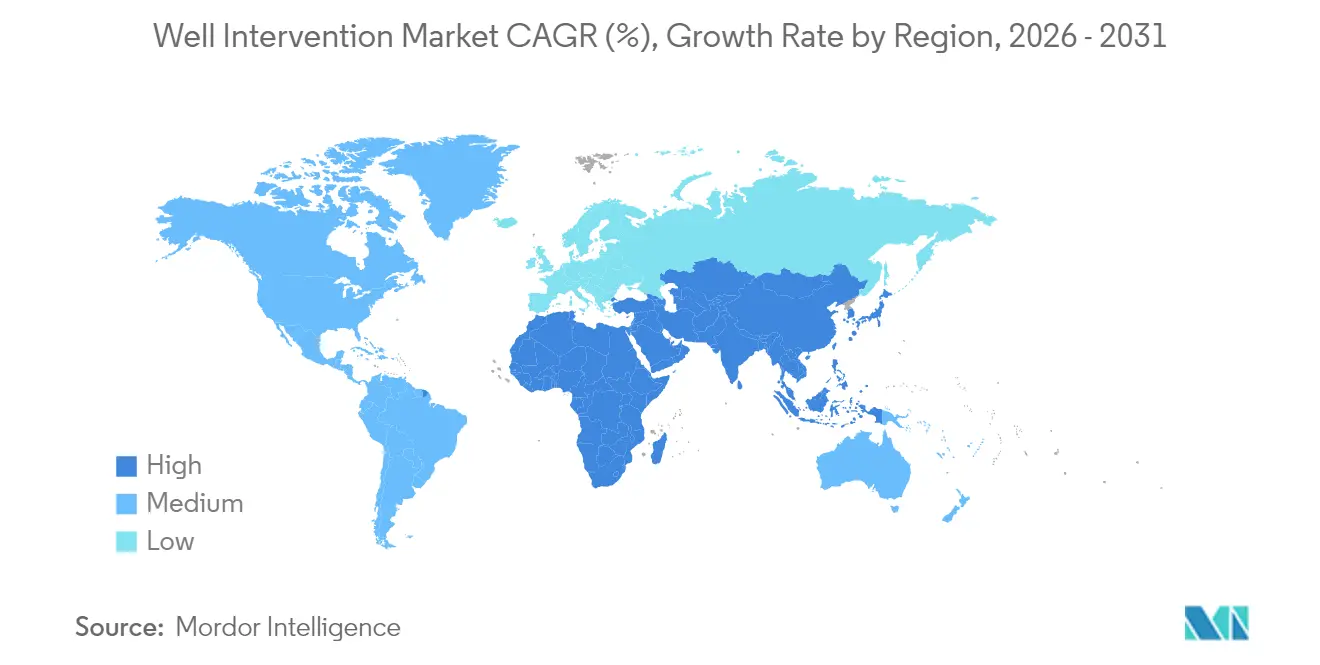

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

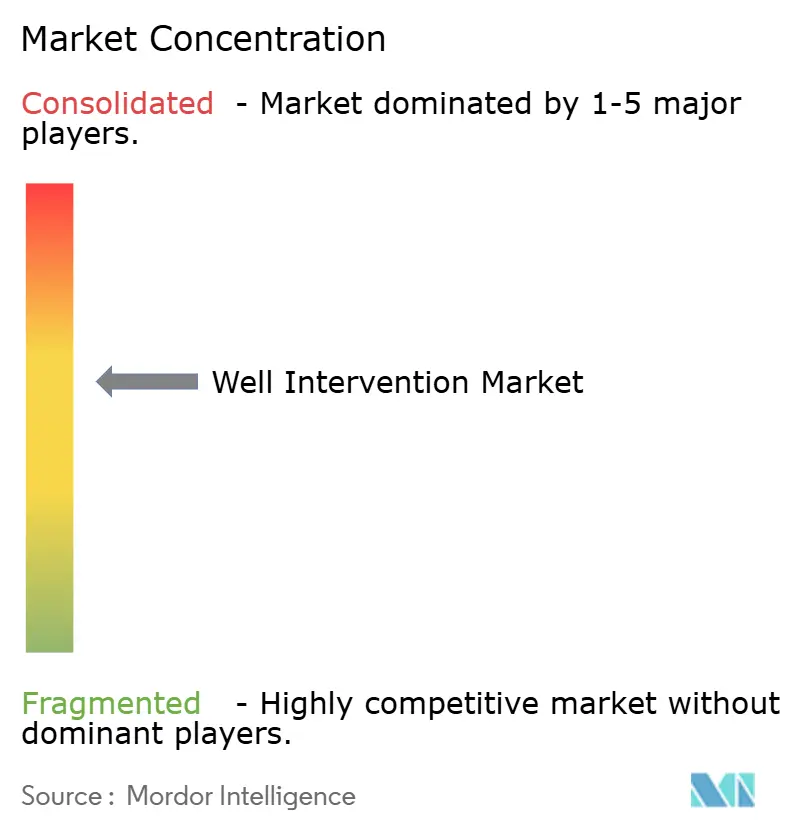

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Well Intervention Market Analysis by Mordor Intelligence

The Well Intervention Market size was valued at USD 9.76 billion in 2025 and estimated to grow from USD 10.29 billion in 2026 to reach USD 13.43 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

Current expansion is fueled by maturing onshore infrastructure that demands recurring workover activity, rising deep- and ultra-deep-water projects that draw premium service pricing, and regulatory mandates for methane-leak remediation that create non-discretionary workloads. North America retains leadership because shale revival campaigns, autonomous downhole robotics, and environmental compliance spending sustain high activity levels. Offshore activity is accelerating as ultra-deep-water wells beyond 1,500 m depths command rapid growth, while the Asia Pacific is emerging as the fastest-growing region thanks to new field development and supportive policy frameworks. The competitive arena remains moderately consolidated, with technologically differentiated portfolios from Schlumberger, Halliburton, and Baker Hughes shaping service standards and pricing.

Key Report Takeaways

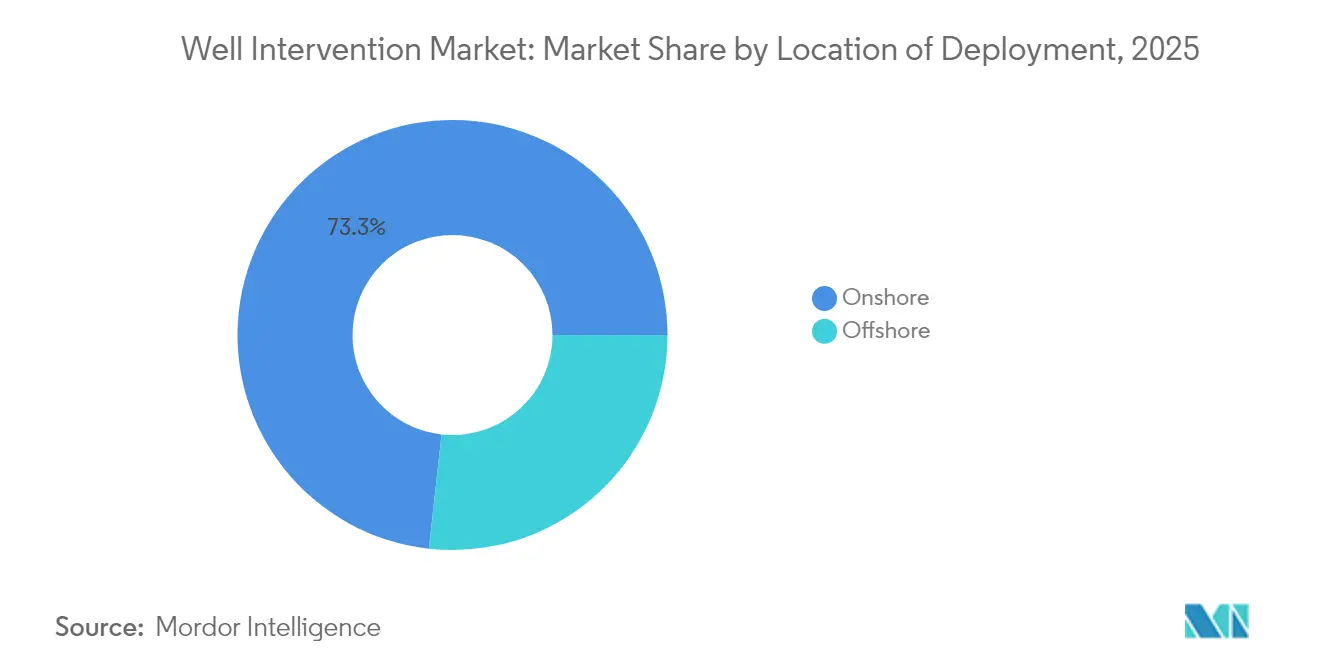

- By location of deployment, onshore operations captured 73.25% of the well intervention market share in 2025, while offshore interventions are expanding at a 6.78% CAGR through 2031.

- By service type, logging and bottom-hole survey services led with 31.90% revenue share in 2025; stimulation services are forecast to advance at a 7.35% CAGR through 2031.

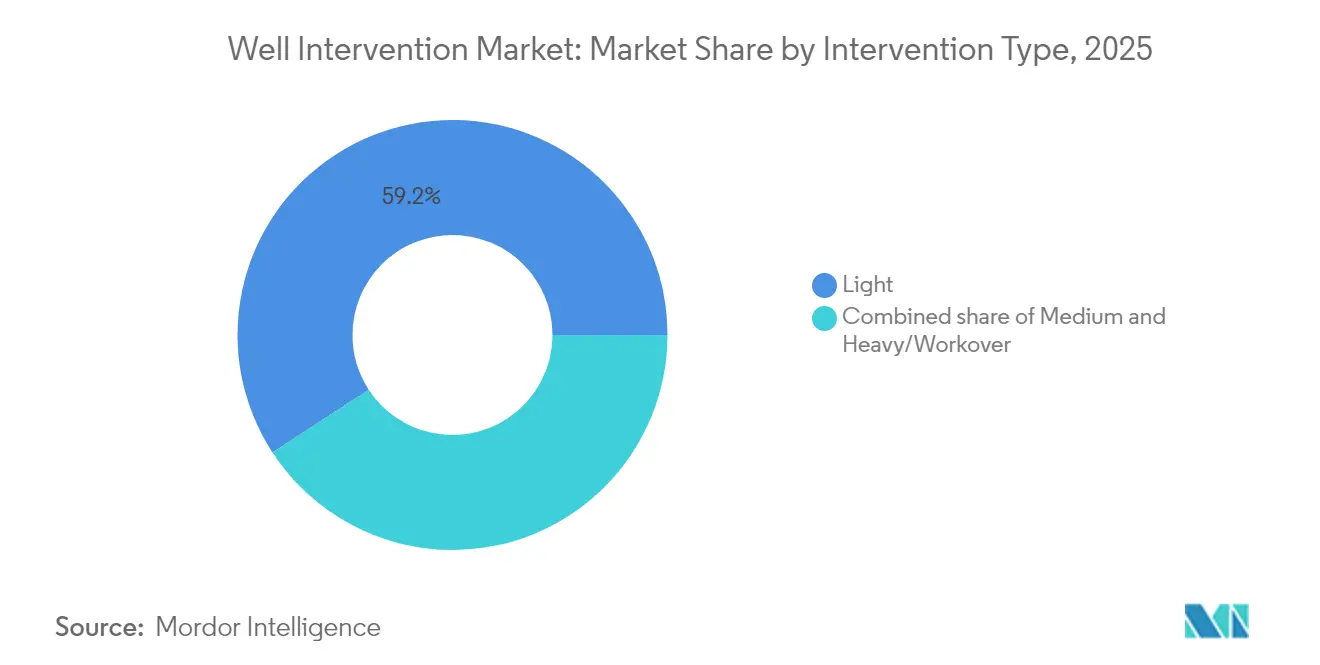

- By intervention type, light interventions held a 59.20% share of the well intervention market size in 2025, whereas heavy workover operations are advancing at a 6.42% CAGR through 2031.

- By well type, horizontal wells accounted for 62.85% of the well intervention market size in 2025 and are projected to expand at a 7.02% CAGR between 2026 and 2031.

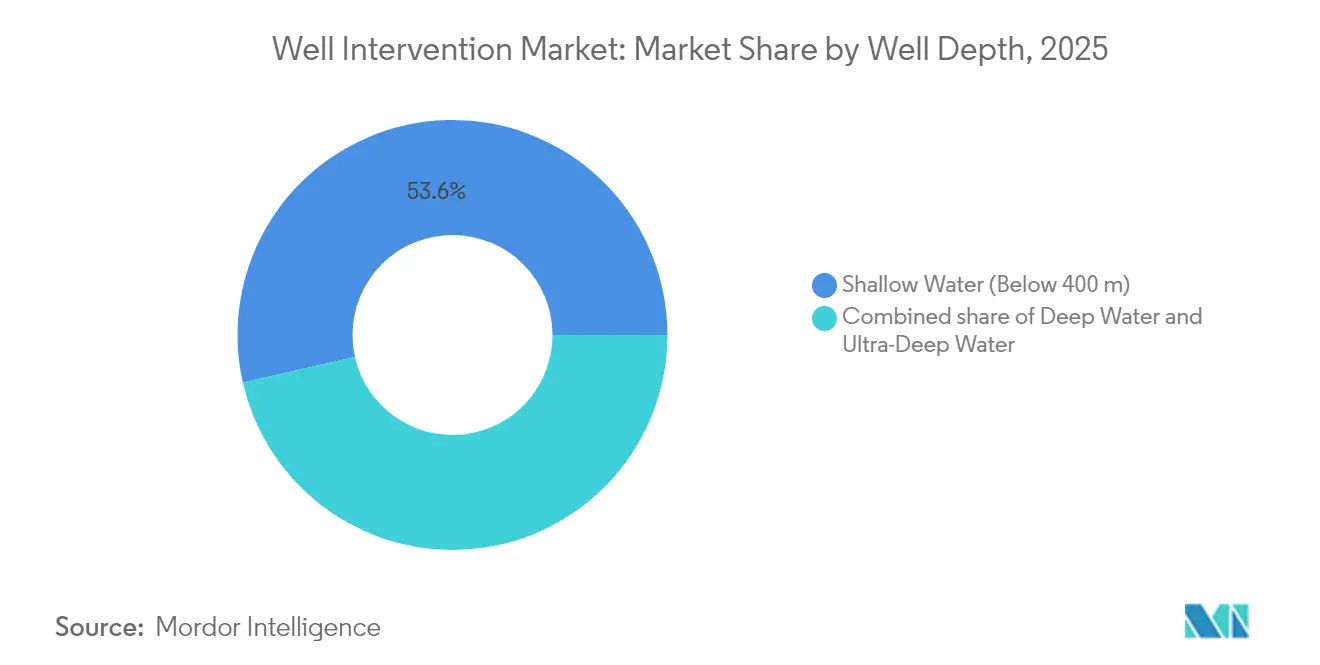

- By well depth, shallow-water operations retained 53.55% of the well intervention market size in 2025; ultra-deep-water wells are the fastest growing, recording an 8.02% CAGR through 2031.

- By geography, North America led with 38.95% revenue share in 2025, whereas the Asia Pacific is poised for a 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Well Intervention Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising workover demand from maturing onshore wells | +1.80% | North America & Europe with spill-over to Asia Pacific | Long term (≥ 4 years) |

| Escalation of deep- and ultra-deep-water developments | +1.50% | Gulf of Mexico, North Sea, Brazil | Medium term (2-4 years) |

| Shale revival in North America fuelling re-fracturing jobs | +1.20% | North America and early adoption in Argentina | Medium term (2-4 years) |

| Mandated methane-leak remediation interventions | +0.90% | Stringent in North America & EU, global adoption | Short term (≤ 2 years) |

| Adoption of digital slickline & autonomous down-hole robots | +0.30% | Early deployment in North America & North Sea | Long term (≥ 4 years) |

| Emerging carbon-capture & storage well conversions | +0.10% | North America & Europe, pilot projects in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Workover Demand from Maturing Onshore Wells

North American and European operators stretch asset life cycles by prioritizing workover programs over fresh drilling. Wells drilled during the 2010-2015 shale expansion need artificial-lift upgrades, stimulation, and mechanical repairs that typically secure 20–30% production uplifts versus 5–10% gains from drilling new wells in mature fields.(1)Baker Hughes, “Artificial-Lift Installations Reach New Milestone,” bakerhughes.com Baker Hughes completed more than 15,000 artificial-lift installations in 2024, 60% of which were in North American onshore basins. Recurring interventions across extended asset life cycles offer steady revenue to service providers and underscore operators’ capital discipline and return-on-existing-infrastructure strategies.

Escalation of Deep- and Ultra-Deep-Water Developments

Ultra-deep-water projects beyond 1,500 m depth are raising technical complexity and service premiums. Chevron’s 20,000 psi Anchor project in the Gulf of Mexico illustrates the specialized equipment needed to execute interventions safely and efficiently.(2)Chevron, “Anchor Project Overview,” chevron.com Service prices in deep water stand 40–60% above shallow-water rates. Petrobras awarded SLB a USD 1.8 billion deep-water intervention contract across pre-salt fields in 2024, signaling robust investment in complex offshore plays. Rigless intervention technologies mitigate cost exposure by replacing ultra-expensive drillships, but deep-water barriers to entry still favor established multinationals with integrated capability suites.

Shale Revival in North America Fuelling Re-fracturing Jobs

US shale producers are reviving aging horizontals by deploying advanced re-fracturing systems that cost 30–50% less than drilling and completing new wells. Eagle Ford case studies reveal refractured laterals outperforming new wells under high price environments, while Bakken operators could generate USD 2 billion from refracturing 400 open-hole wells. Halliburton refrac campaigns in the Permian have delivered 30% production uplifts using diversion agents and optimized completion designs. The re-fracturing segment remains sensitive to commodity price cycles but offers capital-efficient production gains and keeps pressure pumping fleets active.

Mandated Methane-Leak Remediation Interventions

EPA rules now require quarterly leak detection and timely remediation, converting environmental compliance into permanent demand for the well intervention market. Approved Class VI permits for CO₂ storage in depleted reservoirs rose 300% since 2024, with 12 new approvals in 2025, EPA.GOV. Service companies now package methane sensing with immediate intervention solutions, commanding premium pricing because compliance is non-optional and penalties are sizeable. Regulatory momentum shields this demand from the volatility that affects discretionary activity and supports steady backlog pipelines across North America and the European Union.

Restraints Impact Analysis of Well Intervention Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing E&P capex cycles | −1.4% | Global, acute in North American shale | Short term (≤ 2 years) |

| Growing preference for rigless completions | −0.8% | North America & Europe spreading to Asia Pacific | Medium term (2-4 years) |

| ESG-driven capital flight from hydrocarbons | −0.5% | Europe & North America core, selective in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Curbing E&P Capex Cycles

Every dip below USD 55 per barrel triggers 15–25% cuts in intervention budgets as operators defer non-essential projects. Offshore rig utilization slipped in 2024, revealing a direct link between spot pricing and discretionary intervention work scopes. Service revenues swing by up to 40% across cycles, forcing providers to manage cost bases and maintain flexible crews. Capital discipline anchored on free-cash-flow metrics remains a primary check on well intervention market growth until commodity prices stabilize.

Growing Preference for Rigless Completions

Plug-and-perf, dissolvable plug, and simul-frac methods improve initial completions enough to cut future interventions by as much as 60%. Society of Petroleum Engineers case studies show 8% of US completions used simul-frac techniques in Q4 2024, cutting cycle times by more than 60% SPE.ORG. Intervention demand will gradually decline where dissolvable components remove the need for post-stimulation milling, though providers are countering by expanding rigless intervention fleets and diversifying toward stimulation chemistry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Well Intervention Market Segment Analysis

By Location of Deployment:

Offshore Growth AcceleratesOffshore interventions generated robust revenue in 2025, and the segment is positioned for a 6.78% CAGR through 2031 as deep-water and ultra-deep-water wells drive premium-rate work. These high-specification projects underpin a sizeable portion of the well intervention market, and service prices often sit 40–60% above onshore equivalents. Riserless-light-well-intervention vessels, typified by Expro’s AX-S system, can finish offshore jobs in 6–8 days versus 15–20 days for conventional rig support. Operators value reduced downtime and safer crew counts, reinforcing offshore demand despite elevated capital intensity.

Onshore operations still dominate with a 73.25% share in 2025 because thousands of aging shale wells need periodic workovers, artificial-lift changes, and stimulation refresh cycles. Lower unit costs and greater accessibility allow frequent interventions, and upgraded coiled-tubing units shave 20–30% from historical service bills. Asia Pacific and Latin America join North America as active onshore hubs as energy demand and domestic resource development accelerate.

By Service Type:

Stimulation Services Lead GrowthStimulation services rule the growth table with a forecast 7.35% CAGR through 2031. Advances such as emulsified acids, zipper fracturing, and simul-frac enhance contact efficiency while lowering horsepower requirements; Baker Hughes’ OptiPort technology demonstrates better proppant distribution and reduced surface equipment footprint. Operators prioritize these high-impact treatments when commodity prices justify the incremental uplift.

Logging and bottom-hole survey services preserve a 31.90% share because reservoir imaging and mechanical diagnostics remain prerequisites for effective intervention planning. Fiber-optic conveyance and real-time analytics shorten decision loops, letting crews adjust operations on the fly. Artificial-lift, workover and fishing, and niche services such as zonal isolation round out portfolios by solving specific down-hole challenges that surface during production declines or equipment failures.

By Intervention Type:

Heavy Workover Gains MomentumHeavy workovers are pacing at a 6.42% CAGR through 2031, reflecting the mechanical complexity of late-life wells. Hydraulic completion units can now replace tubing strings faster, saving 30–40% time compared with legacy rigs. Higher day rates accompany these jobs because equipment loads and technical risks are greater, but successful workovers often restore production in the 1,000–5,000 barrel-per-day range, easily covering intervention costs.

Light interventions continue as the volume leader at 59.20% share. Digital slickline and advanced coiled tubing help teams execute slickline, e-line, and basic stimulation work expediently. Medium interventions bridge the spectrum, handling tasks like localized recompletions that are too complex for slickline yet do not require full heavy-workover spreads.

By Well Type:

Horizontal Wells Drive MarketHorizontal wells account for 62.85% of the well intervention market size in 2025, mirroring the global shift toward unconventional resource development. Extended laterals require specialized tools for zonal isolation, selective stimulation, and artificial-lift installation. Production boosts of 20–40% after targeted interventions validate the economics of focused remedial campaigns.

Vertical wells retain a presence for legacy production in mature fields. Although less complex and lower priced, intervention frequency is steady because traditional lift systems and older completions require routine servicing. Service firms optimize cost structure in this segment through modular equipment and multi-well campaigns.

By Well Depth:

Ultra-Deep-Water Commands PremiumUltra-deep-water wells deeper than 1,500 m clock the fastest advance at an 8.02% CAGR to 2031, propelled by projects such as Chevron’s Anchor that need 20,000 psi equipment and specialized hydraulic workover units. Service tickets can be triple those for shallow-water jobs, but resource volumes and multi-decade lifespans justify spending.

Shallow-water wells below 400 m still contribute 53.55% market share because they underlie legacy infrastructure across the Gulf of Mexico, North Sea, and Middle East, where continual optimization offsets natural decline. Deep-water projects between 400–1,500 m provide a balanced risk profile and foster incremental technology adoption.

Geography Analysis

North America Well Intervention Market

North America held 38.95% of the well intervention market in 2025 as prolific shale basins, tough methane regulations, and deep-water Gulf of Mexico assets combine to sustain high service intensity. Operators leverage digital slickline, real-time fiber-optic tools, and autonomous robotics to improve efficiency by 20–30% while meeting stringent environmental standards. Recurring refrac campaigns maintain capacity utilization for pressure pumping fleets even when fresh drilling slows.

North Sea Well Intervention Market

Europe follows with a mature yet active theater anchored by the North Sea. Norway and the UK incentivize late-life asset optimization, and carbon-capture storage conversions add fresh intervention demand streams. Stringent ESG policies elevate methane remediation and well-integrity management to core operating priorities, prompting technology-heavy service contracts.

APAC Well Intervention Market

Asia Pacific is the fastest-growing well intervention market fastest-growing region, set for a 6.28% CAGR through 2031. Strong energy demand, supportive government policies, and ambitious offshore gas projects in Southeast Asia spur the deployment of advanced intervention technologies. China’s voracious land rig appetite and India’s upstream liberalization add scale, while Australia’s mature offshore fields require sophisticated interventions to sustain LNG export infrastructure.

Regulatory Landscape

Regulation affecting well intervention activity continues to tighten around well control, barrier management, and formalized consent workflows, particularly offshore. In the United States, BSEE well-operations requirements under 30 CFR Part 250 Subpart G mandate maintaining at least two independent well barriers during well operations, including intervention, with at least one mechanical barrier, which shapes equipment selection and verification practices for interventions in the Gulf of Mexico.

In early 2026, the North Sea Transition Authority (NSTA) published its UKCS Well Applications and Consents Guide (2026 Edition), consolidating the application and consent pathway and reinforcing operator accountability through appointed Well Operators under the Offshore Petroleum Licensing (Offshore Safety Directive) Regulations 2015. The guide also points to digital systems such as WONS for notifications and tracking. Canada clarified scope in 2025 as N.S. Reg. 28/2025 (CNSOPB), explicitly defining well operations to include intervention and workover, bringing these activities into board oversight and compliance processes. UK Environmental Impact Assessment (EIA) Regulations can treat certain re-completions as projects requiring consent where applicable.

Competitive Landscape

The well intervention market exhibits moderate consolidation. Schlumberger, Halliburton, and Baker Hughes command high market visibility with integrated portfolios, global logistics, and continuous R&D investment. They often win multi-year, multi-service tenders that bundle logging, stimulation, and artificial-lift under single commercial frameworks, reducing operator interface risk.

Technology-driven acquisitions augment capability breadth. SLB’s USD 7.1 billion purchase of ChampionX in 2024 fortified artificial-lift and chemical injection offerings, underpinning bigger integrated contracts SLB.COM. Baker Hughes’ USD 850 million buy-out of Altus Intervention’s coiled-tubing assets strengthened rigless offshore execution. White-space players such as Weatherford, Expro, and Welltec carve niches by commercializing autonomous tractors, electric workover units, and riserless intervention systems.

Competitive intensity now revolves around digital enablement, environmental compliance, and risk-sharing contract structures. Providers that merge real-time subsurface data with predictive analytics differentiate on uptime, cost certainty, and ESG reporting, thereby capturing premium margins even during commodity downturns.

Well Intervention Industry Leaders

Schlumberger Limited

Halliburton Company

China Oilfield Services Limited

Weatherford International Plc.

Baker Hughes Company

- *Disclaimer: Major Players sorted in no particular order

Well Intervention Market Companies Covered in this Report

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Weatherford International plc

- Expro Group Holdings NV

- National Oilwell Varco Inc.

- Vallourec SA

- Scientific Drilling International

- China Oilfield Services Ltd (COSL)

- Helix Energy Solutions Group Inc.

- Archer Ltd.

- Welltec A/S

- Superior Energy Services Inc.

- Trican Well Service Ltd.

- Aker Solutions ASA

- Altus Intervention AS

- Hunting PLC

- TechnipFMC plc

- Petrofac Ltd.

- Oceaneering International Inc.

Market Opportunities and Future Outlook

Rigless and vessel-based subsea intervention is broadening beyond its historic North Sea concentration into the Gulf of Mexico, Brazil, Guyana, and Southeast Asia, creating room for providers that can combine subsea access, well control assurance, and faster cycle times. 2026 contract activity reflects this direction, including Unity securing its first Malaysia rigless well intervention and P&A contract, DOF Group ASA securing a three-year award for the Skandi Involver to support subsea IMR and well intervention work in Guyana, and Weatherford winning offshore plug and abandonment and workover scope tied to Constellation Oil Services in Brazil. These awards track operator priorities around brownfield production optimization, integrity repair, and decommissioning workloads that can be executed without full rig spreads.

Technology-driven differentiation is also creating more defined opportunities in subsea well access and digitalized execution. Expro launched Solus, a shear-and-seal valve system tested to API Std 17G, then followed with a Gulf of Mexico contract extension involving Solus deployment, consistent with demand for hardware that reduces debris-related risk during intervention. Onshore and offshore programs are also taking up integrated digital platforms for planning and monitoring. Baker Hughes extending contracts with Equinor, including wireline intervention services and use of the PRIME Technology Platform, supports performance and emissions-related operating requirements through more instrumented, repeatable intervention workflows.

Recent Industry Developments in Well Intervention Market

- April 2026: Halliburton acquired Sekal AS from Sumitomo Corporation to integrate digital drilling autonomy into its offering, combining Halliburton LOGIX with Sekal DrillTronics. The deal strengthens an end-to-end workflow where automated well placement and hydraulics optimization translate into cleaner handoffs to completion and intervention planning, supporting higher-efficiency well lifecycle services.

- December 2025: SLB secured a five-year contract from Aramco covering stimulation, well intervention, and frac automation services for Saudi Arabian unconventional gas developments. The long-term award expands SLB's intervention-linked backlog in a strategic gas growth area and reinforces integrated contracting models that tie well performance improvements to automation and execution consistency.

- December 2024: SLB was awarded an integrated services contract for Petrobras' offshore fields in Brazil, spanning multiple service lines for deepwater operations. The award supports sustained deepwater activity where complex well designs and high service intensity drive recurring intervention and optimization work across the field life cycle.

Well Intervention Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the well intervention market covers paid services and related activity that restore, maintain, or improve oil and gas well performance after drilling, across onshore and offshore wells. Revenue is counted for intervention jobs that change well conditions, improve flow, or provide diagnostics leading to an intervention decision.

Scope exclusions: We exclude routine drilling and completion work, standalone seismic and drilling fluids, and general production operations that do not involve an intervention job.

Segments Covered in This Report

- By Location of Deployment

- Onshore

- Offshore

- By Service Type

- Logging and Bottom-hole Survey

- Stimulation

- Artificial Lift

- Workover and Fishing

- Others (Zonal Isolation, Sand Control etc.)

- By Intervention Type

- Light (Slickline, E-line, CT)

- Medium

- Heavy/Workover

- By Well Type

- Horizontal wells

- Vertical wells

- By Well Depth

- Shallow Water (Below 400 m)

- Deep Water (400 to 1,500 m)

- Ultra-Deep Water (Above 1,500 m)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Norway

- Germany

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- ASEAN Countries

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by locking the market perimeter and building the demand pool for intervention work by region and by onshore and offshore activity. We use public sources such as the EIA for upstream activity signals, the IEA for outlook and production context, and OPEC monthly reports for supply-side direction that impacts intervention budgets.

To translate activity into market value, we also review well count and drilling completions indicators published by agencies and regulators (such as the U.S. BSEE for offshore activity and incident reporting), along with trade association releases and peer reviewed papers that discuss intervention frequency and well integrity drivers. Company annual reports, investor decks, and reputable press coverage help validate service mix changes and pricing direction, and selected paid subscriptions support company financials, news, and patent screening for technology-driven cost shifts. The sources listed here are illustrative only, and many other public documents and references were used to collect, cross-check, and clarify data.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk model with people who plan, buy, or deliver interventions, including operators, service contractors, tool providers, and offshore logistics partners. Since this is a global market, we make sure views are balanced across mature basins and growth basins, and then we re-check any price or utilization assumption that can move the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 20% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up mix, starting with a top-down build where regional upstream activity and well stock signals are converted into an intervention demand pool, and then valued using service mix and typical spend per job for onshore and offshore. Before totals are finalized, we corroborate them with selective bottom-up checks, such as sampling disclosed segment revenues, validating utilization with channel checks, and stress-testing implied pricing using a simple ASP times volume view.

Key inputs used in the model include active producing well counts, maturity of fields (which drives integrity and remedial work), offshore rig and vessel activity as a proxy for complex interventions, typical intervention frequency per well type, and service pricing movement by intervention level (light, medium, heavy). When data is thin for smaller countries, gaps are handled by using proxy basins with similar operating conditions, followed by an expert review so the proxy does not overstate local capability.

For forecasting, scenario analysis is used so near-term spend swings tied to oil and gas price cycles and operator budgets are reflected, and then checked against the forward view from interviewees on intervention cadence, tool availability, and offshore scheduling constraints.

Data Validation & Update Cycle

Outputs are validated through multiple passes that look for logical breaks between regions, sudden step-ups in pricing, or intervention intensity that does not fit the well maturity profile. Analysts compare the modeled totals with independent signals such as regional production trends, offshore activity indicators, and disclosed service line direction from public filings, and then anomalies are reworked until assumptions can be explained plainly.

The report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as sharp changes in upstream spending, regulatory shifts affecting offshore work, or major supply constraints. Before delivery, an analyst performs a fresh pass so clients receive the latest updated market view.

Mordor Intelligence's Global Well Intervention Market Market Size Measured Against Other Published Estimates

Published market values for well intervention do not always match because the inputs are sensitive to how a study treats offshore complexity, intervention frequency, and how quickly pricing is refreshed. Differences also show up when one publisher reports a base year value and another quotes the first forecast year, which can make gaps look larger than they really are.

Some estimates bring adjacent oilfield services into the same number, including broader workover and completion related revenue beyond intervention tasks. For Mordor Intelligence, revenue is counted only when the activity is a defined well intervention job (onshore or offshore), and pricing is refreshed through operator and contractor validation before the forecast is finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.29 B (2026) | |

| Industry Publisher A | USD 9.81 B (2025) | Uses a different base year and a longer horizon, and the earlier year value can understate the near-term uplift from offshore scheduling and recent price resets in intervention services. |

| Global Consultancy B | USD 8.94 B (2023) | Starts from an older base year and shorter forecast window, which can dilute the impact of recent intervention intensity increases in mature fields and the current service mix shift toward higher value jobs. |

The table shows that year selection and what gets counted as intervention revenue are the main reasons for the spread. By tying the model to a clear activity pool and then validating pricing and service mix through repeated expert checks, the estimate stays traceable to practical variables that can be re-tested as conditions change.

Key Questions Answered in the Report

What is the current size of the well intervention market?

The well intervention market size is USD 10.29 billion in 2026, with revenue projected to reach USD 13.43 billion by 2031.

How fast is the well intervention market expected to grow?

The market is forecast to expand at a 5.47% CAGR between 2026 and 2031, reflecting steady demand from both onshore workovers and deep-water projects.

Which region leads the global well intervention market?

North America remains the largest regional market with 38.95% share in 2025, supported by shale activity and stringent methane-leak regulations.

Which region is the fastest growing for well intervention services?

Asia Pacific is the fastest-expanding region, on track for a 6.28% CAGR through 2031 as China, India, and Southeast Asia increase domestic exploration efforts.

What service segment is expected to register the highest growth?

Stimulation services are poised for the quickest expansion, advancing at a 7.35% CAGR through 2031 due to rising refracturing and enhanced-recovery programs.

How do methane-leak regulations influence market demand?

Mandatory leak detection and remediation rules create recurring, non-discretionary intervention work, providing a reliable revenue stream even during oil-price downturns. . . . . . . . New Research

Page last updated on: