Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

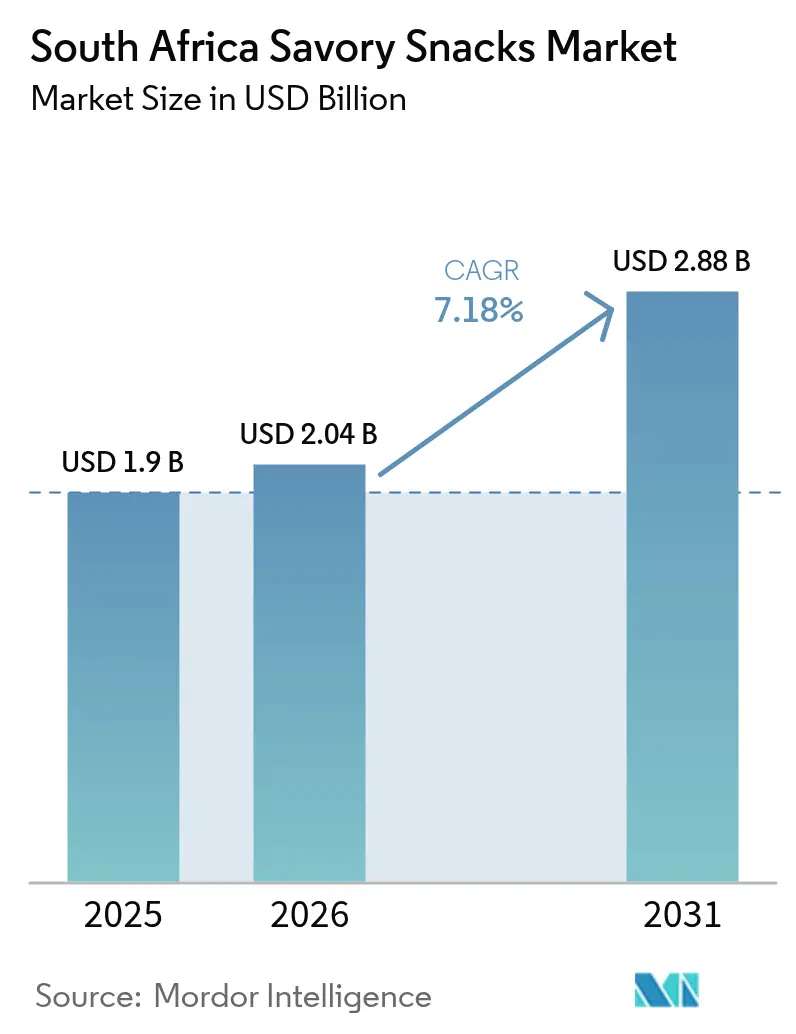

| Base Year Market Size (2025) | USD 1.90 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.88 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

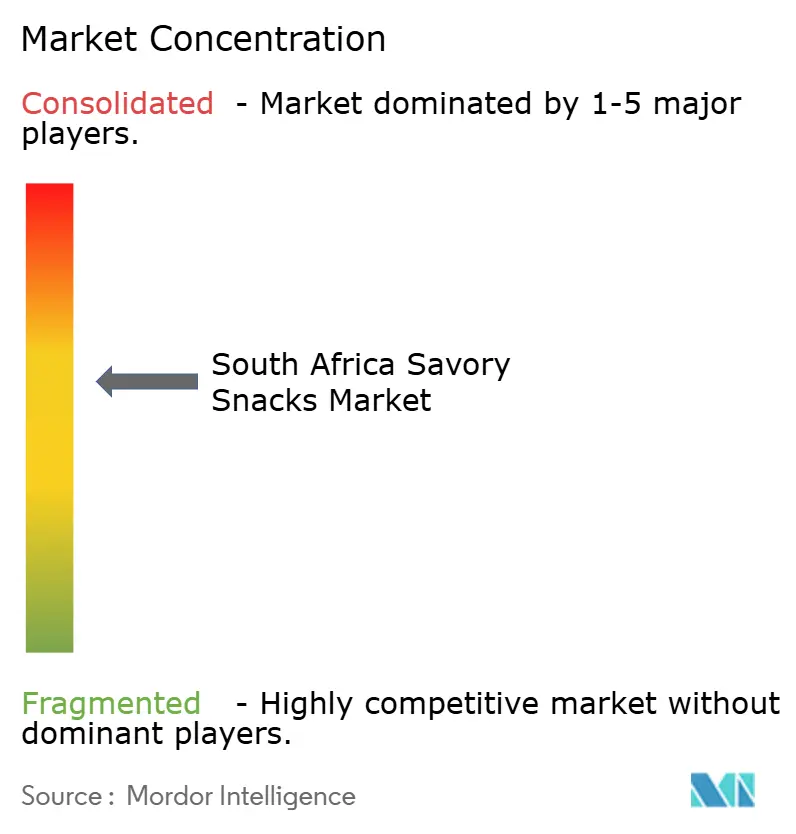

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Savory Snacks Market Analysis by Mordor Intelligence

South Africa savory snacks market size in 2026 is estimated at USD 2.04 billion, growing from 2025 value of USD 1.90 billion with 2031 projections showing USD 2.88 billion, growing at 7.18% CAGR over 2026-2031. Growth rests on three pillars: expanding middle-class spending power, a national preference for bold flavors, and rising demand for on-the-go formats that fit busy urban lifestyles[1]Statistics South Africa, “South African Households Spend R3 Trillion Annually,” statssa.gov.za. Manufacturers respond with local flavor innovations while aligning with global wellness trends, spurring the launch of baked and pulse-based products that meet forthcoming front-of-package labeling rules. Supermarkets underpin volume, yet rapid e-commerce growth—illustrated by Checkers Sixty60’s USD 534 million equivalent in annual turnover—signals a structural shift in retail. Volatile potato and maize prices continue to squeeze margins, but anticipated La Niña rains are expected to ease cost pressures and stabilize supply chains.

Key Report Takeaways

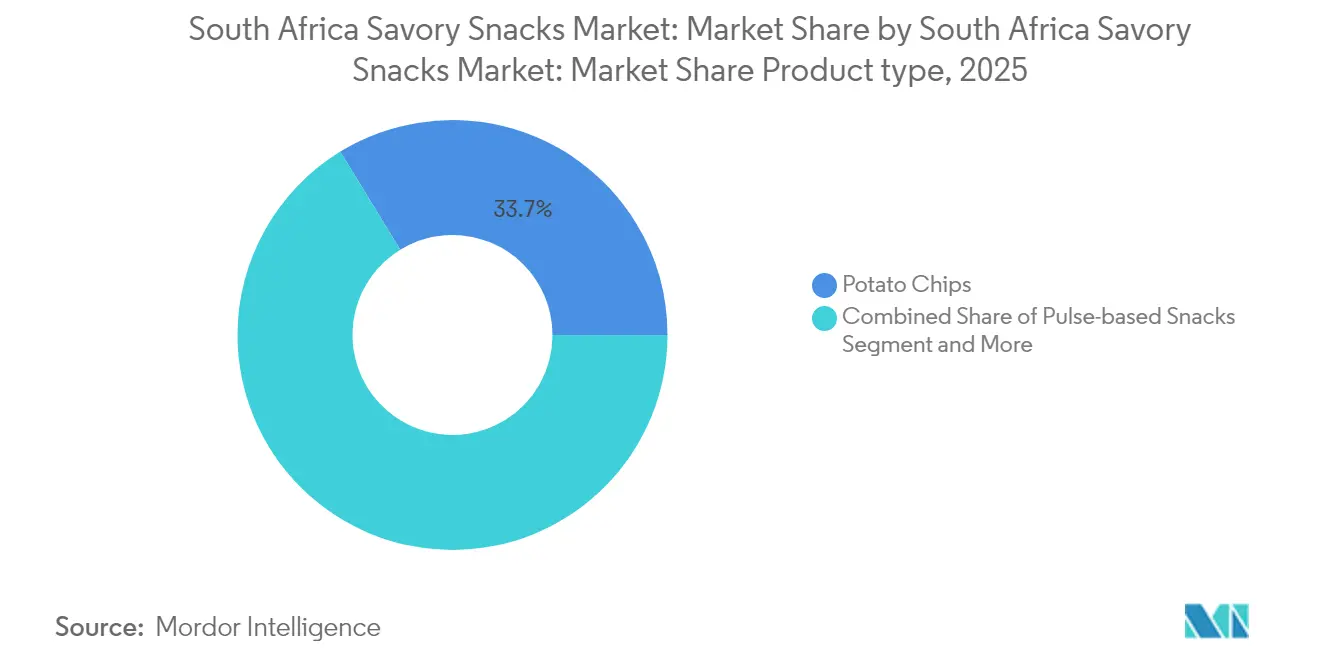

- By product type, potato chips led with 33.74% of the South Africa savory snacks market share in 2025, while pulse-based snacks are forecast to advance at an 8.41% CAGR through 2031.

- By category, fried snacks accounted for 63.05% of the South Africa savory snacks market size in 2025 and baked snacks are expected to post an 8.12% CAGR to 2031.

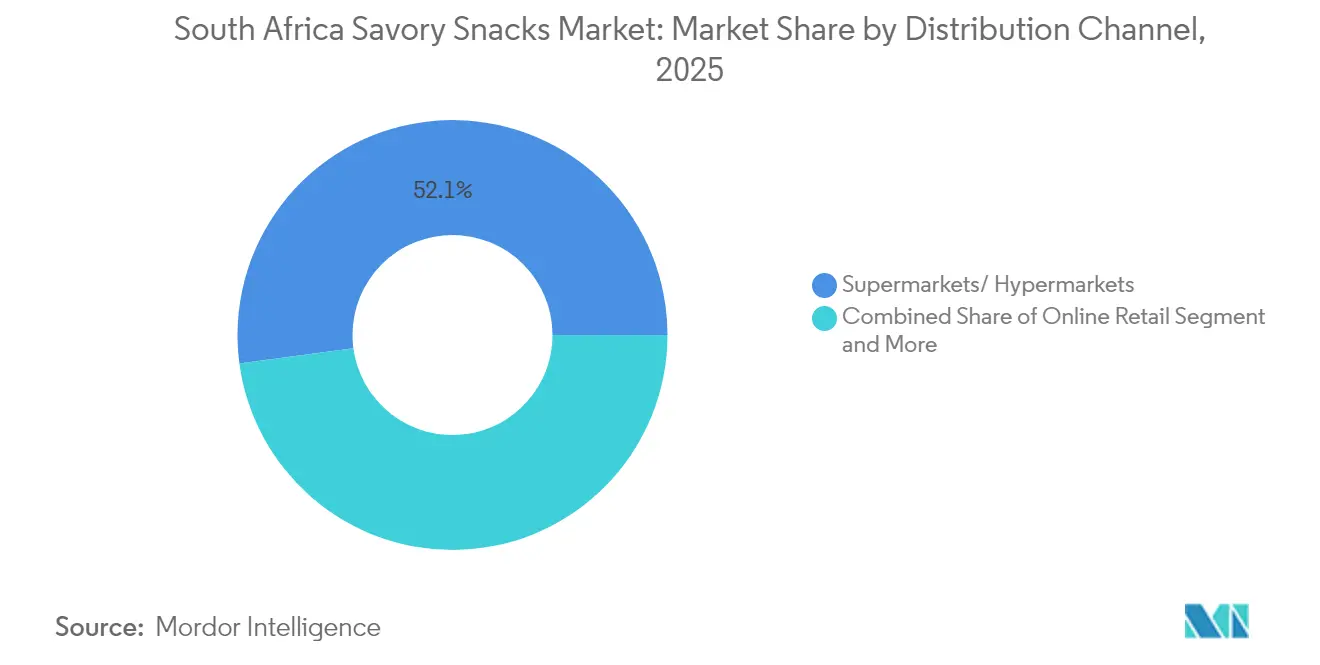

- By distribution channel, supermarkets and hypermarkets held 52.11% revenue share in 2025; online retail is set to expand at a 9.36% CAGR through 2031.

- By geography, Gauteng commanded 35.01% of 2025 sales, and KwaZulu-Natal is projected to register a 7.32% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Savory Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenient snacking options | 1.2% | National, with concentration in Gauteng and Western Cape urban centers | Medium term (2-4 years) |

| Spice tolerance & heat-seeking preferences | 0.9% | National, strongest in KwaZulu-Natal and Eastern Cape | Long term (≥ 4 years) |

| Rising disposable income among middle-class | 1.4% | Gauteng, Western Cape, with spillover to KwaZulu-Natal | Medium term (2-4 years) |

| Shift toward healthier & organic snack formats | 1.1% | Western Cape and Gauteng affluent demographics | Long term (≥ 4 years) |

| Digitalisation of township spaza-shop networks | 0.9% | National township areas, early gains in Gauteng, Western Cape | Short term (≤ 2 years) |

| Indigenous plant-based protein snack innovation | 0.7% | National, with manufacturing concentration in KwaZulu-Natal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Convenient Snacking Options

Urban consumers buy savory items during commutes, at petrol stations, and through delivery apps, helped by 16.28 million adults purchasing fast food monthly. Improved power supply has lifted factory uptime, enabling consistent store replenishment[2]BizCommunity, “South Africans love their fast food… especially KFC,” bizcommunity.com. Mobile payments and same-day delivery broaden reach, with 55% of users now ordering groceries online each month. Checkers Sixty60’s 63.1% sales increase validates the omni-channel model that pairs bricks-and-mortar inventory with app-driven convenience. As township spaza shops connect to digital ordering platforms, impulse snack purchases rise even in areas once served solely by informal trade. Packaging innovations that extend shelf life further support this uptake, keeping products fresh across long supply chains.

Spice Tolerance & Heat-Seeking Preferences

A cultural appetite for bold flavors shapes product pipelines: chili, peri-peri, and masala variants secure shelf space countrywide. PepsiCo developed localized Lay’s and Doritos iterations after in-house sensory panels confirmed that 75% of tasters sought “noticeable burn” in potato chips[3]Food Dive, “How PepsiCo adapts snacks to local tastes,” fooddive.com. KwaZulu-Natal’s growth reflects its culinary heritage that marries spice with indigenous ingredients such as rooibos. Manufacturers in Durban leverage proximity to spice suppliers to reduce formulation costs and accelerate flavor testing. Spice affinity also opens export doors: Halaal-certified fiery snacks now ship to Middle-East partners that view South Africa as a taste-matched sourcing hub. By meeting domestic and diaspora palates, brands build defensible niches against generic imports.

Rising Disposable Income Among Middle-Class

Real household consumption continues climbing, surpassing USD 160 billion annually when measured at current exchange rates. New entrants target aspirational shoppers with premium seasoning blends, resealable packs, and influencer-backed campaigns that signal status without straining budgets. Gauteng’s high-income suburbs favor value-added multipacks, while mid-tier shoppers in secondary cities gravitate toward larger “family share” formats for cost savings. Retail competition intensifies: Shoprite’s aggressive price-lock promotions pull volumes from rivals and keep branded snacks affordable. Rising incomes also expand formal employment, supporting stable snacking budgets even as interest rates fluctuate.

Shift Toward Healthier & Organic Snack Formats

Regulators finalized draft rule R3337 that mandates clear sugar, salt, and saturated-fat icons on front panels, prompting reformulations that replace palm oil with sunflower or explore air-popped bases. Baked launches grew 21% in 2024 by SKU count, and bean-based puffs that deliver 20.4 g protein per 100 g secured listings at major chains.. Western Cape startups draw on local fynbos extracts for antioxidant claims, while Gauteng co-packers invest in gluten-free extrusion lines. Consumers with lifestyle diseases now trade fried chips for low-oil lentil curls positioned as “school-safe” snacks. Although healthier varieties carry 15–20% price premiums, survey data show parents still purchase them monthly, prioritizing nutrient density over volume.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-driven shift to meal replacements | -0.9% | Urban areas in Gauteng and Western Cape | Medium term (2-4 years) |

| Volatile potato and maize input prices | -1.2% | National, with manufacturing concentration impact | Short term (≤ 2 years) |

| Competition from confectionery and baked goods | -0.7% | National, with stronger impact in Western Cape and Gauteng | Medium term (2-4 years) |

| Emerging single-use-plastic regulations | -0.6% | National, with early implementation in Western Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health-Driven Shift to Meal Replacements

Heightened awareness of obesity and micronutrient gaps leads some urban consumers to skip snacks in favor of protein shakes, oat cups, or fortified bars. Food-basket costs climbed to USD 291 per household in May 2025, focusing budgets on essentials. Regulators accentuate this pivot by requiring larger nutrient panels that highlight sodium counts in chips. Category incumbents counter with “mini-meal” positioning, adding legumes and seeds to raise protein while keeping snack sensorial cues. Retailers create adjacent shelf sets that blur traditional categories, prompting co-merchandising of savory bites with functional drinks.

Volatile Potato and Maize Input Prices

Potato prices rose 7% month-on-month in May 2025 as flood-damaged Free State farms curtailed supply. Maize harvests in 2024 fell 19% under El Niño stress, lifting cost curves for corn-based extruded snacks. Manufacturers hedge with forward contracts and diversify into cassava flour and chickpea grit. Expected La Niña precipitation in late 2025 should increase the summer-crop estimate to 14.56 million tonnes, easing feedstock pressure. Still, volatility hampers long-term price points, complicating promotions and retailer negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pulse-Based Innovation Disrupts Potato Dominance

Potato chips retained 33.74% of the 2025 value, but input price swings and nutrition labeling scrutiny constrain long-term upside. Extruded corn curls hold steady due to low-cost scalability and the ability to absorb spicy seasonings that resonate nationally. Popcorn advances modestly, marketed as a low-calorie cinema-style treat. Nuts, seeds, and trail mixes cater to affluent urbanites, yet higher price points limit mass reach.

Pulse-based snacks post the fastest 8.41% CAGR, propelled by 20.4 g protein per 100 g formulations that satisfy gym-goers and parents seeking school-approved items. Indigenous legumes add provenance stories that differentiate SKUs from global rivals. Meat and biltong snacks ride cultural affinity but struggle with 15% beef price surges tied to disease outbreaks. As reformulations multiply, the South Africa savory snacks market embraces hybrid products blending pulses with potato or maize to hedge cost risk and please evolving palates.

By Category: Health Regulations Accelerate Baked Segment Growth

Fried snacks dominated 63.05% in 2025, thanks to entrenched taste expectations and lower unit costs. Retailers rely on this segment for volume promotions and cross-category basket building. Nonetheless, sodium and saturated-fat warnings soon to appear on packs may temper growth, steering shoppers to alternatives.

Baked lines register an 8.12% CAGR, benefitting from oil-reduction messaging and school nutrition guidelines that ban deep-fried snacks at tuck shops. Companies retrofit facilities with conveyor ovens, cutting frying oil spend by up to 40%. Air-popped and dehydrated styles begin to surface in specialty outlets, carrying a 30% price premium yet boasting triple-digit sell-through in pilot stores. Regulatory bodies, including the National Regulator for Compulsory Specifications, continuously audit these facilities, supporting consumer trust.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Supermarkets and hypermarkets commanded 52.11% in 2025 value sales, leveraging weekly specials and loyalty programs to capture family shoppers. Shoprite’s lead derives from efficient distribution centers and fixed-price strategies that absorb some input cost shocks. Convenience stores thrive on impulse buys near petrol stations, while specialty outlets highlight artisanal and allergen-free lines.

Online retail posts the quickest 9.36% CAGR, driving the South Africa savory snacks market closer to real-time demand fulfillment. Checkers Sixty60 moved more than 3.5 million snack units in 2024 alone, a figure projected to double by 2026. Free delivery thresholds encourage basket-building across snack categories. Spaza shop apps extend the digital wave into townships, where licensed operations now access bulk-buy pricing once reserved for formal trade.

Geography Analysis

Gauteng dominates the South Africa savory snacks market, reflecting its economic might and sophisticated retail grid that enables same-day fulfillment. High brand visibility, aggressive promotions, and a concentration of middle-income households keep per-capita snack expenditure well above the national average. Western Cape secures the second-largest stake through an affluent consumer base that values origin stories and low-oil preparation, spurring artisanal baked launches stocked in premium grocers and farmers’ markets.

KwaZulu-Natal is the fastest riser, supported by a robust Halaal certification framework that dovetails with its cultural preference for spicy snacks. The province houses two Tiger Brands plants producing 33 snack brands, ensuring local supply and export readiness. Infrastructure improvements around Durban port also streamline outbound logistics, reducing lead times to Gulf markets. Eastern Cape and a cluster of smaller provinces offer untapped upside as digital ordering and road infrastructure reduce the historic service gap between urban and rural outlets. Government investment in township business upgrades further formalizes retail nodes, deepening market penetration for established brands.

Competitive Landscape

Moderate concentration characterizes the South Africa savory snacks market. PepsiCo steers category leadership through Simba, Lay’s, and Doritos, tailoring seasoning levels to local spice thresholds and securing nationwide cold-chain coverage. AVI Limited’s Willards and Bakers portfolios leverage legacy shopper trust and multi-price-point packs to defend share at both premium and value tiers. Tiger Brands operates Fritos under license, marrying local maize know-how with international flavor IP. Kellogg’s Pringles maintains a premium stack-chip niche that appeals to urban consumers seeking international flair.

White-space innovation centers on pulse-based chips and indigenous protein crisps, where smaller firms such as Herbivore Earthfoods launch cowpea curls positioned as 100% plant-based. Multinationals form joint ventures with R&D spin-offs to secure early access to these crops, ensuring supply certainty. Packaging sustainability gains board-level attention: Guala Closures’ acquisition of Coleus Packaging strengthens local sourcing of metal caps and supports fully recyclable snack tins. Cost pressures prompt network optimization: PepsiCo shuttered a 50-year-old Frito-Lay plant to upgrade to high-throughput lines elsewhere, signaling continued footprint rationalization. Overall, a balance of global scale and local agility defines success in the competitive arena.

South Africa Savory Snacks Industry Leaders

PepsiCo Inc

AVI Limited

The Kellogg Company

Frimax Foods Private Limited

Truda Foods Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: PepsiCo has officially introduced Cheetos in South Africa, marking a significant milestone for the renowned brand. The new snack product flavours include Cheetos Puffs Cheese – a classic favourite with a rich, creamy kick, Cheetos Puffs Chicken a savoury twist that’s sure to be a crowd-pleaser, Cheetos Brix BBQ – smoky and bold, perfect for flavour adventurers and Cheetos Brix Spicy Tomato – a zesty option with a fiery edge.

- December 2023: Kellanova announced three of its snack brands, Cheez-It Snap'd, Cheez-It Puff'd, and Club Crisps, reduced the amount of plastic used in their packaging while maintaining the same amount of food in each package.

- October 2023: Simba collaborated with Chef Benny to create their new Steakhouse Beef flavored chips. Per the company’s claims, this significant collaboration reflects Simba's commitment to creating authentic flavors that resonate with South African culture.

South Africa Savory Snacks Market Report Scope

Savory snacks are small servings of food with a salty or spicy flavor rather than a sweet one. The South African savory snacks market is segmented into product types and distribution channels. The market is segmented into potato chips, extruded snacks, nuts, seeds and trail mixes, popcorn, meat snacks, and other product types based on product type. Based on distribution channels, the market is segmented into supermarkets/ hypermarkets, convenience stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecasting have been done in value terms of USD.

By Product Type

| Potato Chips |

| Extruded Snacks |

| Popcorn |

| Nuts, Seeds, and Trail Mixes |

| Meat Snacks |

| Other Product Types |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Potato Chips |

| Extruded Snacks | |

| Popcorn | |

| Nuts, Seeds, and Trail Mixes | |

| Meat Snacks | |

| Other Product Types | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How big is the South Africa Savory Snacks Market?

The South Africa Savory Snacks Market size is expected to reach USD 2.04 billion in 2026 and grow at a CAGR of 7.18% to reach USD 2.88 billion by 2031.

What is the current South Africa Savory Snacks Market size?

In 2026, the South Africa Savory Snacks Market size is expected to reach USD 2.04 billion.

Who are the key players in South Africa Savory Snacks Market?

PepsiCo Inc, AVI Limited, The Kellogg Company, Frimax Foods Private Limited and Truda Foods Private Limited are the major companies operating in the South Africa Savory Snacks Market.

What years does this South Africa Savory Snacks Market cover, and what was the market size in 2025?

In 2025, the South Africa Savory Snacks Market size was estimated at USD 2.04 billion. The report covers the South Africa Savory Snacks Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the South Africa Savory Snacks Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: