Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

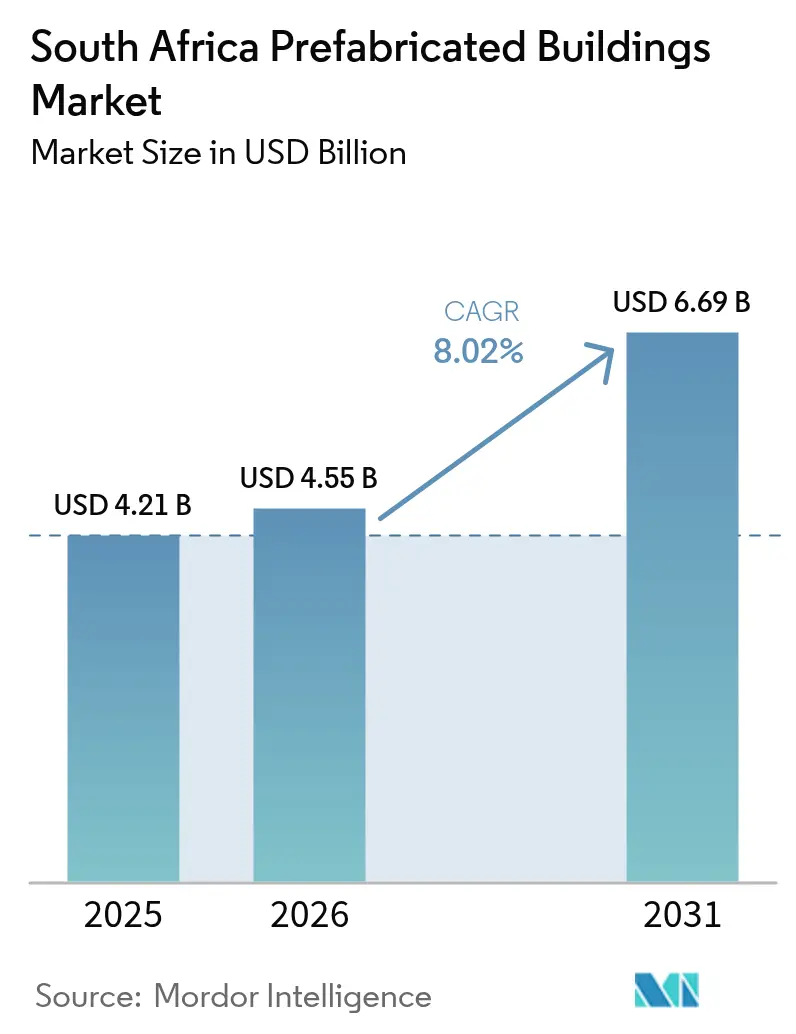

| Base Year Market Size (2025) | USD 4.21 Billion |

| Market Size (2026) | USD 4.55 Billion |

| Market Size (2031) | USD 6.69 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

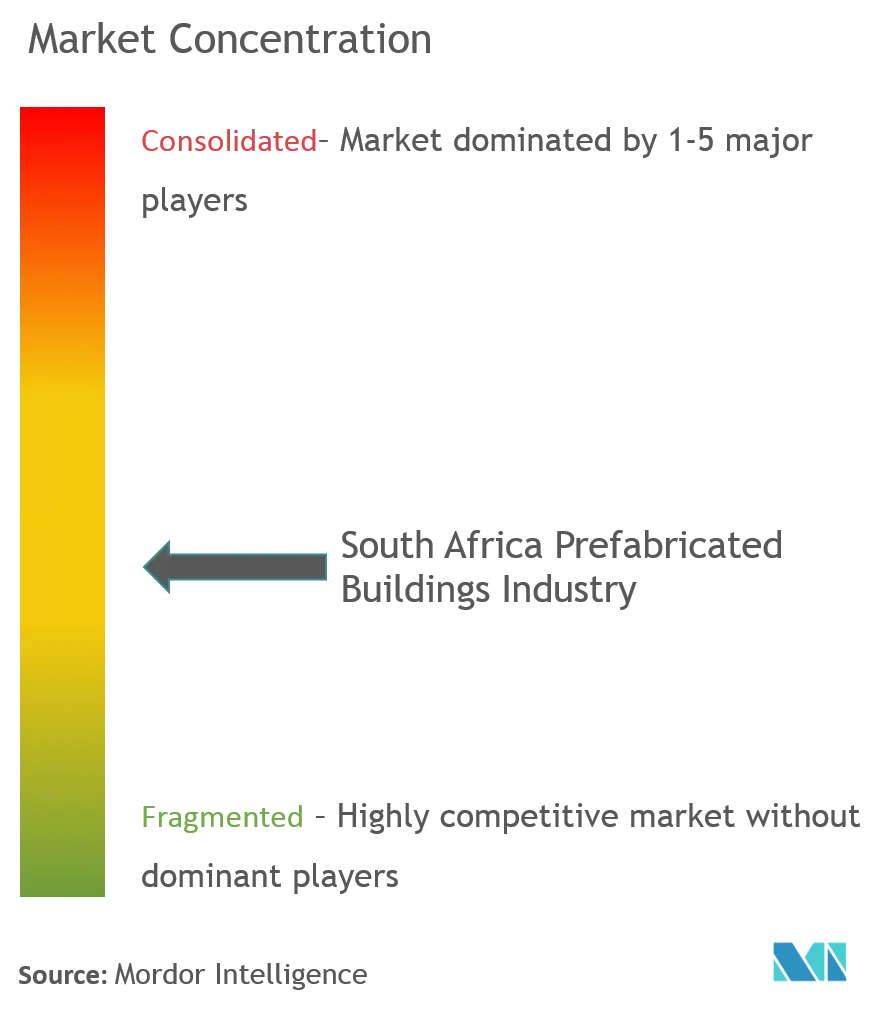

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Prefabricated Buildings Market Analysis by Mordor Intelligence

The South Africa prefabricated buildings market size is expected to grow from USD 4.21 billion in 2025 to USD 4.55 billion in 2026 and is forecast to reach USD 6.69 billion by 2031 at 8.02% CAGR over 2026-2031. Rising demand stems from a 2.3 million-unit housing deficit, the government’s fast-track infrastructure programs, and chronic power-supply disruptions that favor factory-built, solar-ready structures. The Reconstruction and Development Programme (RDP) backlog and a shift toward performance-based public tenders amplify the need for rapid-deployment solutions that avoid traditional site delays. Corporations and mining houses accelerate adoption to house workforces efficiently, while green-building mandates and load-shedding concerns position low-carbon, photovoltaic-integrated modules as premium offerings. Investors view the segment as a hedge against labor shortages and material inflation, fueling factory automation and vertical-integration strategies among leading manufacturers[1]South African Government, “Presidential Investment Projects,” gov.za.

Key Report Takeaways

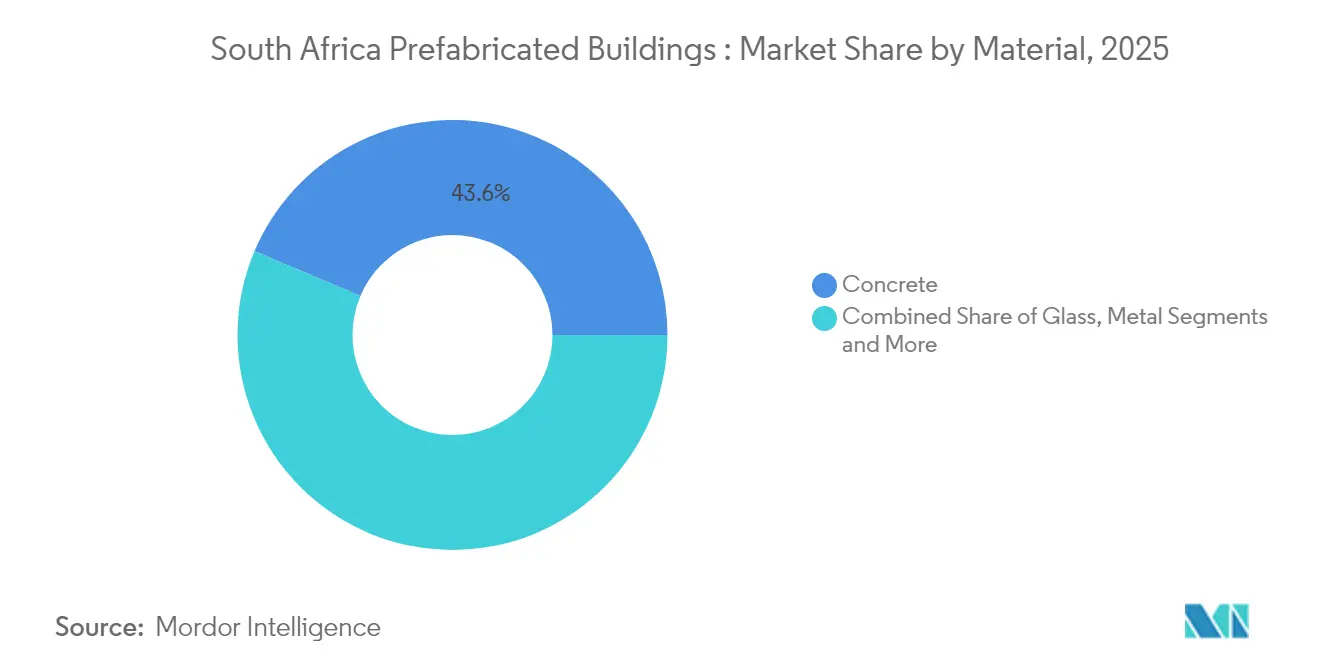

- By material, concrete systems held 43.62% of South Africa's prefabricated buildings market share in 2025; timber solutions recorded the fastest 8.76% CAGR through 2031.

- By application, residential captured 50.62% of the South Africa prefabricated buildings market size in 2025, while commercial deployments expand at an 8.37% CAGR to 2031.

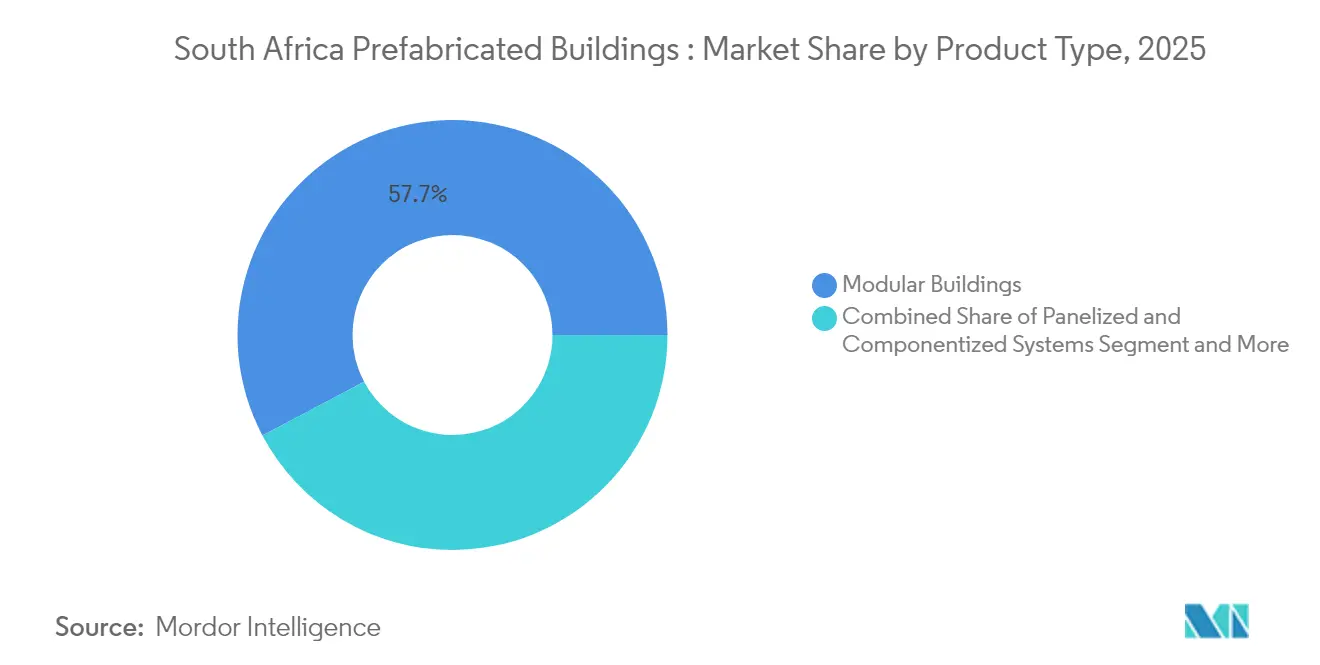

- By product type, modular buildings led with 57.74% of South Africa's prefabricated buildings market share in 2025, and panelized systems posted the quickest 8.64% CAGR to 2031.

- By key city, Johannesburg accounted for 24.18% of the South Africa prefabricated buildings market size in 2025; Cape Town advances at a 8.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RDP housing backlog accelerating rapid-build demand | +1.8% | National: Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Urbanisation-led 2.3 million-unit deficit | +1.5% | Johannesburg, Cape Town, Durban | Long term (≥ 4 years) |

| Mining camp demand for remote modular accommodation | +1.2% | Northern Cape, Limpopo, North West | Short term (≤ 2 years) |

| Load-shedding-proof solar-integrated modules | +1.1% | National, premium in commercial segments | Short term (≤ 2 years) |

| Edge-certified low-carbon prefab recognition | +0.9% | Western Cape, Gauteng | Medium term (2-4 years) |

| Insurance discounts for fire-resistant light-steel frames | +0.7% | High-risk areas; informal settlement upgrades | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RDP Housing Backlog Accelerating Rapid-Build Demand

Government housing completions collapsed from more than 235,000 units in 1998-99 to 34,000 units in 2022-23, forcing municipalities to embrace modular options that slash delivery times from 18-24 months to 6-9 months. President Ramaphosa’s USD 55.6 million Northern Cape program for 4,000 units within 18 months exemplifies this urgency. Performance-based tenders now reward firms that guarantee schedules, channeling contracts toward manufacturers with proven factory capacity. Metropolitan registers in Cape Town alone list 375,000 applicants—further intensifying demand. Consequently, South Africa's prefabricated buildings market participants scale production lines to capture RDP-linked volumes.

Urbanisation-Led 2.3 Million-Unit Deficit

Formal-housing occupancy rose to 83.5% in 2024, yet the absolute shortage widened to 2.3 million units, hitting middle-income earners excluded from RDP subsidies. Prefabricated homes priced between USD 11,100-27,800 fill this gap at volumes traditional builders struggle to serve. Sustained immigration: 3.9% of residents now originate mainly from SADC statesconcentrating pressure in Gauteng and Western Cape. Financial innovators bundle mortgages with factory orders, easing access for salaried buyers. These dynamics underpin the long-run expansion of South Africa's prefabricated buildings market.

Mining Camp Demand for Remote Modular Accommodation

Kumba Iron Ore’s USD 622 million upgrade extending Sishen mine to 2044 typifies capital projects that need scalable worker housing. Modular dormitories travel by road to remote Northern Cape, Limpopo, and North West, arriving ready-wired and furnished within weeks. Operators favor relocatable units that flex with commodity cycles. Safety standards improve because assembly occurs under controlled factory conditions, lowering on-site risk. Suppliers of South Africa's prefabricated buildings market increasingly embed telecoms and solar arrays to meet miners’ off-grid requirements[2]Engineering News, “South Africa’s Solar Capacity Stats 2024,” engineeringnews.co.za.

Load-Shedding-Proof Solar-Integrated Modules

Electricity rationing reached stage-6 levels in 2024, delaying conventional projects and inflating costs. Prefab makers pre-install PV panels and battery rails, ensuring immediate autonomy once sited. National PV capacity climbed to 8.97 GW in 2024, with private arrays contributing two-thirds of the total. Legislation enabling private wheeling accelerates rooftop adoption, making solar-ready modules the logical choice for retailers and clinics. As reliability concerns persist, solar-integrated offerings anchor premium pricing within South Africa's prefabricated buildings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce domestic structural-timber supply | -1.4% | Nationwide, timber-prefab value chain | Long term (≥ 4 years) |

| Public-sector bias for brick-and-mortar tenders | -1.1% | All tiers of government | Medium term (2-4 years) |

| Prefab is perceived as “temporary” in townships | -0.8% | Township and informal areas | Long term (≥ 4 years) |

| Oversized-transport permit bottlenecks | -0.6% | Inter-provincial corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Domestic Structural-Timber Supply

Local mills cannot meet the rising demand for graded lumber, forcing builders to import at elevated prices and longer lead times. Recent droughts degraded pine yields in regional plantations, compounding shortages. Timber-based providers hedge by blending laminated veneer lumber with recycled steel, but volume scalability remains constrained. Government forestry plans focus on conservation, so structural supply gaps may persist into the next decade, limiting the timber segment’s full potential in South Africa's prefabricated buildings market.

Public-Sector Bias for Brick-and-Mortar Tenders

Procurement officers trained on conventional standards often score modular bids lower for “innovation risk” despite cost advantages. The new Public Procurement Act adds transparency layers that could inadvertently slow approvals for unfamiliar techniques. Contractors spend extra months securing plan approvals, eroding prefab speed benefits. Industry bodies lobby for standardized specifications to level scoring criteria, but widespread adoption remains a medium-term prospect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Leads While Timber Gains Pace

Concrete-based units commanded 43.62% of South Africa's prefabricated buildings market share in 2025, benefiting from established codes and ready municipal acceptance. Manufacturers leverage pre-stressed panels and 3-D volumetric pods to speed high-rise social housing in Gauteng, aligning with insurers’ fire-rating criteria. Timber systems, though limited by supply, boast the quickest 8.76% CAGR on the strength of sustainability certifications and weight advantages that cut freight costs.

Concrete’s dominance also reflects well-developed domestic cement supply chains and contractors’ familiarity with load-bearing capacities. Nonetheless, timber’s low-carbon footprint meets corporate ESG mandates, drawing investment into cross-laminated-timber (CLT) pilot plants near Durban. Hybrid assemblies combining steel skeletons with timber infill emerge as compromise solutions addressing both supply and regulation. Collectively, these dynamics cement material diversification within South Africa's prefabricated buildings market.

By Application: Residential Still Rules, Commercial Accelerates

Residential projects held 50.62% of South Africa's prefabricated buildings market size in 2025 on the back of public RDP contracts and private gap-market schemes. Modular suburbs around Johannesburg and Cape Town showcase single-family designs delivered in under 90 days. Commercial demand, while smaller, expands at an 8.37% CAGR as mines, retailers, and data-center operators favor relocatable buildings that scale with operations.

Mining camps require durable dorms for rotating crews, and corporate head offices adopt modular annexes to sidestep zoning delays. Education and healthcare modules also rise, tapped by the USD 266.7 billion national infrastructure pipeline to deliver rural clinics swiftly. Load-shedding resilience adds momentum across all end-uses, pushing developers toward integrated PV-battery packages.

By Product Type: Modular Dominates, Panelized Surges

Fully assembled modular blocks captured 57.74% of South Africa's prefabricated buildings market share in 2025, capitalizing on acute skilled-labor shortages. Factory automation ensures predictable quality and halves onsite labor hours. Panelized kits gain ground at an 8.64% CAGR because they fit standard trucks, reducing escort costs and simplifying inter-provincial shipping.

Growth in panelized solutions also links to rooftop-solar integration carried out on production lines for precise mounting angles. Componentized frames serve niche sectors such as telecom shelters. Looking ahead, digital twins and BIM-enabled factories will likely enhance accuracy, supporting tighter tolerances demanded by green-building schemes, further boosting both modular and panelized adoption.

Geography Analysis

South Africa's prefabricated buildings market clusters around Gauteng, where Johannesburg’s 24.18% share reflects the province’s economic gravity, high homeless headcount, and the presence of corporate headquarters seeking flexible offices. Load-shedding vulnerability in the region accelerates demand for solar-integrated modules that keep operations running during grid curtailments. Proximity to cement and steel suppliers further cements Gauteng’s leadership.

Western Cape delivers the fastest 8.88% CAGR through 2031 as Cape Town rolls out inclusionary-housing bylaws and green-building incentives. Developers target vacant inner-city parcels with vertical modular blocks that satisfy density goals while meeting Six-Star Green Star benchmarks. The city’s tech sector, hosting Amazon’s regional campus, values quick-fit offices and data-center shells that minimize disruption.

KwaZulu-Natal, Eastern Cape, and Free State contribute incremental growth. Durban’s port logistics upgrade spurs prefab warehouses, while Eastern Cape’s auto hubs need supplier parks erected to tight schedules. Free State municipalities pilot modular clinics under the national health-insurance rollout. In the Northern Cape, mining investments such as Sishen’s life-extension drive large orders for dormitories and process buildings, reinforcing the technology’s credibility in extreme environments.

Remote rural areas collectively account for growing volumes as the USD 55.6 million Northern Cape housing drive showcases prefab viability under sparse infrastructure conditions. Government agencies embrace containerized classrooms and clinics to meet service obligations quickly. Rising immigrant settlement outside metros broadens geographic demand, making South Africa's prefabricated buildings market genuinely nationwide.

Competitive Landscape

The competitive landscape in 2024 remains moderately fragmented, with several key players driving innovation and growth. Kwikspace Modular Buildings and Waco Modular, leveraging national depot networks, ensure the delivery of turn-key camps within a swift two-week timeframe. Both companies are investing in robotic welding lines and digital-traceability systems to meet the latest procurement audit requirements. Meanwhile, Concor’s Modular Division stands out by offering tailored financing packages for "missing middle" buyers, effectively addressing the needs of the gap-housing segment.

Emerging players are focusing on specialized niches, such as solar-ready and fire-resistant solutions. For example, Eco-Frame is developing light-steel assemblies pre-wired for 10 kW rooftop solar arrays, catering to clients seeking alternatives to mitigate load-shedding challenges. TimberFrame SA collaborates with plantation owners to secure FSC-certified materials, emphasizing material traceability for environmentally conscious developers. Additionally, strategic partnerships with insurance companies provide premium discounts, influencing purchase decisions in favor of these solutions. Foreign interest in the market is driving increased M&A activity. A European prefab company is reportedly exploring a minority stake in a Gauteng factory to establish a presence in Southern Africa. Local companies are responding by scaling up their operations—Kwikspace, for instance, has announced a 25,000 m² expansion at its Pretoria facility. They are also adopting Building Information Modeling (BIM) to reduce design-to-manufacture cycles to just 10 days. In the South African prefabricated buildings market, success is increasingly defined by a combination of innovation and scalability.

South Africa Prefabricated Buildings Industry Leaders

Kwikspace Modular Buildings

Waco Modular (Pty) Ltd

Module Solutions Africa

Afripanel Building Systems

Concor (Modular Division)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: President Cyril Ramaphosa launched a USD 55.6 million Northern Cape mega-housing project for 4,000 modular homes slated within 18 months. The USD 55.6 million order for 4,000 modular homes gives factories 18 months of guaranteed volume, lets lenders verify cash-flow certainty, and offers a public proof-of-concept that other provinces can replicate, directly lifting state-sector demand.

- August 2024: Kumba Iron Ore committed USD 622 million to extend Sishen mine, generating large orders for modular camps. Kumba’s USD 622 million plan requires long-life yet movable camps, so mining houses will favor rugged modular blocks, deepening commercial share and diversifying revenue beyond residential orders.

- April 2024: ZAR 500 million HTMR-100 reactor project adopted modular methodologies for nuclear components. Using modular construction for nuclear components showcases precision in a highly regulated arena, strengthening market confidence that factory-built methods meet even the strictest technical codes.

- February 2024: U.S. Department of Commerce highlighted 2 million m² certified green-building footprint, elevating prefab prospects. Recognition of a 2 million m² certified green footprint attracts ESG-oriented capital; prefab makers that publish embodied-carbon data become prime candidates for these funds, easing plant-expansion financing.

South Africa Prefabricated Buildings Market Report Scope

Prefabricated buildings (also known as prefabs) are the building structures manufactured offsite and transported to the on-site assembly location. This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, and its impact, porter's five forces analysis, and the impact of COVID-19 on the market. In addition, the report also provides company profiles to understand the competitive landscape of the market.

The South Africa Prefabricated Buildings Industry is segmented by Material Type (Concrete, Glass, Metal, Timber, and Other Material Types) and Application (Residential, Commercial, and Other Applications). The report offers market size and forecasts for the South Africa prefabricated buildings industry in value (USD billion) for all the above segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key Cities

| Johannesburg |

| Cape Town |

| Durban |

| Port Elizabeth |

| Bloemfontein |

| Pretoria |

| Rest of South Africa |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key Cities | Johannesburg |

| Cape Town | |

| Durban | |

| Port Elizabeth | |

| Bloemfontein | |

| Pretoria | |

| Rest of South Africa |

Key Questions Answered in the Report

What is the 2026 value of South Africa prefabricated buildings market?

The market is estimated at USD 4.55 billion for 2026, reflecting robust housing and infrastructure demand.

How fast is the market expected to grow to 2031?

Revenues are projected to rise to USD 6.69 billion by 2031, translating into an 8.02% CAGR over 2026-2031.

Which material dominates current prefab adoption?

Concrete systems lead with 43.62% market share in 2025 share due to regulatory familiarity and strong local supply chains.

Why are solar-integrated modules gaining popularity?

Chronic load-shedding and a 8.97 GW national PV base encourage customers to choose factory-fitted photovoltaic roofs that keep buildings operational during outages.

Which city offers the highest growth potential?

Cape Town records the fastest 8.88% CAGR through 2031 as green-building rules and an acute housing backlog spur modular adoption.

How does public procurement affect vendors?

The new Public Procurement Act’s tech-driven transparency raises compliance hurdles but could favor prefab firms that provide standardized, data-rich project documentation.

Page last updated on: