Data Historian Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

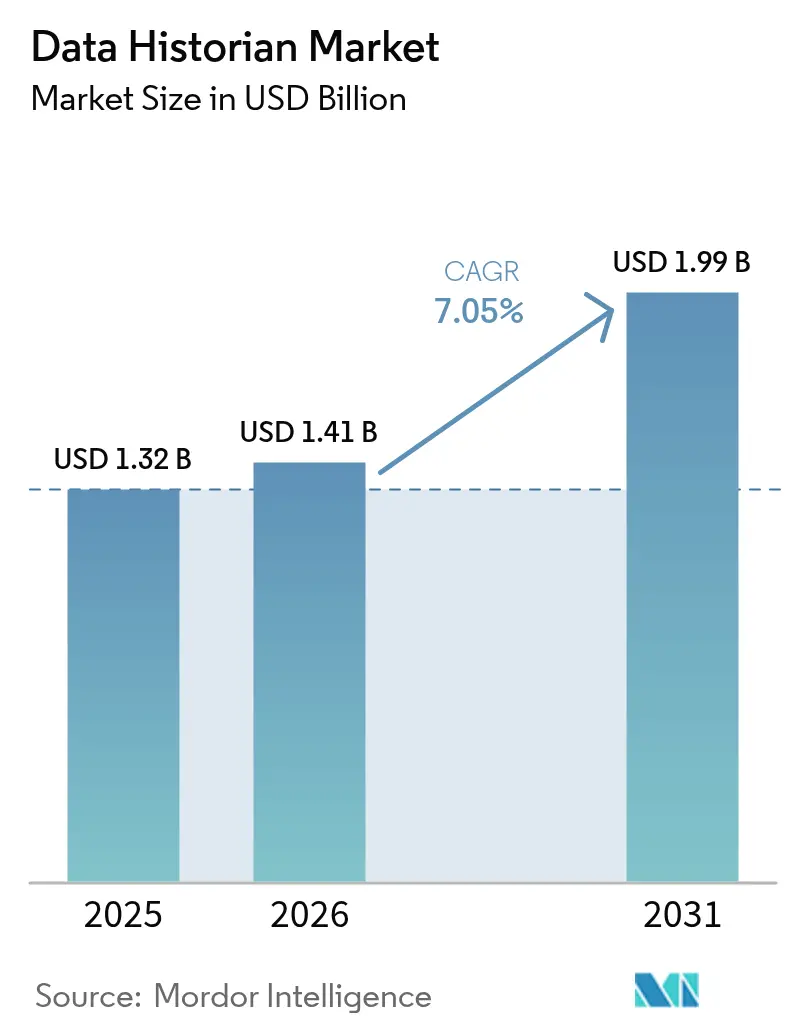

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

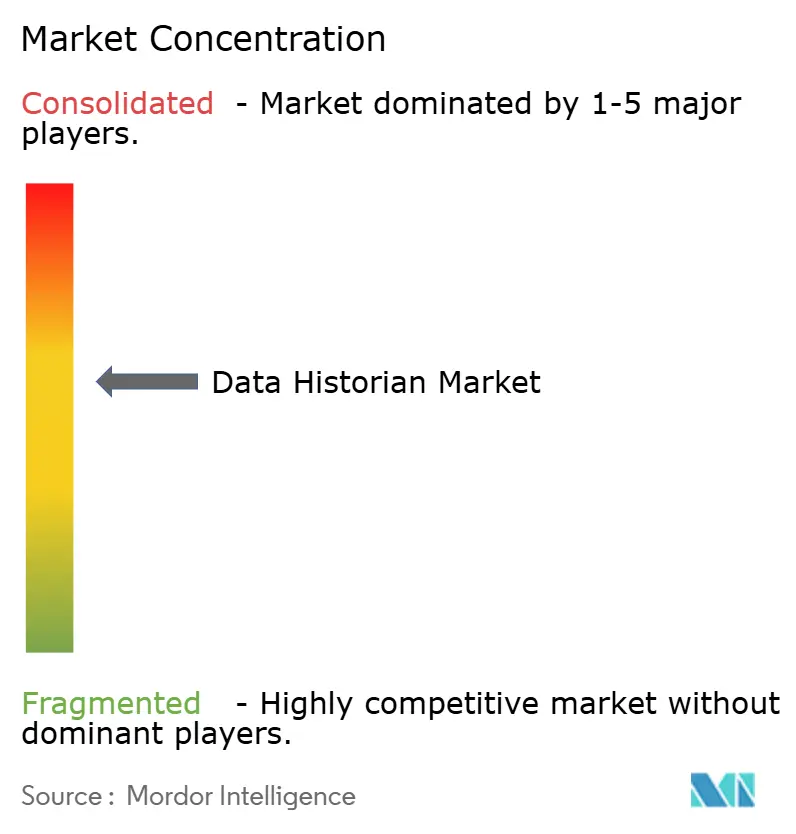

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Historian Market Analysis by Mordor Intelligence

The data historian market size in 2026 is estimated at USD 1.41 billion, growing from 2025 value of USD 1.32 billion with 2031 projections showing USD 1.99 billion, growing at 7.05% CAGR over 2026-2031. Growing convergence of operational-technology and information-technology environments, widespread industrial IoT roll-outs, and the need for real-time analytics are reshaping procurement priorities within the data historian market gevernova. Vendors are modernizing portfolios around cloud-native architectures that scale elastically, support AI/ML workflows, and satisfy stringent cybersecurity mandates. Early adoption across North American oil & gas and power generation facilities validated return-on-investment, while Asia-Pacific manufacturers, unencumbered by legacy systems, are now deploying cloud-first solutions that streamline enterprise-wide visibility. Services revenue is gaining momentum as end users require expert support for historian migration, cybersecurity hardening, and data-governance program design. Finally, competitive intensity has increased as incumbents accelerate M&A to deliver end-to-end data value chains that integrate collection, context, analytics, and visualization.

Key Report Takeaways

- By component, software captured 65.60% of the data historian market share in 2025, while services is projected to grow at 8.85% CAGR through 2031.

- By deployment mode, on-premise led with 70.90% share in 2025; cloud deployment is advancing at an 8.20% CAGR to 2031.

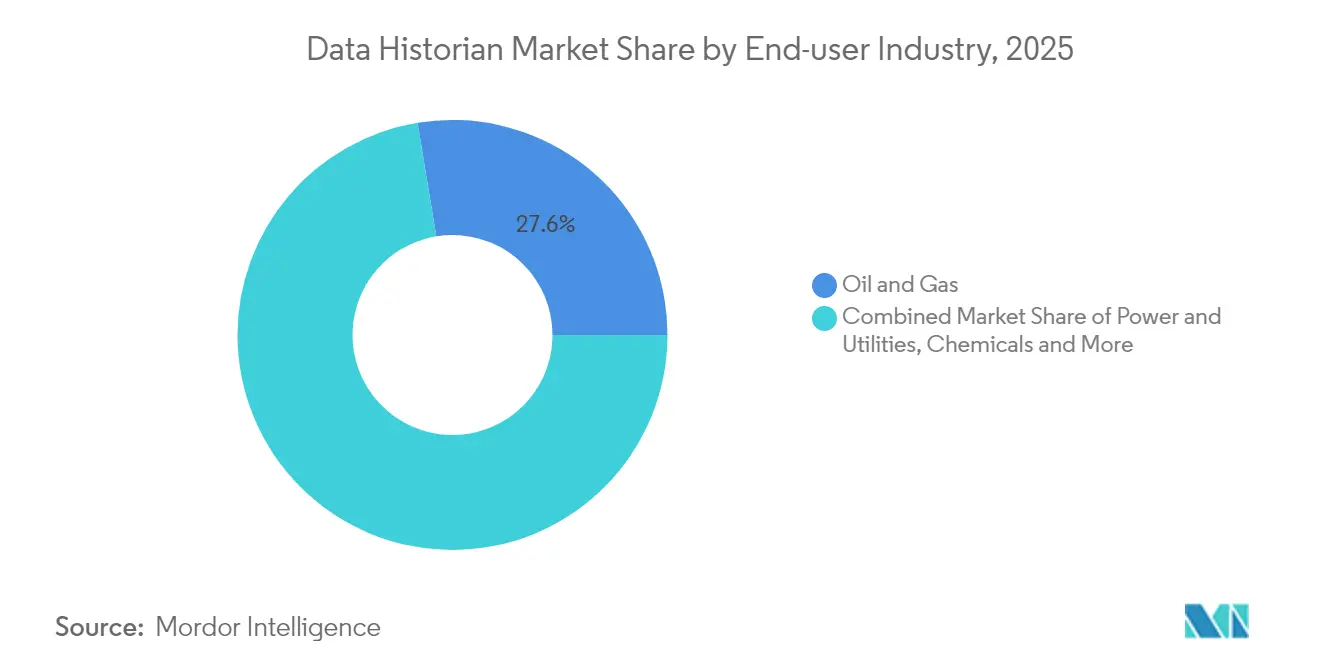

- By end-user industry, oil and gas held 27.60% of the data historian market size in 2025 and data centers are expanding at 8.75% CAGR.

- By data frequency, real-time collection accounted for 51.60% share of the data historian market size in 2025, while near-real-time collection leads growth at 7.65% CAGR.

- By geography, North America commanded 35.10% revenue share in 2025; Asia-Pacific is recording the fastest CAGR at 8.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Historian Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for consolidated data | +1.8% | Global | Medium term (2-4 years) |

| Rising volumes of industrial IoT big data streams | +2.1% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Migration of legacy historians to cloud-native architectures | +1.5% | North America & EU | Medium term (2-4 years) |

| Vendor bundling of historian inside full-stack OT platforms | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Consolidated Data to Optimize Industrial Performance

Manufacturing groups are replacing siloed storage silos with unified historian platforms that merge production, maintenance, and quality datasets. Procter & Gamble’s adoption of GE Vernova’s cloud historian illustrates a 50% reduction in process-setup time through integrated asset and ERP data streams. Contextual data-modeling now automatically links disparate tags, helping operators pinpoint upstream causes of downstream quality deviations and report sustainability metrics with audit-ready lineage.

Rising Volumes of Industrial IoT Big Data Streams

Smart-sensor proliferation is lifting ingestion rates from thousands to millions of tags per second, straining traditional monolithic databases. China’s industrial output expanded 5.6% year-on-year in May 2024, accompanied by a 10.0% surge in high-tech manufacturing, underscoring rapidly growing data loads that require compression algorithms and edge-analytics nodes.[1]National Bureau of Statistics of China, “Industrial Production Operation in May 2024,” stats.gov.cnVendors are responding with containerized micro-services that auto-scale and route non-critical packets to tier-two storage, preserving bandwidth at remote facilities.

Migration of Legacy Historians to Cloud-Native, Micro-Service Architectures

Plants are decommissioning rigid on-premise systems in favor of elastic, API-first platforms that dovetail with AI workbenches. Emerson’s “Project Beyond” epitomizes this shift by embedding software-defined control and historian functions inside a single operations layer.[2]Emerson, “Emerson’s ‘Project Beyond’ to Modernize and Seamlessly Integrate the Industrial Automation Technology Stack,” emerson.com DevOps pipelines now automate deployments, accelerate feature roll-outs, and enforce policy-as-code to satisfy regional data-sovereignty requirements.

Vendor Bundling of Historian Functionality Inside Full-Stack OT Platforms

Automation majors are integrating historian engines into PLCs, HMIs, and industrial PCs to simplify procurement and tighten security domains. Schneider Electric’s Modicon M660 IPC embeds edge analytics alongside motion control, giving users preconfigured historian templates for faster commissioning. Unified stacks reduce interface fragmentation, lower maintenance costs, and enable domain-specific blueprints for life-sciences, chemicals, and utilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for enterprise historian roll-outs | -1.4% | Global | Short term (≤ 2 years) |

| Cybersecurity concerns over exposing OT data | -0.9% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Enterprise-Wide Historian Roll-Outs

End-to-end projects require licenses, specialized hardware, integration services, and ongoing upgrades that can inflate capital outlays by 300%. Rockwell Automation’s FY 2024 results revealed a 21% revenue decline, reflecting hesitation to commit fresh budgets amid macro uncertainty. Hidden costs include tag rationalization, data cleansing, performance tuning, and workforce upskilling, constraining adoption among mid-tier manufacturers.

Cybersecurity Concerns Over Exposing OT Data to IT Networks/Cloud

Converged environments widen attack surfaces, prompting operators to keep mission-critical tags on-premise. ISA’s 2024 white paper highlights gaps between standard IT frameworks and IIoT realities, urging new reference models for edge-cloud protection.[3]International Society of Automation, “ISA White Paper on IIoT Systems Addresses Unique Cybersecurity Needs,” isa.org Sectors under heavy regulation remain cautious until zero-trust architectures, secure tunnels, and deterministic firewalls prove capable of safeguarding service availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Platform Consolidation

Software accounted for 65.60% of the data historian market share in 2025, validating preference for unified suites that blend collection, storage, analytics, and visualization. Vendors increasingly deliver subscription models that bundle time-series compression, asset models, and no-code dashboards, reducing tool sprawl inside plant networks. The services segment is advancing at a 8.85% CAGR through 2031 as operators enlist integration partners for OT-IT convergence, cybersecurity patching, and AI pipeline orchestration. HighByte’s USD 12 million financing round showcased investor appetite for Industrial DataOps services that unlock historian data across multi-vendor fleets.

The data historian market size upside remains tied to managed-services adoption, where providers monetize continuous optimization, model retraining, and regulatory reporting. As customers outsource historian lifecycle management, specialist consultancies deepen domain differentiation in pharmaceuticals, energy, and food & beverage, boosting recurring revenue visibility and reinforcing the platform-plus-services paradigm of the data historian market.

By Deployment Mode: Cloud Acceleration Challenges On-Premise Leadership

On-premise deployments retained 70.90% of the data historian market in 2025 due to latency sensitivity, sovereignty mandates, and ingrained procurement habits in hazardous industries. Plants continue to upgrade rack-mounted appliances, deploy redundant fail-over clusters, and maintain air-gapped backup nodes. Simultaneously, cloud instances are gaining 8.20% CAGR as CIOs pursue elastic capacity, managed security postures, and micro-service agility. Regulatory bodies now publish guidance on hosting process data in approved public regions, diminishing historical barriers.

Hybrid topologies are becoming mainstream in the data historian market as organizations stream low-frequency tags to the cloud while preserving real-time loops locally. Cloud vendors provide edge gateways with deterministic fail-safe modes, encouraging shift-and-lift of historical datasets for AI model training. Over the forecast horizon, total cost of ownership comparisons will continue to favor consumption-based billing, hastening workload migration in discrete manufacturing and fast-growing electrification verticals.

By End-User Industry: Data Centers Emerge as High-Growth Application

Oil & gas held 27.60% of the data historian market size in 2025, leveraging historians for reservoir optimization, emissions compliance, and predictive maintenance across distributed assets. Multi-site macro architectures integrate SCADA alarms, environmental sensors, and vibration analytics, requiring petabyte-scale storage. Conversely, data centers represent the fastest-growing segment at 8.75% CAGR, driven by hyperscale AI clusters seeking thermal-efficiency gains. Siemens has earmarked USD 10 billion for US manufacturing and AI-centric projects to serve this demand.

Rising power densities compel data-center operators to instrument every cooling loop and UPS string, feeding sub-second tags into high-availability historians that forecast hot-spot formation. This shift widens addressable opportunities for vendors offering packaged energy dashboards, carbon accounting modules, and ML-based failure prediction. Adjacent growth stems from chemicals, pharmaceuticals, and utilities modernizing legacy environments to satisfy net-zero pledges and stringent validation reporting.

By Data Frequency: Real-Time Dominance Reflects Operational Criticality

Real-time (sub-second) collection captured 51.60% of the data historian market share in 2025, emphasizing mission-critical process control. Steam crackers, rolling mills, and microelectronics fabs rely on deterministic performance to circumvent safety trips and yield losses. Systems employ memory-resident buffers, lossless compression, and redundant pairs to meet zero-data-loss objectives.

Near-real-time (1 second – 1 minute) feeds are registering 7.65% CAGR through 2031, bolstered by condition-monitoring, batch analytics, and remote diagnostics. Hitachi and NTT’s 600 km real-time synchronization trial demonstrated long-haul data consistency for disaster recovery, validating cross-site historian replication. Batch/periodic polling retains relevance for environmental compliance and quality sampling, yet vendors increasingly unify all frequencies under single tag-licensing models to streamline administration within the data historian market.

Geography Analysis

North America dominates the data historian market with 35.10% share in 2025, underwritten by large installed bases in oil & gas, power generation, and automotive assembly. Federal infrastructure programs and workforce modernization grants accelerate retrofits of aging DCS nodes into API-enabled historians. Siemens’ USD 10 billion investments in Texas and California illustrate how OEM manufacturing and AI data-center growth reinforce domestic demand.

Asia-Pacific delivers the fastest CAGR at 8.25% through 2031 on the back of China’s data-economy blueprint and Japan’s advanced robotics initiatives. Hitachi and Microsoft plan to upskill 50,000 staff in generative-AI methodologies, highlighting the human-capital dimension of historian adoption. Indian policy incentives for semiconductor fabs and electric-vehicle battery plants further enlarge the regional pipeline of green-field historian installations. Also, Beijing’s three-year action plan targets 20% annual data-industry growth and over 300 use-case demonstrations, highlighting strong policy support. Europe maintains steady contributions under reinforced GDPR 2024 mandates that formalize retention, audit, and transfer rules.

Europe records moderate growth as revised GDPR provisions and the Digital Operational Resilience Act compel firms to prove lineage, access controls, and immutability of industrial data. Energy-intensive industries adopt historians to certify carbon-footprint disclosures, while EU investment in hydrogen value chains triggers demand for high-frequency data capture across electrolyzer fleets. Emerging economies in Latin America, Middle East, and Africa remain nascent yet attractive long-term opportunities as they install new process plants without legacy constraints, enabling direct leapfrog to cloud-ready historian topologies within the data historian market.

Regulatory Landscape

Industrial data historian deployments are increasingly shaped by OT cybersecurity guidance and machinery safety rules that extend to software-enabled control environments. In the United States, NIST updated its OT security direction with NIST SP 800-82 Revision 3 and continued manufacturing-sector implementation work through NIST IR 8183 Revision 2 (Cybersecurity Framework 2.0 Manufacturing Profile). Asset owners use these documents to benchmark access control, segmentation, and monitoring practices for historian-connected ICS networks.

In Europe, Machinery Regulation (EU) 2023/1230 establishes a new compliance baseline for machinery placed on the market, with staged milestones ahead of full application in January 2027. For historian vendors and integrators supporting machine builders and regulated plants, the regulation increases the focus on secure-by-design connectivity, software update governance, and evidence retention for audit trails. IEC 62443 (including IEC PAS 62443-1-6:2025 guidance for IIoT applications) continues to be a common technical reference for IACS security controls tied to historian data flows.

Value Chain Analysis

The data historian value chain begins with data generation and connectivity (sensors, PLC/SCADA/DCS, gateways), then moves through ingestion and normalization (protocol adapters, OPC UA/MQTT connectors), core historian software (time-series storage, compression, buffering, replication), and application consumption layers (asset models, dashboards, analytics, AI/ML workbenches, and reporting). Systems integrators and OT service providers cover steps such as tag rationalization, migration of legacy archives, and validation in regulated environments, while hyperscalers and database providers increasingly participate where cloud-side analytical stores and lakehouses complement plant-side historians.

A key value-chain bottleneck is context, translating high-speed tags into governed, reusable information models that can feed MES/ERP and AI tools. This has supported Industrial DataOps middleware patterns and hybrid stacks, where on-premise historians remain close to operations while data management layers handle model governance and cross-system harmonization. Implementations and platform releases in 2025-2026 also pointed to sustained demand for bulk archive migration, multi-vendor connectivity, and bridging between Level 2 operations data and enterprise applications, supporting ongoing services and tooling needs around integration, security hardening, and lifecycle management.

Competitive Landscape

The data historian market displays moderate concentration as multi-discipline automation vendors embed historian engines into unified OT platforms to defend share against cloud-native challengers. AVEVA, Honeywell, Siemens, and GE Vernova leverage decades of domain knowledge and service footprints, reinforcing customer stickiness through template libraries and lifecycle agreements. Emerson’s buy-out of AspenTech strengthens its software-defined control ambitions, integrating advanced analytics and planning functions into one programmable environment.

Strategic consolidation extends downstream: CAI Software acquired Parsable to merge connected-worker insights with historian data, aiming to reduce mean-time-to-resolution via guided workflows. Start-ups differentiate through open-standards connectors, subscription pricing, and rapid deployment kits that minimize capital expenditure. Competitive success hinges on three capabilities: AI model orchestration, secure edge-to-cloud pipelines, and industry-specific compliance packages. Vendors that master these levers will capture the incremental spend as enterprises transition to predictive, autonomous operations.

Data Historian Industry Leaders

General Electric Company

Siemens AG

ABB Group

Honeywell International Inc.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in modernization programs that decouple operational historization from analytics while preserving deterministic plant performance and regulatory traceability. One widely cited 2026 design pattern uses on-premise historians for operations and cloud-side analytical stores (time-series platforms and lakehouse architectures) for broader AI and enterprise workloads, which creates opportunities for secure edge gateways, bidirectional replication, and policy-driven data routing across hybrid deployments.

AI-enabled operations and governance are also expanding purchase criteria beyond storage and trending. Honeywell commercialized an AI control room assistant that merges historical and real-time operational data, and several vendors are advancing roadmap items such as MQTT-based auto-configuration and managed-database integrations for PI System infrastructure. Separately, manufacturing digital programs increasingly quantify cost-saving targets, including IoT Analytics 2026 process-manufacturing organizations targeting 12% annual plant operating cost savings via digital transformation, which raises the requirement for historians that can support contextualization, standardized information models, and auditable data lineage as prerequisites for scaling analytics and AI across multiple sites.

Recent Industry Developments

- June 2026: Honeywell launched Safety Suite 2.0 with expanded historical data, dashboards, and forecasting capabilities for gas detection fleets. The upgrade strengthens historian-adjacent use cases in safety and compliance by turning fleet telemetry into longer-horizon, auditable trends and actionable insights across sites.

- May 2025: Hitachi launched a product traceability solution that unifies historian feeds and no-code device connectivity to strengthen quality and risk management. The release supports faster deployment of cross-line genealogy and compliance reporting, expanding historian pull-through into manufacturing execution and quality workflows.

- September 2024: CAI Software acquired Parsable, adding connected-worker capabilities to its manufacturing execution suite. The deal improves the ability to link frontline digital work instructions and observations with historian-derived events, tightening closed-loop improvement across operations, maintenance, and quality.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the data historian market covers commercial software and related services that capture, compress, store, and retrieve time-stamped operational data from industrial assets for fast analysis and visualization. Coverage includes on-premises, edge, and cloud-native deployments offered through licenses or subscriptions.

Scope exclusions: We exclude generic time-series databases used only for IT logs, website analytics, or consumer app telemetry.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Mode

- On-premise

- Cloud

- By End-user Industry

- Oil and Gas

- Power and Utilities

- Chemicals and Petrochemicals

- Pulp and Paper

- Metals and Mining

- Water and Waste-water

- Data Centers

- Food and Beverages

- Pharmaceuticals

- By Data Frequency

- Real-time (<1 sec)

- Near-real-time (1 sec - 1 min)

- Batch / Periodic (>1 min)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- APAC

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of APAC

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public signals on where historians sit in industrial automation, and how quickly end users are adding connected assets. We reviewed material such as US Energy Information Administration statistics, National Institute of Standards and Technology guidance on industrial cybersecurity, and IEEE publications on time-series data handling, which helped anchor typical data capture rates and reliability expectations.

We then used sources such as regulatory and standards bodies (for example ISA and IEC publications), selected patent databases, and public procurement and project announcements to map adoption patterns across process industries. Company filings, investor presentations, and reputable press were also used to verify product positioning and typical go-to-market models (license, subscription, and services). For financial cross-checks, we used a paid subscription for company financials and news intelligence. This list is not exhaustive, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what desk research could not show cleanly, namely how deployments are actually scoped and priced across plants and regions. We spoke with a mix of automation stakeholders and software users (including operations, OT/IT integration, and plant digital teams) to confirm typical deal structures, service attachment, and migration pace from on-premises to hybrid and cloud.

For a global market like this, conversations were balanced across APAC, EMEA, and the Americas so adoption signals from manufacturing-heavy and energy-heavy clusters were not over-weighted in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 41% |

| Mid tier: 47% | Functional/Unit leaders: 28% | EMEA: 36% |

| Smaller Players: 18% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where industrial automation and software spending indicators were reconstructed into a realistic demand pool for historian deployments, then narrowed using adoption and replacement rates discussed by practitioners. In parallel, selective bottom-up checks were run using sampled average selling price ranges, typical plant-level node counts, and service attachment assumptions, which are then used to adjust totals when results drifted away from observable buying patterns.

Key inputs in the model included the installed base trend of connected industrial assets (PLCs, SCADA, and DCS environments), the pace of IIoT sensor additions, license versus subscription mix, typical upgrade and migration cycles, and average project scope (single site versus multi-site rollouts). We also tracked the share of spend that lands in services for integration and ongoing support, since that often varies by industry and region. Where bottom-up visibility was limited, gaps were handled by using conservative ranges and then tightening those ranges using interview feedback and publicly visible project signals.

For forecasting, we used scenario analysis supported by variable-level expectations from experts, which helped keep the outlook practical when macro conditions change. Growth cases were stress-tested using inputs such as industrial production outlooks, digitalization budgets, and cybersecurity-driven modernization activity, before the final year-by-year curve was locked.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, before the final numbers were approved. We compared implied spend per site and per deployment against what interviews described as typical, and we reviewed year-on-year movements to flag jumps that were not supported by adoption or pricing logic.

Anomalies are reviewed in more than one step, including peer analyst checks and targeted re-contacts when assumptions look too optimistic or too conservative. Reports are refreshed annually, and interim updates are made when material events shift adoption, pricing, or deployment models. Before delivery, an analyst does a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Data Historian Market Size Compared Against Other Published Estimates

Published market values for data historians can differ because each publisher chooses its own product boundary, pricing basis, and timing for currency and inflation assumptions. Some studies also blend adjacent software categories into the same total, which makes comparisons confusing unless the inclusions are clearly stated.

Installed base signals from industrial automation environments, combined with deal-structure checks from interviews, are the evidence that keeps Mordor Intelligence's USD 1.41 B (2026) estimate focused on historian software plus related services, instead of expanding into broader IoT platforms or general IT observability tooling.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.41 B (2026) | |

| Regional Consultancy A | USD 1.45 B (2024) | This figure appears to time-shift the market to an earlier year and can mix in near-real-time data infrastructure that sits outside industrial historian deployments, which changes the boundary and the pricing base. |

| Industry Association B | USD 1.74 B (2024) | This estimate likely adds adjacent IoT platform modules and applies broader digital transformation growth multipliers, which can inflate totals versus a historian-only scope with services counted only when tied to historian rollouts. |

The spread across published numbers is mainly explained by category overlap and timing choices, not by a disagreement that historians are growing steadily. By keeping the scope tied to identifiable historian deployments and by applying repeatable checks on adoption, pricing, and services attachment, we deliver a market total that is easier to trace and easier to update as conditions change.

Key Questions Answered in the Report

What is the current size and projected growth rate of the global data historian market?

The market stands at USD 1.41 billion in 2026 and is expected to reach USD 1.99 billion by 2031, reflecting a 7.05% CAGR.

Which component segment is expanding the fastest?

Services is the quickest-growing component, advancing at a 8.85% CAGR as enterprises seek expert support for OT-IT integration, cybersecurity, and AI enablement.

Why are cloud deployments gaining traction despite on-premise dominance?

Cloud-native platforms offer elastic scalability, automatic updates, and easier integration with modern analytics, driving an 8.20% CAGR even though on-premise still holds 70.90% share.

Which end-user industry shows the strongest growth outlook?

Data centers lead with a 8.75% CAGR through 2031, as hyperscale operators use historian data to optimize cooling, predict failures, and manage rising AI workloads.

What primary factors are boosting adoption of historian platforms?

Key drivers include the need for consolidated operational data, surging industrial IoT data streams, migration to cloud-native architectures, and vendor bundling of historian functions within full-stack OT suites.

How significant are cybersecurity concerns for cloud historian adoption?

Cybersecurity remains a chief restraint, cutting forecast CAGR by 0.9 percentage points as critical-infrastructure operators weigh data-sovereignty and threat-landscape risks before moving OT data to the cloud.

Page last updated on: