Sonar Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

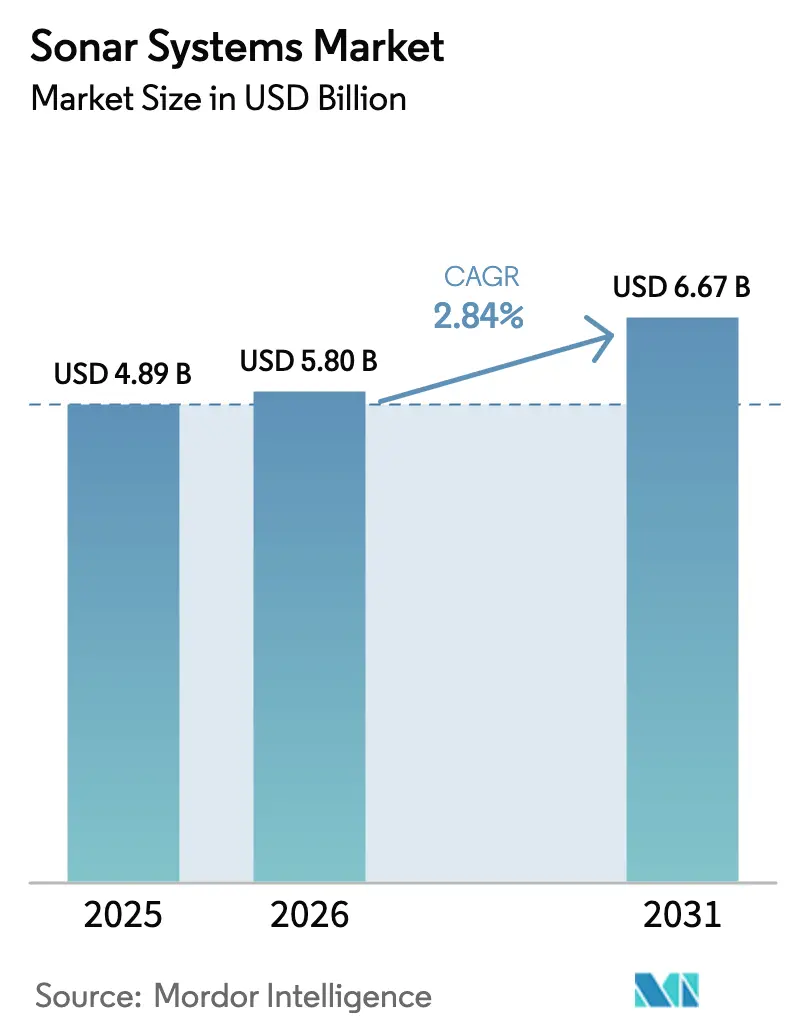

| Market Size (2026) | USD 5.80 Billion |

| Market Size (2031) | USD 6.67 Billion |

| Growth Rate (2026 - 2031) | 2.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

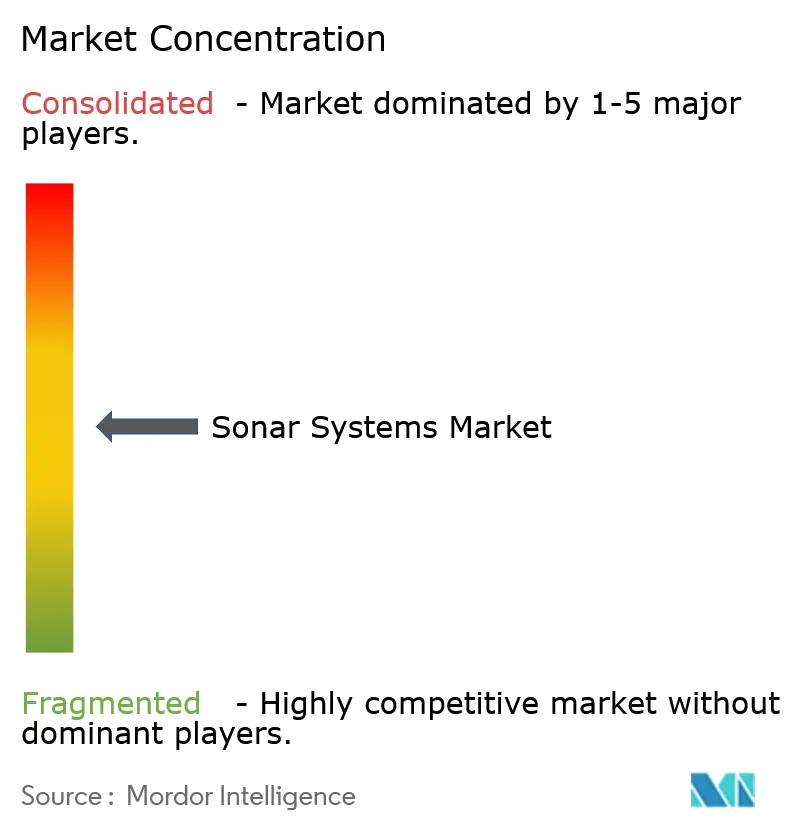

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sonar Systems Market Analysis by Mordor Intelligence

The sonar systems market size is expected to grow from USD 4.89 billion in 2025 to USD 5.80 billion in 2026 and is forecasted to reach USD 6.67 billion by 2031 at a 2.84% CAGR over 2026-2031. This modest headline growth conceals a structural shift, as procurement budgets shift from large, hull-mounted hardware toward software-defined acoustic arrays and autonomous vehicles that deliver more exhaustive coverage at lower lifecycle costs. [1]Source: Department of the Navy, “FY 2025 Budget Estimates,” SECNAV.NAVY.MIL Navies are steering funds toward edge-compute signal processing, while commercial operators use multi-static AUV fleets to shorten inspection cycles and cut vessel charter costs. Increasing offshore wind construction, stricter International Maritime Organization underwater-noise rules, and AI-enabled target classification continue to broaden the commercial addressable base. At the same time, persistent cyber-hardening gaps and the rise of optical or magnetic sensing alternatives keep competitive pressure high, forcing vendors to differentiate themselves through open architectures, sovereign AI software stacks, and turnkey service models.

Key Report Takeaways

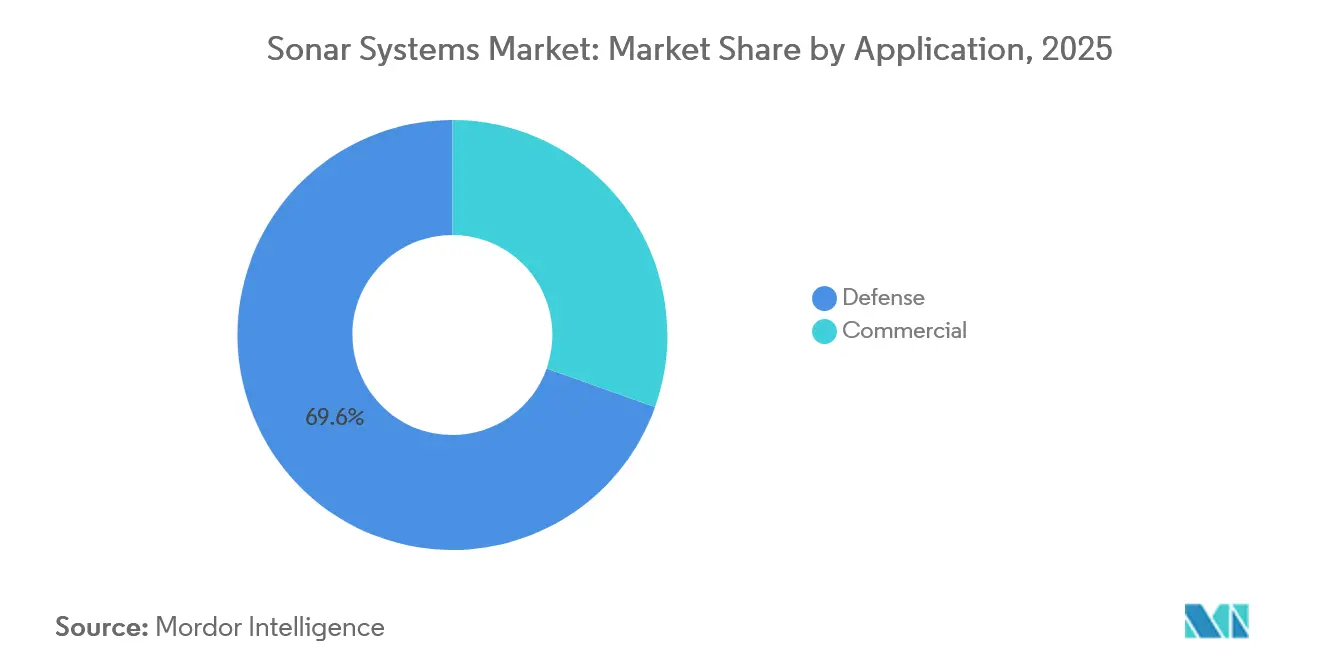

- By application, defense retained 69.87% of the sonar systems market share in 2025, while the commercial segment is projected to record the fastest 4.30% CAGR from 2026 to 2031.

- By technology, passive sonar led with 54.70% share in 2025; multi-static solutions are poised to expand at 5.10% CAGR through 2031.

- By installation platform, ship-mounted systems accounted for 47.10% of revenue in 2025, whereas unmanned platforms are expected to grow at a 6.65% CAGR through 2031.

- By mounting type, hull-mounted transducers accounted for 46.25% of the sonar systems market in 2025, and seabed nodes are projected to grow at a 6.05% CAGR through 2031.

- By frequency, mid-frequency arrays captured 47.35% revenue in 2025; high-frequency systems are forecast to post a 5.78% CAGR to 2031.

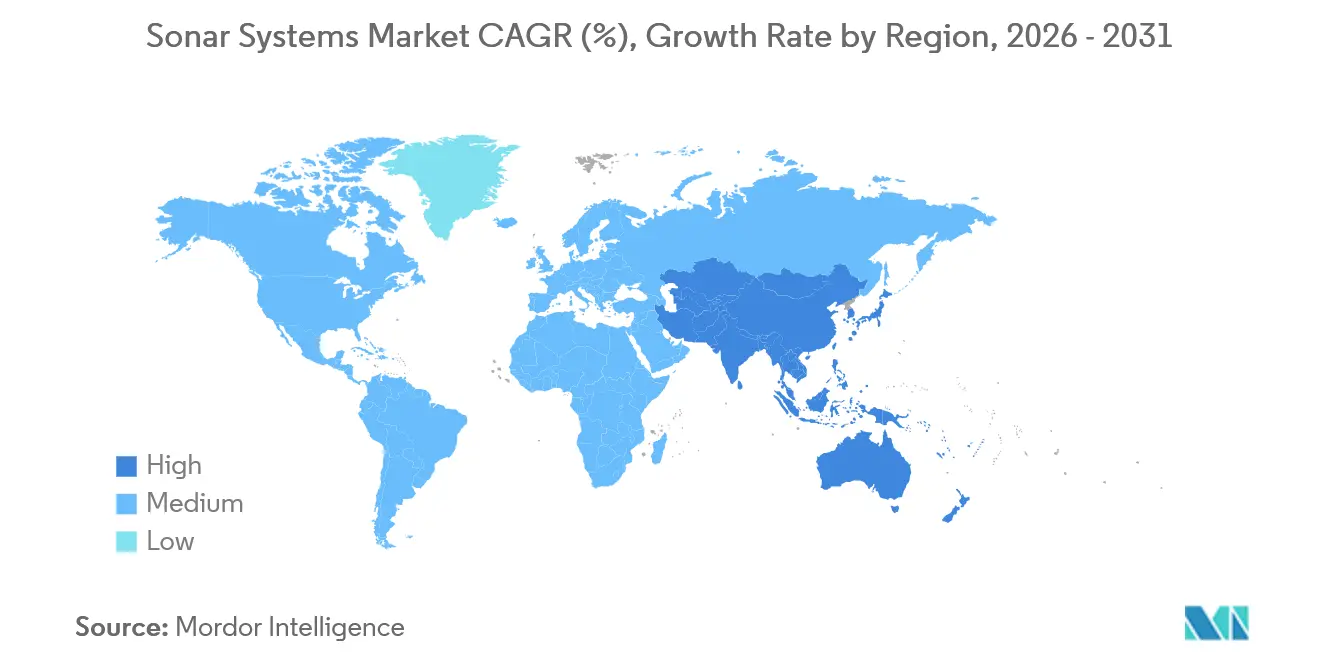

- By geography, North America accounted for 36.98% of revenue in 2025, while the Asia-Pacific region is expected to grow at the fastest 4.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sonar Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naval fleet modernization programs | +0.9% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Expanding offshore energy exploration | +0.5% | North Sea, Gulf of Mexico, Brazil, Southeast Asia | Medium term (2-4 years) |

| Protecting critical subsea energy infrastructure | +0.4% | Europe, Middle East, Asia-Pacific | Short term (≤2 years) |

| Surge in unmanned underwater vehicles (UUVs) | +0.7% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Integrating AI for signal processing | +0.6% | Global, led by North America and Europe | Long term (≥4 years) |

| Mandatory IMO-2028 underwater noise limits | +0.3% | Early adoption in Europe and North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Naval Fleet Modernization Programs

Cold-War era arrays are being replaced with modular, software-defined systems that slot into network-centric architectures. The US Navy allocated USD 57.5 million to Undersea Warfare Applied Research and USD 53.6 million to Acoustic Search Sensors in FY 2025, indicating a priority for incremental sonar upgrades over new hulls. AUKUS nuclear-powered submarines and Japan’s expanded Maritime Self-Defense Force orders further amplify demand for through-life support, flank arrays, and training infrastructure across the Asia-Pacific. Programs such as the Mk 48 torpedo Advanced Processor Build 6, slated for its first operational use in 2026, demonstrate how navies are embedding AI inference at the edge to extend the life cycles of legacy platforms and reduce their dependency on satellite bandwidth. As more fleets opt for retrofit paths, vendors with open-architecture firmware and sovereign-compute credentials strengthen their foothold.

Expanding Offshore Energy Exploration

Deepwater oil operators are shifting to AUV patrols equipped with synthetic-aperture and side-scan sonar because weather downtime hinders surface vessels. Equinor reduced pipeline survey time in the North Sea from 14 days to 5 days, resulting in a 60% decrease in vessel costs by 2025. [2]Source: Equinor ASA, “Annual Report 2025,” EQUINOR.COM Offshore wind developers, especially in Europe and the United States, mandate high-resolution multibeam surveys to map boulder fields and unexploded ordnance before construction begins. Fisheries deploy split-beam echosounders coupled with convolutional neural networks to separate quota species from bycatch in real time, helping avoid fines. Aquaculture cages utilize similar arrays to monitor biomass density and detect net tears, ensuring optimal feed usage and environmental compliance. Together, these moves expand the sonar systems market beyond its historical naval core.

Protecting Critical Subsea Energy Infrastructure

The 2022 Nord Stream incident prompted Norway to allocate USD 140 million in 2024 for seabed-mounted acoustic sensors around strategic pipelines. Middle Eastern desalination plants and LNG export terminals are adding perimeter arrays that alert operators to diver delivery vehicles in seconds, rather than minutes. The US Navy’s USD 15.9 million MEDUSA contract demonstrates interest in modular UUVs that patrol chokepoints for up to 30 days. Persistent nodes slash operating expenditure by roughly 50% versus crewed patrol craft, making continuous coverage financially viable even for mid-tier asset owners.

Surge in Unmanned Underwater Vehicles (UUVs)

Huntington Ingalls Industries secured a USD 347 million ceiling under the Lionfish program to supply REMUS 300 vehicles through 2028. The Large Displacement UUV initiative selected Oceaneering, Kongsberg, and Anduril for prototypes that will deploy from Virginia Payload Module tubes. The United Kingdom placed USD 13.4 million with M Subs for its CETUS extra-large UUV, mirroring allied demand for unmanned mine countermeasure systems. Commercial survey firms are moving to rental models that package AUVs, multibeam sonar, and data analytics on a per-survey fee, removing the USD 50,000-per-day burden of a crewed vessel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and lifecycle costs | -0.6% | Budget-constrained navies and emerging markets | Medium term (2-4 years) |

| Spectrum-management and licensing hurdles | -0.3% | Global, variable by EEZ | Short term (≤2 years) |

| Rising efficacy of non-acoustic detection | -0.4% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Cyber-hardening gaps in legacy platforms | -0.5% | Global aging fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Costs

A single frigate sonar suite costs more than USD 20 million and requires another 60% of that figure for support over 25 years. [3]Source: National Oceanic and Atmospheric Administration, “Marine Mammal Protection Regulations,” FISHERIES.NOAA.GOVSmaller navies defer upgrades to fund multi-role patrol vessels, thereby reducing their anti-submarine capacity. Commercial multibeam rigs range from USD 500,000 to USD 1 million, with annual calibration consuming 10%-15% of the list price. Leasing and service-bundle models lower entry costs but shift operators into recurring fees. Software-defined arrays promise 30% lifecycle savings, yet they require an upfront integration commitment that legacy systems often cannot support.

Spectrum-Management and Licensing Hurdles

Active sonar shares bands with marine mammal communications, triggering environmental impact assessments that delay projects up to two years. European operators must align with the Marine Strategy Framework Directive, incorporating multi-agency permitting layers. Hydrographic firms submitting frequency requests across multiple exclusive economic zones face weeks of administrative lag, compressing exploration windows and raising mobilization costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Defense Dominance Persists While Commercial Momentum Builds

Defense accounted for 69.87% of the sonar systems market size in 2025 and is expected to remain the largest segment, as anti-submarine warfare, mine detection, and port security missions continue to receive funding priority. The commercial segment is projected to register a 4.30% CAGR because offshore energy companies now treat high-resolution seabed data as an operational necessity rather than an optional cost line. Unmanned patrols enable navies and oil majors to achieve 24/7 coverage without exposing crews to contested waters, thereby supporting the broader adoption of this technology across both customer groups.

AUV-based synthetic-aperture sonar surveys saved Equinor six ship days per pipeline inspection in 2025, prompting similar operators to add contract capacity for 2026 campaigns. Fisheries and aquaculture use split-beam arrays with real-time species recognition to cut bycatch penalties. Despite the faster expansion on the civil side, high R&D barriers and export-control hurdles will keep defense in control of absolute revenue through 2031.

By Technology: Passive Listening Leads as Multi-Static Strategies Accelerate

Passive arrays delivered 54.70% of 2025 revenue, reflecting the enduring need to detect adversaries while remaining silent. Multi-static architectures, where separated transmitters and receivers triangulate faint diesel-electric returns, are forecast to grow at a 5.10% CAGR. This uptick positions multi-static tools as the fastest-advancing technology segment in the sonar systems market.

MEDUSA UUVs will coordinate distributed nodes to cover chokepoints without a surface escort, amplifying adoption in both green- and brown-water operations. Active sonar keeps its niche in mine countermeasures and harbor defense but must navigate stricter environmental reviews. The technology split underscores a mission-driven rather than one-size-fits-all future for the sonar systems market.

By Installation Platform: Unmanned Growth Outpaces Crewed Baselines

Ship-mounted arrays contributed 47.10% to the 2025 demand, leveraging decades of installed infrastructure and a reliable power supply. Unmanned platforms, however, are projected to expand at a 6.65% CAGR to 2031, the highest rate among all platform categories. Defense programs like Lionfish and the Large Displacement UUV create a volume pull for commercial survey firms that seek similar endurance without military security overhead.

The sonar systems market size for unmanned installations is set to widen, as service contracts bundle vehicle time, acoustic payloads, and real-time analytics into repeatable packages. Submarine-mounted flank arrays still dominate covert blue-water detection tasks, while airborne dipping sonars sustain relevance in shallow straits where mines restrict vessel traffic.

By Mounting Type: Seabed Nodes Deliver Persistent Infrastructure Oversight

Hull-mounted transducers represented 46.25% of 2025 revenue, benefitting from integrated cabling and power draw on existing hulls. Seabed nodes, expected to post a 6.05% CAGR, support continuous monitoring of pipelines and cables without surface interference. This mounting style unlocks a market share gain for sonar systems vendors that can fine-tune battery endurance and low-current electronics.

Norway’s 2024 seabed defense investment showed that a moderate capital outlay can secure wide-area assets and reduce operating expenditure by half. Nevertheless, the practicality of hull integration and simplicity of maintenance will keep hull-mounted systems as the most significant slice of the mounting sub-market over the forecast horizon.

By Frequency: High-Frequency Demand Rises in Shallow-Water Missions

Mid-frequency arrays controlled 47.35% of 2025 sales because they balance range and resolution for multi-role tasks. High-frequency systems, essential for mine countermeasures and port security, are projected to grow at a 5.78% CAGR to 2031. As offshore wind developers require centimeter-scale seabed maps, hydrographic firms rely on higher frequencies to differentiate services.

Converged processing chains cue active high-frequency beams only after passive mid-band detection, reducing environmental noise signatures and safeguarding marine life. Low-frequency SURTASS assets will remain pivotal for strategic open-ocean surveillance, but high-frequency agility dictates growth in near-shore and infrastructure-protection missions.

Geography Analysis

North America generated 36.98% of global revenue in 2025, underpinned by USD 3.9 billion in US Submarine Industrial Base funding and sustained investment in edge-compute sonar upgrades. High-volume procurement cycles and sole-source contracts give the region structural scale advantages, ensuring that the sonar systems market remains anchored in the United States through 2031.

The Asia-Pacific region is projected to register the fastest 4.75% CAGR as Australia procures nuclear-powered submarines under AUKUS, Japan expands hull-mounted deployments, and South Korea invests in mine countermeasure drones. Regional governments view seabed awareness as a prerequisite for ensuring energy security and effective enforcement of the exclusive economic zone. The sonar systems market size in the Asia-Pacific region is driven by simultaneous growth in defense and offshore energy.

Europe maintains steady replacement demand, with the UK and France upgrading their Barracuda-class flank arrays, while smaller NATO members stagger their upgrades. Norway’s pipeline protection spend highlights a shift toward seabed monitoring investments. In the Middle East, port authorities are installing perimeter arrays around desalination intakes, and Brazil’s offshore expansion is fueling South America’s modest uptick. Collectively, these geographies form a mosaic where growth hotspots revolve around maritime sovereignty and energy supply resilience.

Competitive Landscape

The sonar systems market exhibits a moderate level of concentration. Thales, RTX, L3Harris, Kongsberg, and General Dynamics leverage deep naval credentials to win long-cycle, integrated contracts. Open-architecture mandates enable smaller sensor houses and AI software vendors to secure payload slots within large programs without owning the vehicle's hull. The USD 15.9 million MEDUSA award to General Dynamics Mission Systems, which is scalable to USD 58.1 million, demonstrates that integrators can swap acoustic payloads without requiring redesign of the host platform.

Software-first entrants train deep-learning classifiers on synthetic acoustic libraries, slicing time and cost from sea trials. SBIR solicitations welcome these firms, thereby widening the vendor pool and eroding the incumbent's share. Cyber-secure firmware and hardware security modules command price premiums but require operator upskilling, tilting competition toward partners that bundle training and support.

Defense primes are responding through acquisitions and joint ventures that add AI talent and sovereign-compute footprints. Commercial service firms pivot to per-survey or per-inspection pricing, which combines sonar, vehicle, and analytics into a single invoice, increasing stickiness. The resulting landscape shifts the competitive axis from monolithic platforms to modular ecosystems.

Sonar Systems Industry Leaders

Thales Group

RTX Corporation

L3Harris Technologies, Inc.

Kongsberg Gruppen ASA

General Dynamics Mission Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Danish Ministry of Defence Acquisition and Logistics Organisation (DALO) signed a contract with TKMS Atlas Elektronik GmbH for Towed Array Sonar systems. This strategic move enhances Denmark’s anti-submarine warfare capabilities, reflecting a broader trend among European nations to invest in advanced maritime defense technologies in response to evolving underwater security challenges.

- March 2025: Thales announced its agreement with Naval Group to supply a sonar suite for the Royal Netherlands Navy's Orka-class submarines under the RNSC programme. This agreement highlights the strategic importance of advanced sonar technologies in naval modernization, strengthening Thales' market position and supporting the Netherlands' efforts to address evolving underwater threats.

Global Sonar Systems Market Report Scope

Sonar, which stands for Sound Navigation and Ranging, is a device that helps detect objects located underwater by using high-frequency sound waves. Moreover, the sound waves are transmitted from a transducer, which, after striking an object underwater, echoes back to the transducer.

The sonar systems market is segmented by application, technology, installation platform, mounting, frequency band, and geography. By application, the market is segmented into defense and commercial. By technology, the market is segmented into active, passive, and multi-static sonar. By installation platform, the market is segmented by ship-mounted, submarine-mounted, airborne, and unmanned platforms. The market is segmented by mounting type, including hull-mounted, towed array, dipping sonar, and seabed-mounted. By frequency band, the market is segmented into low-frequency, mid-frequency, and high-frequency. The report also covers the market sizes and forecasts for the sonar systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Defense | Anti-Submarine Warfare (ASW) |

| Mine Detection and Countermeasures | |

| Port Secuirty | |

| Others | |

| Commercial | Offshore Oil and Gas |

| Hydrographic Survey and Research | |

| Fisheries and Aquaculture |

| Active Sonar |

| Passive Sonar |

| Multi-static Sonar |

| Ship-mounted |

| Submarine-mounted |

| Airborne |

| Unmanned Platforms (UUV/USV) |

| Hull-Mounted |

| Towed Array |

| Dipping Sonar |

| Seabed-Mounted |

| Low-Frequency |

| Mid-Frequency |

| High-Frequency |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Defense | Anti-Submarine Warfare (ASW) | |

| Mine Detection and Countermeasures | |||

| Port Secuirty | |||

| Others | |||

| Commercial | Offshore Oil and Gas | ||

| Hydrographic Survey and Research | |||

| Fisheries and Aquaculture | |||

| By Technology | Active Sonar | ||

| Passive Sonar | |||

| Multi-static Sonar | |||

| By Installation Platform | Ship-mounted | ||

| Submarine-mounted | |||

| Airborne | |||

| Unmanned Platforms (UUV/USV) | |||

| By Mounting | Hull-Mounted | ||

| Towed Array | |||

| Dipping Sonar | |||

| Seabed-Mounted | |||

| By Frequency Band | Low-Frequency | ||

| Mid-Frequency | |||

| High-Frequency | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the sonar systems market in 2026?

The sonar systems market size reached USD 5.80 billion in 2026 and is projected to climb steadily at a 2.84% CAGR.

Which region accounts for the highest revenue?

North America led with 36.98% revenue in 2025, buoyed by sustained US Navy procurement.

Which application segment is expanding fastest?

Commercial uses such as offshore energy surveys are forecast to post the highest 4.30% CAGR to 2031.

What technology segment is gaining share most rapidly?

Multi-static sonar is expected to grow at a 5.10% CAGR as navies seek covert detection of quiet submarines.

How are IMO noise rules shaping demand?

Pending IMO-2028 caps on underwater radiated noise are pushing shipbuilders and ports to adopt calibrated passive-listening packages, creating new commercial demand.

Who are the leading vendors?

Thales, RTX, L3Harris, Kongsberg and General Dynamics Mission Systems anchor the market, while software specialists are entering via open-architecture payload slots.

Page last updated on: