Military Navigation Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.97 Billion |

| Market Size (2031) | USD 18.01 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Navigation Systems Market Analysis by Mordor Intelligence

The military navigation systems market size in 2026 is estimated at USD 12.97 billion, growing from 2025 value of USD 12.15 billion with 2031 projections showing USD 18.01 billion, growing at 6.79% CAGR over 2026-2031. Defense ministries are steadily increasing their spending on assured positioning, navigation, and timing (PNT) as unmanned platforms proliferate, while persistent jamming incidents expose the limitations of legacy Global Positioning System (GPS) receivers. The market is shifting toward hybrid architectures that blend multi-constellation Global Navigation Satellite System (GNSS), inertial sensors, and terrestrial beacons, enabling continuity of operations in contested electromagnetic environments. Quantum and MEMS-based inertial units are maturing, commercial low-Earth-orbit (LEO) PNT constellations are entering service, and export-controlled anti-jam antennas are seeing wider adoption. Incumbent primes retain scale advantages, yet software-defined solutions from startups are resetting competitive benchmarks for accuracy, size, weight, power, and cost.

Key Report Takeaways

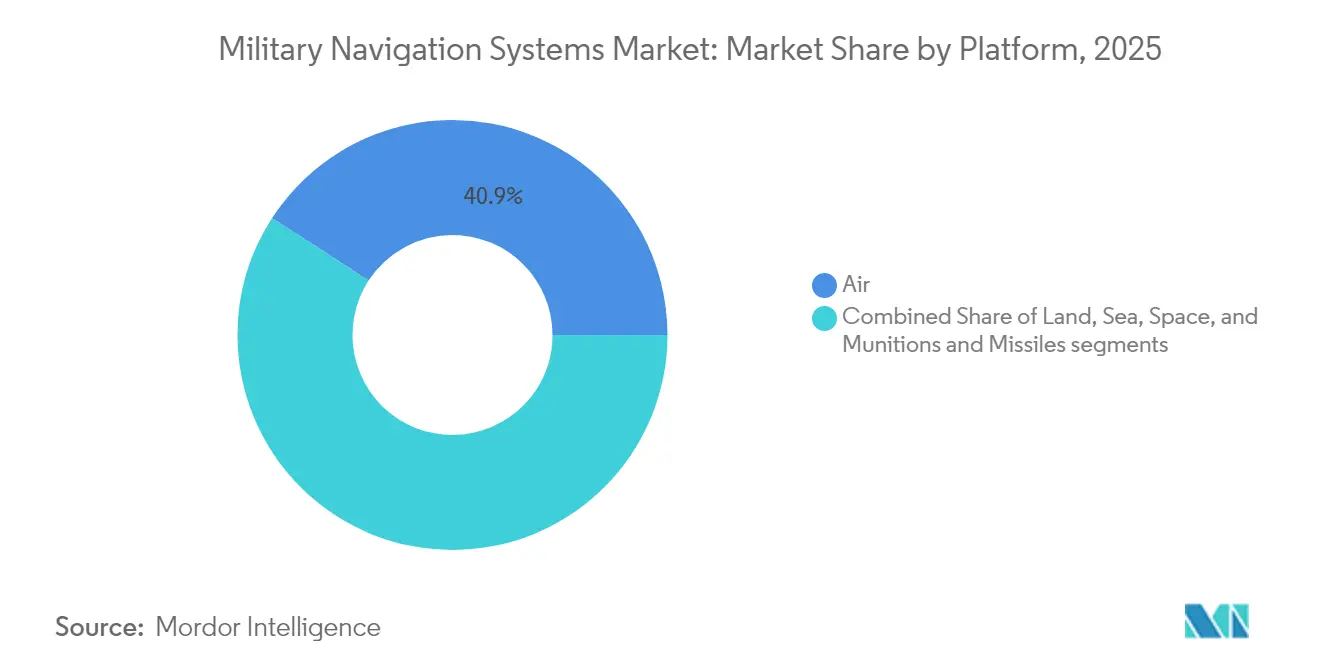

- By platform, airborne systems led the military navigation systems market with a 40.85% share in 2025, while the space segment is expected to post a 7.44% CAGR through 2031.

- By application, command and control (C2) accounted for 29.02% of 2025 revenue; search and rescue (SAR) is the fastest-growing use case at a 7.29% CAGR through 2031.

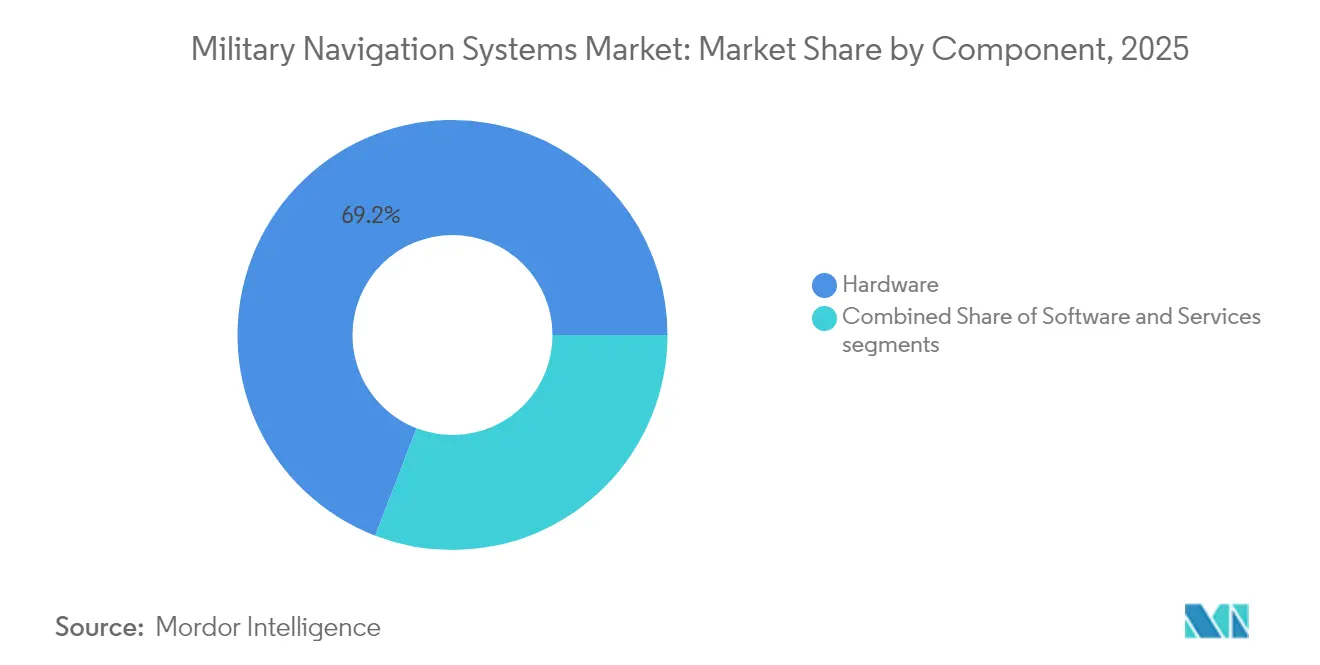

- By component, hardware retained 69.15% of 2025 sales, yet software is expanding at an 7.78% CAGR as AI-enabled sensor fusion gains traction.

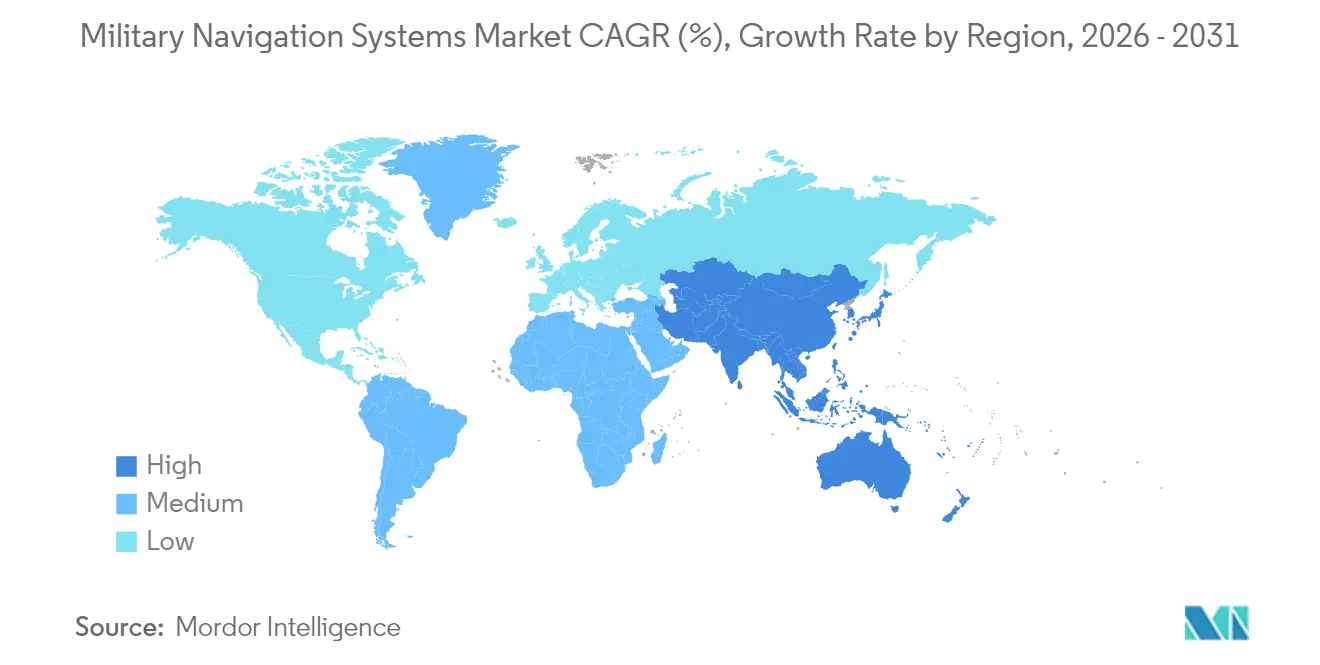

- By geography, North America captured 38.25% of the 2025 revenue, whereas the Asia-Pacific region is rising fastest at a 7.62% CAGR, driven by the integration of BeiDou, NavIC, and QZSS.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Navigation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing deployment of autonomous and unmanned military platforms | +1.4% | Global, especially North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption of anti-jam and anti-spoof GNSS navigation systems | +1.3% | Europe and the broader Indo-Pacific | Short term (≤2 years) |

| Rising defense modernization spending across Asia and the Middle East and Africa | +1.5% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥4 years) |

| Government mandates for assured PNT capabilities | +1.2% | North America, Europe, allied Indo-Pacific nations | Medium term (2-4 years) |

| Advancements in quantum and MEMS-based inertial navigation technologies | +0.9% | North America and Europe, pilot programs in Asia-Pacific | Long term (≥4 years) |

| Use of commercial LEO-based PNT constellations to enhance navigation resilience | +0.6% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Deployment of Autonomous and Unmanned Military Platforms

Surface vessels, UAVs, and robotic ground vehicles now require centimeter-grade positioning for extended periods without operator input. The US Navy’s Ghost Fleet Overlord trials demonstrated that a 72-hour GPS-denied operation requires fiber-optic gyros integrated with visual-inertial odometry.[1]U.S. Navy, “Ghost Fleet Overlord Autonomous Surface Vessel Program,” navy.mil DARPA’s Squad X robots validated similar requirements for sub-5-meter accuracy inside urban canyons. Loitering munitions must stay on course after deliberate jamming, which shifts procurement from consumer GNSS boards to tactical-grade inertial units. Vendors capable of delivering low-drift sensors in compact housings are seeing a rise in orders as autonomy becomes a standard requirement across the military navigation systems market.

Increasing Adoption of Anti-jam and Anti-spoof GNSS Navigation Systems

Electronic warfare (EW) tactics have matured, forcing armed forces to harden their receivers. Galileo’s authenticated OSNMA messages blocked spoofing attempts on civil aviation in the Eastern Mediterranean during 2024.[2]European Union Agency for the Space Programme, “Galileo OSNMA Anti-Spoofing Service,” euspa.europa.eu GPS III satellites now transmit encrypted M-Code on three bands, yet only receivers with controlled-reception-pattern antennas gain the extra 20 dB jamming margin. Raytheon and Collins Aerospace dominate fighter and armor retrofits, while NovAtel provides dual-frequency CRPA antennas to smaller fleets. The move to multi-constellation chips that blend GPS, Galileo, GLONASS, and BeiDou enhances resilience by forcing adversaries to jam four frequencies simultaneously.

Rising Defense Modernization Spending Across Asia and the Middle East and Africa

SIPRI records a 4.3% increase in Asia-Pacific defense budgets for 2024, with India, Japan, and South Korea allocating funds to sovereign navigation programs. India’s NavIC receivers are entering Tejas fighters and Arjun tanks; Japan’s seven-satellite QZSS supplies sub-meter coverage across the Indo-Pacific. Saudi Arabia and the UAE co-produce inertial units to localize sensitive supply chains. Because each constellation uses distinct codes and frequencies, integrators must certify equipment against multiple standards, thereby enlarging the addressable demand but also raising engineering complexity.

Government Mandates for Assured PNT Capabilities

The US Department of Defense (DoD) now requires critical platforms to function 30 days without GPS, elevating inertial systems from backup to primary navigation sources. NATO urges member states to adopt Galileo’s encrypted Public Regulated Service, and the UK sponsors a sovereign atomic clock under Project Aquila to protect national timing. Australia’s defense review calls for multilayer architectures that pair satellites with eLoran and quantum inertial systems. These mandates necessitate redesigns of avionics to accommodate bulkier backup sensors, thereby increasing unit cost while ensuring mission continuity in the event of jamming.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict export-control regulations governing secure and encrypted PNT technologies | –0.8% | Global, most restrictive in North America and Europe | Short term (≤2 years) |

| Dependence on limited supply chains for radiation-hardened electronic components | –0.6% | Global, severe in space and munitions segments | Medium term (2-4 years) |

| Size, weight, power, and cost limitations in dismounted soldier navigation systems | –0.4% | Global, impacts infantry programs | Short term (≤2 years) |

| Heightened cyber and electronic-warfare threats to space-based navigation infrastructure | –0.7% | Eastern Europe, Indo-Pacific, Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Strict Export-control Regulations Governing Secure and Encrypted PNT Technologies

ITAR classifies Y-code GPS receivers and high-grade inertial systems as Category XI items, which require a US State Department license for most exports. Wassenaar Arrangement amendments now capture sensors with drift better than 0.5°/h, blocking many sales to Asia and Africa.[3]Wassenaar Arrangement, “Dual-Use Export Controls List 2024,” wassenaar.org The EU applies similar curbs to Galileo PRS hardware. Vendors must operate separate civilian and military production lines with distinct firmware and audited supply chains, which increases overhead and narrows the pool of eligible buyers. Small firms lacking compliance resources cede ground to primes that can navigate legal complexities.

Dependence on Limited Supply Chains for Radiation-hardened Electronic Components

Only a handful of foundries, led by Microchip and Renesas, manufacture radiation-hardened (rad-hard) chips for space and munitions payloads. Scarce capacity stretches delivery schedules, raising costs and deferring satellite launches. Emerging economies struggle to secure priority wafers, widening capability gaps. Allied governments have funded on-shore rad-hard fabrication, but meaningful volumes will not arrive before 2028. Until then, production bottlenecks constrain platform rollouts and dampen near-term growth in the military navigation systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Assets Steer Next-Generation Precision

The space segment is forecasted to grow at a 7.44% CAGR from 2026 to 2031, building on atomic-clock and quantum-sensor deployments that enhance timing accuracy under jamming conditions. The GPS III spacecraft hosts rubidium standards that drift less than one nanosecond per day, enabling precision strikes without ground augmentation. The European Galileo Second Generation program introduces hydrogen masers with ten-fold stability improvements. While air platforms held 40.85% of the military navigation systems market share in 2025, their growth is expected to moderate as retrofit cycles mature. Land vehicles utilize MEMS IMUs, delivering 1°/h drift at commercial price levels, and sea vessels rely on fiber-optic gyroscopes paired with Doppler logs for extended submerged endurance. Disposable munitions embed USD 5,000 to 20,000 IMUs that now integrate scene-matching software, cutting satellite dependencies during terminal guidance.

Growing interest in electro-optic-aided inertial navigation within unmanned aerial vehicles further diversifies demand. The US Army’s Future Vertical Lift program specifies sensor-fusion avionics that maintain accuracy when GPS is unavailable. International Telecommunication Union regulations on frequency coexistence drive design choices for new constellations, while DO-316 standards set anti-jam thresholds for aircraft receivers. Together, these factors reinforce space systems as the innovation frontier, even as airborne and land fleets provide the bulk of installed revenue for the military navigation systems market.

By Application: Search-and-Rescue Gains New Momentum

SAR navigation use cases are advancing at a 7.29% CAGR through 2031, lifted by mandates that emergency beacons shift to second-generation transponders with return-link capability by 2025. C2 retained 29.02% of 2025 spending, reflecting its central role in force coordination. ISR platforms require continuous three-dimensional position fixes and nanosecond-level timestamps to accurately geo-reference sensor data. Targeting systems now combine inertial navigation with terrain-matching algorithms to sustain precision under deliberate jamming. Personnel recovery, convoy guidance, and refueling remain smaller yet indispensable sub-segments, each imposing distinct accuracy and availability requirements.

Urban canyon operations are driving the adoption of dual-band beacons. The US Coast Guard selected dual-frequency devices transmitting on 406 MHz and Galileo E1 to ensure signals reach satellites despite terrain masking. Lockheed Martin’s JASSM-ER cruise missile illustrates targeting advances, matching infrared scenes to stored maps during the final 100 km of flight without GNSS feeds. Command-and-control radios with software-defined multiband receivers dynamically select the least-jammed constellation, preserving real-time situational awareness.

By Component: Software Emerges as Value Center

Hardware commanded 69.15% of 2025 revenue; however, software is on track for an 7.78% CAGR as AI-driven sensor fusion raises performance ceilings. Collins Aerospace’s TruNet suite fuses GNSS, inertial, and radar-altimeter streams through Kalman filters, sustaining five-meter accuracy amid jamming. Services covering calibration and lifecycle support grow in tandem, particularly where performance-based logistics contracts transfer availability risk to vendors.

Machine learning (ML) models now predict GNSS outages using terrain, weather, and electronic-order-of-battle inputs, queuing preemptive map downloads, or inertial-only modes. BAE Systems’ NAVSOP leverages signals of opportunity from cellular towers and Wi-Fi hotspots to achieve downtown accuracy of ten meters, eliminating the need for satellites. Vector Atomic’s drift-free cold-atom gyroscope promises months-long submarine patrols without GPS. Meanwhile, Honeywell’s HGuide ships with a 40,000-hour mean time between failures guarantee, reflecting the push toward service-wrapped offerings.

Geography Analysis

North America accounted for 38.25% of 2025 revenue as the US DoD invested USD 1.8 billion annually in PNT modernization, funding GPS III launches, M-Code receiver rollouts, and quantum inertial research. Canada committed CAD 500 million (USD 370 million) to retrofit CF-18 avionics and Arctic vessels with next-generation receivers that mitigate high-latitude signal degradation. Mexico's demand is limited to patrol drones and coastal craft, which use hardened commercial receivers.

The Asia-Pacific region is growing at a 7.62% CAGR, the fastest rate worldwide. China mandates BeiDou across the People's Liberation Army's (PLA's) platforms, while India integrates NavIC into its fighters, armor, and carriers. Japan's seven-satellite QZSS constellation delivers sub-meter augmentation, and South Korea's KPS aims for regional independence by 2027. Australia's layered PNT doctrine combines satellites with eLoran and quantum sensors, echoing across the Indo-Pacific.

Europe benefits from the Galileo constellation yet faces procurement fragmentation. France relies on Safran inertials for the Rafale, while Germany relies on Honeywell for the Eurofighter, limiting cross-fleet economies of scale. The Middle East is expanding its precision-strike arsenals; Saudi Arabia's THAAD purchase included M-Code receivers, and the UAE is co-developing inertial units with Safran. Africa remains nascent, with South Africa producing basic IMUs and most sub-Saharan forces operating commercial GNSS equipment. Brazil leads South America, upgrading Super Tucano aircraft for jungle missions where vegetation attenuates signals

Regulatory Landscape

Military navigation systems operate within a tightly controlled regulatory environment shaped by assured PNT policy and dual-use export controls. In the United States, DoD guidance on navigation warfare and PNT management (DoDI 4650.06) drives requirements for resilience to jamming and spoofing, while Space Policy Directive-7 formalizes the role of secure, resilient space-based PNT and reinforces M-Code integration as modernization proceeds. These directives flow into program-level compliance checkpoints for platform upgrades and new acquisitions, where encrypted signals, controlled-reception antennas, and resilient timing become procurement baselines.

Cross-border sales and technology transfer are further constrained by ITAR and EAR classification decisions, along with allied export-control regimes such as the Wassenaar Arrangement thresholds for high-performance inertial sensors and EU restrictions around Galileo PRS-related equipment. A January 2026 Federal Register update to the U.S. Export Administration Regulations highlights how licensing pathways can shift for certain UAV categories with trusted partners, but secure PNT technologies remain sensitive and compliance-heavy. On the standards side, NISTs 2026 update to the Foundational PNT Profile (NIST IR 8323r2) adds a voluntary cybersecurity lens for PNT usage, reinforcing the need for secure integration, monitoring, and anomaly detection in military and dual-use navigation deployments.

Value Chain Analysis

The value chain begins with tightly controlled upstream components, including GNSS chipsets and secure modules, high-grade inertial sensors (FOG, DFOG, and emerging quantum/MEMS), timing devices, anti-jam antennas (including CRPA arrays), and rad-hard electronics for space and missile applications. Specialized sensor manufacturers supply subsystem providers that build embedded GPS/INS units and resilient navigation modules, which are then integrated by primes and platform OEMs into aircraft, land vehicles, naval vessels, space payloads, and munitions, followed by calibration, sustainment, and software updates across the lifecycle. Recent sourcing patterns emphasize trusted and sovereign supply chains, with AUKUS-aligned procurement and audited firmware and configuration control increasingly shaping supplier eligibility for defense programs.

Midstream activity centers on system integration and certification, where multi-constellation GNSS plus inertial fusion, M-Code capable receiver integration, and open-architecture interfaces are key differentiators. The market also shows more direct linkages between primes and specialist PNT suppliers, as reflected in defense vehicle programs that source strategic-grade INS from focused vendors (for example, Rheinmetall vehicle programs supplied by Advanced Navigation and Exail). Downstream, defense ministries and armed services remain the dominant buyers, often purchasing through platform primes under long-duration modernization and retrofit cycles, while services revenue grows through depot calibration, navigation warfare testing, and performance-based logistics. Across the chain, limited availability of rad-hard components and export-control compliance overhead continue to shape lead times, making qualified supply a competitive advantage.

Competitive Landscape

The top five vendors held a prominent market share in the global market in 2024, indicating moderate concentration within the military navigation systems market. Northrop Grumman’s LN-251 fiber-optic gyroscope dominates submarine and strategic-missile niches with 0.001°/h drift. Honeywell International Inc. leverages in-house MEMS fabrication to supply cost-effective HGuide units across more than 30 aircraft types, undercutting European rivals. Safran SA, Thales Group, and Collins Aerospace anchor European programs, while their software-defined offerings increasingly accept third-party sensor feeds.

Startups are reshaping value pools. Vector Atomic’s cold-atom sensor removes drift entirely, but it must fall below USD 50,000 to reach scale. BAE Systems’ NAVSOP demonstrates how terrestrial signals of opportunity can supplement GNSS, although global mapping remains a challenge. Xona’s forthcoming LEO constellation promises encrypted PNT with interior and dense-city reach, while Q-CTRL licenses quantum-control firmware to incumbents, accelerating the diffusion of technology.

System integrators are pivoting from proprietary hardware to open-architecture software. Collins Aerospace’s TruNet accepts heterogeneous sensor inputs on commercial processors, letting platform builders swap suppliers without redesigning avionics racks. White-space opportunities persist in anti-jam antennas and rad-hard chip supply, where specialized firms command premium margins despite lower absolute volumes.

Military Navigation Systems Industry Leaders

Northrop Grumman Corporation

Safran SA

Honeywell International Inc.

Thales Group

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Assured PNT requirements are creating whitespace for modular, multi-source navigation packages that combine GNSS (including modernized signals), inertial navigation, and non-satellite alternatives within open interfaces. The DoD focus on complementary PNT sources, reflected in GAO assessments of GPS alternatives and the DoD PNT science and technology roadmap direction, supports demand for solutions that cross-verify position and time using diverse inputs rather than relying on a single signal. At the same time, mandated open-architecture approaches such as MOSA, and current DoD interoperability work including the All-Source Positioning and Navigation (ASPN) initiative, create room for component and software providers to plug into standardized data messaging and integrate new sensors or algorithms more quickly.

Near-term opportunity is reinforced by concrete spending and modernization actions tied to contested electromagnetic environments. In July 2026, the U.S. Air Force committed USD 49.7 million toward navigation alternatives in response to rising GPS interference, signaling procurement pull for resilient navigation beyond legacy receivers. The growing emphasis on cyber-resilient PNT integration, supported by NISTs updated PNT Profile guidance, also favors vendors that pair navigation performance with monitoring, anomaly detection, and secure update pathways. Outside the United States, the spread of sovereign GNSS programs and encrypted services (such as Galileo PRS) expands integration and certification work for multi-constellation and multi-standard receivers, increasing demand for scalable, export-compliant product lines and local industrial participation models.

Recent Industry Developments

- June 2026: Exail unveiled the Advans Vega SL inertial navigation system for amphibious operations in GNSS-contested littoral environments. The product focus on continuous positioning without reliable satellite signals supports naval and marine missions where jamming and terrain masking are common, expanding the addressable market for high-end maritime INS solutions.

- November 2025: Honeywell achieved U.S. government authorization for an M-Code military navigation solution. The approval strengthens Honeywell's position in modernization programs that require secure GPS signals and accelerates upgrade pathways for legacy fleets moving to M-Code capable user equipment.

- June 2024: Exail secured a contract with Rheinmetall to supply 1,004 Advans Ursa FOG-based inertial navigation systems for German Army Caracal 4x4 vehicles. The large-volume ground vehicle award highlights the shift toward tactical platforms adopting higher-grade inertial solutions to sustain navigation performance during GNSS disruption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from military navigation systems used to determine position, navigation, and timing across defense platforms and missions, including hardware, software, and related services that enable navigation in normal and contested environments.

Scope exclusions: We exclude general consumer navigation devices and purely civilian navigation infrastructure unless the product is procured and configured for military use.

Segmentation Overview

- By Platform

- Air

- Land

- Sea

- Space

- Munitions and Missiles

- By Application

- Command and Control (C2)

- Intelligence, Surveillance and Reconnaissance (ISR)

- Targeting and Guidance

- Search and Rescue (SAR)

- Others

- By Component

- Hardware

- Software

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand boundary and build the first pass of the model before interviews began. We relied on public defense budget documents and procurement releases, NATO and allied capability roadmaps, and government trade and customs statistics for relevant electronics and defense equipment flows. Technical grounding was strengthened using sources such as the International Civil Aviation Organization where military aviation context overlaps, peer reviewed journals on inertial sensors and GNSS resilience, and patent databases to track navigation related filings and design direction.

On the supply side, we reviewed annual reports, 10-K style filings, and investor presentations, along with reputable defense and aerospace press, to understand program timing and pricing behavior. In a few cases, subscription databases were used for company financial intelligence, news and financials, defense contract and tender tracking, and patent search depth, to cross check public statements. These desk sources are illustrative and not exhaustive, and many other public references were used for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work focused on interviews and structured questionnaires with program level stakeholders, integrators, component specialists, and downstream users involved in airborne, ground, naval, space, and guided munitions navigation. We used these conversations to confirm what gets counted as a navigation system sale versus adjacent electronics, and to sanity check pricing, retrofit intensity, and service attach rates across major regions where defense procurement is active.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 15% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Market size was constructed using a top-down approach where defense procurement and modernization activity is translated into an addressable navigation spend pool, and then split by platform and application. Because military navigation demand moves with program cycles, we tracked indicators such as aircraft and helicopter upgrade cadence, armored vehicle and naval fleet modernization timelines, guided munitions procurement volume, and satellite and space payload activity where navigation subsystems are embedded. Input shaping also used the mix shift between GNSS aided solutions and inertial or integrated navigation, the penetration of anti-jam and assured PNT features, and typical service and support shares attached to deliveries.

We corroborated the results with selective bottom-up approximations, using sampled platform counts multiplied by typical fit rates and average selling prices, then checked against supplier and integrator revenue exposure statements. Where public volumes were missing for sensitive programs, we used proxy variables like budget line items and delivery schedules, and then adjusted through interview based ranges. Forecasts were built using scenario analysis tied to defense budget outlooks, procurement cycle length, and expected ASP progression, and the final curve was accepted only after the variables aligned with expert consensus on timing and mix.

Data Validation & Update Cycle

Validation was handled through multiple checks so that one data stream could not overly drive the total. We compared outputs with independent signals such as platform delivery and upgrade counts, regional defense spending direction, and program award activity, and then investigated large variances before sign off. When a datapoint looked inconsistent, we rechecked the scope boundary and recontacted relevant interviewees to confirm whether it was a one-off contract, a multi-year award, or a pricing outlier.

The report is refreshed annually, and interim updates are made when material events occur such as major procurement announcements, policy shifts impacting navigation resilience, or notable currency and inflation movements. Before final delivery, a fresh review pass is performed so the published numbers reflect the latest available public updates and primary feedback.

Mordor Intelligence's Military Navigation Systems Market Size Compared With Other Published Estimates

It is normal to see different market sizes for military navigation systems because each publisher draws the line differently on what counts as navigation, and they also pick different base years and pricing logic. Exchange rate timing, inflation treatment, and whether services and retrofit work are counted can all move the final number even when the topic sounds the same.

In this study, the spread is most influenced by how often assumptions are refreshed and how average selling prices are stepped up across multi-year defense programs, especially when contracts are awarded in one year but delivered over several. Currency conversion timing and the way platform subsystems are classified (navigation versus adjacent mission electronics) also matter, and these checks are updated on an annual cycle with exception reviews, which is where Mordor Intelligence can land away from estimates that rely on older price points or broader system definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.97 B (2026) | |

| Global Consultancy A | USD 12.83 B (2024) | Uses an earlier base year and a longer forecast window, and the platform taxonomy and component boundaries appear broader, which can pull in adjacent combat electronics alongside navigation specific subsystems. |

| Market Publisher B | USD 2.10 B (2024) | Likely applies a narrower scope limited to selected platforms or solution categories, and may exclude major guided munitions, space, or service revenues that are captured when navigation is counted across full platform subsystems. |

The comparison shows that timing and boundary choices explain most of the gap, not just different growth assumptions. By keeping the scope tied to clearly defined platforms and applications, and by updating pricing and currency inputs with repeatable checks, the final number stays traceable to the same demand signals year after year.

Key Questions Answered in the Report

How large is the military navigation systems market in 2026?

It is valued at USD 12.97 billion and is forecasted to climb to USD 18.01 billion by 2031, reflecting a 6.79% CAGR.

Which platform type is expanding fastest?

Space-based navigation payloads are growing at a 7.44% CAGR due to atomic-clock and quantum-sensor adoption in new GPS III and Galileo satellites.

Why is Asia-Pacific demand accelerating?

Regional defense budgets are funding BeiDou, NavIC, and QZSS integration to cut dependence on US GPS, propelling a 7.62% CAGR in the region.

What technology trend is reshaping future procurements?

AI-enabled sensor fusion software that combines GNSS, inertial, and signals of opportunity is moving value toward the software segment, which is growing at an 7.78% CAGR.

How are export controls affecting vendor strategies?

ITAR and Wassenaar rules force companies to maintain separate civilian and military product lines, raising compliance costs and narrowing the buyer pool.

Page last updated on: