Somatostatin Analogs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

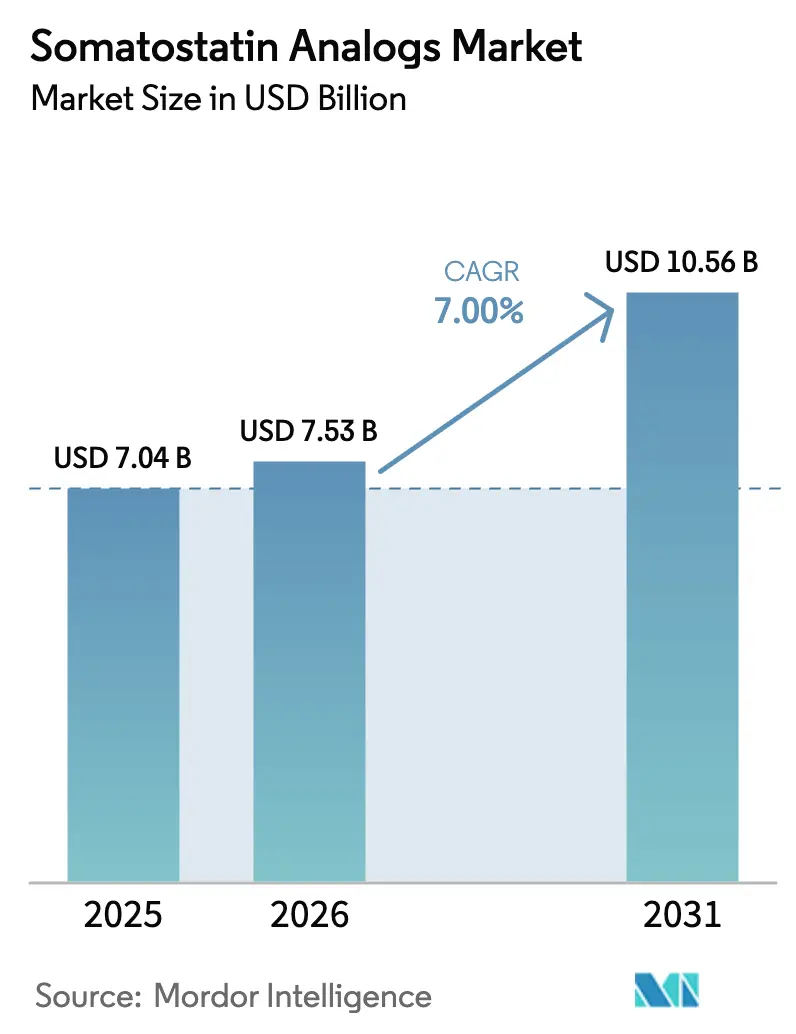

| Market Size (2026) | USD 7.53 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

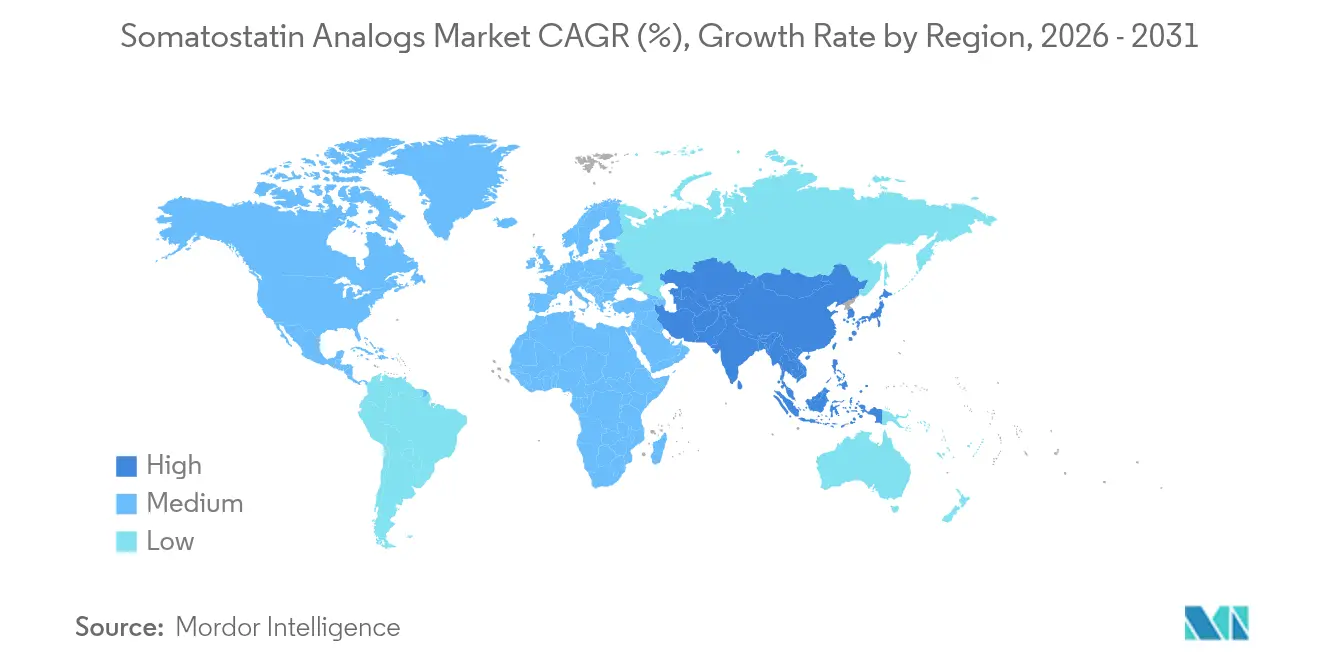

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

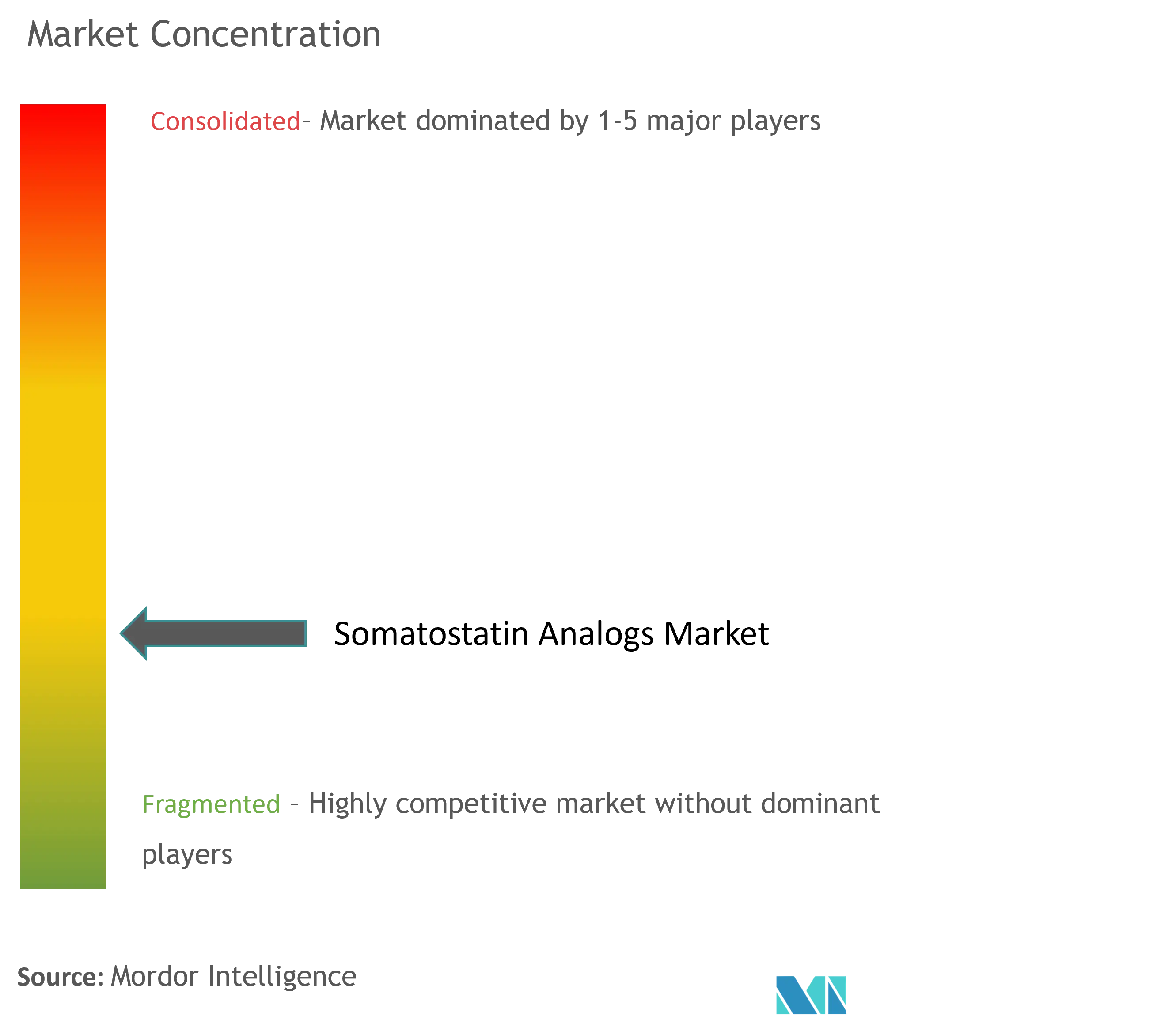

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Somatostatin Analogs Market Analysis by Mordor Intelligence

Somatostatin analogs market size in 2026 is estimated at USD 7.53 billion, growing from 2025 value of USD 7.04 billion with 2031 projections showing USD 10.56 billion, growing at 7.00% CAGR over 2026-2031. Rising neuroendocrine tumor (NET) prevalence, growing acromegaly diagnoses, and rapid innovation in drug-delivery platforms keep the growth curve steady. Approvals of oral formulations, integration of radiolabeled theranostics, and SSTR-subtype-selective R&D collectively remove long-standing treatment gaps. Mature reimbursement systems in North America contrast with widening patient-access programs across Asia Pacific, creating region-specific momentum in the somatostatin analogs market. Depot technologies, digital pharmacy channels, and capacity expansions in peptide active pharmaceutical ingredient (API) manufacturing reshape competitive dynamics while insulating growth against generic price pressure. Overall, the somatostatin analogs market maintains a mid-single-digit trajectory that aligns with the broader shift toward precision endocrinology.

Key Report Takeaways

- By drug type, octreotide led with 46.52% of the somatostatin analogs market share in 2025, while pasireotide is forecast to expand at a 9.80% CAGR to 2031.

- By formulation, long-acting depot products captured 54.28% revenue share in 2025; the “Others” category (oral, transdermal, implantable) advances at a 8.95% CAGR through 2031.

- By route of administration, intramuscular injections held 58.40% of the somatostatin analogs market size in 2025; oral routes project a 9.97% CAGR between 2026-2031.

- By application, Gastro-entero-pancreatic NETs accounted for a 58.05% share of the somatostatin analogs market size in 2025, while Cushing’s disease applications grow at a 10.24% CAGR.

- By distribution channel, hospital pharmacies dominated with 60.52% share in 2025; online pharmacies record the strongest CAGR at 11.11% to 2031.

- By geography, North America commanded 38.28% of the somatostatin analogs market in 2025, whereas Asia Pacific registers the fastest regional CAGR at 9.59% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Somatostatin Analogs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of acromegaly & NETs | +1.8% | North America, Europe, APAC | Long term (≥ 4 years) |

| Adoption of long-acting depot formulations | +1.2% | North America, EU, APAC | Medium term (2-4 years) |

| Expanding label indications (Cushing’s) | +0.9% | US, EU, Global | Medium term (2-4 years) |

| Radiolabeled SSA theranostics demand surge | +0.7% | North America, EU, APAC | Long term (≥ 4 years) |

| Oral octreotide approval broadening access | +0.6% | US, EU, Global | Short term (≤ 2 years) |

| SSTR-subtype-selective pipeline momentum | +0.5% | US, EU, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Acromegaly & NETs

NETs commanded 58.79% application share in 2024, and improved diagnostics continue to uncover previously hidden cases, especially across modernizing Asia Pacific health systems.[1]Hongzhang Yang, “Somatostatin Receptor 2 (SSTR2) Expression Is Associated With Better Clinical Outcome and Prognosis in Rectal Neuroendocrine Tumors,” Scientific Reports, nature.com FDA clearance of Lutathera for pediatric patients in April 2024 extends treatment eligibility and enlarges the patient pool. Robust SSTR2 expression—observed in 66.9% of rectal NET biopsies—correlates with 98.5% five-year survival, underpinning strong clinical demand. Together, widened screening, earlier detection, and pediatric indications create a growing baseline for the somatostatin analogs market. Steady diagnosis rates convert into longer treatment durations, sustaining revenue visibility beyond the forecast window.

Adoption of Long-Acting Depot Formulations

Long-acting depots already capture 55.12% share, and positive CHMP opinion for CAM2029 demonstrates regulator confidence in next-generation gels and microspheres. Subcutaneous self-administration reduces office visits and drives adherence, a benefit that resonates in regions with stretched clinical capacity. Depot manufacturing relies on specialized microsphere know-how, giving innovators defensible pricing despite upcoming generic octreotide LAR launches. In emerging markets, fewer clinic trips translate into measurable cost savings, making depot uptake even faster than in developed countries. As payers narrow formularies, proven compliance gains strengthen the economic case, keeping depot solutions central to the somatostatin analogs market.

Expanding Label Indications (Cushing’s)

Cushing’s disease presents the fastest indication CAGR at 10.67%, fueled by pasireotide’s demonstrated efficacy and the impending arrival of oral paltusotine. FDA acceptance of paltusotine’s NDA in December 2024 positions the SSTR2-selective tablet as a once-daily alternative that matches biochemical control while bypassing depot injections. Although pasireotide’s hyperglycemia risk remains a constraint, endocrinologists often prioritize disease suppression, especially in severe ACTH tumors. Revenue diversification into Cushing’s reduces over-reliance on acromegaly and NET lines, opening fresh pricing headroom in small but high-value patient groups. Collectively, indication expansion underpins a durable growth pillar for the somatostatin analogs market.

Radiolabeled SSA Theranostics Demand Surge

Theranostics marry imaging and therapy, allowing clinicians to select only SSTR-positive tumors for radioligand treatment. NETTER-2 data revealed a 72% mortality-risk reduction over standard care, reinforcing payer willingness to reimburse high-cost radiopharmaceuticals. CMS reclassification of radiopharmaceuticals as drugs in 2025 improves reimbursement, accelerating U.S. uptake. Production complexity requires hot-cell facilities and stringent logistics, erecting natural barriers to fast-following competitors. As pediatric use rises, total addressable volumes for radiolabeled products expand, enhancing the premium segment within the somatostatin analogs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & reimbursement hurdles | -1.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Adverse-event-driven discontinuation (hyperglycemia) | -0.8% | Global, pasireotide focused | Short term (≤ 2 years) |

| Competition from GH-antagonists & PRRT combos | -0.6% | North America, EU | Medium term (2-4 years) |

| Limited global peptide-API manufacturing capacity | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Reimbursement Hurdles

Radiopharmaceutical courses often exceed USD 300,000, constraining adoption in cost-sensitive markets even when efficacy is superior. Economic analyses show octreotide LAR remains cheaper than lanreotide over five years by USD 37,323, influencing payer preference. Generic octreotide from Teva entered the U.S. in October 2024, applying price pressure yet lowering gross margins for original brands. Emerging-market insurers often cap specialty-drug spending, pushing patients toward limited charity programs. Collectively, high price points temper volume growth in the somatostatin analogs market.

Adverse-Event-Driven Discontinuation (Hyperglycemia)

Pasireotide raises HbA1c and may prompt therapy switches unless proactive glucose management is introduced.[2]Kaibin Niu, “Adverse Events in Different Administration Routes of Semaglutide: A Pharmacovigilance Study Based on the FDA Adverse Event Reporting System,” Frontiers in Pharmacology, frontiersin.org GLP-1 analog co-administration mitigates risk but raises regimen complexity and cost. Hyperglycemia is especially problematic in Cushing’s disease, where baseline glucose dysregulation already exists. Elevated discontinuation rates shorten treatment duration and compress lifetime revenue. Accordingly, tolerability remains a gating factor in the somatostatin analogs market until subtype-selective therapies mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Octreotide Dominance Faces Precision Challenge

Octreotide retained 46.52% share of the somatostatin analogs market in 2025 owing to widespread physician familiarity and multi-indication approvals. Pasireotide, however, rises at a 9.80% CAGR by 2031 on the strength of Cushing’s disease efficacy and receptivity among endocrinologists seeking targeted approaches. Lanreotide holds steady in gastroenteropancreatic NET use, while niche analogs such as vapreotide persist in specialized settings. The competitive picture evolves as Crinetics’ paltusotine moves closer to approval, promising the first oral option that could erode depot loyalty. Pipeline agents that zero in on SSTR subtypes forecast deeper segmentation of the somatostatin analogs industry, potentially displacing broad-spectrum molecules over the long term.

Second-line players differentiate through delivery innovation rather than pharmacodynamics. Oral octreotide, subtype-selective small molecules, and depot gels show clear positioning against older depot injections. New entrants exploit gaps such as pediatric dosing or rare tumor subtypes, turning the once homogenous somatostatin analogs market into a multisegmented competitive arena. While octreotide’s entrenched guidelines secure near-term revenue, share erosion appears inevitable as payers embrace clinically equivalent yet more convenient formulations.

By Formulation: Depot Technology Drives Innovation

Long-acting depots make up 54.28% of revenue, reflecting decades of incremental delivery advances and patient compliance benefits. Microsphere manufacturing and injectable gel technologies reinforce pricing power by raising entry barriers for generic makers. Meanwhile, “Others” formulations—oral, transdermal, implantable—advance at 8.95% CAGR, buoyed by self-administration convenience. Immediate-release injections shrink in relative terms as chronic disease management moves outside clinic walls. CAM2029’s self-injectable design further compresses follow-up schedules, promising both payer savings and patient preference gains. Consequently, formulation innovation remains central to sustaining value in the somatostatin analogs market.

As more oral candidates clear development, daily capsules could disrupt depot-centric revenue streams. Yet depot supply chains remain indispensable for patients resistant to oral absorption variability. Companies that balance both modalities can hedge cannibalization risks, fortifying their positions across the broader somatostatin analogs industry landscape.

By Route of Administration: Oral Revolution Reshapes Access

Intramuscular injections still hold 58.40% of somatostatin analogs market size because historical guidelines mandate depot use for consistent pharmacokinetics.Oral administration accelerates at a 9.97% CAGR as permeability-enhancer technologies translate more peptides into capsules. Subcutaneous routes fill a niche for self-managed weekly gels, whereas intranasal options remain proof-of-concept. Successful rollout of Mycapssa illustrates how oral dosing reduces infusion-center dependence, cuts travel costs, and enhances quality of life. Tele-endocrinology integration further supports oral uptake in rural settings, boosting compliance. Over time, diffusion of oral routes into emerging markets could reorganize regional revenue mix within the somatostatin analogs market.

By Application: NETs Leadership Faces Cushing’s Disruption

Gastro-entero-pancreatic NETs generated 58.05% of sales in 2025, thanks to high SSTR expression and proven survival benefit in trials like NETTER-2. Cushing’s disease, though smaller in absolute terms, advances at the highest CAGR of 10.24%, reshaping strategic focus. Acromegaly growth remains steady due to early diagnosis and endocrine society screening guidelines. Carcinoid syndrome symptom control stays niche but clinically critical.

The arrival of pediatric NET indications widens the NET base, while pasireotide and paltusotine add momentum to Cushing’s. This evolving mix diversifies revenue streams in the somatostatin analogs market and reduces reliance on historically dominant indications.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies still move 60.52% of product volume because depot injections demand cold-chain handling and trained staff ashp.org. Online pharmacies, however, log an 11.11% CAGR as oral and self-injectable depots migrate to direct-to-patient platforms. Specialty pharmacies act as adherence hubs, blending virtual counseling with dispensing.

Drug shortages such as the 2025 lanreotide acetate gap highlight vulnerabilities in traditional channels, prompting manufacturers to diversify distribution. Digital platforms integrate refill reminders, blood-glucose tracking, and telehealth consultations, strengthening retention. As payer contracts embrace mail-order fulfillment, online channels should influence the future shape of the somatostatin analogs market.

Geography Analysis

North America controlled 38.28% of the somatostatin analogs market in 2025, anchored by comprehensive insurance coverage, early oral octreotide uptake, and widespread theranostics use. FDA approvals flow swiftly into clinical practice, aided by electronic prior-authorization portals that shorten time-to-therapy. Robust supply chains, now bolstered by CordenPharma’s USD 975 million peptide-platform expansion, minimize back-order risk and maintain high service levels.

Asia Pacific posts the fastest 9.59% CAGR through 2031 as hospitals adopt advanced imaging and endocrine testing. China accelerates NET diagnoses through government cancer-screen programs, while Japan’s aging population heightens acromegaly prevalence. India leverages domestic manufacturing to deliver cost-effective generics, improving affordability and widening access. Regional health ministries increasingly reimburse radioligand therapies, spurring rapid volume growth across the somatostatin analogs market.

Europe maintains balanced expansion, supported by EMA centralized approvals and long-standing national reimbursement frameworks. Germany, France, and the United Kingdom lead uptake of depot innovations, while Southern Europe benefits from EU cohesion funds aimed at cancer-care infrastructure. Depot plants in Switzerland and France ensure supply resilience. Budget constraints encourage pharmaco-economic reviews, yet the demonstrated survival benefits of radiolabeled analogs secure funding. Collectively, diversified geographic drivers protect the global somatostatin analogs market from over-exposure to single-region risk.

Competitive Landscape

The somatostatin analogs market displays moderate consolidation, with top players holding a combined 68% share in 2024. Novartis leverages its Sandostatin and Lutathera franchises, pairing peptide injectables with radioligands to create lifecycle synergies. Ipsen’s Somatuline depot derives strength from chronic NET use as well as an expanding label in pediatric acromegaly. Teva’s generic octreotide LAR entry in late 2024 sets a precedent for biosimilar waves expected later in the decade, putting downward pressure on baseline prices but expanding total treated population.

New entrants focus on differentiated modalities. Crinetics designs oral small-molecule agonists like paltusotine, while Camurus engineers self-injectable gels with extended release profiles. Both target therapy-convenience gaps that incumbents struggle to match quickly. Radiopharmaceutical upstarts invest in isotope-production partnerships to secure supply ahead of anticipated demand spikes.

Strategically, manufacturers diversify across indications to offset price erosion. SSTR-selective research aims to reduce adverse-event discontinuation and extend dosing intervals, potentially expanding net revenue. Co-promotion deals with digital-health firms add adherence analytics, cementing long-term market positioning. As product differentiation intensifies, competitive advantage shifts toward companies mastering delivery technology, supply-chain agility, and real-world outcomes documentation within the somatostatin analogs market.

Somatostatin Analogs Industry Leaders

Novartis AG

Sun Pharmaceutical Industries Ltd

Ipsen Pharma

Teva Pharmaceuticals Ltd.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Camurus received positive CHMP opinion for Oczyesa (CAM2029) EU marketing authorization, planning launch in H2 2025.

- December 2024: Crinetics Pharmaceuticals announced FDA acceptance of the paltusotine NDA for adult acromegaly maintenance therapy.

- October 2024: Teva launched the first U.S. generic Sandostatin LAR, marking a milestone in somatostatin analog genericization.

Global Somatostatin Analogs Market Report Scope

As per the scope of the report, somatostatin analogs are synthetic compounds that mimic the actions of the naturally occurring hormone somatostatin. These analogs bind to somatostatin receptors in various tissues and organs, exerting regulatory effects on hormone secretion, cell growth, and neurotransmission.

The somatostatin analogs market is segmented by type (octreotide, lanreotide, pasireotide, and other types), application (acromegaly, neuroendocrine tumors (NETs), and other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

| Octreotide |

| Lanreotide |

| Pasireotide |

| Other Analogs (e.g., Vapreotide, Somatoprim) |

| Long-Acting Depot (LAR, Autogel) |

| Immediate-Release Injection |

| Others (Oral, Transdermal, Implantable) |

| Sub-cutaneous |

| Intra-muscular |

| Oral |

| Intranasal & Others |

| Acromegaly |

| Gastro-entero-pancreatic NETs |

| Cushing’s Disease |

| Carcinoid Syndrome Symptom Control |

| Other Endocrine & Oncologic Uses |

| Hospital Pharmacies |

| Retail & Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Octreotide | |

| Lanreotide | ||

| Pasireotide | ||

| Other Analogs (e.g., Vapreotide, Somatoprim) | ||

| By Formulation | Long-Acting Depot (LAR, Autogel) | |

| Immediate-Release Injection | ||

| Others (Oral, Transdermal, Implantable) | ||

| By Route of Administration | Sub-cutaneous | |

| Intra-muscular | ||

| Oral | ||

| Intranasal & Others | ||

| By Application | Acromegaly | |

| Gastro-entero-pancreatic NETs | ||

| Cushing’s Disease | ||

| Carcinoid Syndrome Symptom Control | ||

| Other Endocrine & Oncologic Uses | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is fueling current growth in the somatostatin analogs market?

Demand is rising because neuroendocrine tumor and acromegaly diagnoses keep increasing, while oral formulations, radiolabeled theranostics, and SSTR-subtype–selective assets remove long-standing treatment gaps.

How large is the somatostatin analogs market in 2026?

The market is valued at USD 7.53 billion in 2026 and is forecast to reach USD 10.56 billion by 2031, reflecting a 7.00% CAGR over 2026-2031.

Which geographic region is expanding the fastest?

Asia Pacific is the quickest-growing region, advancing at a 9.59% CAGR through 2031 as diagnostic infrastructure and reimbursement access improve.

Why are long-acting depot formulations still dominant?

Depots deliver proven adherence benefits and reduced clinic visits, holding 54.28% revenue share in 2025 even as oral options gain momentum.

What therapeutic area offers the strongest upside beyond NETs?

Cushing’s disease shows the highest forecast CAGR (10.24%) thanks to pasireotide uptake and the pending launch of oral paltusotine.

Page last updated on: