Solar Cell Paste Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

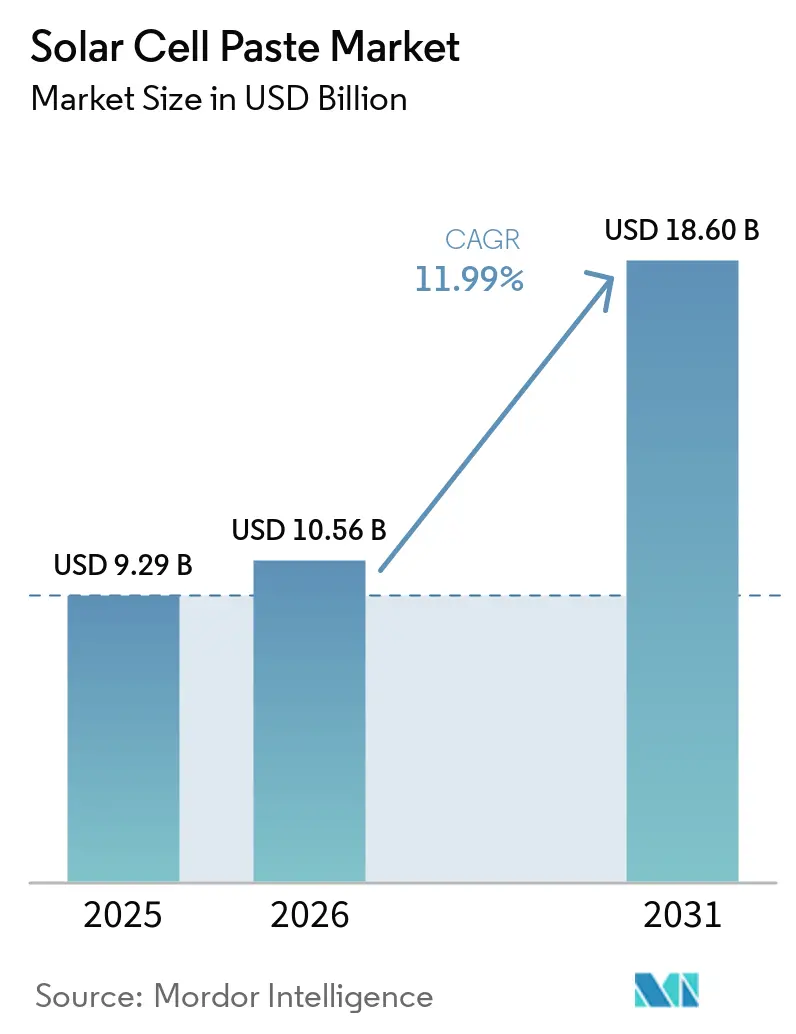

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 18.60 Billion |

| Growth Rate (2026 - 2031) | 11.99% CAGR |

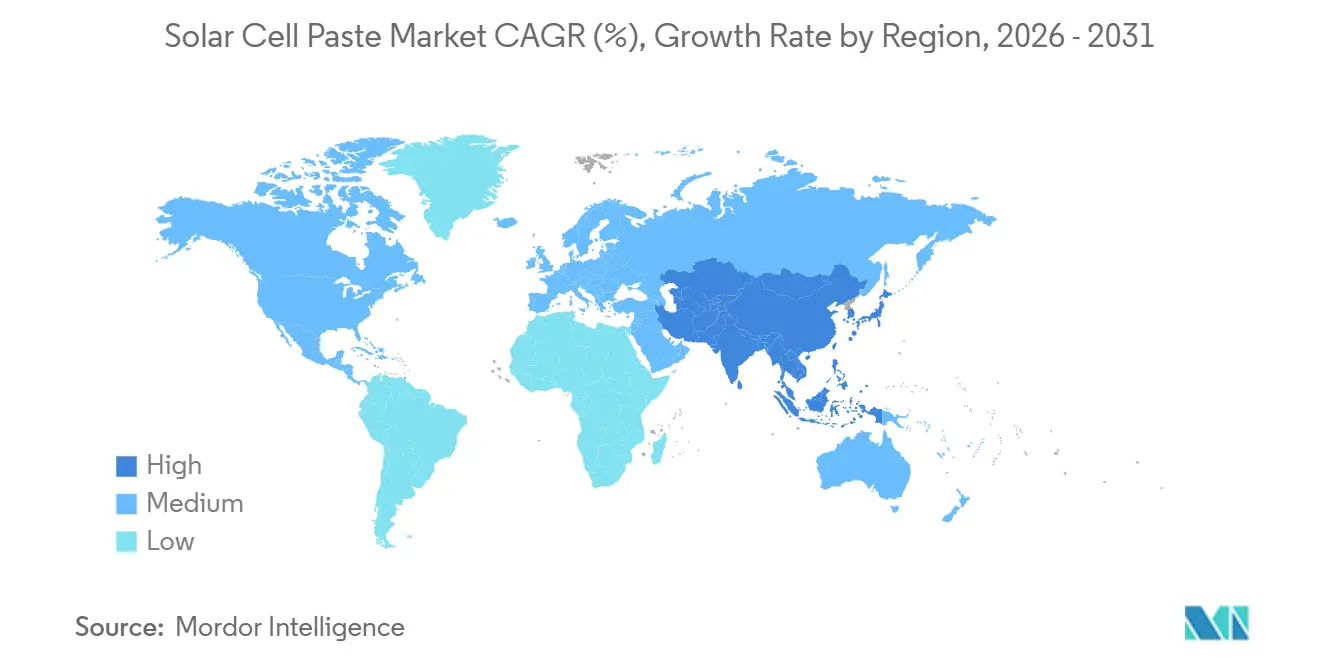

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

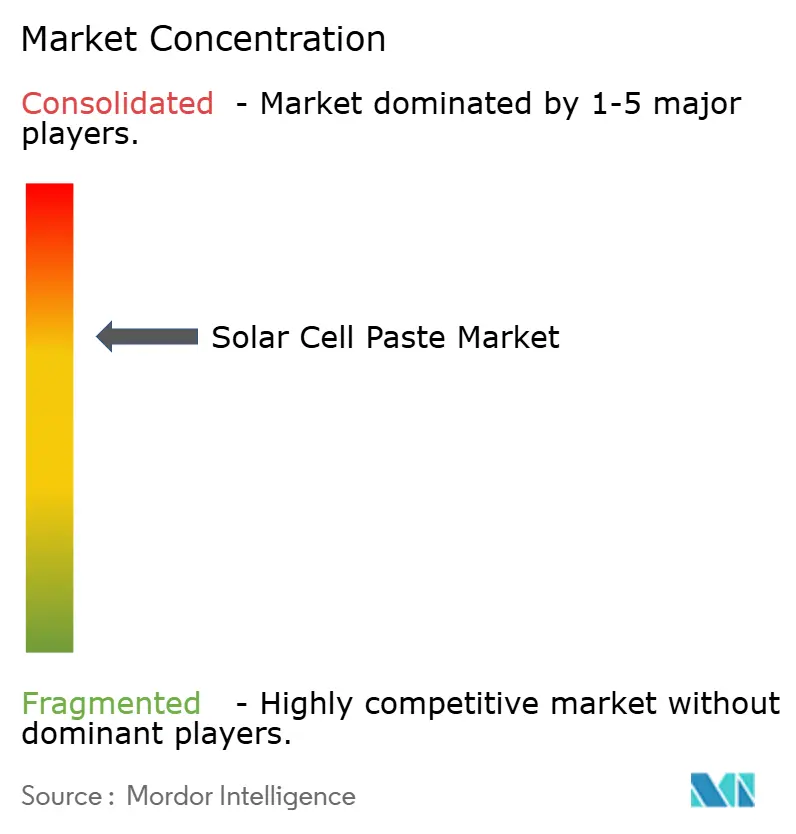

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Cell Paste Market Analysis by Mordor Intelligence

The Solar Cell Paste Market size is projected to be USD 9.29 billion in 2025, USD 10.56 billion in 2026, and reach USD 18.60 billion by 2031, growing at a CAGR of 11.99% from 2026 to 2031. Cell manufacturers are migrating from volume-driven expansion to technology-led differentiation, accelerating demand for pastes that enable narrower line widths, lower contact resistance, and reduced silver loading, especially for TOPCon, HJT, and emerging perovskite-tandem architectures. Volatility in silver pricing that peaked at USD 3.70 per gram in January 2026 has sharpened the industry’s cost-down focus, driving R&D into silver-coated-copper and lead-free multi-metal formulations.[1]Ben Blanchard, “China Adds 280 GW Cell Capacity in Two Years,” reuters.com Simultaneously, localization programs such as the IRA in the United States and REPowerEU in Europe are redrawing supply chains, prompting Heraeus, DuPont and other leaders to commission regional blending lines to capture tariff-protected margins. The solar cell paste market is also benefiting from policy-backed expansion of distributed generation, with rooftop economics favoring higher-efficiency cells that require premium metallization materials. Together, these forces underpin a structural shift from commodity paste to application-specific recipes, reinforcing pricing power for suppliers able to meet tightening performance specs.

Key Report Takeaways

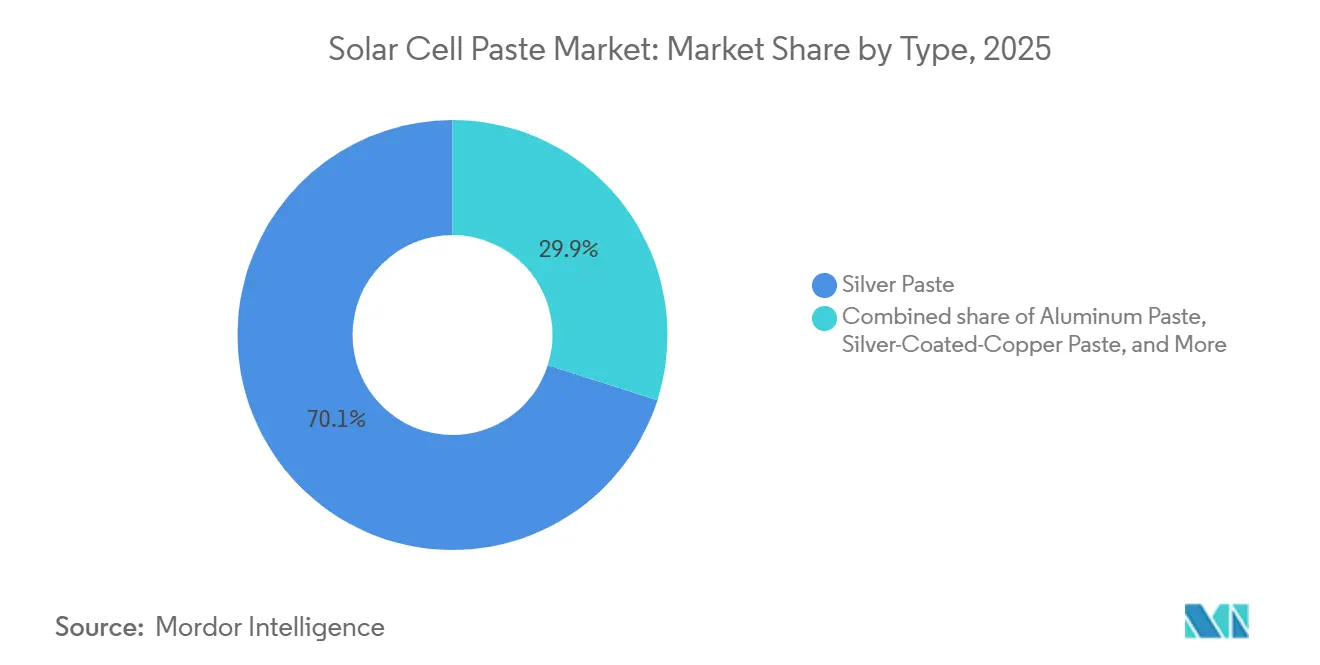

- By type, Silver Paste led with 70.1% revenue share of the solar cell paste market in 2025, while Lead-Free Multi-Metal Paste is projected to expand at a 14.1% CAGR to 2031.

- By application, monocrystalline cells held 58.5% of the solar cell paste market share in 2025; perovskite-tandem formats are advancing at a 48.0% CAGR through 2031.

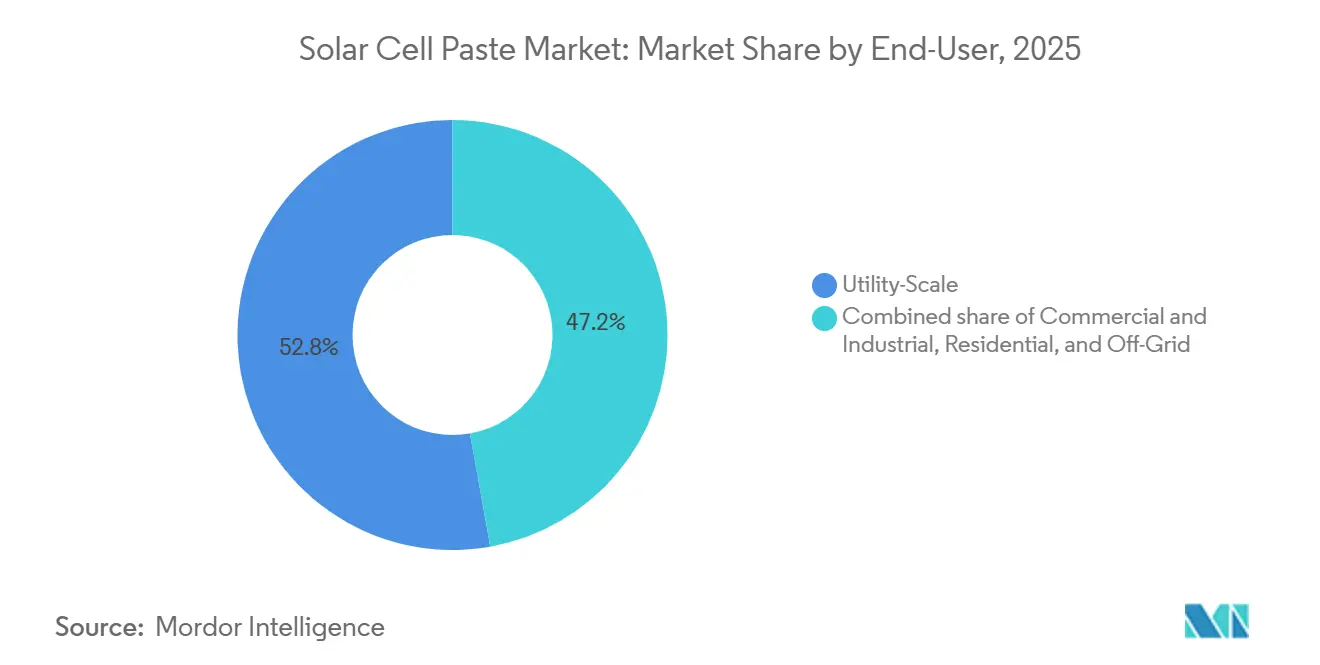

- By end-user, utility-scale installations accounted for 52.8% of the solar cell paste market size in 2025, yet the residential segment is forecast to grow at a 16.3% CAGR by 2031.

- By geography, Asia-Pacific commanded 62.7% of the solar cell paste market size in 2025 and is growing at a 13.4% CAGR, supported by China’s and India’s manufacturing build-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solar Cell Paste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Relentless PV capacity additions in China, India & US boosting paste demand | +3.2% | APAC, North America | Medium term (2-4 years) |

| Rapid shift to PERC, TOPCon & HJT cells requiring higher-performance pastes | +2.8% | APAC hubs, spillover to Europe & North America | Short term (≤ 2 years) |

| IRA, REPowerEU & other localization schemes spurring new paste lines outside Asia | +2.1% | North America, Europe | Medium term (2-4 years) |

| Cost-down race driving silver-coated-copper & low-temperature pastes uptake | +1.9% | Global early adoption in China, South Korea, Japan | Short term (≤ 2 years) |

| Surge in perovskite-tandem R&D demanding screen-printable conductive inks | +1.5% | Global R&D hubs, early pilots in Europe & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Relentless PV Capacity Additions in China, India & US Boosting Paste Demand

China alone added 280 GW of new cell capacity during 2024-2025, pushing cumulative capability beyond 800 GW and lifting past consumption as lines run at higher utilization to amortize fixed costs.[2]Ben Blanchard, “China Adds 280 GW Cell Capacity in Two Years,” reuters.com India’s USD 2.4 billion Production-Linked Incentive mandates domestic paste sourcing, catalyzing joint ventures between local cell makers and Korean suppliers.[3] PV-Magazine, “DuPont Breaks Ground on NC Paste Plant,” pv-magazine.com In the United States, the IRA’s 45X credit is underwriting a projected climb to 50 GW of annual cell output by 2027, trimming lead times for paste deliveries to 30 days as suppliers commission regional blending plants. Regionalization reduces working capital tied up in inventory by up to 20%, freeing cash for further process upgrades. The driver’s impact stays pronounced through 2028, underpinning baseline demand even as per-watt paste loadings decline.

Rapid Shift to PERC, TOPCon & HJT Cells Requiring Higher-Performance Pastes

TOPCon overtook PERC in quarterly capacity additions by late 2025, delivering module efficiencies above 24.5% that justify dual-layer metallization and selective-emitter architectures, which in turn require front-side pastes that achieve contact resistivity under 1.5 mΩ·cm² and line widths under 25 µm.[4]PV-Tech Editorial, “Aiko Solar Copper Plating Rollout,” pv-tech.org HJT cells demand low-temperature silver formulations that fire below 200 °C to preserve amorphous-silicon layers; REC Solar and Huasun expect 10 GW of combined HJT capacity online by end-2026. These tighter specs limit qualified suppliers to fewer than 10 globally, consolidating purchasing around Heraeus, DuPont, and Giga Solar. As manufacturers pivot, paste vendors investing in rheology control and nano-silver dispersion secure premium pricing and longer-term contracts, cushioning margin pressure from silver volatility.

IRA, REPowerEU & Localization Schemes Spurring New Paste Lines Outside Asia

The IRA’s domestic-content bonus worth USD 0.01 per W for U.S.-made cells and pastes has attracted USD 1.2 billion of announced metallization investments, including DuPont’s 500-ton-per-year line in North Carolina slated for Q3 2026, creating new demand nodes for the solar cell paste market. Europe’s REPowerEU targets 30 GW of annual solar installations and requires 20% local content by 2027, spurring paste blending and QC facilities in Germany, Italy, and Spain. Shorter supply chains cut freight costs on aluminum pastes by up to 12% of the landed price, improving gross margins by roughly 250 basis points. Localization also hedges geopolitical risk, securing supply for Western module assemblers as trade tensions persist.

Cost-Down Race Driving Silver-Coated-Copper & Low-Temp Pastes Uptake

Silver-coated-copper pastes that replace 60-80% of silver with copper cores showed 98.7% of pure silver conductivity in DK Electronic Materials’ 2025 pilot, reducing metallization costs by USD 0.012 per W, translating to USD 12 million annual savings for each GW of cell output. Yet accelerated aging tests still indicate 2-3 ppt fill-factor loss after 1,000 hours at 85 °C/85% RH, restraining mass adoption. For HJT, low-temperature nano-silver pastes firing at 180-200 °C lift module efficiencies above 25% and command 20-25% price premiums. Combined, these technologies can trim paste consumption per watt by 10-15%, but overall volumes still grow because cell output expands faster than thrifting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silver price volatility enlarging cost risk for cell makers | -1.8% | Global, acute in APAC | Short term (≤ 2 years) |

| Accelerated silver-thrifting & copper plating threaten paste volumes | -1.3% | China, South Korea, Japan | Medium term (2-4 years) |

| Tighter lead-based frit regulations raising reformulation costs | -0.9% | Europe, China, North America | Medium term (2-4 years) |

| High supplier concentration limits buyers’ bargaining power | -0.7% | Global, strongest in TOPCon & HJT | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Silver Price Volatility Enlarging Cost Risk for Cell Makers

Silver rallied 76% from January 2025 to January 2026, then retraced to USD 2.65-2.90 per g by March 2026, forcing Tongwei, LONGi, and JA Solar to book USD 1.1 billion in combined Q1 2026 losses tied to unhedged silver exposure. Paste suppliers now offer fixed-price contracts indexed to three-month forwards, but these shift commodity risk upstream, compressing supplier gross margins by up to 200 bps. To cope, average silver consumption dropped from 110 mg to 92 mg per wafer between 2023 and 2025 through finer screen meshes. Volatility, therefore, reduces revenue predictability and accelerates the uptake of thrifting technologies.

Accelerated Silver-Thrifting & Copper Plating Threaten Paste Volumes

Aiko Solar will begin copper electroplating on a 5 GW line in Zhejiang in Q2 2026, projecting USD 75 million annual silver savings and eliminating 90% of rear-side paste needs. But copper’s higher diffusivity into silicon poses long-term reliability concerns, deterring use in residential modules with 25-year warranties. Multi-busbar screens cut paste per watt by 8-12% without compromising efficiency, and combined plating plus thrifting could trim global paste volume per GW by 25% by 2028. Suppliers must therefore pivot toward higher-margin specialty formulations or adjacent materials such as encapsulants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silver Leadership Faces Multi-Metal Disruption

Silver Paste captured 70.1% of the solar cell paste market share in 2025, underpinned by its high conductivity and broad qualification across PERC, TOPCon, and HJT. The segment’s dominance shields near-term revenues, yet silver volatility and regulatory headwinds limit upside. Lead-Free Multi-Metal Paste is forecast to post a 14.1% CAGR, benefiting from EU REACH and China’s GB/T 38597 mandates; Sn-Ag-Cu blends add roughly 10% to production cost but remove compliance risk. Aluminum Paste remains relevant for Al-BSF cells in utility-scale projects, though share erodes as TOPCon spreads. Copper and silver-coated copper pastes present high upside if adhesion and migration challenges are solved.

Suppliers are aligning portfolios accordingly. Heraeus and DuPont funnel R&D into low-temperature nano-silver dispersions for HJT, leveraging 20-25% price premiums. Chinese contenders like Giga Solar double down on aluminum and conventional silver pastes aimed at price-sensitive gigawatt farms. Early certification of lead-free blends offers first-mover advantage in Europe’s tightening policy environment, while silver-coated-copper pilots act as an option on future cost shocks. Competitive positioning, therefore, hinges on parallel bets across premium-efficiency and cost-optimized formulations, with IP around sintering additives and wetting agents forming key moats.

By Application: Monocrystalline Dominance, Tandem Momentum

Monocrystalline formats absorbed 58.5% of the solar cell paste market size in 2025, mirroring their 85% share of global cell output and reliance on high-performance metallization to unlock 24-25% module efficiencies. Paste loadings for mono TOPCon average 90-95 mg Ag per wafer, underpinning steady revenue despite thrifting. Perovskite-silicon tandem cells, although less than 1% of shipments today, are expanding at 48% CAGR toward 2031 as pilot lines in Germany and the United States commercialize sub-150 °C printable inks. These low-temperature pastes will initially command 30-40% pricing premiums and create a fresh TAM exceeding USD 600 million by 2030. Overall, application diversity is rising, pressuring suppliers to support half a dozen discrete rheology recipes in parallel.

By End-User: Utility-Scale Maturity, Residential Upshift

Utility-scale farms consumed 52.8% of the solar cell paste market size in 2025, reflecting the gigawatt pipelines in China, India, and the Middle East that prize cost per watt over maximum efficiency. However, residential installations are forecast to grow at a 16.3% CAGR through 2031 on the back of rooftop subsidies such as the extended U.S. ITC, Germany’s KfW loans, and Australia’s SRES. Residential rooftops favor high-efficiency TOPCon and HJT modules that rely on premium pastes, nudging suppliers to tailor darker, low-reflectivity formulations to improve aesthetics. Commercial & industrial rooftops hold a significant share and grow broadly in line with the overall market, driven by corporate PPAs. Off-grid and microgrid systems demand comes mainly from Africa and Southeast Asia, and remains price sensitive, anchoring demand for conventional silver and aluminum pastes. The mix shift toward rooftops, therefore, raises average selling prices even if utility volumes remain the largest bucket.

Geography Analysis

Asia-Pacific controlled 62.7% of the solar cell paste market share in 2025 and is expanding at a 13.4% CAGR to 2031, fueled by China’s plan for 500 GW of additional PV by 2030 and India’s National Solar Mission target of 280 GW. Jiangsu, Zhejiang, and Anhui house over 60% of global cell capacity, concentrating paste demand and enabling economies of scale. India’s domestic-content rules have already lured Daejoo Electronic Materials and Giga Solar into Gujarat and Tamil Nadu joint ventures, trimming logistics lead times from 90 days to 30 days. South Korea and Japan, though smaller in volume, drive innovation in low-temperature HJT pastes, supported by extensive semiconductor materials expertise.

North America’s share is set to rise rapidly through 2028 as the IRA’s 45X credit propels U.S. cell capacity from 8 GW in 2023 to a forecast 50 GW by 2027, bringing with it localized paste demand. DuPont’s North Carolina line and Heraeus’s Ohio tech center illustrate first-mover capture of this resurgent market. Europe, targeting 30 GW per annum under REPowerEU, faces a manufacturing gap; local paste consumption therefore hinges on the success of intra-EU cell projects led by Meyer Burger and Enel Green Power. Still, the regulatory push for lead-free formulations positions European plants at the forefront of Sn-Ag-Cu adoption.

The Middle East and Africa are emerging growth zones. Saudi Arabia’s Vision 2030 aims for 20 GW of solar, prompting Heraeus to open a Riyadh service hub in 2026. The UAE’s 5 GW Al Dhafra farm and South Africa’s procurement rounds will lift regional paste imports, though domestic manufacturing remains nascent. South America, led by Brazil and Chile, imports most cells but could catalyze future blending facilities if local content rules tighten. Collectively, these geographies diversify revenue streams, but Asia-Pacific will remain the anchor of the solar cell paste market through at least 2031.

Competitive Landscape

Competition is moderately concentrated. Silver volatility and localization incentives are encouraging regional blending investments, yet high qualification barriers mean most newcomers enter through joint ventures or niche perovskite inks. Heraeus and DuPont channel R&D toward low-temperature silver pastes and hybrid inks for tandem cells, targeting rooftop and commercial customers willing to pay premiums for efficiency and aesthetics. Chinese participants, notably Giga Solar, Rutech, and Daejoo Electronic Materials, scale conventional silver and aluminum pastes for cost-sensitive utility projects, leveraging domestic raw-material access to defend margins.

Disruptors are surfacing. DK Electronic Materials demonstrated silver-coated-copper paste that retained 98.7% conductivity, while Kumelle, backed by Fraunhofer, focuses exclusively on perovskite paste lines. Technology differentiation is shifting toward AI-assisted rheology optimization, with inline systems that detect viscosity drift within 0.5% tolerance, lowering scrap rates. Consolidation pressures are evident in Haitian New Material’s 2025 acquisition of Heraeus Photovoltaics, signaling that paste portfolios carry strategic weight as metallization accounts for up to 12% of cell manufacturing cost. Competitive intensity is thus a function of both materials science and geographic reach.

Solar Cell Paste Industry Leaders

Heraeus Photovoltaics

DuPont Microcircuit Materials

Giga Solar Materials

Rutech (Guangzhou Ruxing)

Daejoo Electronic Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: DK Electronic Materials unveiled a silver-coated copper paste with 98.7% of silver conductivity and USD 0.012 W cost savings, pending reliability validation.

- July 2025: Aiko Solar confirmed copper plating rollout on a 5 GW line, aiming for 90% reduction in rear-side paste use by mid-2026.

- April 2025: Fraunhofer ISE cut silver use to 1.4 mg/Wp via copper rear contacts on HJT cells, demonstrating a 60% reduction from industry norms.

- January 2025: Haitian New Material acquired Heraeus Photovoltaics, consolidating advanced paste IP under a vertically integrated materials platform.

Global Solar Cell Paste Market Report Scope

In photovoltaics, solar cell paste, also referred to as metallization paste or conductive paste, is a high-viscosity material used to print electrical contacts onto solar wafers. It is a crucial auxiliary material, contributing to approximately 50–60% of the non-silicon costs in cell production.

The Solar Cell Paste Market is segmented into type, application, end-user, and geography. By type, the market is segmented into silver paste, aluminum paste, copper paste, silver-coated-copper paste, and lead-free multi-metal paste. By application, the market is segmented into monocrystalline, polycrystalline, thin-film, HJT, and perovskite/tandem solar cells. By end-user, the market is segmented into residential, commercial/industrial, utility-scale, and off-grid applications. The report also covers the market size and forecasts for the solar cell paste market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Silver Paste |

| Aluminum Paste |

| Copper Paste |

| Silver-Coated-Copper Paste |

| Lead-Free Multi-Metal Paste |

| Monocrystalline Cells |

| Polycrystalline Cells |

| Thin-Film Cells |

| Heterojunction (HJT) Cells |

| Perovskite and Tandem Cells |

| Residential |

| Commercial and Industrial |

| Utility-Scale |

| Off-Grid/Micro-grid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Silver Paste | |

| Aluminum Paste | ||

| Copper Paste | ||

| Silver-Coated-Copper Paste | ||

| Lead-Free Multi-Metal Paste | ||

| By Application | Monocrystalline Cells | |

| Polycrystalline Cells | ||

| Thin-Film Cells | ||

| Heterojunction (HJT) Cells | ||

| Perovskite and Tandem Cells | ||

| By End-User | Residential | |

| Commercial and Industrial | ||

| Utility-Scale | ||

| Off-Grid/Micro-grid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the solar cell paste market by 2031?

The solar cell paste market size is projected to reach USD 18.60 billion by 2031.

Which paste type is growing fastest?

Lead-Free Multi-Metal Paste is expanding at a 14.1% CAGR due to tightening lead regulations and cost-reduction goals.

How will localization policies affect suppliers?

Programs like the IRA and REPowerEU are spurring regional blending plants, trimming lead times from 90 days to about 30 days and shifting supply closer to Western cell factories.

Why are silver-coated-copper pastes attracting interest?

They can cut metallization cost per watt by up to 30% while retaining more than 98% of silver conductivity, though reliability testing is still under way.

Which region dominates demand?

Asia-Pacific held 62.7% of solar cell paste market share in 2025 and remains the fastest-growing region through 2031.

Page last updated on: