Soft Magnetic Material Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

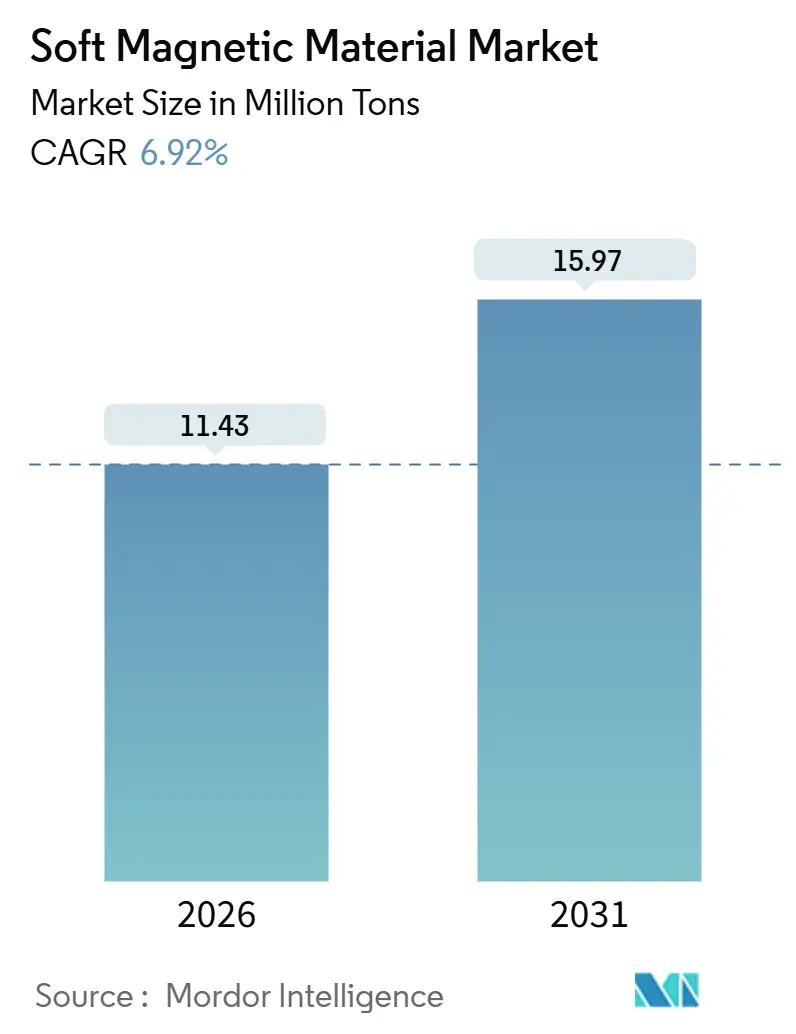

| Market Volume (2026) | 11.43 Million tons |

| Market Volume (2031) | 15.97 Million tons |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

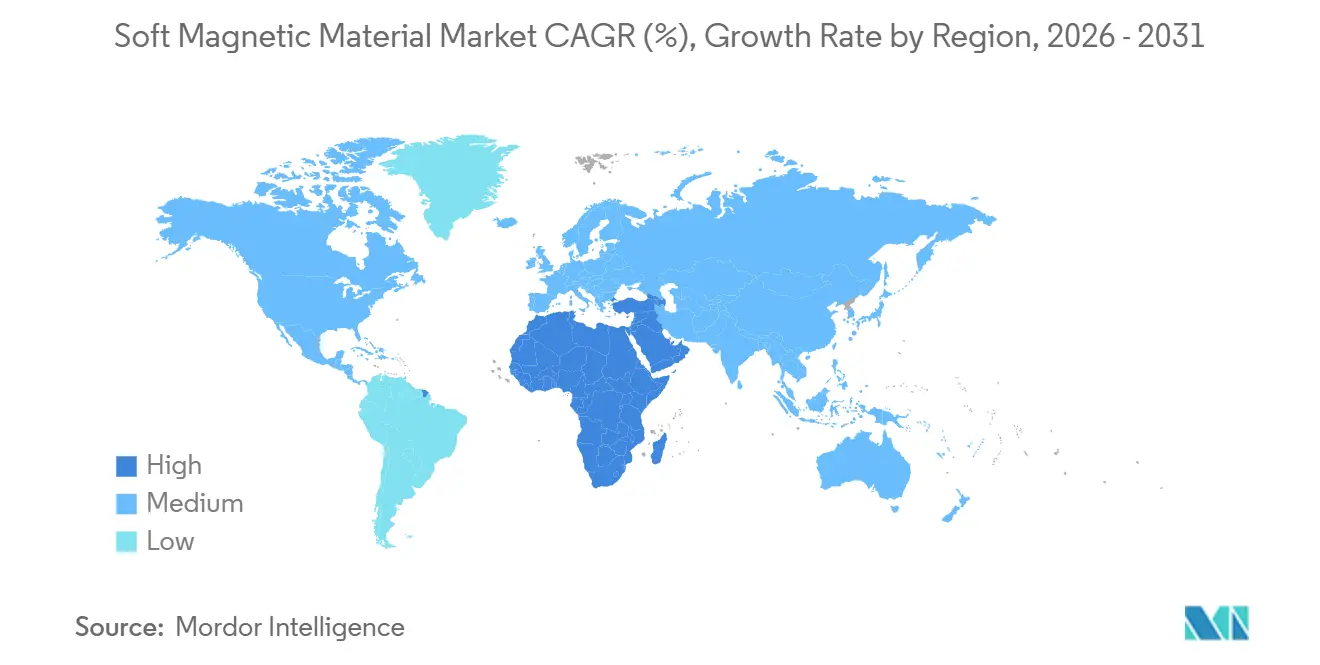

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

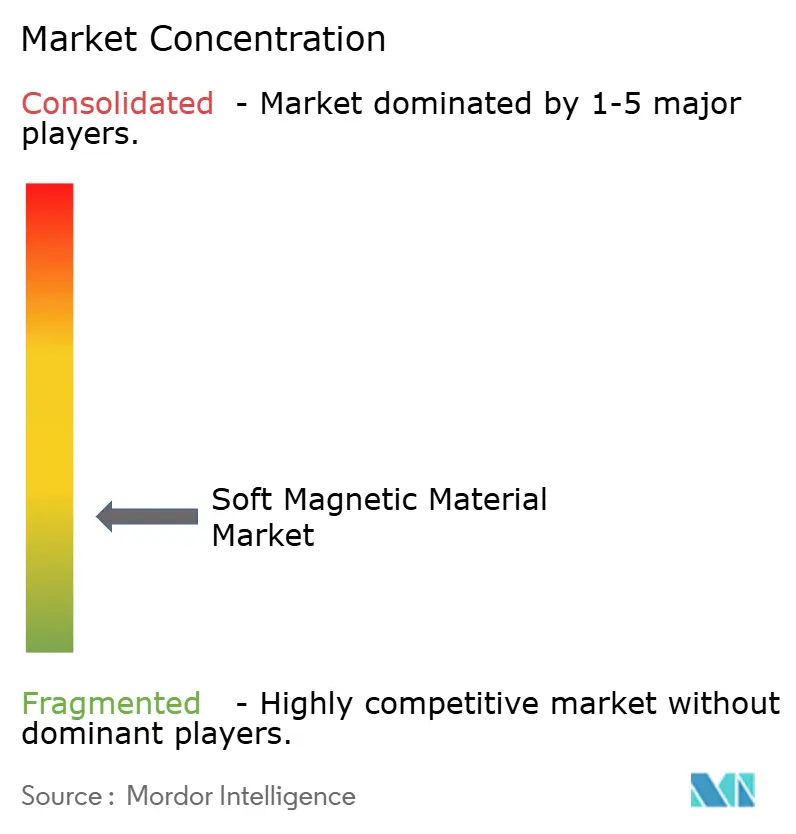

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soft Magnetic Material Market Analysis by Mordor Intelligence

The Soft Magnetic Material Market size is estimated at 11.43 million tons in 2026, and is expected to reach 15.97 million tons by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Rapid electrification of vehicle powertrains, stringent energy-efficiency rules for transformers and motors, and the migration of consumer-electronics power stages toward switching frequencies above 100 kHz are the primary growth catalysts. Electric steel retains critical volume thanks to its cost-per-kilowatt advantage, yet demand for soft magnetic composites and nanocrystalline ribbons is accelerating as designers target lighter, quieter, and higher-frequency cores. Asia-Pacific dominates the soft magnetic materials market due to China’s integrated steel ecosystem and India’s transformer build-out, while the Middle-East and Africa are emerging as the fastest-growing region on the back of grid-modernization projects. Competitive dynamics are shifting as powder-metallurgy specialists and additive-manufacturing start-ups win share from incumbent steelmakers through custom geometries and three-dimensional flux paths.

Key Report Takeaways

- By material type, electric steel led with 52.46% of the soft magnetic materials market share in 2025, while soft magnetic composites and advanced ferrites are advancing at a 7.34% CAGR through 2031.

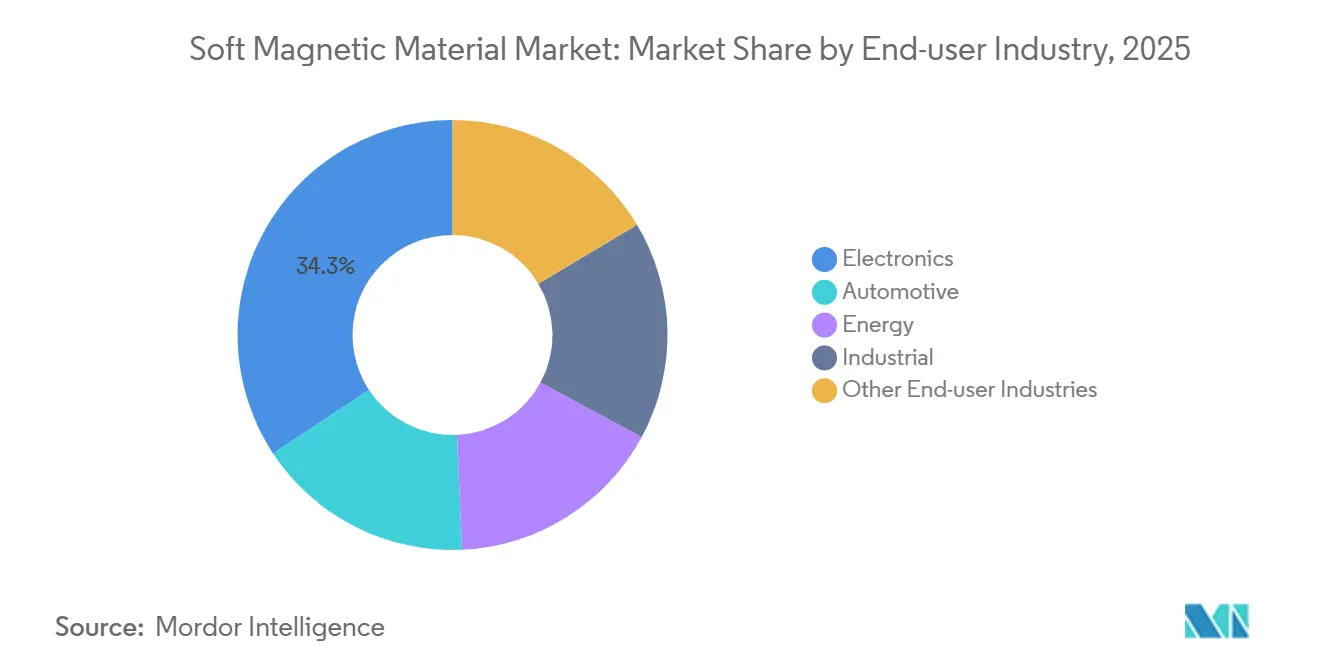

- By end-user industry, electronics contributed 34.28% of 2025 volume, but automotive is forecast to expand at a 7.27% CAGR to 2031 on the back of rapid EV and HEV adoption.

- By geography, the Asia-Pacific held 49.37% of the market share in 2025. While the Middle-East and Africa are forecast to expand at a 7.22% CAGR through 2031, the fastest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soft Magnetic Material Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics-miniaturization demand surge | +1.2% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Electrification of transformers and motors | +1.5% | EU and China, expanding to India and ASEAN | Long term (≥ 4 years) |

| Rapid EV/HEV power-train adoption | +1.8% | APAC core, North America, Western Europe | Medium term (2-4 years) |

| Additive manufacturing of custom cores | +0.6% | North America and EU | Long term (≥ 4 years) |

| Nanocrystalline and amorphous cores for SiC/GaN power electronics | +1.1% | Global research and development led by Japan, Germany, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electronics-Miniaturization Demand Surge

As demand surges for ultra-compact inductors in smartphones, wearables, and edge-AI servers, designers are increasingly gravitating towards switching frequencies exceeding 1 MHz[1]Apple Inc., “Apple Annual Report 2025,” apple.com. At these frequencies, laminated silicon steel faces significant eddy-current losses. In the realm of DC-DC converters under 100 W, ferrite beads, powder cores, and soft magnetic composites have taken the lead. Within rack-level power-delivery networks, point-of-load converters are now seeking magnetic components under 5 mm³. This preference has led to a rise in distributed-gap powder cores, known for maintaining inductance even under DC bias. Suppliers are innovating by co-firing nickel-zinc ferrite with low-temperature co-fired ceramic substrates. This integration allows for the embedding of capacitors and magnetics within modules just 1 mm thick, marking a decisive move away from conventional laminated cores. The outcome? Enhanced performance characterized by increased power density and reduced EMI, solidifying the position of advanced ferrites and composites in the soft magnetic materials market.

Electrification of Transformers and Motors

Regulators have aggressively targeted loss reductions for transformers and industrial motors. Under IEC 60034-30-1, the IE4 and IE5 classes are mandated, achieving significant cuts in no-load losses[2]International Electrotechnical Commission, “IEC 60034-30-1,” iec.ch. To comply, grain-oriented electric steel is needed, boasting a high flux density at 50 Hz. Additionally, non-oriented grades must be optimized for high-frequency traction motors. The EU's Ecodesign extension is now encompassing sub-0.75 kW motors. This shift is channeling additional volumes into fractional-horsepower drives, which traditionally relied on lower-grade cold-rolled steel. On another front, there's ongoing experimentation with amorphous metal stators. These hold the potential for a remarkable reduction in core losses, though their brittleness poses a challenge in manufacturing. As a result of these regulatory pushes, there's a sustained baseline demand for electric steel. Simultaneously, these developments are carving out niches for amorphous and nanocrystalline alternatives in the soft magnetic materials market.

Rapid EV/HEV Power-Train Adoption

Battery-electric and plug-in hybrids consumed soft magnetic material in 2025, with a significant portion going into traction motors. Each permanent-magnet synchronous motor requires non-oriented electric steel, and migration to 800 V architectures is boosting the need for nanocrystalline common-mode chokes. Ferrite-assisted synchronous reluctance motors, commercialized by leading European automakers in 2024–2025, forgo rare-earth magnets but raise soft magnetic content per vehicle. China’s production of new-energy vehicles increased in 2025, and output is expected to grow further by 2028, implying cumulative demand over the forecast horizon. This makes automotive the highest-growth opportunity within the soft magnetic materials market.

Additive Manufacturing of Custom Cores

Laser powder-bed fusion and binder jetting have enabled the creation of toroidal and topology-optimized cores, a feat previously unattainable through stamping or tape winding. A 3D-printed nanocrystalline transformer core achieved a reduction in no-load losses and elevated power density. Presently, challenges persist with build speeds lagging and powder costs remaining high. Yet, aerospace and medical OEMs have emerged as early adopters, drawn by the elimination of tooling and the advantages of conformal cooling features. Additive manufacturing could capture demand in programs characterized by low volume and high mix. As advancements in throughput and powder recycling continue, additive manufacturing is poised to become a pivotal differentiator for suppliers in the competitive landscape of the soft magnetic materials market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (Fe, Ni, Co) | -0.8% | Global, with acute impact on permalloy and supermalloy producers in North America and Europe | Short term (≤ 2 years) |

| Substitute competition (laminated alloys, powder cores) | -0.4% | Global, concentrated in mid-frequency applications (10-100 kHz) across automotive and industrial segments | Medium term (2-4 years) |

| EMC and safety compliance cost escalation | -0.3% | Global, most acute in EU and North America due to stringent IEC 61000 series enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Fe, Ni, Co)

Nickel prices swung during 2024–2025, while cobalt also experienced significant fluctuations, compressing margins for nickel permalloy producers. Silicon-metal surcharges for electrical steel spiked in early 2025 after power-curtailment policies in Yunnan and Sichuan provinces, further unsettling cost structures. Several western mills idled capacity or reformulated toward iron-cobalt alloys, creating supply uncertainty that encourages OEMs to dual-source or backward-integrate. Although iron ore stayed relatively stable, the nickel and cobalt volatility introduced a drag on the soft magnetic materials market CAGR.

Substitute Competition and EMC Compliance Cost Escalation

Powder cores and distributed-gap ferrites are eroding silicon-steel share below 100 kHz by offering lower eddy-current loss and complex shapes despite higher raw-material cost. IEC 61000-4-8 now mandates magnetic-field immunity testing, adding shielding or core redesign per inverter and extending product cycles. Certification fees burden small manufacturers and consolidate demand with vertically integrated players. The combined expense shaves growth from the forecast CAGR across the soft magnetic materials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Volume Anchored in Electric Steel, Innovation Led by Composites

Electric steel captured 52.46% of 2025 volume, buoyed by grain-oriented grades achieving high flux density and low core losses. To cater to the rising demand for traction motors, manufacturers bolstered their cold-rolling capacity during 2024 and 2025. Cobalt alloys, prized in aerospace, maintain Curie points exceeding 900 °C. While iron-based powder cores cater to mid-frequency inductors, their permeability is capped at sub-200 values. On the other hand, soft magnetic composites and advanced ferrites are advancing at a 7.34% CAGR through 2031. Dominating EMC suppression, nickel-zinc and manganese-zinc ferrites saw widespread adoption. This landscape positions electric steel as the volume cornerstone, while composites and nanocrystalline alloys command premium margins, highlighting a strategic investment landscape in the soft magnetic materials market from 2026 to 2031.

By End-User Industry: Electronics Leads Share, Automotive Powers Growth

Electronics accounted for 34.28% of 2025 demand, reflecting massive inductor and filter counts in power supplies, data-center racks, and mobile devices. Unit growth is modest, but miniaturization steers the mix toward high-value ferrites. Automotive applications are expanding at a 7.27% CAGR, with battery-electric vehicles now incorporating more magnetics compared to internal-combustion cars.

In 2025, energy infrastructure consumption was driven by UHV lines in China and India that necessitate premium grain-oriented steel. Industrial motors and automation saw increased demand, with upgrades to IE4/IE5 boosting the need for non-oriented steel. While niche applications in medical imaging and telecom together make up a smaller share of the volume, they command elevated prices due to their stringent performance requirements. This diverse consumption profile highlights the need for multi-material portfolios in the soft magnetic materials market to strike a balance between scale and profitability.

Geography Analysis

Asia-Pacific held 49.37% of global volume in 2025, accounting for a significant share of the total volume. China's output of electrical steel and Japan's expertise in nanocrystalline ribbons were pivotal. India, with its consumption of grain-oriented steel for transformers, is ramping up local mill capacities to reduce imports. During 2024–2025, ASEAN nations drew in substantial foreign direct investment for magnetic-materials manufacturing, as producers shifted closer to automotive assembly hubs.

North America, capturing a notable portion of the 2025 demand, was driven by sectors like EV powertrains, data-center expansions, and aerospace electrification. Thanks to the Inflation Reduction Act, new electrical-steel lines are emerging, highlighted by Arnold Magnetic Technologies' addition of capacity in 2025. Europe, with its consumption of electrical steel, is navigating strict Ecodesign regulations, especially with many of its industrial motors set for IE4 upgrades by 2027.

The Middle-East and Africa are on track for a 7.22% CAGR, bolstered by renewable-grid projects in Saudi Arabia, the UAE, and South Africa, all of which have a pressing need for low-loss transformer cores. In South America, the market is predominantly Brazilian, where the production of automotive and white goods propels the demand for non-oriented steel. While Gerdau and Aperam cater to local motor manufacturers, grain-oriented grades still find their way through imports. This geographic dispersion in both demand and capacity highlights the critical need for regionalized supply chains in the soft magnetic materials market.

Competitive Landscape

The soft magnetic material market is fragmented. Integrated steel giants have slashed conversion costs by operating continuous-annealing lines. Leaders in powder metallurgy are outpacing their competitors by offering soft magnetic composites that not only reduce assembly labor but also allow for intricate shapes. Suppliers of nanocrystalline materials dominate high-margin niches, with their ribbons fetching high prices and boasting significant gross margins. In terms of strategic maneuvers, expansions and acquisitions have been notable, along with joint ventures focusing on high-flux-density electric steel. The landscape of technology differentiation is evolving, now emphasizing additive manufacturing, gradient-index cores, and alloys tailored for specific applications, thereby elevating the entry barriers for newcomers in the soft magnetic materials arena.

Soft Magnetic Material Industry Leaders

PROTERIAL, Ltd.

TDK Corporation

JFE Steel Corporation

VACUUMSCHMELZE GmbH & Co. KG

Daido Steel Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Advanced Technology & Materials Co., Ltd. stated that new projects in its materials portfolio, including amorphous and nanocrystalline materials, were started in 2025. This is expected to affect the magnetic material market.

- February 2025: Niterra acquired Toshiba Materials, now called Niterra Materials, which makes amorphous and soft-magnetic noise-suppression products. This acquisition is expected to strengthen Niterra's position in the market.

- March 2024: Cyclic Materials, a metals recycling company, partnered with VACUUMSCHMELZE (VAC), a magnetic materials developer, to recycle by-products from permanent magnets. This supports a sustainable supply chain for EVs, wind turbines, and electronics.

Global Soft Magnetic Material Market Report Scope

A material that can be easily magnetized and demagnetized is called a soft magnetic material. These materials have low coercivity and high permeability.

The soft-magnetic material market is segmented by material type, end-user industry, and geography. By material type, the market is segmented into electric steel, cobalt, iron, nickel, and other material types (soft magnetic composites (SMC), soft ferrite, silicon ferrite, permalloy, supermalloy, etc.). By end-user industry, the market is segmented into electronics, automotive, energy, industrial, and other end-user industries (telecommunication, medical, industrial transformers, etc.). The report also covers the market size and forecasts for the soft magnetic material market for 17 major countries. For each segment, the market sizing and forecasts have been done in terms of volume(Tons).

| Electric Steel |

| Cobalt |

| Iron |

| Nickel |

| Other Material Types (Soft Magnetic Composites (SMC), Soft Ferrite, Silicon Ferrite, Permalloy, Supermalloy, etc.) |

| Electronics |

| Automotive |

| Energy |

| Industrial |

| Other End-user Industries (Telecommunication, Medical, Industrial Transformers, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Electric Steel | |

| Cobalt | ||

| Iron | ||

| Nickel | ||

| Other Material Types (Soft Magnetic Composites (SMC), Soft Ferrite, Silicon Ferrite, Permalloy, Supermalloy, etc.) | ||

| By End-user Industry | Electronics | |

| Automotive | ||

| Energy | ||

| Industrial | ||

| Other End-user Industries (Telecommunication, Medical, Industrial Transformers, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global demand for soft magnetic materials and their expected growth by 2031?

Worldwide consumption is 11.43 million tons in 2026 and is projected to reach 15.97 million tons by 2031, reflecting a 6.92% CAGR.

How are electric vehicles changing the consumption of soft magnetic materials?

Each battery-electric vehicle uses magnetic cores, and rising EV output is adding incremental demand between 2026 and 2031.

Which material segment is expanding fastest within soft magnetic materials?

Soft magnetic composites and advanced ferrites are growing at a 7.34% CAGR through 2031, outpacing traditional electric steel.

Why is Asia-Pacific the dominant production hub for soft magnetic materials?

China’s integrated steel mills, India’s transformer build-out, and ASEAN’s cost-competitive plants give the region nearly half of global volume.

How do raw material price swings affect suppliers of soft magnetic materials?

Volatility in nickel and cobalt prices has impacted permalloy margins, prompting some producers to either idle their capacity or reformulate their alloys.

Page last updated on: