Soap Noodles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

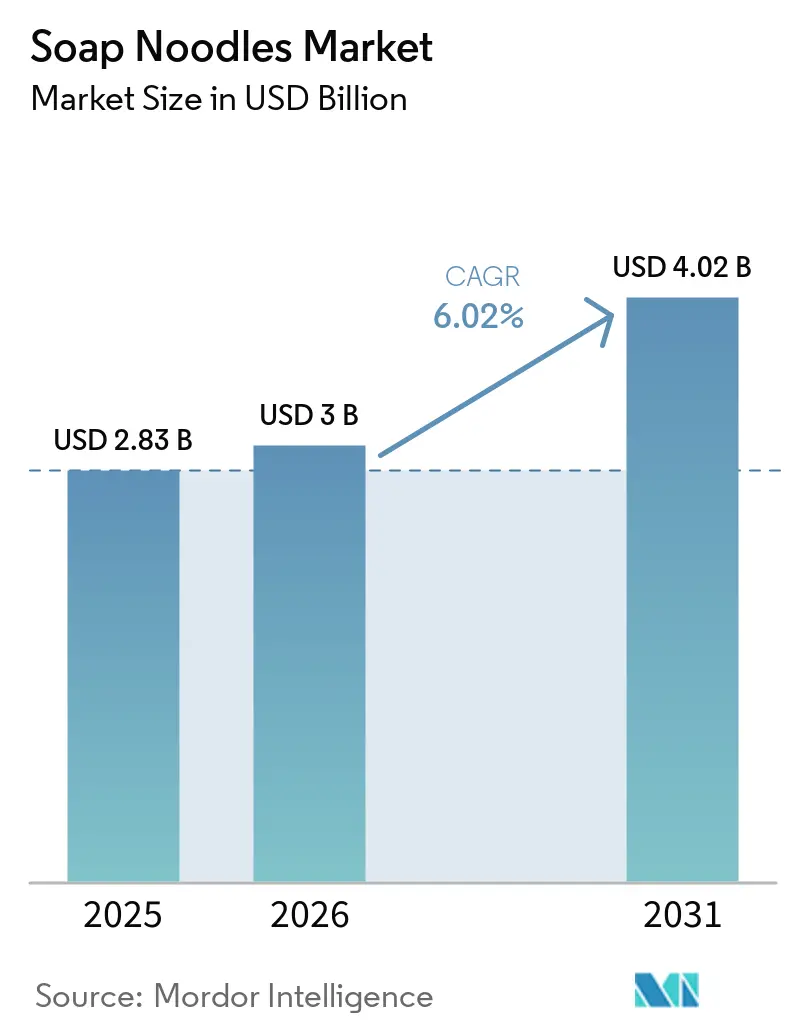

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soap Noodles Market Analysis by Mordor Intelligence

The Soap Noodles Market size is expected to increase from USD 2.83 billion in 2025 to USD 3 billion in 2026 and reach USD 4.02 billion by 2031, growing at a CAGR of 6.02% over 2026-2031. Structural changes in oleochemical feedstock allocation, increasing compliance costs due to new deforestation regulations, and a growing consumer preference for plant-derived personal-care bars are influencing demand. Indonesia's B60 biodiesel program has reduced the availability of palm-based feedstocks. This has raised soap-noodle spot prices above USD 900 per ton and established an 88% correlation between feedstock prices and upstream crude palm oil values. In North America and Europe, the trend of premiumization is advancing. Google Trends data indicates that searches for luxury hand soap have tripled year-over-year, leading manufacturers to introduce high-purity, traceable grades that command a 3%-5% premium. Capacity expansions in Indonesia, Malaysia, and India, along with blockchain-enabled traceability platforms, are providing a competitive advantage to vertically integrated producers. These producers are better positioned to manage raw-material price fluctuations and ensure sustainable sourcing documentation.

Key Report Takeaways

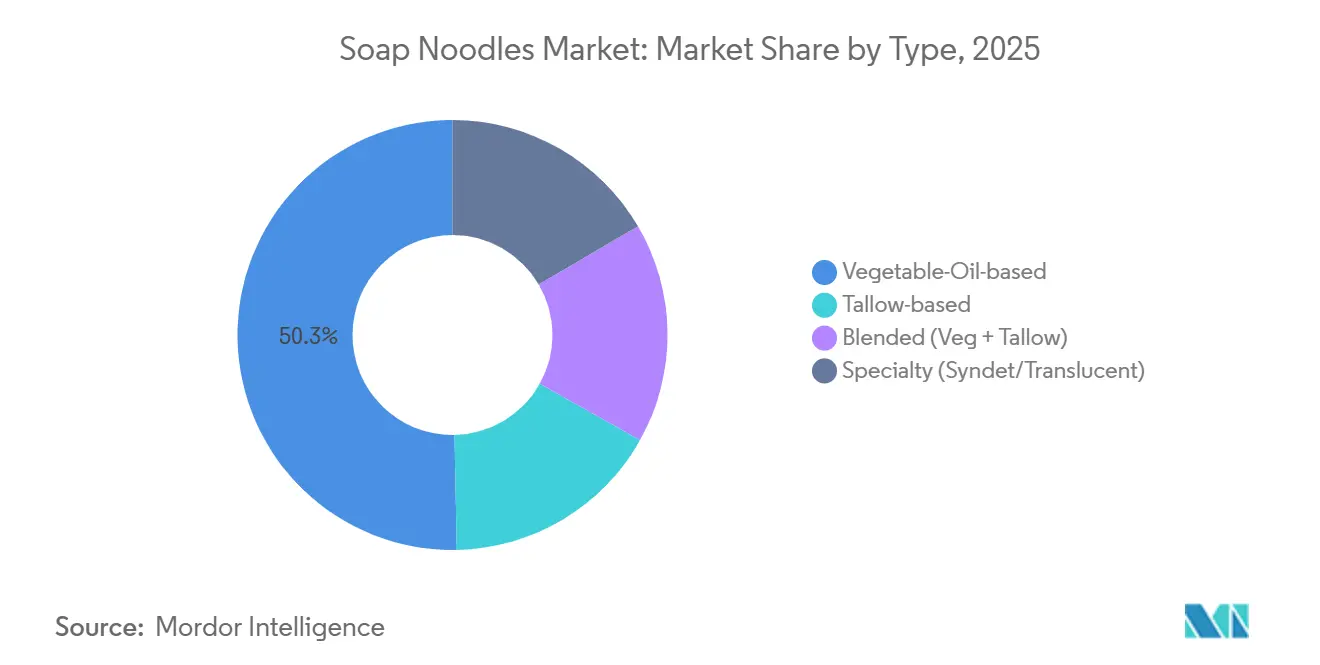

- By type, vegetable-oil-based formulations led with 50.31% of the soap noodles market share in 2025, and Specialty (Syndet/Translucent) will rise at 6.27% CAGR to 2031.

- By production process, the saponification route led with 59.22% of the soap noodles market share in 2025, and the neutralization route is forecast to expand at a 6.31% CAGR through 2031, the fastest among all production processes.

- By application, personal hygiene soap accounted for 46.17% of the soap noodles market size in 2025, and specialty and hand-crafted bars are projected to grow at a 6.47% CAGR to 2031.

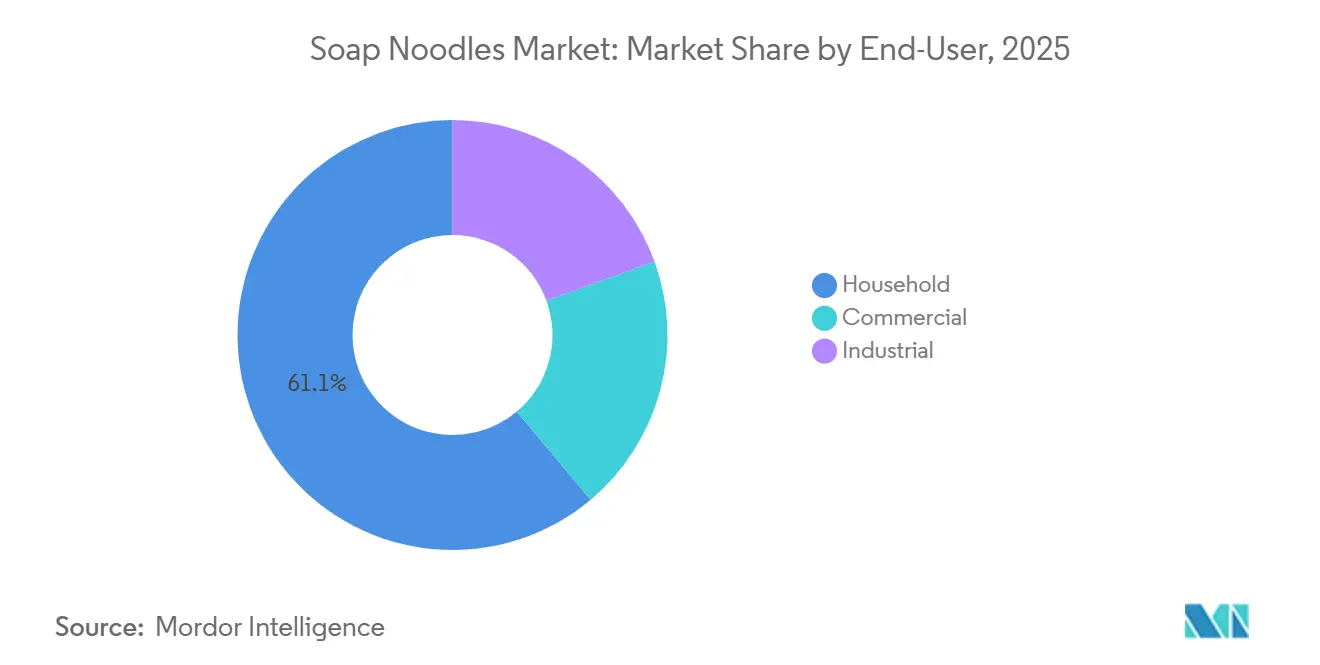

- By end-user, household led with 61.11% of the soap noodles market share in 2025, and the commercial end-user segment is expected to register a 6.65% CAGR between 2026 and 2031.

- By distribution channel, direct/bulk contracts captured 60.45% of the soap noodles market share in 2025, and online platforms are set to rise at a 7.28% CAGR through 2031.

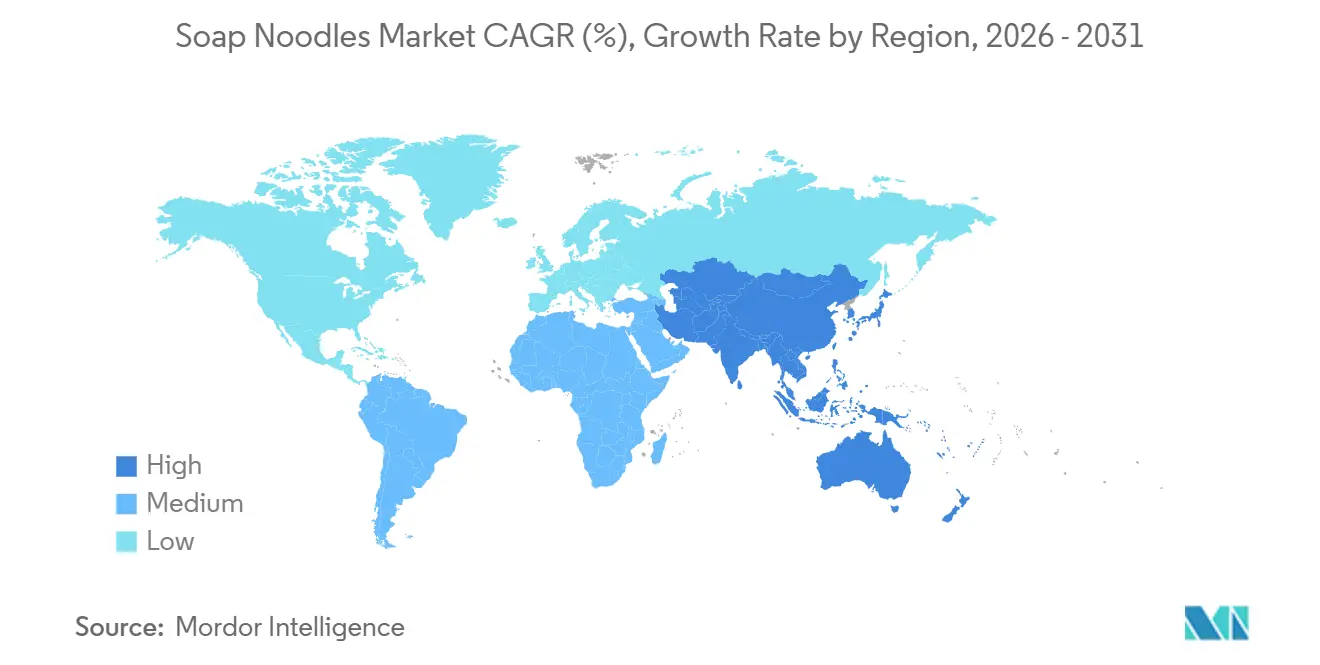

- By geography, Asia-Pacific captured 66.12% share in 2025 and is projected to advance at a 7.22% CAGR to 2031, the strongest regional performance.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soap Noodles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of Asia-Pacific oleochemical capacity | +1.2% | Indonesia, Malaysia, India, China; spill-over to Middle East & Africa | Medium term (2–4 years) |

| Premiumisation of bar-soap formats | +0.8% | North America, Europe; emerging in urban Asia-Pacific (India, China) | Long term (≥ 4 years) |

| Blockchain-enabled palm-oil traceability | +0.6% | Global, with strongest adoption in EU and North America supply chains | Short term (≤ 2 years) |

| E-commerce-driven craft-soap micro-brands | +0.5% | North America, Europe, urban India; nascent in Latin America | Medium term (2–4 years) |

| Carbon-footprint–linked FMCG procurement mandates | +0.7% | Global, led by multinational FMCG headquartered in North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Asia-Pacific Oleochemical Capacity

In Southeast Asia, a decade's worth of oleochemical expansion is progressing at a significant pace creating strong momentum for the soap noodles market. Under the Ministry of Industry Regulation No. 13/2021, Indonesia aims to achieve a national capacity of 4 million tons. In Gresik, Wilmar International launched a new fatty-alcohol line with a capacity of 110,000 tons per annum, increasing the group's total output to 560,000 tons annually. Meanwhile, IOI Oleochemicals, following a USD 52 million upgrade, increased its Penang output by 15%[1]. Godrej Industries from India, with an investment of USD 90 million, plans to double its fatty-alcohol capacity and add 24,000 tons of glycerin, while targeting 75% renewable-energy usage at its facility. These strategic developments strengthen regional leadership as Indonesia's B60 biodiesel program redirects 15 million tons of crude palm oil, reducing the availability of exportable stearin and lauric acids. Companies with integrated operations, spanning plantations to downstream conversion, are better positioned to maintain margins, while standalone converters face challenges due to raw material constraints.

Premiumisation of Bar-Soap Formats

Consumers are increasingly favoring bar soaps with transparent labeling and artisanal qualities. Data from Google Trends indicates a rise in interest, with "luxury hand soap" reaching an index of 91 in October 2025, surpassing searches for "luxury bath soap" by over threefold. Brands utilizing cold-process methods, which retain glycerine and allow for botanical additions like jojoba and hemp, are achieving retail prices between USD 5-15 per bar. In 2024, handmade soap sales in India reached USD 3.77 billion, driven by Ayurvedic and vegan claims, and are projected to grow at a compound annual growth rate (CAGR) of 6.8%. Additionally, high-purity noodles, certified as sustainable and containing greater than or equal to 78% total fatty matter, are commanding premiums of 3% to 5% in the soap noodles market. This trend is being adopted by mainstream fast-moving consumer goods (FMCG) companies to protect brand equity.

Blockchain-Enabled Palm-Oil Traceability

The European Union Deforestation Regulation, effective in 2025, mandates plantation-level GPS (Global Positioning System) polygons for all palm-oil derivatives, making traceability a commercial requirement in the soap noodles market. Platforms such as Golden Agri-Resources' SmartTrace and Roundtable on Sustainable Palm Oil's (RSPO) PRISMA are leading the way by recording farm-gate transactions and satellite verifications on immutable ledgers. For example, during the palm-kernel-oil shortage of 2025, suppliers with certified contracts achieved 98% supply reliability compared to 85% for conventional buyers, highlighting the value of traceability in mitigating risks[2]. Although certified noodles incur a premium of up to 3.8%, the benefits of avoiding tariffs and reducing compliance penalties resulted in a net procurement saving of 2.1% for European Union buyers in early 2026.

E-Commerce-Driven Craft-Soap Micro-Brands

The growth of digital commerce has reduced entry barriers for artisan soap producers in the soap noodles market. In India, clean-process contract manufacturers now accept minimum runs of 500 bars. Platforms like Shopify enable these micro-brands to access international markets without retail mark-ups. This trend has increased demand for small-batch, vegan, and palm-free noodles, while also intensifying competition for specialty feedstocks. For instance, palm-kernel-oil prices rose by 5.5% in December 2025, impacting margins for start-ups without hedging strategies. In response, aggregator platforms have emerged, consolidating micro-brand orders to negotiate volume discounts on certified noodles, creating a new distribution model.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from syndet surfactant bases | -0.9% | Global, with highest substitution in North America & Europe | Long term (≥ 4 years) |

| European Union deforestation-free supply-chain compliance cost | -0.6% | EU importers; upstream impact on Indonesia & Malaysia exporters | Short term (≤ 2 years) |

| Shipping decarbonisation surcharges on palm-oil lanes | -0.4% | Southeast Asia to Europe/North America trade lanes | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Competition from Syndet Surfactant Bases

Syndet bars, formulated with sodium cocoyl isethionate or lauryl sulfoacetate, offer a milder pH and enhanced lather, driving their adoption in premium personal-care segments. In developed markets, liquid body washes, primarily syndet-based, have surpassed bar sales, reducing the demand for traditional soap noodles. Regulatory initiatives aimed at phasing out non-biodegradable surfactants are encouraging research and development (R&D) into oleochemical-derived alkyl polyglucosides. This trend provides soap noodle suppliers with an opportunity to diversify into the green surfactant market.

European Union Deforestation-Free Compliance Cost

Importers are now mandated to provide geo-referenced documentation verifying that palm-sourced products comply with deforestation-free requirements in the soap noodles market. This compliance process imposes higher costs on smallholders, particularly those without cadastral records. Certification and satellite monitoring increase costs by USD 3-5 per ton for traders, compressing margins for mid-tier participants and redirecting uncertified volumes to less regulated markets in South Asia and Africa at competitive prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Plant-Derived Grades Dominate but Blended Options Offer Flexibility

In 2025, vegetable-oil-based grades accounted for 50.31% of the soap noodles market, driven by multinational fast-moving consumer goods (FMCG) companies targeting a 40% reduction in petroleum-derived inputs. Indonesia and Malaysia, responsible for approximately 85% of global palm exports, form the foundation for this feedstock. However, Indonesia's B60 bio-diesel initiative has redirected up to 15 million tons of crude palm oil. This shift has constrained the supply of lauric acid and led to a 5.5% increase in palm kernel oil prices in December 2025. In the United States, tallow-based grades are increasingly utilized in renewable-diesel value chains, reducing their availability for traditional applications. Blended formulations of vegetable oils and tallow enhance hardness and lather while managing feedstock variability, though they add complexity to certification processes.

Specialty noodles, including translucent and syndet bases, are projected to grow at a 6.27% compound annual growth rate (CAGR) from 2026 to 2031, supported by the increasing demand for premium bars. The market for specialty soap noodles catering to the gift and hospitality sectors is expected to reach USD 720 million by 2031, reflecting a trend toward premiumization. Kao Corporation's 2025 off-take agreement for non-palm C12-C14 fatty alcohols indicates a growing preference for palm-free alternatives to mitigate sourcing risks in the soap noodles market.

By Production Process: Neutralization Gains Momentum

In 2025, saponification held a 59.22% market share, driven by its cost efficiency in household laundry bars. However, the neutralization of pre-split fatty acids is forecast to grow at a 6.31% CAGR, the highest in its category. This process, which retains glycerine and maintains lower free-alkali levels, is increasingly favored by skin-care brands. The market for neutralized soap noodles, particularly those linked to premium personal care, is projected to grow from USD 1.16 billion in 2026 to USD 1.59 billion by 2031. Godrej Industries' glycerine-rich output demonstrates how co-product monetization can improve margins while meeting moisturizing-bar requirements in the soap noodles market.

By Application: Specialty Bars Lead Growth Curve

In 2025, personal-hygiene bars represented 46.17% of total volume in the soap noodles market. However, specialty and hand-crafted formats are expected to grow at a 6.47% CAGR through 2031. The market share for luxury hand soap is increasing most rapidly in urban North America and Europe, influenced by social media trends and gifting practices. Brands using cold-process methods rely on high-purity noodles (with greater than or equal to 12% moisture) to maintain texture and scent, ensuring consistent demand even during fluctuations in commodity-grade prices.

By End-User: Commercial Buyers Accelerate Post-Pandemic

In 2025, households accounted for 61.11% of total consumption. However, commercial sectors including hospitality, institutional hygiene, and contract cleaning are forecast to grow at a 6.65% CAGR. As hotels transition from liquid amenity bottles to bar formats wrapped in compostable paper, demand is shifting toward certified-sustainable noodles suitable for smaller guest soaps. Meanwhile, industrial sectors use soap noodles as emulsifiers in textile and metalworking fluids, maintaining a steady and specialized demand.

By Distribution Channel: Digital Platforms Outpace Legacy Bulk Contracts

Direct annual contracts remain dominant, accounting for 60.45% of tonnage. This is particularly true for tier-1 FMCG buyers who manage feedstock costs with index-linked formulas. However, online business-to-business (B2B) platforms are projected to grow at a 7.28% CAGR. These platforms aggregate demand from smaller brands and provide real-time traceability documentation. By 2031, the market size of soap noodles transacted through digital channels is expected to exceed USD 500 million, driven by reduced intermediary costs and lower minimum order quantities.

Geography Analysis

In 2025, Asia-Pacific accounted for 66.12% of the global volume and is projected to grow at a 7.22% compound annual growth rate (CAGR), supported by capacity expansions and consumer preference for bar soap. Wilmar's recent expansion has increased the region's fatty-alcohol capacity to over 560,000 tons annually. Similarly, IOI Oleochemicals has enhanced its output by an additional 109,500 tons with an upgrade in Penang. India's USD 90 million investment in glycerine and fatty-alcohol capacity reflects a focus on domestic value addition. However, in 2026, floods caused by La Niña in North Sumatra reduced palm harvests, leading to a 15% price increase within a month and highlighting the industry's exposure to climate risks.

North America and Europe are experiencing the fastest growth in premium product adoption. Data from Google Trends indicates increased interest in luxury hand-soaps, driving demand for certified Roundtable on Sustainable Palm Oil (RSPO)-segregated and palm-free alternatives. Additionally, Kao's acquisition of U.S.-sourced, non-palm fatty alcohols and European Union (EU) freight surcharges due to disruptions in the Red Sea emphasize a shift in supply chains toward regional and alternative feedstocks.

In South America, the Middle East, and Africa, cost-effective laundry bars remain prevalent, but urban centers are showing initial interest in halal-certified and vegan products. Currency fluctuations against a strong U.S. dollar are reducing purchasing power, prompting formulators to either accept higher moisture levels or reduce the use of premium ingredients in response to rising import costs.

Competitive Landscape

The soap noodles market is moderately concentrated. Asian conglomerates, now more vertically integrated, are strengthening their position in the market. Wilmar acquired Natural Oleochemicals in Malaysia for USD 192 million, securing both upstream traceable feedstock and downstream conversion in a single transaction. KLK OLEO's acquisition of an Italian ester expands its European portfolio but also highlights potential overcapacity challenges; its newly established complex in East Kalimantan faced losses in 2025 due to reduced demand from the European Union (EU). Smaller players are differentiating themselves, with Golden Agri-Resources utilizing its SmartTrace blockchain traceability system to secure long-term contracts with fast-moving consumer goods (FMCG) companies that prioritize documentation over pricing. Additionally, high-purity certified noodles command a 3%-5% premium over commodity grades, providing a margin cushion during crude palm oil price spikes.

Soap Noodles Industry Leaders

IOI Oleochemicals

KLK OLEO

Musim Mas Group

Wilmar International Ltd

Godrej Industries Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: IOI Oleochemicals has partnered with ChemPoint to distribute Palmac stearic acid and glycerine across North America. This collaboration utilizes a digital platform to cater to the pharmaceutical and personal care industries. Stearic acid, a key ingredient in soap noodles, is widely used in these sectors.

- March 2025: Kao Corporation signed a multi-year agreement with Future Origins for non-palm-based C12 (dodecanol) and C14 (tetradecanol) fatty alcohols produced in the U.S. Midwest. This agreement aligns with Kao's strategy to support the production of palm-free soap noodles, which are a key ingredient in personal care products, including soaps and detergents.

Global Soap Noodles Market Report Scope

Soap noodles are the primary raw material, consisting of dried, saponified, and noodle-shaped soap flakes, used by manufacturers to produce soap bars. These noodles, typically derived from palm oil or animal fats, are combined with fragrances, colors, and additives. The mixture is then processed into final products such as toilet soap, laundry bars, and beauty soaps.

The soap noodles market is segmented by type, production process, application, end-user industry, distribution channel, and geography. By type, the market is segmented into vegetable-oil-based, tallow-based, blended (veg + tallow), and specialty (syndet/translucent). By production process, the market is segmented into the saponification route, the fatty-acid route, and the neutralization route. By application, the market is segmented into personal hygiene soap, laundry soap, multi-purpose soap, industrial use, and specialty/hand-crafted. By end-user industry, the market is segmented into household, commercial, and industrial. By distribution channel, the market is segmented into direct/bulk contracts, distributors and traders, and online platforms. The report also covers the market size and forecasts for asoap noodles in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Vegetable-Oil-based |

| Tallow-based |

| Blended (Veg + Tallow) |

| Specialty (Syndet/Translucent) |

| Saponification Route |

| Fatty-Acid Route |

| Neutralisation Route |

| Personal Hygiene Soap |

| Laundry Soap |

| Multi-purpose Soap |

| Industrial Use |

| Specialty/Hand-crafted |

| Household |

| Commercial |

| Industrial |

| Direct/Bulk Contracts |

| Distributors and Traders |

| Online Platforms |

| Asia-Pacific | China |

| India | |

| Indonesia | |

| Malaysia | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Vegetable-Oil-based | |

| Tallow-based | ||

| Blended (Veg + Tallow) | ||

| Specialty (Syndet/Translucent) | ||

| By Production Process | Saponification Route | |

| Fatty-Acid Route | ||

| Neutralisation Route | ||

| By Application | Personal Hygiene Soap | |

| Laundry Soap | ||

| Multi-purpose Soap | ||

| Industrial Use | ||

| Specialty/Hand-crafted | ||

| By End-User Industry | Household | |

| Commercial | ||

| Industrial | ||

| By Distribution Channel | Direct/Bulk Contracts | |

| Distributors and Traders | ||

| Online Platforms | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Indonesia | ||

| Malaysia | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the soap noodles market expected to grow through 2031?

The Soap Noodles Market size is expected to increase from USD 2.83 billion in 2025 to USD 3 billion in 2026 and reach USD 4.02 billion by 2031, growing at a CAGR of 6.02% over 2026-2031.

Which region contributes the most volume in the soap noodles market?

Asia-Pacific holds 66.12 % of global demand and is also the fastest-growing region at a 7.22 % CAGR.

What feedstock dominate current production?

Vegetable-oil-based grades, mainly from palm and palm-kernel oil, account for just over half of global volume.

Which distribution channel is rising the fastest?

Online B2B platforms are forecast to grow at a 7.28 % CAGR as they pool micro-brand demand and provide real-time sustainability documentation.

Page last updated on: