Myanmar Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

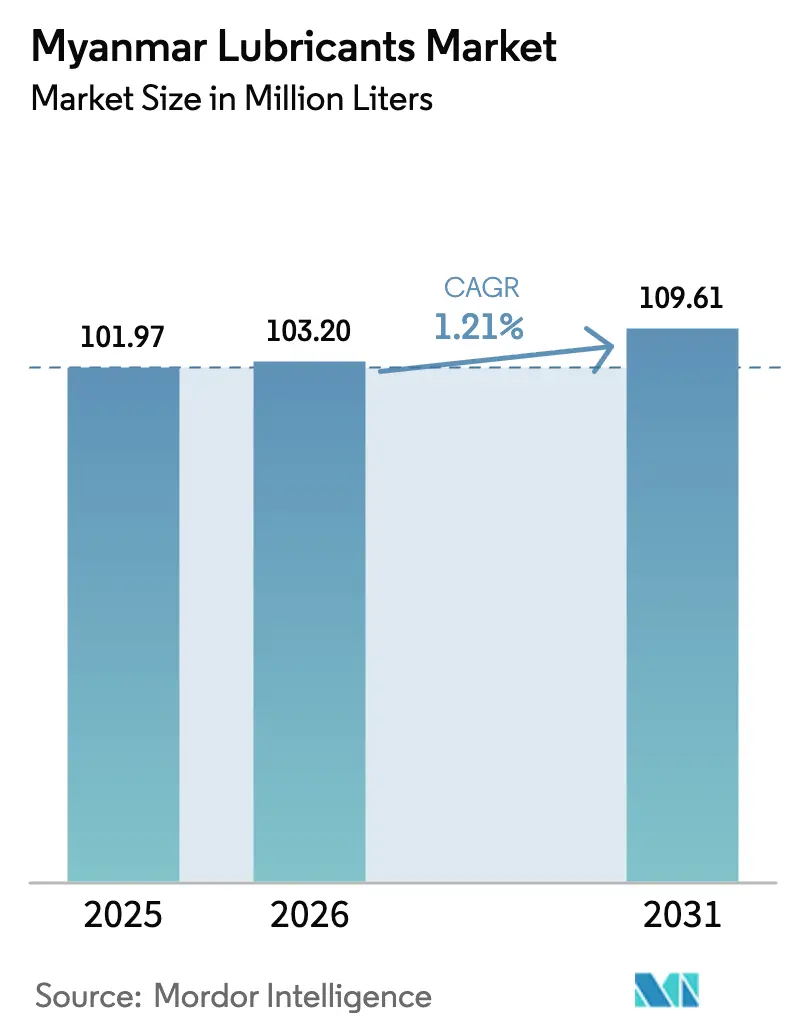

| Base Year Market Size (2025) | 101.97 Million liters |

| Market Volume (2026) | 103.2 Million liters |

| Market Volume (2031) | 109.61 Million liters |

| Growth Rate (2026 - 2031) | 1.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar Lubricants Market Analysis by Mordor Intelligence

The Myanmar Lubricants Market size is expected to grow from 101.97 million liters in 2025 to 103.2 million liters in 2026 and is forecast to reach 109.61 million liters by 2031 at 1.21% CAGR over 2026-2031. This steady trajectory reflects a gradual rebound in industrial activity, persistent growth of the national vehicle parc, and government-led infrastructure spending that lifts lubricant consumption across automotive, heavy equipment, and power-generation applications. Engine oils remain the core volume driver because of the country’s dependence on internal-combustion engines, while diesel-based backup power systems sustain incremental demand from utilities and commercial facilities. Parallel trends, such as agricultural mechanization and the expansion of the mining sector, diversify end-use opportunities, although foreign-exchange volatility and import licensing delays temper near-term growth prospects. International brands participate mainly through distributors, creating space for agile local suppliers to capture share in the Myanmar lubricants market.

Key Report Takeaways

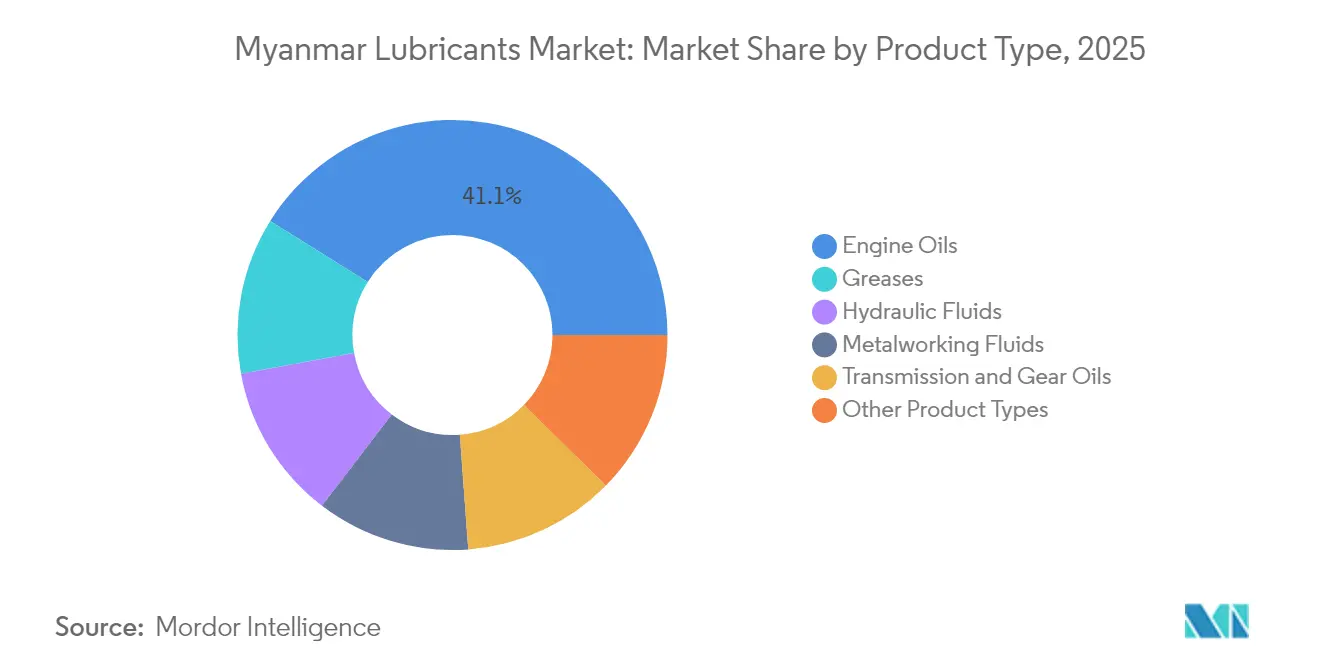

- By product type, engine oils commanded 41.10% of the Myanmar Lubricants market share in 2025, and the segment is projected to grow at a 1.72% CAGR to 2031.

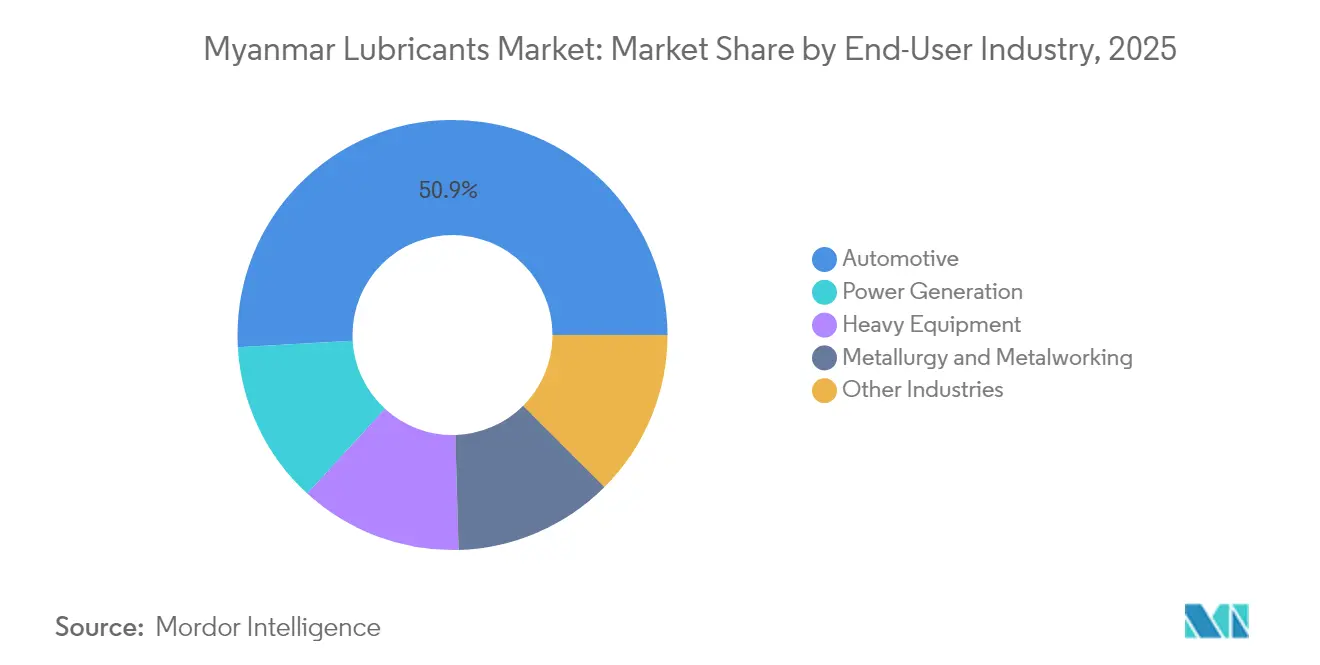

- By end-user industry, the automotive segment accounted for 50.90% of the Myanmar Lubricants market size in 2025, while power generation is set to expand at a 1.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Myanmar Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle-parc and aftermarket demand | +0.4% | Yangon and Mandalay corridors | Medium term (2-4 years) |

| Rapid mechanization of agriculture | +0.3% | Central Myanmar and Ayeyarwady Delta | Long term (≥ 4 years) |

| Expansion of mining and heavy machinery fleets | +0.2% | Kachin, Shan, coastal regions | Medium term (2-4 years) |

| Government-backed road-freight corridors | +0.2% | Cross-border routes to China, Thailand, India | Long term (≥ 4 years) |

| Re-refining incentives enlarging base-oil pool | +0.1% | Yangon industrial zones and planned refineries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle-Parc and Aftermarket Demand

Vehicle registrations have recovered sharply since 2024, supported by easing import rules that widen model choices and lower acquisition costs. Commercial trucks servicing the China–Myanmar Economic Corridor clock high annual mileage, accelerating oil-drain intervals and spurring repeat purchase cycles in the Myanmar lubricants market. Local workshops rely on affordable multigrade engine oils, encouraging parallel imports and private-label offerings. Growing ride-hailing fleets increase regular maintenance volumes, while the increasing density of motorcycles in peri-urban zones sustains demand for two-stroke and four-stroke oils. Aftermarket retailers utilize flexible payment terms to foster loyalty among a price-sensitive consumer base.

Rapid Mechanization of Agriculture

National mechanization programs subsidize tractor loans and harvesting equipment, thereby driving the uptake of lubricants in rural supply chains. Imported machinery operates under tropical heat and dust, necessitating premium hydraulic fluids and gear oils with robust oxidation resistance. Dealer-bundled service contracts lock in lubricant offtake and introduce farmers to higher performance grades that reduce downtime. Development agencies fund training on preventive maintenance, reinforcing awareness of the proper selection of oil. As acreage under mechanized cultivation rises, the Myanmar lubricants market benefits from predictable lubricant replenishment cycles that align with planting and harvesting seasons.

Expansion of Mining and Heavy Machinery Fleets

Mining concessions in jade, copper, and rare-earth deposits attract modern excavators, haul trucks, and stationary compressors that require specialized high-viscosity lubricants. Remote sites in Kachin and Shan States require bulk delivery and on-site storage solutions, favoring suppliers that offer drum-to-bulk conversion programs. Equipment OEMs stipulate the use of longer-life synthetic or semi-synthetic oils to meet warranty terms, nudging the product mix toward premium formulations and widening margins in the Myanmar lubricants market. Environmental regulations on waste oil disposal further encourage advanced lubricants with extended drain intervals. Rising commodity prices sustain capital inflows, anchoring lubricant demand over the medium term.

Re-Refining Incentives Enlarging Domestic Base-Oil Pool

Fiscal incentives for used-oil collection and re-refining help diversify base-oil supply and buffer against import disruptions. Planned recycling plants near Yangon target Group I and light Group II output, which can cover a portion of domestic blending needs. A stable waste-oil stream lowers feedstock costs and supports competitive local brands, potentially compressing price gaps versus foreign products. Environmental compliance strengthens brand credibility, aiding market penetration among industrial customers. Over time, re-refined base oils could supply higher-value specialties, enhancing overall self-reliance of the Myanmar lubricants market[1]Ministry of Electricity and Energy, “Used-Oil Re-Refining Incentives,” moee.gov.mm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of electric two-wheelers | -0.20% | Urban centers, particularly Yangon and Mandalay | Short term (≤ 2 years) |

| Crude-price volatility pressuring margins | -0.10% | National, affecting all distribution channels | Short term (≤ 2 years) |

| Import-licence delays disrupting supply continuity | -0.10% | National, concentrated at major ports and border crossings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Electric Two-Wheelers

Urban consumers are adopting battery-powered scooters in response to fuel price swings and municipal incentives, thereby curbing demand for conventional motorcycle engine oils. Although the electric segment currently accounts for less than 4% of two-wheeler sales, accelerated uptake could erode a key volume contributor to the Myanmar lubricants market over the next two years. Suppliers explore dielectric fluids and specialty greases for hub motors, but replacement intervals and volumes remain lower than for combustion counterparts. Workshops face revenue loss from oil-change services, hastening a pivot to broader maintenance packages. Traditional lubricant brands must adapt marketing and product portfolios to capture emerging opportunities in the e-mobility ecosystem.

Crude-Price Volatility Pressuring Margins

The country imported USD 4.53 billion worth of refined fuels in 2024, exposing distributors to fluctuating landed costs and tight working-capital cycles. Smaller players often lack hedging instruments and absorb price shocks, thereby compressing their operating margins. Import licensing bottlenecks lead to higher inventory holdings, thereby amplifying exposure. Currency depreciation inflates dollar-denominated base-oil purchases, further squeezing profitability in the Myanmar lubricants industry. Persistent volatility may trigger market exits or consolidation, altering the competitive fabric.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Drive Market Leadership

Engine oils retained 41.10% of the Myanmar lubricants market share in 2025, reflecting the dominance of internal-combustion engines across automotive and industrial settings. The segment is projected to expand at a 1.72% CAGR through 2031, outpacing the broader Myanmar lubricants market. Entry-level mineral grades continue to appeal to cost-conscious vehicle owners; however, gradually rising awareness of extended-drain semi-synthetics opens up room for value migration. Greases follow as the next significant product line, supplying indispensable protection for bearings in mining and construction machinery. Hydraulic fluids are experiencing steady sales momentum as infrastructure spending increases, leading to higher excavator and loader usage. Metalworking fluids, although still niche, are benefiting from the growing machining activity at the Thilawa Special Economic Zone. Transmission and gear oils are experiencing moderate growth, constrained by longer service intervals and advancements in drivetrain technologies.

The Myanmar lubricants market size for greases is forecast to approach 16.4 million liters by 2031, advancing at around 1.22% CAGR, driven by heavy-equipment rebuild cycles and the mining sector’s high shock-load requirements. Hydraulic-fluid demand benefits from government road-building and border logistics projects, pushing the sub-segment toward 12.35 million liters by the end of the decade. Metalworking fluids could reach 4.15 million liters as local fabrication value chains deepen. While volume growth in transmission and gear oils lags, premium formulations offering fuel economy and seal compatibility give suppliers pricing leverage. Overall, product diversification shields the Myanmar lubricants market from abrupt swings in any single application area.

By End-User Industry: Automotive Sector Dominance

The automotive sector represented 50.90% of the Myanmar lubricants market size in 2025 and remains the primary consumption pillar. The country produced 2,711 motor vehicles in 2024. Commercial trucks traversing cross-border corridors undergo frequent oil changes, while rapidly expanding ride-hailing fleets create consistent demand for passenger vehicles. Motorcycles contribute sizable volumes of two-stroke and four-stroke models, despite growing electric competition. Heavy-equipment users form the second-largest end-user group, consuming hydraulic fluids, greases, and gear oils for construction and resource-extraction machines. Power generation is projected to display the fastest CAGR of 1.56% through 2031, driven by the continued reliance on diesel generators during grid expansion phases.

Metallurgy and metalworking facilities draw on neat cutting oils and water-soluble coolants on a domestic manufacturing scale. Consumer goods factories and food processors constitute additional, albeit smaller, demand centers for lubricants. Collectively, these applications diversify exposure and stabilize overall growth in the Myanmar lubricants market. Migration of automotive workshops toward preventive-maintenance packages broadens the sale of ancillary fluids and greases. Industrial customers increasingly request technical support and oil-analysis services, presenting differentiation avenues for suppliers with on-site expertise.

Geography Analysis

Yangon and Mandalay corridors together account for an estimated 61.40% of nationwide lubricant consumption, anchored by dense vehicle fleets and clustered manufacturing assets. Proximity to ports ensures regular replenishment of imported finished lubricants and base oils, supporting the Myanmar lubricants market in these regions. Special Economic Zones, such as Thilawa, house automotive assembly, packaging, and chemical industries that demand diverse fluid portfolios. Coastal areas capitalize on maritime supply chains, importing bulk products from Singapore and Malaysia for local repackaging and distribution.

Northern states, notably Kachin and Shan, exhibit above-average growth as mining investments and Chinese trade links drive the deployment of heavy equipment. Border towns evolve into logistics nodes, requiring warehouse forklifts and standby generators, which adds lubricant volume. The Ayeyarwady Delta and Central Dry Zone are experiencing a rise in mechanized farming, which underpins demand for tractor engine oils and hydraulic fluids. Government electrification targets drive persistent generator oil consumption in villages awaiting grid connections, underscoring the rural relevance of the Myanmar lubricants market.

By 2031, aggregated demand outside Yangon and Mandalay could exceed 44.3 million liters, narrowing the regional imbalance. Planned refineries in Thanlyin and Dawei may shorten supply lines and foster domestic blending clusters near feedstock sources. Improved highway networks accelerate distributor reach, reducing stock-out risk in interior townships. Localized warehouse investments by major distributors enhance delivery reliability and product freshness, supporting brand differentiation. Geographic expansion thus underpins a more balanced growth path for the Myanmar lubricants market.

Competitive Landscape

The Myanmar Lubricants market is moderately concentrated. International majors—Shell, BP, TotalEnergies, and ExxonMobil—lean on exclusive agents for market access, focusing on premium automotive and industrial lines. Asian peers, such as Petronas, PTT, and Pertamina, leverage geographic proximity to supply bulk products via the Yangon and Thilawa terminals, thereby sustaining a steady presence. Strategic partnerships with equipment OEMs (original equipment manufacturers) and power-plant EPC (Engineering, Procurement, and Construction) contractors represent viable paths to secure captive volume streams in the Myanmar lubricants market.

Myanmar Lubricants Industry Leaders

BP p.l.c.

PT Pertamina Lubricants

Shell plc

TotalEnergies

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: Goodyear Tire & Rubber Company, in collaboration with Assurance Intl Limited, launched a new range of lubricant oils. This new product line, distributed in South Asia and Southeast Asia markets, including Myanmar, addresses the diverse lubricant oil needs of both commercial and passenger vehicles.

- December 2022: Puma Energy signed an agreement to sell its stake in Puma Energy Asia Sun (PEAS) in Myanmar, as well as its minority share in National Energy Puma Aviation Services (NEPAS), to a locally owned private company, amid a challenging and constantly evolving situation.

Myanmar Lubricants Market Report Scope

Any substance that is physically integrated to reduce friction between two or more moving surfaces is referred to as a lubricant. On metallic surfaces, lubricants aid in preventing material degradation, erosion, corrosion, and rust development. Lubricants are typically made up of 90% petroleum-based oil and various additives to give them desirable properties specific to a given purpose.

The Burmese lubricants market is segmented by product type and end-user industry. By product type, the market is segmented into engine oils, greases, hydraulic fluids, metalworking fluids, transmission and gear oils, and other product types (process oils, circulating oils, aviation oils, etc.). By end-user industry, the market is segmented into automotive, heavy equipment, metallurgy and metalworking, power generation, and other end-user industries (food and beverage, chemical manufacturing, textile, etc.). For each segment, market sizing and forecasts have been done on the basis of volume in liters.

| Engine Oils |

| Greases |

| Hydraulic Fluids |

| Metalworking Fluids |

| Transmission and Gear Oils |

| Other Product Types |

| Automotive |

| Heavy Equipment |

| Metallurgy and Metalworking |

| Power Generation |

| Other Industries |

| By Product Type | Engine Oils |

| Greases | |

| Hydraulic Fluids | |

| Metalworking Fluids | |

| Transmission and Gear Oils | |

| Other Product Types | |

| By End-user Industry | Automotive |

| Heavy Equipment | |

| Metallurgy and Metalworking | |

| Power Generation | |

| Other Industries |

Key Questions Answered in the Report

How large is the Myanmar lubricants market in 2026?

The Myanmar lubricants market size reached 103.2 million liters in 2026.

What CAGR is expected for lubricant demand in Myanmar through 2031?

Lubricant consumption is projected to grow at a 1.21% CAGR between 2026 and 2031.

Which product leads sales volumes?

Engine oils lead with 41.10% market share in 2025 and are expected to remain dominant.

Which end-use sector consumes the most lubricants?

Automotive applications account for 50.90% of total volume, driven by a growing commercial vehicle fleet.

What is the main growth opportunity outside automotive?

Power generation shows the fastest CAGR at 1.56% as diesel generators support grid expansion.

Page last updated on: