Smart Wine Cellar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

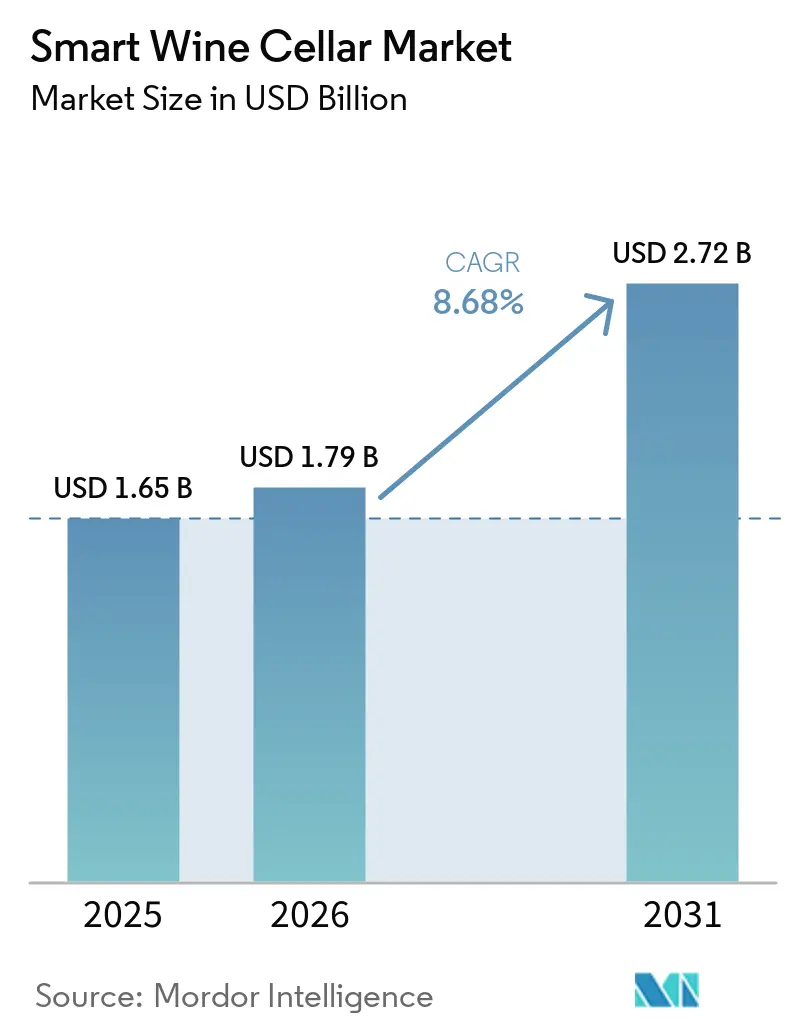

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 8.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Wine Cellar Market Analysis by Mordor Intelligence

The Smart Wine Cellar Market size was valued at USD 1.65 billion in 2025 and is estimated to grow from USD 1.79 billion in 2026 to reach USD 2.72 billion by 2031, at a CAGR of 8.68% during the forecast period (2026-2031). Robust growth is tied to connected-home adoption, hospitality modernization, and environmental regulations that push manufacturers toward low-GWP refrigerants and sensor-rich designs. Europe’s F-gas phase-down is accelerating product refresh cycles, while North American remodeling drives demand for freestanding units. Asia-Pacific consumption gains and emerging direct-to-consumer wine channels further widen the addressable base. Competitive intensity is moderate, with European premium specialists and North American mid-tier brands vying for share as appliance giants layer remote diagnostics and firmware updates onto their portfolios.

Key Report Takeaways

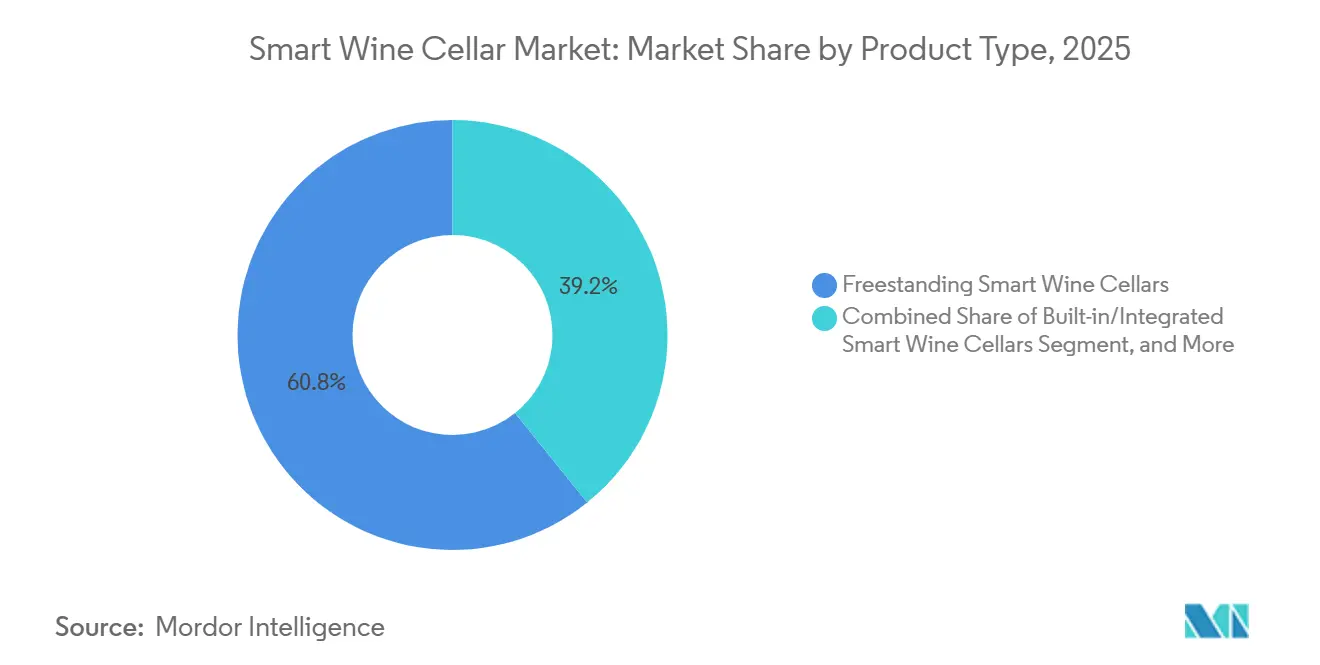

- By product type, freestanding smart wine cellars captured 60.77% of the Smart Wine Cellar market share in 2025, whereas commercial-grade walk-in smart cellars are forecast to expand at a 9.17% CAGR through 2031.

- By capacity, the 51-150 bottles segment accounted for 46.23% of the Smart Wine Cellar market size in 2025; the above-150-bottles category is projected to register a 9.76% CAGR on the back of emerging-market merchant demand.

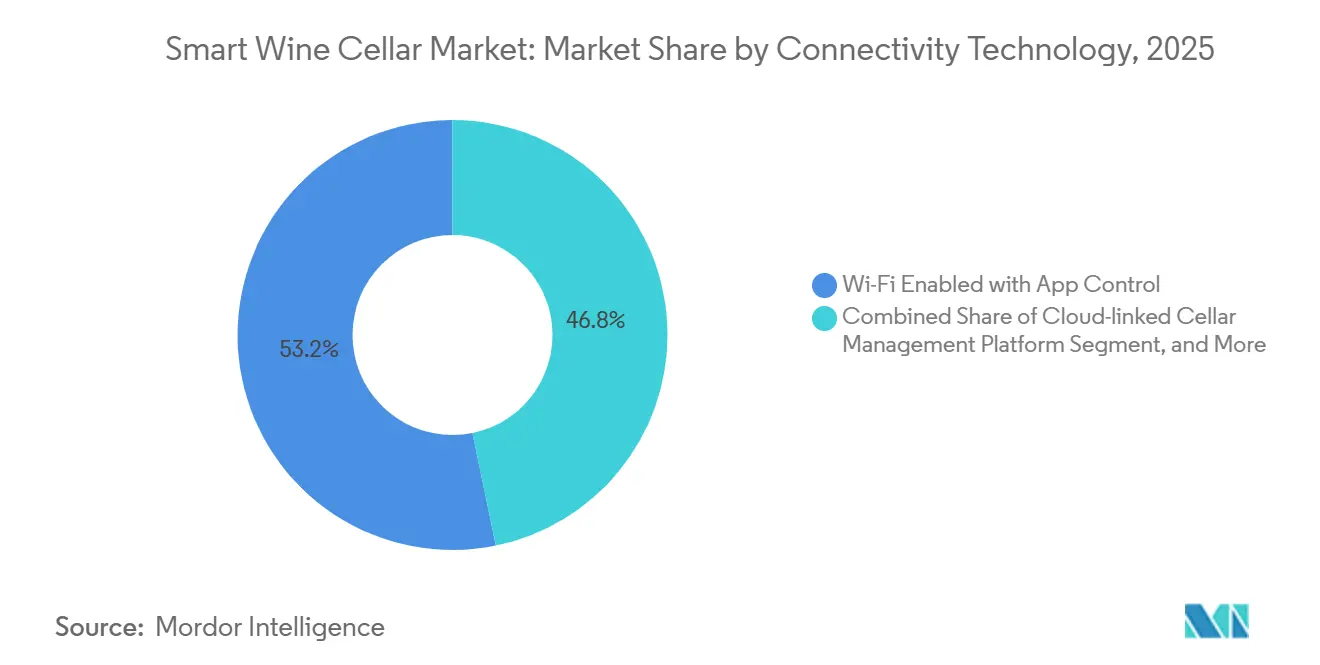

- By connectivity, Wi-Fi-enabled units with app control held 53.22% revenue share in 2025, while cloud-linked cellar-management platforms are expected to grow at 9.67% CAGR as multi-site hospitality operators centralize monitoring.

- By end-user, residential buyers accounted for 62.11% of 2025 revenue, yet the wineries and wine-merchant segment is set to grow at a 9.86% CAGR amid direct-to-consumer business models and vintage volatility.

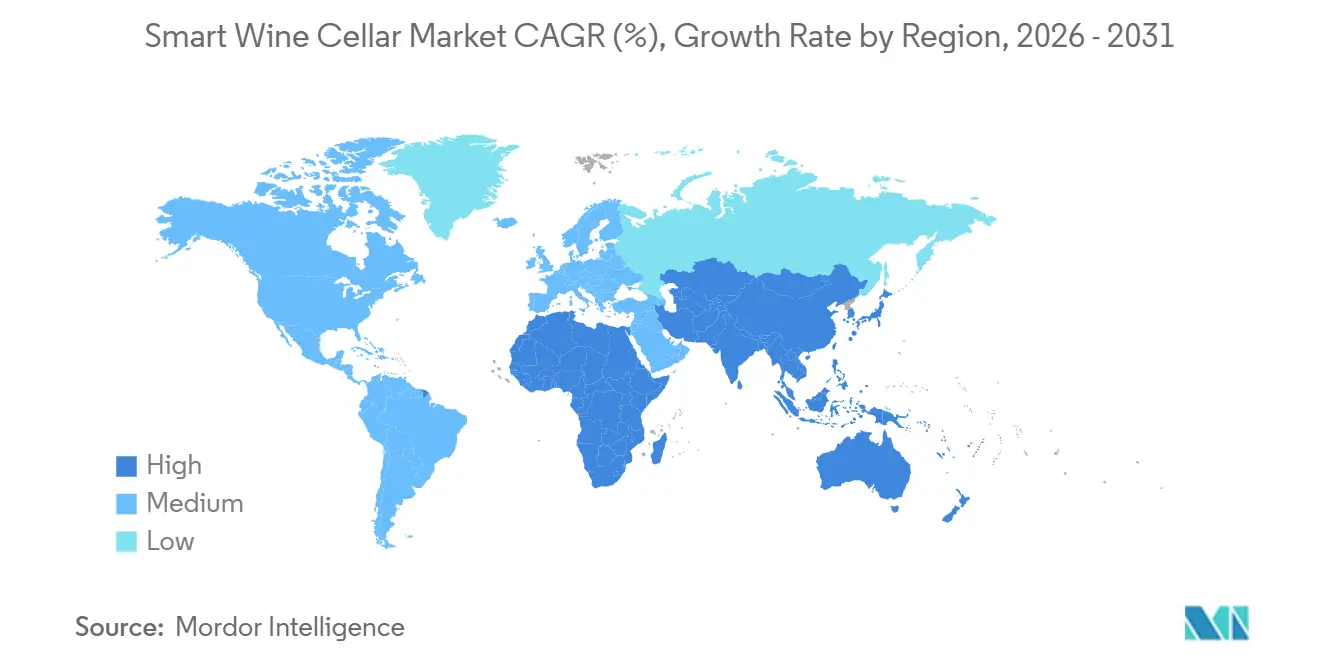

- By geography, North America led with 36.43% share in 2025, whereas Asia-Pacific is the fastest growing region at an 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Wine Cellar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected-Home Penetration Uplifting Premium Appliance Demand | +1.8% | Global, strongest in North America and Western Europe | Medium term(2-4 years) |

| Rising Wine Consumption in Emerging Economies | +1.5% | Asia-Pacific and South America | Long term(≥4 years) |

| Residential Remodels Featuring Dedicated Wine Rooms | +1.2% | North America and Europe | Medium term(2-4 years) |

| Hospitality Sector Upgrades to IoT-Enabled Storage | +1.4% | Global luxury hospitality hubs | Short term(≤2 years) |

| AI-Driven Flavor-Profiling Cellars for Collectors | +0.9% | Niche high-net-worth segments worldwide | Long term(≥4 years) |

| Carbon-Neutral Refrigeration Mandates Spurring Replacements | +1.6% | Europe and select U.S. states | Short term(≤2 years) |

| Source: Mordor Intelligence | |||

Connected-Home Penetration Uplifting Premium Appliance Demand

Smart-home ecosystems are shifting from individual gadgets to integrated platforms, positioning wine cellars as centerpiece appliances in open-concept kitchens. Voice-assistant compatibility, RFID tracking, and over-the-air updates raise average selling prices and shorten replacement cycles, especially as affluent homeowners seek unified dashboards across lighting, security, and refrigeration. Hospitality operators mirror this trend by embedding cellar data into property management systems, unlocking cross-sell opportunities for analytics-driven upselling.[1]Future Today Strategy Group, “2025 Tech Trend Report,” ftsg.com

Rising Wine Consumption in Emerging Economies

In 2024, global wine production reached a 60-year low, resulting in significant scarcity premiums across the market. Concurrently, urbanization and rising disposable incomes in countries such as China, Japan, India, Brazil, and Argentina are driving an increase in per-capita wine consumption. This growing demand for wine, coupled with limited supply, has created a challenging environment for merchants in these regions. To address these challenges, merchants are increasingly adopting advanced, climate-controlled storage solutions to preserve their scarce and valuable vintages. These systems are designed to maintain optimal storage conditions, ensuring the quality and longevity of the wine. Furthermore, the integration of cloud-managed technology in these storage solutions is enabling merchants to monitor and manage their inventory more efficiently. This trend is fueling the demand for high-capacity, technologically advanced storage systems, which are becoming essential tools in the wine supply chain.

Residential Remodels Featuring Dedicated Wine Rooms

Luxury homeowners often demand built-in or walk-in cellars equipped with advanced features such as humidity control, UV-filtered glass, and low-vibration compressors to preserve their wine collections under optimal conditions. These cellars are designed not only to maintain the quality of the wine but also to enhance the overall aesthetic appeal of the space. Premium brands, like Liebherr with its GrandCru Selection, cater to these high expectations by offering innovative features such as humidity alarms and dual sensors. These additions ensure precise environmental control while aligning with the sophisticated design and functional requirements of luxury living spaces.[2]Liebherr-Hausgeräte, “EWT 9275 Built-in Wine Fridge,” home.liebherr.com

Hospitality Sector Upgrades to IoT-Enabled Storage

Hotels and restaurants are increasingly adopting RFID and computer-vision systems to effectively monitor the origins of bottles and minimize spoilage, ensuring better inventory management and quality control. Additionally, open APIs facilitate the seamless integration of cellar data with loyalty programs, enabling businesses to provide hyper-personalized pairing recommendations. These tailored suggestions not only enhance the overall guest experience but also contribute to increased beverage sales by aligning offerings with customer preferences.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost vs. Conventional Coolers | -1.3% | Global, acute in emerging markets | Short term(≤2 years) |

| Limited Consumer Awareness Outside Connoisseur Niches | -0.9% | Asia-Pacific, South America, the Middle East, and Africa | Medium term(2-4 years) |

| Semiconductor Supply-Chain Volatility Hitting Smart Controllers | -0.7% | Export-dependent manufacturers worldwide | Short term(≤2 years) |

| E-Waste Regulations Increasing End-of-Life Compliance Costs | -0.5% | Europe, spillover to other regions | Medium term(2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Conventional Coolers

Smart cellar prices, influenced by the inclusion of advanced features such as sensor arrays, connectivity modules, and natural-refrigerant compressors, are 40-70% higher than basic units. This significant price difference restricts their adoption in price-sensitive markets, where affordability remains a key concern. On the other hand, entry-level thermoelectric models, priced under USD 300, compete aggressively by catering to cost-conscious consumers. In contrast, premium smart versions, such as Liebherr’s EWT 9275, are priced above USD 5,000, further widening the affordability gap and highlighting the stark contrast between basic and high-end offerings in the market.

Limited Consumer Awareness Outside Connoisseur Niches

In emerging markets, casual drinkers often lack awareness of optimal wine storage guidelines, which plays a significant role in limiting their willingness to invest in premium refrigeration solutions. This reluctance persists despite a noticeable increase in interest in wine consumption. Efforts to address this gap through educational outreach are underway, with digital influencers and winery partnerships leading the initiatives. However, these efforts are scaling at a gradual pace, which continues to delay the widespread adoption of proper storage practices among consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Walk-In Cellars Gain Commercial Traction

Freestanding units commanded 60.77% of the Smart Wine Cellar market share in 2025, favored for their retrofit flexibility in established homes and small hospitality venues. Mid-tier North American brands dominate these retail channels, offering dual-zone Wi-Fi models at USD 1,500-3,500 price points. Built-in appliances entice remodelers seeking seamless cabinetry integration, while appliance giants leverage cross-category bundling to upsell undercounter solutions. Commercial-grade walk-in smart cellars are projected to grow at a 9.17% CAGR to 2031 as wineries and restaurateurs scale RFID-enabled storage, underscoring a shift toward large, serviceable footprints.

Walk-in formats enable modular expansion, redundant cooling, and centralized monitoring, meeting the needs of merchants facing vintage scarcity and direct-to-consumer fulfillment. Multi-zone cabinets remain popular in Asia-Pacific’s space-constrained apartments, blending entertainment aesthetics with precise climate control. Competitive differentiation is migrating from compressor hardware to software, with cloud dashboards and predictive analytics defining the premium tier.

By Capacity: Large-Format Storage Accelerates for Merchants

The 51-150 bottles band represented 46.23% of Smart Wine Cellar market size in 2025, matching typical collector inventories and standard kitchen footprints. Units below 50 bottles struggle to justify the cost of advanced electronics, as thermoelectric coolers commoditize the market. Demand is tilting toward above-150-bottle systems, forecast to grow at a 9.76% CAGR, as merchants, hotels, and high-net-worth collectors seek scalable storage with dual sensors and cloud alerts.

Vintage volatility, underscored by a 13% drop versus the ten-year production average in 2024, drives merchants to bank inventory and monetize cellar services such as paid aging. Large-capacity models facilitate upsized racking, vibration isolation, and multi-temperature zoning, differentiating premium cellars from conventional refrigerators. This trend reflects a growing demand for advanced storage solutions in the wine industry.

By Connectivity and Technology: Cloud Platforms Enable Multi-Site Management

Wi-Fi-only units accounted for 53.22% of revenue in 2025, offering app-based temperature control without monthly fees. Retrofit sensors cater to owners of legacy cabinets but lack compressor integration. Commercial operators prefer cloud-linked platforms, projected to rise at 9.67% CAGR, featuring fleet dashboards, API hooks, and over-the-air diagnostics.

Machine-learning models, once confined to monitoring winery fermentation, are now guiding consumers in their cellars, detecting anomalies and suggesting optimal drink times. These advancements are enhancing the precision and efficiency of wine storage and consumption. In high-value hospitality venues, cellular or LoRaWAN backhaul introduces redundancy, bolstering subscription analytics and certifying provenance. The increasing adoption of IoT in refrigeration systems is driving this growth.

By End-User: Wineries Embrace Inventory Intelligence

Residential customers generated 62.11% of 2025 revenue, valuing design aesthetics and intuitive apps. Feature uptake centers on door-open alerts, humidity readouts, and voice-assistant commands. Commercial restaurants and hotels prioritize durability, service turnaround, and multi-user permissions, selecting walk-in or built-in units with cloud APIs. The growing adoption of smart technologies is driving innovation in both residential and commercial segments.

Wineries and merchants are the fastest-growing end-user cohort, with a 9.86% CAGR through 2031, leveraging smart cellars to safeguard scarce vintages and monetize storage-as-a-service models. Inventory visibility, blockchain provenance, and insurance-grade condition logs create high switching costs, anchoring long-term vendor relationships. This growth is further driven by increasing consumer demand for premium and rare wines.

Geography Analysis

North America held 36.43% share in 2025. U.S. per-capita consumption dipped, sharpening focus on quality preservation over volume and driving demand for multi-zone smart solutions. State-level HFC bans mirror European regulation, nudging suppliers toward propane and isobutane refrigerants. Canada and Mexico add incremental growth through wine tourism investments in British Columbia and Baja California. Europe remains a significant market thanks to entrenched wine culture and stringent environmental mandates.

Regulation (EU) 2024/573 enforces the use of low-GWP refrigerants, and WEEE obligations raise recycling costs, rewarding manufacturers with design-for-recycling expertise. Premium built-in categories flourish under brands such as EuroCave and Climadiff, while replacement demand accelerates ahead of 2027 GWP caps. Asia-Pacific is the fastest-growing region, with an 8.86% CAGR, driven by urban affluence and import growth. Consumers in Tokyo, Seoul, Shanghai, and Mumbai gravitate toward compact multi-zone cabinets that blend with limited living spaces.

Awareness campaigns and direct-to-consumer channels are gradually closing knowledge gaps, while wineries in Australia and India are adopting IoT-enabled cellars to differentiate tasting-room experiences. South America and the Middle East and Africa contribute smaller bases but exhibit rising hospitality investments. Argentina’s double-digit production rebound in 2024 and Brazil’s urban middle-class expansion propel demand for scalable walk-in storage, whereas Gulf hospitality megaprojects integrate presentation-grade cellars into luxury dining concepts.

Competitive Landscape

Market fragmentation is moderate. European specialists EuroCave, La Sommelière, Climadiff, and Artevino command brand loyalty in premium built-in niches. North American players Vinotemp, Wine Enthusiast, Allavino, and EdgeStar dominate the freestanding and e-commerce channels. Global appliance firms Liebherr and Dometic leverage manufacturing scale, energy-efficiency credentials, and broad dealer networks to cross-sell smart wine cellars with minibars and undercounter refrigeration.

The technology competition centers on connectivity, software ecosystems, and readiness for low-GWP technologies. Liebherr’s Vinidor line integrates dual-sensor redundancy and SmartDevice remote alerts; Dometic’s minibar portfolio meets ENERGY STAR Most Efficient benchmarks and fully transitioned away from high-GWP refrigerants in 2025.[3]Dometic Group AB, “Annual and Sustainability Report 2025,” dometicgroup.com Smaller brands face cost pressure from semiconductor volatility and compliance overhead, prompting interest from diversified appliance leaders in partnerships or acquisitions.

Software is the emerging battleground, with over-the-air firmware, fleet dashboards, and predictive maintenance shaping differentiation. AI-based flavor profiling and blockchain provenance offer future monetization streams, favoring vendors capable of bundling hardware with subscription analytics.

Smart Wine Cellar Industry Leaders

EuroCave SAS

Vinotemp International Corporation

La Sommelière International SAS

Artevino SAS

Wine Enthusiast Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Liebherr marked the first anniversary of the unveiling of Vinidor Selection multi-zone wine refrigerators with TempProtect Plus dual sensors, VibrateSafe low-vibration technology, and ENERGY STAR certification.

- February 2026: Liebherr launched fully integrated beverage refrigerators featuring SmartDeviceBox connectivity, PowerCooling with FreshAir filtration, and dual temperature drawers, targeting premium compact installations.

- January 2026: Dometic, a renowned player in the wine chiller sector, reported net sales of SEK 21.04 billion (USD 1.95 billion) for FY 2025 in its Q4 2025 interim report.

- January 2025: The U.S. Department of Energy finalized 2029 efficiency standards for commercial refrigeration cabinets, directly impacting wine cellar cooling units and requiring compliance by 2029 for new installations.

Global Smart Wine Cellar Market Report Scope

The smart wine cellar market represents an industry dedicated to advanced, technology-driven wine storage solutions. Utilizing IoT, sensors, and automation, these systems are designed to maintain wine quality while offering sophisticated management capabilities. Unlike traditional cellars, these innovative solutions provide precise control over temperature, humidity, and lighting. Additionally, they feature digital inventory management, mobile app integration, and AI-powered recommendations, delivering a highly efficient, modernized wine storage experience.

The Smart Wine Cellar Market Report is Segmented by Product Type (Freestanding Smart Wine Cellars, Built-In / Integrated Smart Wine Cellars, Commercial-Grade Walk-In Smart Cellars, and Multi-Zone Smart Cabinets), Capacity (Up to 50 Bottles, 51-150 Bottles, and Above 150 Bottles), Connectivity and Technology (Wi-Fi Enabled with App Control, Stand-Alone Smart Sensors and Controllers, and Cloud-Linked Cellar Management Platforms), End-User (Residential, Commercial Restaurants and Hospitality, and Wineries and Wine Merchants), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Freestanding Smart Wine Cellars |

| Built-In / Integrated Smart Wine Cellars |

| Commercial-Grade Walk-In Smart Cellars |

| Multi-Zone Smart Cabinets |

| Up to 50 Bottles |

| 51-150 Bottles |

| Above 150 Bottles |

| Wi-Fi Enabled with App Control |

| Stand-Alone Smart Sensors and Controllers |

| Cloud-Linked Cellar Management Platforms |

| Residential |

| Commercial, Restaurants and Hospitality |

| Wineries and Wine Merchants |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Product Type | Freestanding Smart Wine Cellars | ||

| Built-In / Integrated Smart Wine Cellars | |||

| Commercial-Grade Walk-In Smart Cellars | |||

| Multi-Zone Smart Cabinets | |||

| Capacity | Up to 50 Bottles | ||

| 51-150 Bottles | |||

| Above 150 Bottles | |||

| Connectivity / Technology | Wi-Fi Enabled with App Control | ||

| Stand-Alone Smart Sensors and Controllers | |||

| Cloud-Linked Cellar Management Platforms | |||

| End-User | Residential | ||

| Commercial, Restaurants and Hospitality | |||

| Wineries and Wine Merchants | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current Smart Wine Cellar market size and growth outlook?

The Smart Wine Cellar market size stood at USD 1.65 billion in 2025 and is projected to reach USD 2.72 billion by 2031,expanding at an 8.68% CAGR.

Which product type is leading sales?

Freestanding smart wine cellars led with 60.77% 2025 revenue, favored for retrofit flexibility in residential and hospitality spaces.

Which capacity range is growing fastest?

Units above 150 bottles are set for a 9.76% CAGR to 2031 as wineries and merchants scale climate-controlled storage.

How are regulations influencing product design?

Europe's F-gas Regulation (EU) 2024/573 and similar U.S. state rules force adoption of low-GWP refrigerants such as R290, prompting sensor-rich safety features and compressor redesigns.

What connectivity features are gaining traction?

Cloud-linked cellar-management platforms with fleet dashboards, API integration, and over-the-air updates are the fastest growing connectivity segment at 9.67% CAGR.

Who are the key players in the competitive landscape?

EuroCave, La Sommelière, Vinotemp, Wine Enthusiast, Liebherr, Dometic, and Allavino are leading manufacturers, with appliance giants leveraging scale and software to capture share.

Page last updated on: