Smart Railways Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

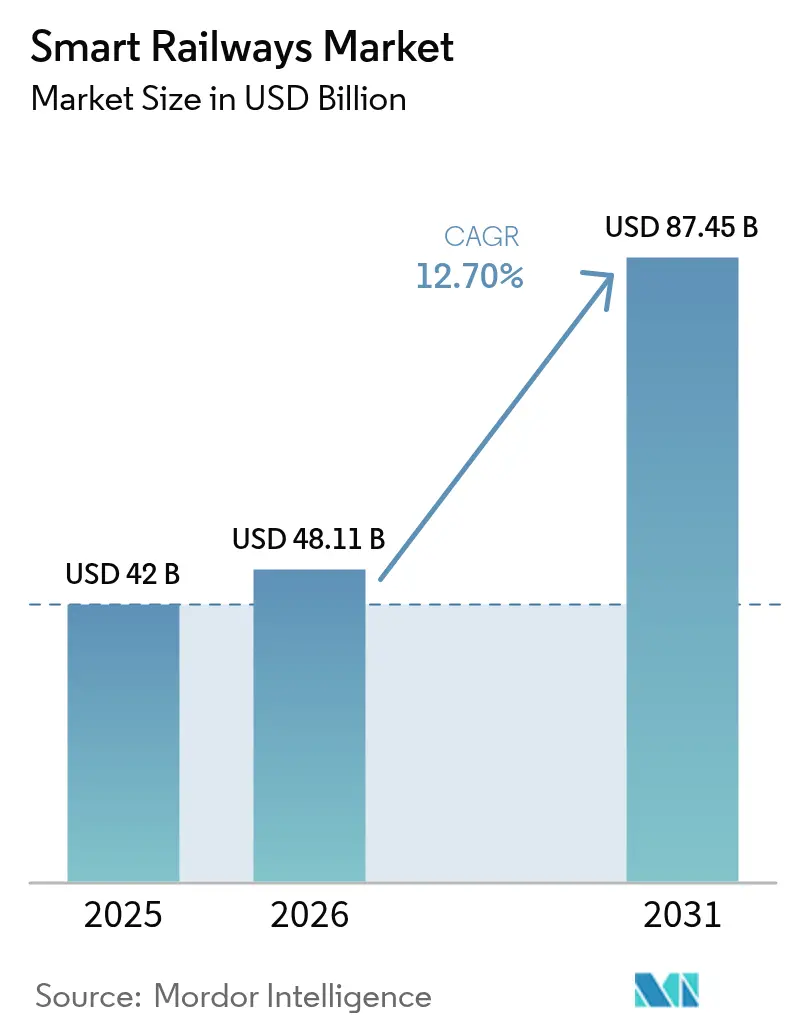

| Market Size (2026) | USD 48.11 Billion |

| Market Size (2031) | USD 87.45 Billion |

| Growth Rate (2026 - 2031) | 12.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Railways Market Analysis by Mordor Intelligence

The smart railways market size is projected to be USD 42 billion in 2025, USD 48.11 billion in 2026, and reach USD 87.45 billion by 2031, growing at a CAGR of 12.7% from 2026 to 2031. Growing commitments to net-zero transportation, large-scale 5 G rollouts, and multibillion-dollar European Rail Traffic Management System (ERTMS) grants are pushing rail operators to replace analogy signalling with digital-native platforms. Operators are prioritizing software-defined networking and predictive analytics that extend the life of existing rolling stock, reducing the need for costly new trains even as passenger demand rebounds. Procurement teams are shifting capital toward integrated turnkey projects because governments now tie financing to interoperable, open-architecture solutions rather than proprietary point products. The net effect is a market in which signalling upgrades, edge-AI hardware, and cloud-hosted traffic-management applications all expand in lockstep, creating scale economics that further accelerate adoption.

Key Report Takeaways

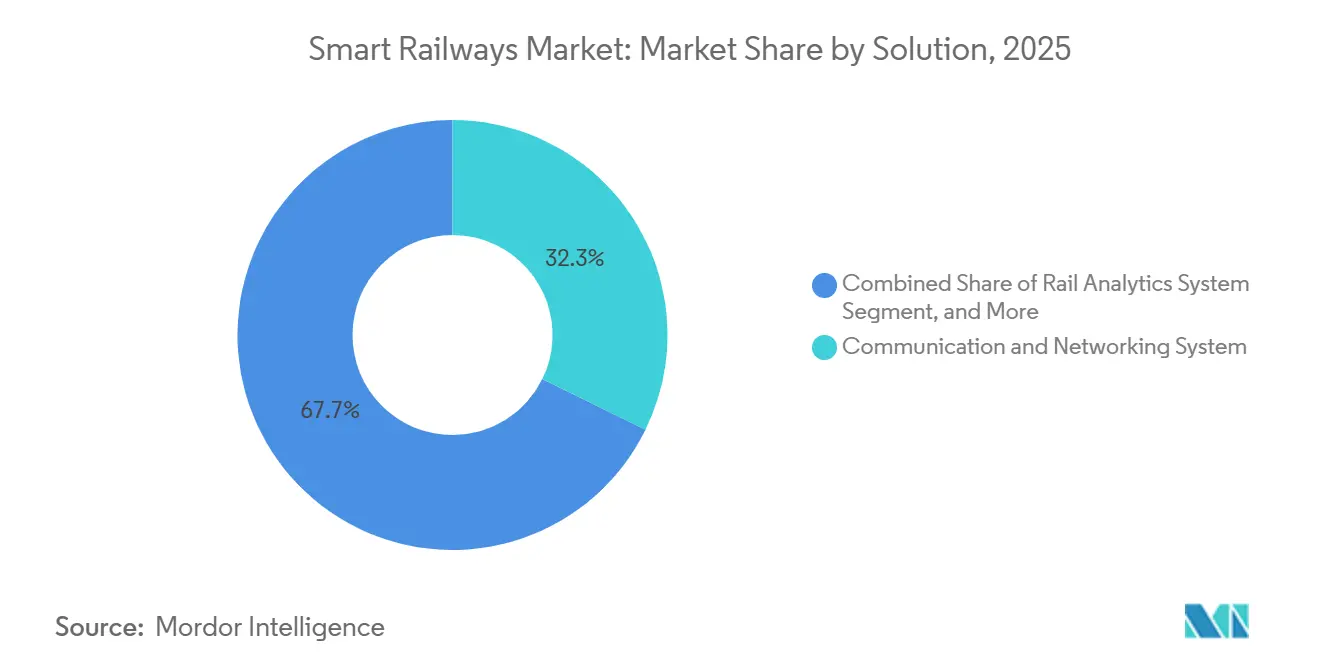

- By solution, Communication and Networking Systems held 32.27% of 2025 revenue while Rail Analytics Systems are expanding at a 13.8% CAGR through 2031.

- By rail type, Passenger Rail commanded 46.75% share of the smart railways market size in 2025, and High-Speed Rail is projected to advance at a 13.34% CAGR between 2026 and 2031.

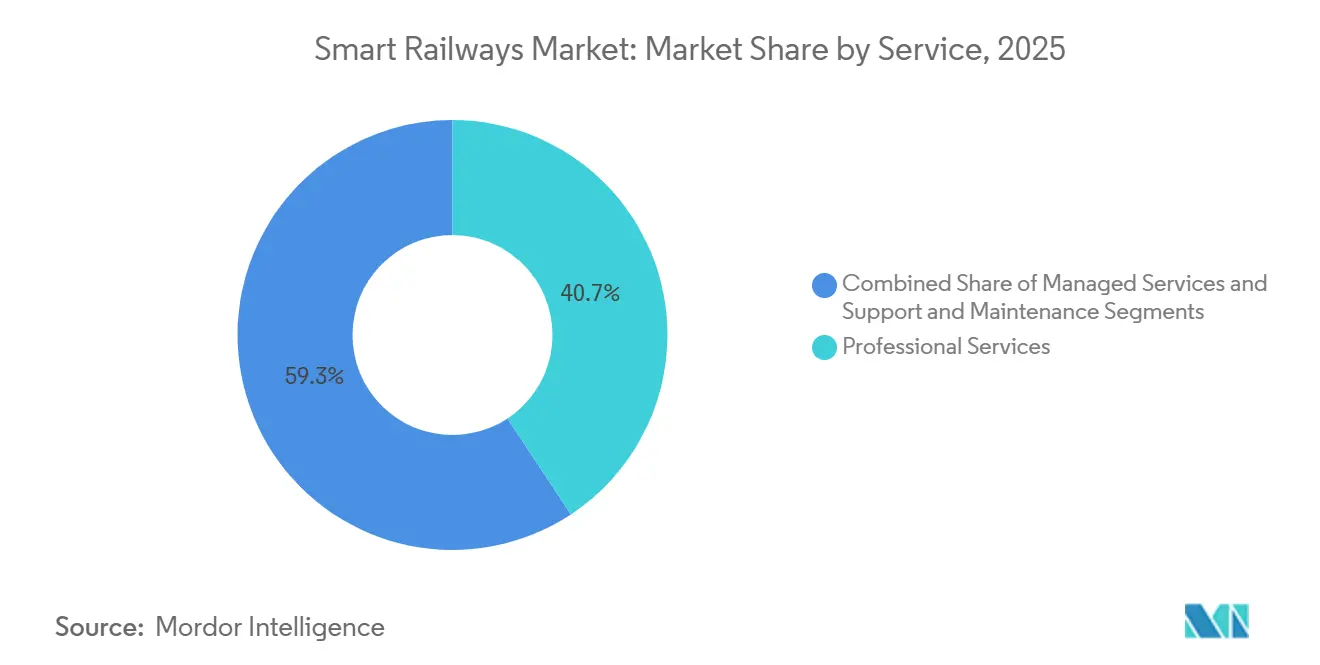

- By service, Professional Services captured 40.71% of revenue in 2025 whereas Managed Services exhibit the fastest growth at 13.23% CAGR through 2031.

- By deployment mode, Cloud led with 48.49% share in 2025, while Hybrid architectures are forecast to grow 13.45% annually to 2031.

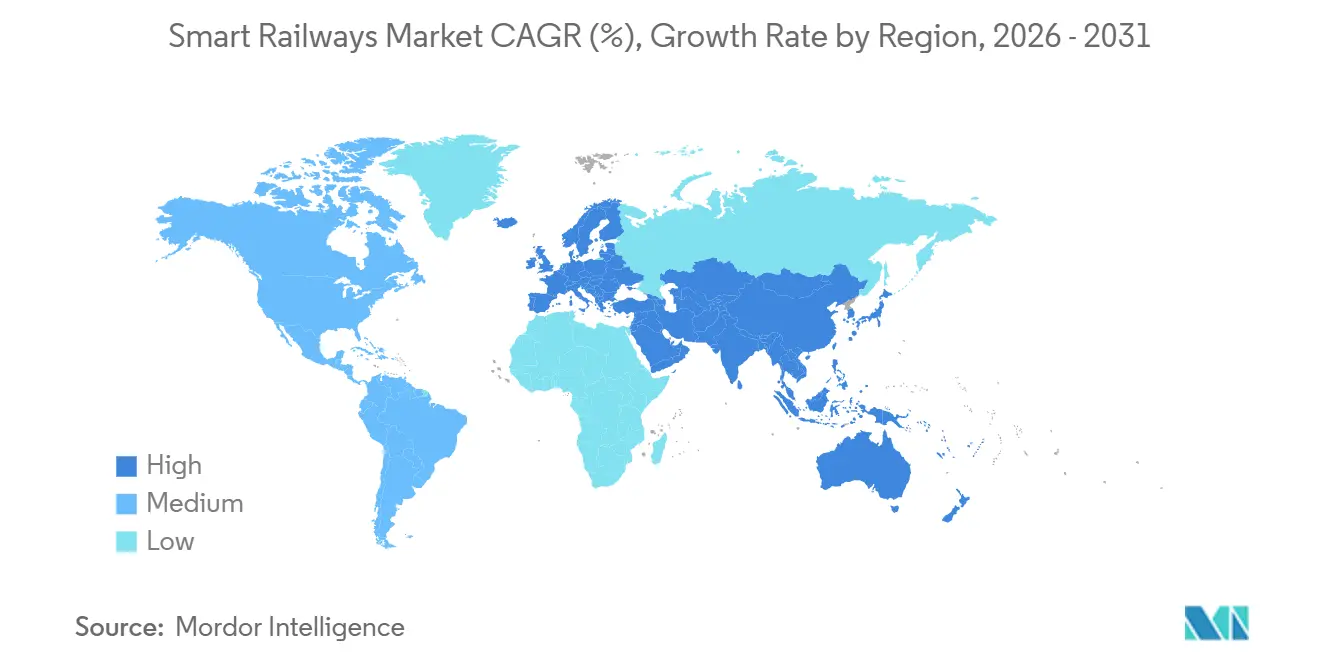

- By geography, Asia-Pacific accounted for 41.53% of smart railways market share in 2025 and the Middle East is the fastest-growing region at a 12.99% CAGR from 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Railways Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Smart-City and Net-Zero Mandates | +2.80% | Global, with concentration in EU, China, India | Medium term (2-4 years) |

| Rapid Roll-Out of FRMCS/5G Private Networks for Rail | +2.50% | Europe, Asia-Pacific core, early adoption in GCC | Short term (≤ 2 years) |

| Adoption of AI-Driven Predictive Maintenance Platforms | +2.20% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Growth in High-Speed Rail and Urban Transit Megaprojects | +2.00% | Asia-Pacific, Middle East, selective European corridors | Long term (≥ 4 years) |

| Cross-Border ERTMS and TEN-T Compliance Funding Surge | +1.60% | Europe, with spillover to North Africa and Turkey | Medium term (2-4 years) |

| DBaaS-Enabled MaaS Platforms Improving Passenger UX | +1.20% | Urban centers in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Smart-City and Net-Zero Mandates

National decarbonization rules are drawing rail budgets toward full route electrification and real-time energy dashboards that correlate traction load with timetable adherence, ensuring every kilowatt is traceable to a carbon target.[1]UK Department for Transport, “Rail Network Enhancements Pipeline,” gov.uk United Kingdom funding of GBP 3.2 billion (USD 4.13 billion) for the Trans-Pennine upgrade stipulates cloud-hosted energy management by 2027, pushing suppliers to bundle traction-power analytics with digital signalling. India now requires new rolling stock to demonstrate 30% energy savings compared with 2020 baselines, accelerating uptake of AI-driven driver advisory systems that dynamically adjust speed profiles.[2]Ministry of Railways, Government of India, “National Rail Plan and Kavach Deployment,” indianrailways.gov.in In Japan, disclosure of Scope 3 emissions has led JR East to install smart meters in 1,800 stations, integrating consumption data with its wholesale electricity trading desk. EU freight-mode-shift objectives, which aim for 30% of long-haul cargo to move by rail by 2030, stimulate automation investment in marshalling yards, reinforcing the business case for machine-vision-based wagon identification.[3]European Commission, “Connecting Europe Facility – Transport Sector,” ec.europa.eu

Rapid Roll-Out of FRMCS / 5 G Private Networks for Rail

Migration from GSM-R to Future Railway Mobile Communication System unlocks multigigabit capacity for high-definition CCTV, passenger Wi-Fi, and continuous train diagnostics. Deutsche Bahn’s Berlin–Munich pilot validated network slicing that keeps command-and-control traffic logically isolated, meeting EU safety-case expectations. China Railway’s standalone 5 G deployment across 8,000 route-kilometers by December 2025 positions Chinese integrators to export turnkey packages across Southeast Asia and Africa.[4]Ministry of Industry and Information Technology, China, “Railway 5 G Spectrum Allocation,” miit.gov.cn Meanwhile, Network Rail’s GBP 250 million (USD 322.5 million) FRMCS contract with Siemens Mobility surfaced latency spikes during handoffs, prompting hybrid GSM-R / FRMCS gateways that other EU operators are now replicating. Emerging revenue models let operators lease excess 5 G capacity to logistics firms located along the right-of-way, a non-fare income stream that strengthens project cash flows.

Adoption of AI-Driven Predictive Maintenance Platforms

Edge-AI chips that fuse vibration, current, and thermal telemetry are cutting unplanned locomotive downtime by double digits, making predictive analytics the fastest-growing smart railways market solution category. Hitachi Rail’s Lumada platform reduced Trenitalia faults 40% after ingesting 2 billion sensor records and correlating anomalies with track geometry. Wabtec’s reinforcement-learning Trip Optimizer is now mandatory on 3,500 BNSF freight locomotives, saving USD 150 million in annual fuel and lowering brake-shoe replacements 25%. Integration barriers still exist because many computerized maintenance management systems rely on SOAP rather than REST APIs; vendors buying middleware specialists, such as Siemens with its Sqills acquisition, solve this bottleneck.

Growth in High-Speed Rail and Urban Transit Megaprojects

Governments view high-speed corridors as strategic infrastructure that supports tourism and economic diversification, often accepting cost overruns private investors would reject. Saudi Arabia ordered 20 additional Avelia trainsets valued at USD 1.2 billion to lift Haramain High-Speed Railway capacity to 300 km/h. India’s under-construction 21 km under-sea tunnel on the Mumbai–Ahmedabad line requires continuous FRMCS coverage and seismic-resistant signalling, limiting bidders to large Japanese European consortia. Japan’s Chuo Shinkansen maglev demands sub-millimeter track-alignment monitoring, driving R&D partnerships on fiber-optic sensing. The common denominator across projects is a contractual requirement for digital twins that anticipate component fatigue before it threatens timetable integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy System Interoperability Bottlenecks | -1.40% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| High Upfront CAPEX for Digital Signalling Upgrades | -1.20% | Europe, North America, selective Asia-Pacific markets | Medium term (2-4 years) |

| Cyber-Security and Safety-Certification Complexity | -0.90% | Global, with stringent requirements in EU and Japan | Medium term (2-4 years) |

| Skilled-Labour Shortages for Rail-ICT Convergence | -0.70% | Europe, North America, Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy System Interoperability Bottlenecks

Mixed fleets equipped with multiple Automatic Train Control standards force suppliers to build custom gateways that inflate project budgets and complicate software patch management. SNCF’s need to lease 200 dual-mode locomotives during the ERTMS transition underscores how upgrade phasing can erode operational resilience. In North America, the USD 15 billion cost of integrating Positive Train Control with legacy block signalling still weighs on balance sheets, delaying new digital-overlay adoption. Each additional translation layer also expands the cyber-attack surface, making holistic modernization harder to justify.

High Upfront CAPEX for Digital Signalling Upgrades

Deutsche Bahn’s plan to digitize 12,000 route-kilometers carries an EUR 8.5 billion (USD 9.44 billion) price tag, forcing the operator to stage investments and accept fragmented benefits. Onboard ETCS equipment still costs EUR 150,000–200,000 per locomotive, a sum exceeding many wagons’ residual value, deterring private freight owners. Even software-defined interlocking needs years of safety-case preparation, as Alstom’s GBP 80 million (USD 103.2 million) Northern Line pilot showed, signalling that complexity, not silicon, is the primary cost driver.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Analytics Platforms Outpace Connectivity Investments

Rail Analytics Systems expanded its share of the smart railways market size by 13.8% CAGR because operators found immediate savings through component-life extension and inventory rationalization. Communication and Networking Systems still accounted for 32.27% revenue in 2025, boosted by FRMCS infrastructure, but growth is levelling as first-wave deployments finish. In freight corridors, asset-management suites combine historical failure logs with live sensor feeds, letting Canadian Pacific Kansas City trim locomotive downtime 18% after a continent-wide rollout. Smart ticketing converges with Mobility-as-a-Service, as Singapore riders now pay for integrated journeys with one digital wallet. Cyber-security solutions await final IEC 62443-4-2 guidelines, delaying contracts but setting the stage for an eventual spending surge.

Second-generation analytics add computer-vision defect detection and federated learning, features that process data on-device to comply with data-sovereignty mandates. Suppliers therefore bundle rugged edge gateways and cloud inference into one license, aligning with operators’ shift to outcome-based procurement. The smart railways market continues reallocating budgets from raw connectivity to higher-margin analytics that accelerate return on capital and unlock ancillary revenue such as predictive spares provisioning.

By Rail Type: High-Speed Corridors Drive Digitalization Intensity

Passenger Rail contributed 46.75% of 2025 revenue as city transit agencies funded Wi-Fi, video, and crowd-monitoring tools that shorten dwell times. High-Speed Rail, however, is projected to outgrow all other categories at 13.34% CAGR, scaling digital twins for superconducting magnets on Japan’s maglev and tilt-control algorithms on Spain’s 330 km/h services. Freight Rail lags, but Union Pacific’s GPS-beacon mandate is forcing leasing firms to embed telematics, opening the door for industrial-IoT newcomers.

Urban Transit systems embrace Communications-Based Train Control from day one, seen in Riyadh’s 90-second headways that exceed what conventional signalling supports. Light Rail projects in North America integrate traffic-signal priority through standardized APIs, demonstrating interagency cooperation once deemed impractical. Each sub-segment’s growth reflects how closely capital intensity aligns with the operational benefits digitalization unlocks.

By Service: Managed Services Gain as Operators Outsource Complexity

Professional Services held 40.71% of 2025 spending because ERTMS migration and safety-case documentation remain labour intensive. Managed Services display a 13.23% CAGR because operators want vendors to shoulder cyber-risk, uptime guarantees, and software patches. Alstom’s 15-year fixed-fee maintenance for hydrogen iLint fleets exemplifies outcome pricing that converts capital into predictable opex.

Operators with limited in-house IT, such as Queensland Rail, now hand entire radio networks to third parties, letting staff focus on timetable design. EU rules that require independent safety validation for every code change drive a consulting bottleneck, increasing day rates and reinforcing the managed-services case. As the smart railways market matures, suppliers weave analytics, hardware, and 24 / 7 monitoring into one service-level agreement.

By Deployment Mode: Hybrid Architectures Reconcile Latency and Sovereignty

Cloud captured 48.49% revenue in 2025 because passenger-facing apps benefit from elastic scale and global content delivery. Hybrid deployments grow 13.45% annually as CENELEC EN 50126 forces operators to keep fail-safe logs on premises. Hitachi Rail’s dual-plane design for Trenitalia splits safety traffic locally while analysing patterns in the cloud, minimizing latency without breaching sovereignty.

Freight carriers favour on-premises for dispatch systems after a 2024 hyperscaler outage stalled U.S. locomotive dashboards, prompting Norfolk Southern to repatriate workloads. Meanwhile, EU cybersecurity guidelines recommend EU-hosted data and quantum-resistant encryption, favouring regional clouds. Gateway vendors like Cisco now preprocess anomalies at the trackside, cutting bandwidth 70% for Indian Dedicated Freight corridors, underlining the hybrid model’s economic appeal.

Geography Analysis

Asia-Pacific accounts for over 41.5% of the smart railways market size due to China’s 45,000 km high-speed grid and India’s USD 130 billion modernization plan. Both nations mandate domestic content, compelling European and U.S. suppliers to form joint ventures, localize software, and transfer intellectual property. Japan’s maglev experiments create a halo effect, raising digital-twin expectations across the region.

The Middle East posts the fastest 12.99% CAGR through 2031. Saudi Arabia’s USD 22.5 billion Riyadh Metro Phase 2 and the UAE’s AI-refit of Dubai Metro prove governments will pay premium prices for turnkey reliability in harsh desert climates. Localization clauses drive global suppliers to set up GCC factories, accelerating technology diffusion and regional job growth.

Europe trails in growth but remains pivotal because Brussels finances cross-border ERTMS corridors. The EUR 1.6 billion (USD 1.78 billion) Connecting Europe Facility reduces risk for projects traversing Rhine-Alpine and Scandinavian-Mediterranean routes. However, fragmented national rules dilute scale economies, slowing adoption versus Asia.

North America focuses spending on freight efficiency, but USD 8.2 billion in U.S. intercity funding allows Amtrak’s 220 mph trainsets to integrate 5 G routers and ETCS Level 2. Canada and Mexico watch outcomes before committing to similar upgrades. South America’s investments center on mining railways, such as Vale’s autonomous iron-ore trains, which function as proofs of concept for passenger adaptation. Africa concentrates on North African high-speed builds like Morocco’s 320 km/h extension to Marrakech.

Regulatory Landscape

In Europe, interoperability and digital-data governance are tightening around harmonized specifications that directly shape smart-rail procurement. Commission Implementing Regulation (EU) 2026/253, adopted in February 2026 and brought into force with European Union Agency for Railways (ERA) implementation in March 2026, sets the Telematics Applications TSI and formalizes interoperable passenger and freight data sharing, including standardized data models (ERA Ontology) and cybersecurity expectations for rail data exchange.

Capacity and traffic-management rules are also pushing operators toward digital tools. Regulation (EU) 2026/1184, adopted in May 2026, targets infrastructure capacity management in the single European railway area and elevates the role of digital platforms for planning and traffic management, reinforcing demand for open-architecture traffic management, control-center software, and compliant integration services. In the United States, the Federal Railroad Administration (FRA) continues to guide rail technology through safety oversight and research pathways, including positive train control software-change processes and aligned applied research solicitations, keeping certification and compliance requirements central to deployments of connected and automated rail systems.

Competitive Landscape

Siemens, Alstom, Hitachi, Huawei, and Cisco controlled 52% of 2025 revenue, indicating moderate concentration. Siemens’ purchase of Sqills boosts software credentials, enabling bids that bundle equipment, data integration, and multi-year managed services. Alstom’s Saudi joint venture satisfies localization in Gulf Cooperation Council tenders, pre-empting Chinese challengers.

Edge-AI capability is the new battleground. Hitachi processed 2.3 billion sensor events for 14 European operators in 2025, transforming data lakes into actionable alerts. Thales leverages defense-grade cybersecurity to win contracts requiring quantum-safe encryption. Cisco’s Time-Sensitive Networking switches converge passenger Wi-Fi, CCTV, and signalling onto one IP backbone, attracting metros with space constraints.

White-space opportunities emerge in freight telematics where niche players like Advantech and Moxa supply rugged gateways immune to intermodal vibration extremes. Larger integrators focus on passenger comfort, leaving freight IoT an open arena. The competitive trend favours vendors offering entire digital twins across rolling stock and infrastructure, reducing multi-vendor risk for operators.

Smart Railways Industry Leaders

Alstom SA

Hitachi Ltd.

Wabtec Corporation

Bombardier Transportation Inc.

Indra Sistemas SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory convergence around interoperable data and standardized testing is creating whitespace for vendors that can package compliance into repeatable platforms. The EU Telematics TSI (Regulation (EU) 2026/253) consolidates passenger and freight telematics into one technical framework, supporting demand for packaged connectors, API management, and data-governance layers that translate legacy rail IT into NeTEx/SIRI-aligned exchanges and ERA Ontology-based semantics. At the same time, Commission Implementing Regulation (EU) 2026/693 adds updated test specifications for ETCS Baseline 4 and ATO Baseline 1, which supports accredited test tooling, simulation, verification services, and upgrade kits that reduce the burden of safety-case preparation during digital signalling migrations.

Rail communications modernization is also shifting from single-vendor roadmaps to multi-vendor integration, expanding demand for FRMCS-ready hardware, core-network software, and managed network operations that can coexist with legacy systems during transition. ETSI published TS 103 764 V1.1.1 in January 2026 to define the high-level FRMCS architecture, and the FRMCS introduction program has spotlighted lab integration and interoperability testing as a near-term focus for suppliers. Outside Europe, national digital backbones and unified control initiatives widen the market for analytics and integrated operations platforms, reflected in India Ministry of Railways issuing an RFI in July 2026 for a next-generation unified infrastructure engineering and traffic-control system (RIEC-NG) and launching Rail Bhoomi as a digital land-acquisition management platform tied into core railway systems, both of which reinforce demand for enterprise software integration, data platforms, and operational technology cybersecurity across rail assets.

Recent Industry Developments

- July 2026: Hitachi Rail completed the acquisition of Clever Devices, expanding its intelligent transportation systems footprint and strengthening its digital portfolio for fleet and asset management. The deal supports more end-to-end delivery across rail and adjacent transit modes by aligning operational data, passenger information, and control-center applications under broader platform offerings.

- June 2026: Alstom led a consortium that signed contracts worth EUR 690 million with Egyptian National Railways to modernise strategic corridors, including ETCS Level 1 signalling, telecommunications, and operations control capabilities. The scope shows how national corridor upgrades are being packaged as integrated digital programmes rather than isolated signalling replacements, favoring suppliers with turnkey delivery and local execution capacity.

- April 2026: Alstom commissioned the ARGOS computerised interlocking system at Montbard, France, in partnership with SNCF Reseau, designed to integrate with ERTMS-based speed control. Bringing a new-generation digital interlocking into service provides an in-field reference for software-centric signalling architectures and supports qualification pathways for similar deployments across ERTMS migration projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers digital and connected solutions used by rail operators and infrastructure managers to improve how rail networks run, stay safe, and serve passengers, including software, hardware, and related services that enable smarter operations.

Scope exclusions: Conventional rail rolling stock manufacturing, basic track construction, and non-digital civil works are excluded unless they are bundled with smart systems delivery.

Segmentation Overview

- By Solution

- Rail Analytics System

- Communication and Networking System

- Rail Asset Management and Maintenance

- Smart Ticketing and Revenue Management

- Cyber-Security and Safety

- By Rail Type

- Passenger Rail

- Freight Rail

- Urban Transit / Metro / LRT

- High-Speed Rail

- By Service

- Professional Services

- Managed Services

- Support and Maintenance

- By Deployment Mode

- On-Premise

- Cloud

- Hybrid

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by collecting consistent rail activity signals and public spending direction so the model has a realistic demand pool. We reviewed sources such as the International Union of Railways for network and traffic context, the European Union Agency for Railways for safety and interoperability indicators, and national transport statistics portals for ridership and freight trends.

We then used railway modernization plans, regulator and ministry publications, and investor presentations to map where spending is likely to concentrate, such as signaling upgrades, communications, and passenger-facing systems. For pricing and supply-side direction, we used public company filings and reputable press, and we also used a paid subscription focused on company financials and another on patent databases to validate solution maturity and investment themes. The sources listed here are illustrative only, and many other public documents were also referenced to fill gaps and validate assumptions.

Primary Interviews and Surveys

Primary discussions were used to check what is actually being deployed on active rail programs and how budgets are split between software, hardware, and services. We spoke with rail operators, system integrators, and component suppliers across the main regions so that regional rollout timing, procurement cycles, and typical contract scope could be normalized before final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 19% | APAC: 45% |

| Mid tier: 53% | Functional/Unit leaders: 22% | EMEA: 32% |

| Smaller Players: 20% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where national rail digitization budgets, priority corridors, and program pipelines are reconstructed into an addressable spend pool for smart solutions, and then allocated using observed mix splits by solution type and service intensity. To keep the totals realistic, we corroborate these outputs with selective bottom-up approximations, such as sampled contract values, typical system pricing ranges, and volume proxies tied to route-km, station counts, and fleet modernization activity.

Key inputs used in the model include passenger ridership recovery levels, rail freight ton-km trends, the pace of signaling and communications upgrades (including interoperability programs), cloud and cybersecurity adoption for rail operations, and average implementation and support cycle lengths. Where supplier-side checks leave gaps, the model uses conservative midpoint pricing bands and penetration ranges that were validated through interviews, before totals are finalized.

Forecasts are generated using scenario analysis supported by expert consensus on how quickly modernization projects move from planning to award to deployment. Assumptions are stress-tested for delays from funding shifts, tender timing, and integration constraints, and then rolled into the final year-by-year outlook.

Data Validation & Update Cycle

Outputs are checked against independent rail activity signals, procurement announcements, and public funding direction, and then compared across regions to ensure growth rates look plausible. When a variance appears, we revisit the underlying drivers, re-check conversion rates such as projects-to-awards, and re-contact sources if the gap affects the final totals.

A multi-step analyst review is followed so that calculation logic, unit consistency, and currency treatment are clean before sign-off. Reports are refreshed annually, with interim updates triggered by material events such as large program awards, major policy changes, or sharp macro shifts, and a final pre-delivery scan is done so clients receive the latest view.

Mordor Intelligence's Smart Railways Market Estimate Compared With Other Published Estimates

Published market sizes for smart railways often do not match because each study draws the market boundary differently and uses its own conversion logic from rail activity into spend. Differences also come from how services are treated, how quickly pricing is assumed to move, and whether the estimate is anchored to awarded projects or broader planned investment.

Program award values, tender pipelines, and rail digitalization budgets are the main evidence used to keep Mordor Intelligence's estimate aligned to what operators and infrastructure managers can reasonably procure within the year. Gaps usually show up when a source counts broader rail capex (or adjacent smart city spending), applies aggressive penetration without contract validation, or mixes constant currency with spot conversion.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 48.11 B (2026) | |

| Global Consultancy A | USD 36.49 B (2025) | Uses an earlier base year and a narrower spend capture that appears to emphasize solutions counted by offering, which can undercount multi-year services and lifecycle support that sit inside rail digital programs. |

| Industry Research Group B | USD 33.26 B (2025) | Applies a components-first framing with a different base year and forecast window, which can shift what gets counted in-year when projects are planned but not yet in deployment or revenue recognition stage. |

The table shows that the spread is mainly explained by base-year selection and what is treated as in-scope smart railway spend at the point of measurement. By tying the model to observable procurement signals and practical adoption ranges, the final numbers stay traceable to clear demand drivers and can be repeated with the same steps as new data comes in.

Key Questions Answered in the Report

How large will global spending on smart railways reach by 2031?

The smart railways market is forecast to reach USD 87.45 billion by 2031.

What is the projected CAGR for smart railway investments from 2026 to 2031?

Spending is expected to rise at a compound annual growth rate of 12.7% during the forecast period.

Which region leads current smart railway revenue?

Asia-Pacific generated 41.53% of global revenue in 2025 thanks to large Chinese and Indian programs.

Which rail type is growing fastest in digital adoption?

High-Speed Rail shows the highest momentum with a 13.34% CAGR to 2031.

Why are hybrid deployments gaining traction inside rail IT architectures?

Regulators require safety-critical logs to stay on-premise for reliability, while analytics workloads benefit from cloud elasticity, driving a hybrid split-plane approach.

Which service model is taking share from traditional professional services?

Managed Services are rising 13.23% annually as operators offload cyber-security and uptime guarantees to vendors.

Page last updated on: