Smart Home Security Camera Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

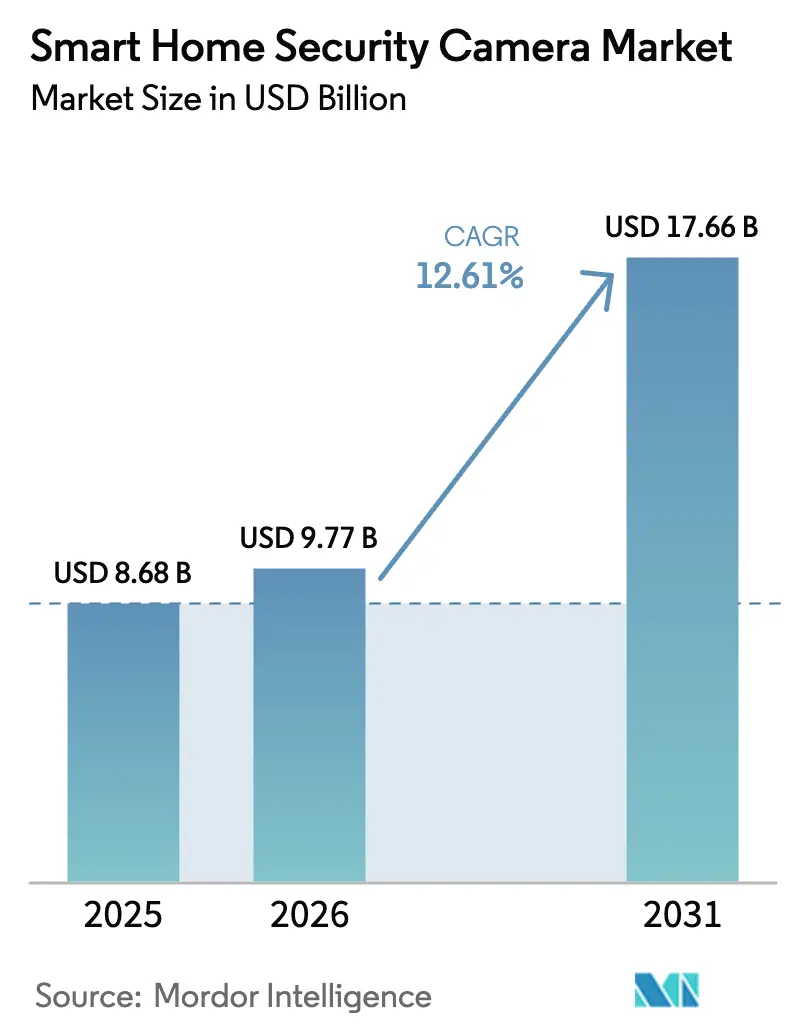

| Market Size (2026) | USD 9.77 Billion |

| Market Size (2031) | USD 17.66 Billion |

| Growth Rate (2026 - 2031) | 12.61% CAGR |

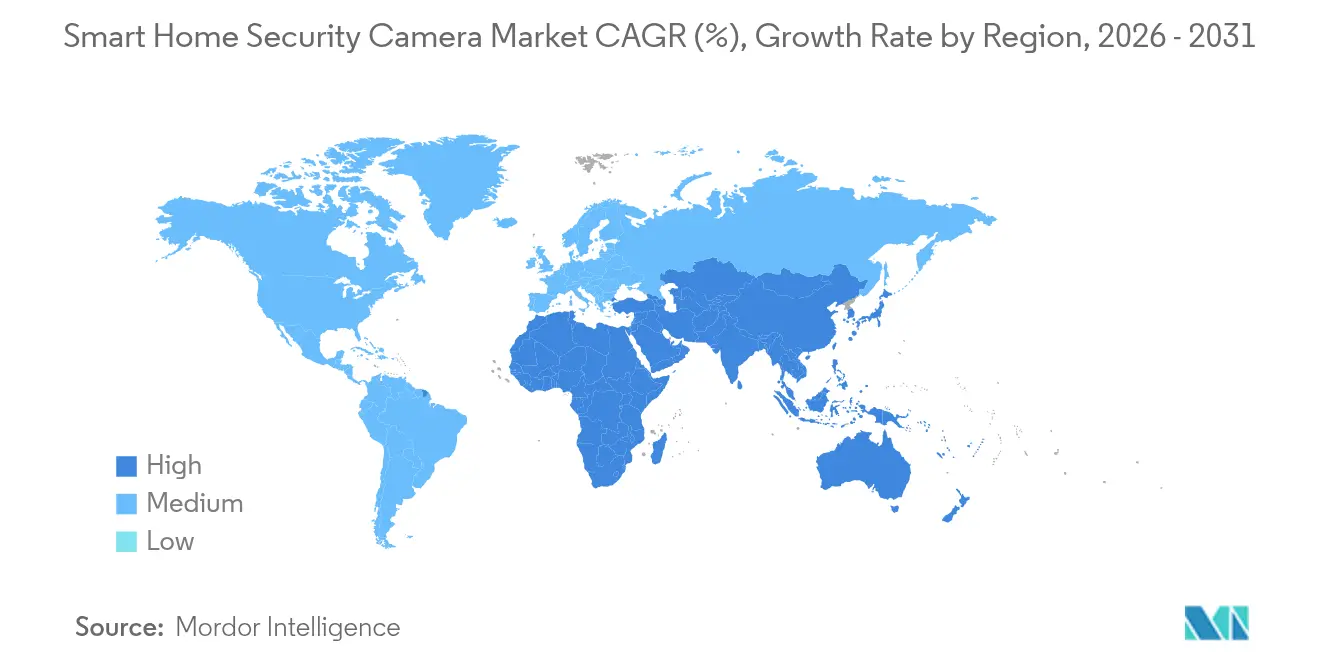

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Security Camera Market Analysis by Mordor Intelligence

smart home security camera market size in 2026 is estimated at USD 9.77 billion, growing from 2025 value of USD 8.68 billion with 2031 projections showing USD 17.66 billion, growing at 12.61% CAGR over 2026-2031. This momentum reflects rising household concerns about property crime, broader smart-home adoption, and rapid advances in artificial intelligence, edge processing, and cloud storage. Growing insurer discounts, expanding retrofit subsidies in Asia, and falling component costs are also broadening the customer base beyond early adopters. Established brands continue to invest in higher-resolution imaging and on-device analytics that cut bandwidth usage and lower false-alarm rates, while budget challengers focus on value pricing and firmware updates that add premium features. As a result, average selling prices are holding firm in North America and Western Europe even as unit volumes accelerate in Asia Pacific.

Key Report Takeaways

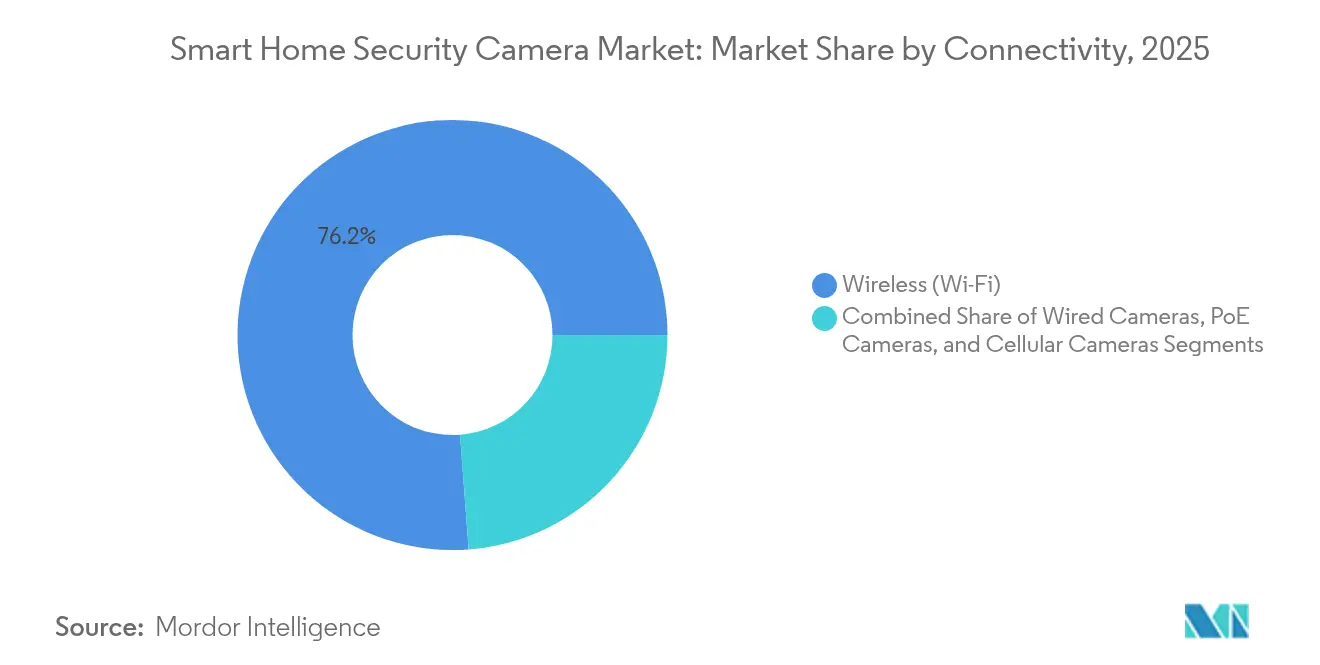

- By connectivity, wireless (Wi-Fi) units led with 76.20% revenue share in 2025, while cellular models are projected to expand at a 12.48% CAGR through 2031.

- By camera type, IP devices controlled 63.20% of the smart home security camera market share in 2025; PTZ IP cameras are on track for the fastest 13.85% CAGR to 2031.

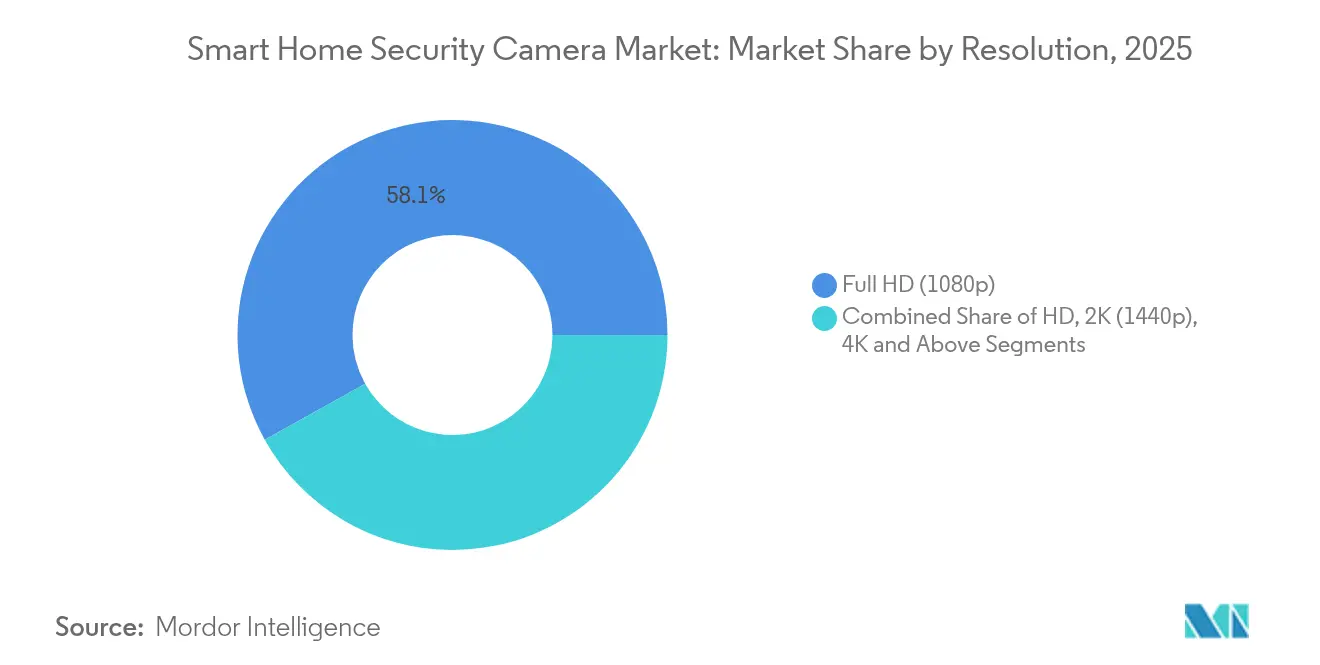

- By resolution, Full HD held 58.10% of the smart home security camera market size in 2025, yet 4 K and above resolutions are advancing at a 14.76% CAGR to 2031.

- By location, indoor products commanded 57.25% share of the smart home security camera market size in 2025, whereas outdoor units are set for a 13.18% CAGR during 2026-2031.

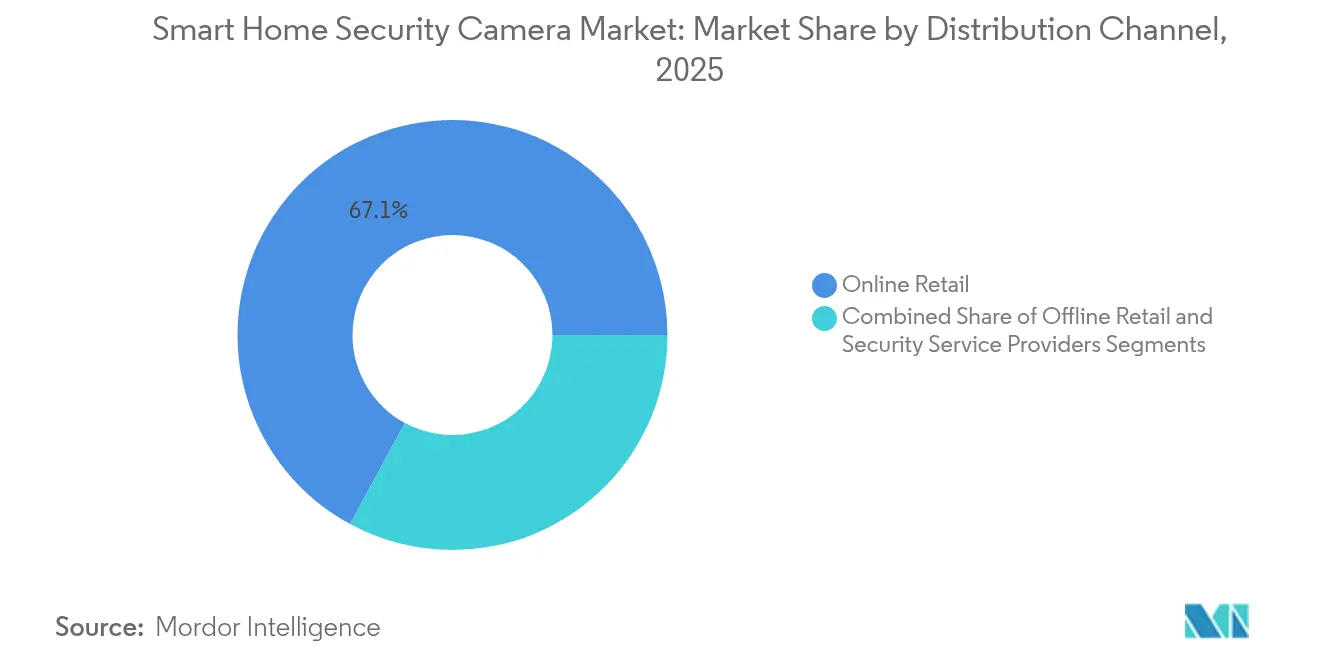

- By distribution channel, online retail accounted for 67.10% revenue in 2025, while security service providers are forecast to post a 12.92% CAGR to 2031.

- By geography, North America held 37.60% of global revenue in 2025; Asia Pacific is the fastest-growing territory with a 13.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Security Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled edge analytics driving premium upgrades | 2.50% | North America, Western Europe | Medium term (2-4 years) |

| Subscription “Camera-as-a-Service” models expanding | 2.10% | Europe, North America | Medium term (2-4 years) |

| Wireless doorbell adoption among urban renters | 1.80% | China, Japan, South Korea | Short term (≤2 years) |

| Smart-home insurance discounts accelerating installations | 1.70% | United States, United Kingdom | Medium term (2-4 years) |

| Japan’s “Digital Garden City” subsidies boosting retrofits | 1.50% | Japan | Short term (≤2 years) |

| Voice-assistant ecosystem integration lifting demand | 1.30% | Brazil, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-enabled Edge Analytics Driving Premium Upgrades in North America

Local processing has reduced outbound video traffic by 65%, trimming cloud fees and accelerating alert delivery. NVIDIA’s Jetson toolkit lets developers add person, vehicle, and pet recognition on entry-level boards.[1]NVIDIA Corporation, “Jetson Platform Services Documentation,” nvidia.com Retail data showed a 43% rise in subscription retention when edge AI was bundled with advanced alerts, supporting higher price points. U.S. insurers now certify models with local analytics for premium discounts, helping lift install counts in suburban markets. Western European adoption is following because on-device processing keeps footage within national borders. These dynamics raise the premium segment’s weight within the smart home security camera market and encourage continued R&D investment.

Subscription “Camera-as-a-Service” Models Expanding in Europe

Recurring bundles that merge hardware, cloud storage, and monitoring are reshaping revenue. Arlo’s Secure Plus plan at USD 17.99 per month for unlimited cameras is a leading example. European buyers are receptive because a single fee simplifies compliance with strict privacy laws that mandate timely firmware updates. Customer lifetime value climbs 3.2 times versus one-off hardware sales, while churn falls below 8% annually. Vendors gain predictable cash flow to offset hardware margin pressures and managed updates reduce vulnerabilities that regulators scrutinize. North American households are adopting similar tiers as insurance providers link policy discounts to active subscriptions.

Wireless Doorbell Adoption Among Urban Renters in Asia

Battery-powered doorbell cameras fit rental properties that prohibit drilling and permanent wiring. Demand is spiking in dense Japanese and South Korean cities where rentals dominate housing stock. Independent testing found Ring and Blink models well-suited to apartment doorframes thanks to slim mounts and extended battery life. Landlords appreciate non-destructive fixtures that reduce turnover costs, while tenants value portability when relocating. Unit shipment data indicates the doorbell subsegment outpaced the overall smart home security camera market by 7 percentage points during 2024-2025. Manufacturers are responding with bundled chimes, multilingual apps, and quick-release batteries to serve this fast-rotating customer base.

Smart-Home Insurance Discounts Accelerating Installations in US/UK

Property insurers now offer 5-20% premium reductions for homes protected by connected cameras. An ADT program delivered average annual savings of USD 233 for monitored households. Insurers also require firmware patch compliance, which lifts subscription retention 27% because homeowners keep monitoring active to maintain discounts. Vendors design models to meet insurer certification, while policy bundles shorten payback periods for consumers. The financial incentive is strongest in high-theft postal codes, driving above-average unit growth in Chicago, London, and Manchester.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented privacy regulations increasing compliance costs | -1.80% | EU, China, California | Long term (≥4 years) |

| Firmware vulnerabilities in low-cost OEMs eroding trust | -1.50% | European Union | Medium term (2-4 years) |

| Limited 5 GHz spectrum in multi-dwelling units | -1.20% | Global urban centers | Medium term (2-4 years) |

| Price wars on e-commerce platforms compressing margins | -1.00% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented Privacy Regulations Increasing Compliance Costs

The EU’s GDPR, California’s CCPA, and China’s PIPL each impose different consent, retention, and facial recognition rules. Engineering teams must build region-specific firmware, adding 23% to global R&D budgets. Compliance drains resources from product innovation, especially at start-ups where legal spending now consumes 18% of operating expenses. Rollout delays are common because certification testing differs by jurisdiction, slowing global launches and reducing scale benefits.

Firmware Vulnerabilities in Low-Cost OEMs Eroding EU Trust

An 83% jump in reported breaches between 2023 and 2024 dented consumer confidence.[2]Consumer Protection, “How To Secure Your Home Security Cameras,” Federal Trade Commission, consumer.ftc.gov Weak encryption and default passwords allowed intrusions that regulators flagged as avoidable. European buyers now pay a 37% premium for brands with proven security track records. Value-tier vendors face restricted addressable markets unless they certify devices under schemes such as Singapore’s Cybersecurity Labelling System.[3]Cyber Security Agency of Singapore, “About Cybersecurity Labelling Scheme for IoT,” csa.gov.sg The shift stratifies the channel and narrows margins at the low end of the smart home security camera market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity: Cellular Options Gaining Ground

Wireless (Wi-Fi) cameras still account for 76.20% of 2025 revenue, but cellular units are rising fastest at a 12.48% CAGR. Outage resilience attracts rural homeowners and owners of second properties who lack stable broadband. Falling IoT data pricing has closed the cost gap with Wi-Fi systems by 42% since 2023. The smart home security camera market size for cellular devices is projected to reach USD 3.42 billion by 2031. Vendors add dual-mode connectivity that switches to LTE when routers fail, raising perceived reliability. PoE cameras keep their niche in high-value installations where a single cable supports both power and data. Hybrid solutions combining Wi-Fi, LTE, and local storage continue to gain mindshare with professional integrators seeking fail-safe architectures.

In parallel, operators bundle SIM plans with hardware, creating a service annuity similar to smartphone models. Regulatory hurdles for indoor cellular transmitters have eased in North America, encouraging wider adoption. Asia Pacific shows early interest because 5 G coverage in suburban Japan and South Korea outpaces fiber deployment. Competitive differentiation now centers on data-usage optimization and seamless roaming across carrier networks. As the technology matures, a broader software ecosystem will emerge around firmware-based network health analytics, boosting uptime and supporting predictive maintenance.

By Camera Type: PTZ Flexibility Drives Premium Growth

IP cameras dominated with a 63.20% share in 2025, displacing analog almost entirely in new residential installs. PTZ models captured mindshare by lowering price premiums to 30% over fixed units. The smart home security camera market size for PTZ devices will expand at a double-digit CAGR, lifted by pan-tilt motors rated for –20 °C operation and tighter integration with AI-based auto-tracking. Homeowners value remote repositioning that maximizes coverage with fewer devices, saving wiring and subscription fees. Fixed IP units retain the volume lead by offering dependable coverage at entry prices below USD 40.

360° fisheye lenses are carving out niches in open-plan interiors by delivering complete room visibility. Innovation continues around modular designs that let buyers attach floodlights, sirens, and even smart-speaker bases to the camera chassis. This modularity extends replacement cycles because accessories can be swapped without discarding the core sensor block. In the higher tier, PTZ platforms now support presets that automatically reposition when a courier approaches, integrating with package-drop detection to reduce porch theft.

By Resolution: 4K Adoption Accelerates

Full HD remained the mainstream resolution at 58.10% share in 2025, yet 4K units are forecast to grow at 14.76% CAGR. The smart home security camera market share for 4K products reached 21.37% in 2025, reflecting sharper facial recognition and license-plate capture. H.265+ compression lessens storage penalties, halving bandwidth relative to earlier codecs. Cloud plans are evolving: footage is stored in full resolution only for motion events classified as important by on-device AI. Manufacturers such as Reolink have introduced dual-sensor designs that combine a wide-angle 4K lens with a telephoto module for crisp zoom without interpolation.

2K cameras satisfy cost-sensitive buyers who want crisper images than 1080p without paying the 4K premium. In emerging markets, 720p is slipping to a single-digit share as resale pricing pressures quicken. Suppliers are integrating adaptive streaming that downgrades quality when mobile bandwidth constrains viewing, ensuring consistent live-view performance for smartphones on public networks. The move toward higher resolution also drives demand for smarter search tools, including thumbnail scrubbing and text-based scene queries.

By Location: Outdoor Segment Accelerates

Indoor models contributed 57.25% of 2025 volume because renters prefer quick placement on shelves and desktops. Outdoor cameras are growing faster at 13.18% CAGR, fueled by ruggedized enclosures, IP66 waterproof ratings, and integrated floodlights. Solar-powered versions eliminate battery swaps; Reolink recorded 127% year-over-year growth for its solar line. Mount systems now pivot between soffit, wall, and pole to suit the varied architecture. Night-vision quality is improved with dual infrared and white-light LEDs that deter intruders while preserving image detail for identification.

The smart home security camera market size for outdoor units is expected to match indoor volume by 2028 as homeowners prioritize perimeter detection. Floodlight cameras command a 35% price premium yet sell briskly because one device replaces separate lighting and surveillance gear. Vendors bundle voice warnings in multiple languages that play when motion exceeds risk thresholds, aligning with global deployment. Multifunctionality is becoming a baseline requirement, blurring lines between camera, intercom, and security lighting.

By Distribution Channel: Service Providers Leverage Installation Expertise

Online marketplaces captured 67.10% of 2025 revenue as shoppers valued price transparency and quick shipping. Security service providers, however, are tracking a 12.92% CAGR because they solve installation complexity. They tailor layouts, drill cable holes where needed, and configure networking for homeowners who lack technical confidence. The smart home security camera market size routed through professional channels will top USD 4.38 billion by 2031. Providers also sell maintenance contracts that guarantee firmware updates, mitigating breach risk.

Retail showrooms are evolving into experiential hubs that present live demos in staged living rooms. Shoppers compare field-of-view differences and voice assistant integration before purchasing, which raises attachment rates for accessories such as solar panels and microSD cards. Hybrid purchase journeys are common: consumers research online, configure systems with virtual advisors, and schedule in-person setups. This omnichannel approach lifts average order value, especially for packages exceeding four cameras. Financing plans with zero-interest terms further remove adoption barriers for premium bundles.

Geography Analysis

North America retained the largest share at 37.60% in 2025, buoyed by strong disposable income and insurance programs that subsidize hardware. United States buyers have shifted toward AI-centric devices, with 63% of new installs supporting person recognition. Canadian demand mirrors U.S. trends, albeit at a smaller absolute scale, while Mexico shows rapid growth in metropolitan areas where property-crime rates exceed rural levels. The region’s regulatory environment encourages cloud services, yet privacy-minded consumers increasingly prefer edge analytics to limit external data transfer.

Asia Pacific posted the fastest growth at a projected 13.96% CAGR for 2026-2031. China leads unit volume as domestic manufacturers drive aggressive price competition and execute nationwide e-commerce campaigns around shopping festivals. Japan benefits from the “Digital Garden City” program, which subsidizes up to 40% of retrofit costs for qualifying households. South Korea is advancing integrated smart-home platforms where cameras auto-trigger lighting scenes and alarm systems. India’s penetration remains below 7% of potential households, yet power-backup features and regional language apps are accelerating uptake. Southeast Asian markets like Indonesia and Thailand are in earlier stages but benefit from improving broadband reach.

Europe accounted for 27.85% of 2025 revenue but displays wide intra-regional variance. The United Kingdom leads in absolute sales, helped by familiarity with CCTV culture and attractive insurer rebates. Germany and France follow, though buyers demand subscription flexibility and local storage to satisfy GDPR constraints. Nordic countries exhibit the highest per-capita penetration, driven by early smart-home adoption and security needs for remote vacation cabins. Southern Europe is in catch-up mode as economic recovery lifts discretionary spending; vacation-home owners in Spain and Portugal favor battery-powered outdoor units with solar panels to safeguard unoccupied properties.

Competitive Landscape

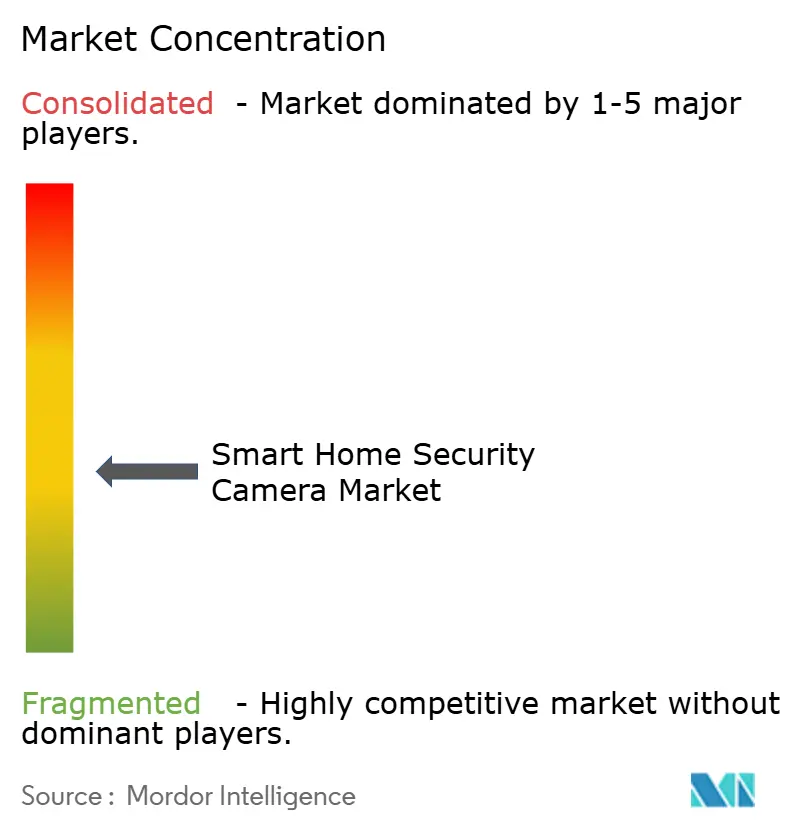

The market remains moderately fragmented: the top five vendors hold roughly 47% combined revenue share. Amazon Ring maintains its lead in North America through tight Alexa integration and an expansive device portfolio that shares a single app. Google Nest remains strong among Android households and leverages Google’s AI to keep false alerts low. Hikvision dominates in China and parts of Europe, where distributors prize its breadth of form factors and competitive pricing. WYZE undercuts rivals on hardware cost while backfilling premium features through firmware updates, prompting incumbents to keep entry prices in check.

Artificial intelligence is the central battleground. Vendors stress the ability to recognize packages, pets, and vehicles while storing video only when a risk event occurs. Edge computing is added to mid-range lines to meet European privacy demands and to reduce cloud fees that erode margins. At the same time, the subscription race is intensifying. Players such as Arlo and Deep Sentinel monetize live monitoring services, while hardware-centric brands experiment with freemium tiers to funnel users toward premium storage plans.

Strategic partnerships signal consolidation of ecosystem play. Arlo aligned with ADT to blend DIY cameras with professional monitoring. TP-Link adopted Matter to ease cross-brand compatibility, opening doors to Apple and Samsung hubs. Hikvision protects channel share by offering integrators white-label apps in local languages, locking in service revenues. Venture funding remains available for specialists focusing on privacy-first designs and energy harvesting, as seen in SimpliSafe’s USD 130 million raise to speed up European expansion.

Smart Home Security Camera Industry Leaders

Hangzhou Hikvision Digital Technology Co. Ltd

FrontPoint Security Solutions Inc.

Honeywell International, Inc.

SimpliSafe, Inc.

ADT Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Google Nest launched an outdoor model that identifies people, packages, vehicles, and animals with 98.5% accuracy, cutting false alerts by 65%.

- April 2025: Amazon Ring released a pan-tilt indoor camera featuring 360° coverage and a physical shutter for privacy.

- March 2025: Arlo and ADT partnered to combine Arlo devices with ADT professional monitoring.

- February 2025: Hikvision introduced AcuSense 2.0, enhancing AI filters to ignore animals and moving foliage.

Global Smart Home Security Camera Market Report Scope

Smart home security cameras are sophisticated surveillance devices that seamlessly integrate with home automation systems, delivering superior monitoring and security capabilities. This integration allows users to access live feeds, receive timely notifications, and regularly store recorded footage. The overall protection is significantly bolstered by adding smart cameras to home security setups.

The study monitors global revenues generated from sales of smart home security camera products. It also examines key market metrics, growth drivers, and leading industry vendors, bolstering market estimates and projections. Additionally, the analysis delves into the macroeconomic influences on the market. The report covers market sizing and forecasts across different segments.

The smart home security camera market is segmented by type (analog camera and IP camera [PTZ cameras]), resolution (HD and full HD), location (indoor and outdoor), shape (bullet, dome, pan, and other shapes), and by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Wired Cameras |

| Wireless (Wi-Fi) Cameras |

| Power-over-Ethernet (PoE) Cameras |

| Cellular (4G/5G) Cameras |

| Analog Cameras | |

| IP Cameras | Fixed IP Cameras |

| PTZ IP Cameras | |

| 360°/Fisheye IP Cameras |

| HD (=720p) |

| Full HD (1080p) |

| 2K (1440p) |

| 4K and Above |

| Indoor Cameras |

| Outdoor Cameras |

| Online Retail |

| Offline Retail (Electronics and DIY Stores) |

| Security Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Gulf Cooperation Council Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Connectivity | Wired Cameras | |

| Wireless (Wi-Fi) Cameras | ||

| Power-over-Ethernet (PoE) Cameras | ||

| Cellular (4G/5G) Cameras | ||

| By Camera Type | Analog Cameras | |

| IP Cameras | Fixed IP Cameras | |

| PTZ IP Cameras | ||

| 360°/Fisheye IP Cameras | ||

| By Resolution | HD (=720p) | |

| Full HD (1080p) | ||

| 2K (1440p) | ||

| 4K and Above | ||

| By Location | Indoor Cameras | |

| Outdoor Cameras | ||

| By Distribution Channel | Online Retail | |

| Offline Retail (Electronics and DIY Stores) | ||

| Security Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Gulf Cooperation Council Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the smart home security camera market?

The smart home security camera market size is USD 9.77 billion in 2026 and is forecast to grow to USD 17.66 billion by 2031.

Which region is growing fastest for smart home cameras?

Asia Pacific is the fastest-expanding geography, with a projected 13.96% CAGR from 2026 to 2031 due to urbanization, rising incomes, and supportive government programs.

What connectivity option is gaining traction beyond Wi-Fi?

Cellular (4 G/5 G) cameras are emerging quickly, posting a 12.48% CAGR because they operate during broadband outages and suit rural or secondary properties.

How are insurers influencing adoption in North America?

U.S. and U.K. insurers give 5-20% premium discounts for homes with connected cameras, effectively shortening payback periods and boosting installation rates.

Why is edge analytics important?

Processing video on device cuts bandwidth and speeds alerts, while satisfying privacy rules that restrict cloud uploads, thereby driving premium upgrades in North America and Western Europe.

What trend is shaping European purchasing behavior?

Subscription “Camera-as-a-Service” bundles that include hardware, storage, and monitoring are popular, raising customer lifetime value and reducing churn.

Page last updated on: