Mirrorless Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

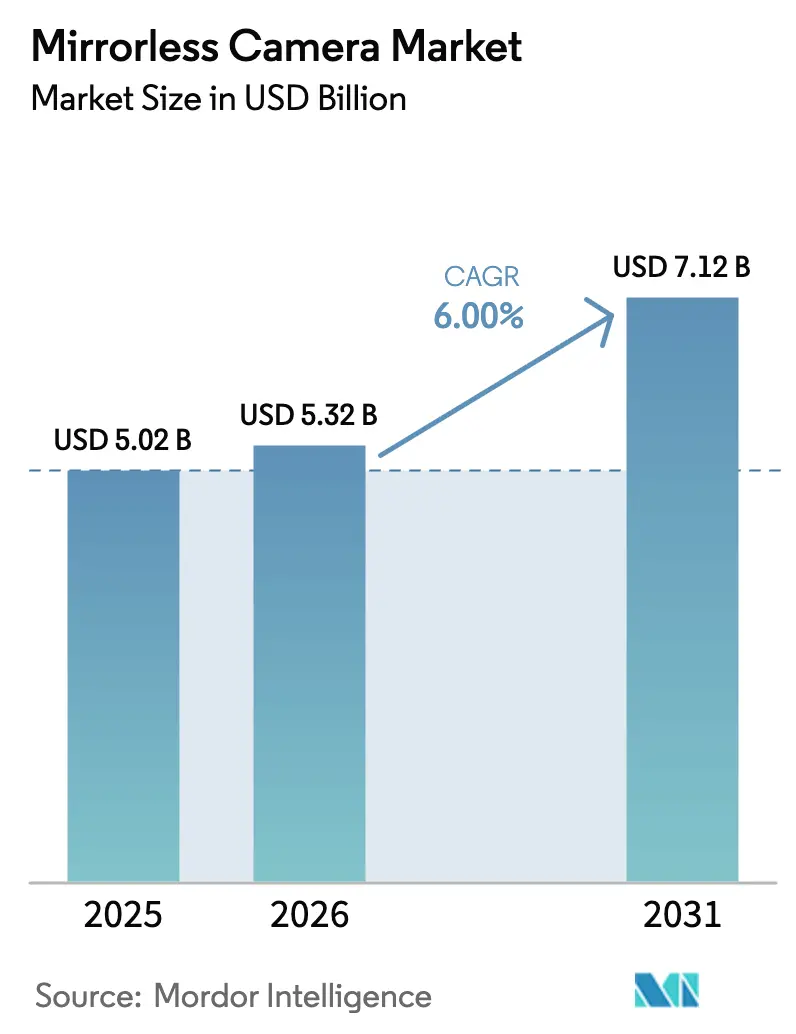

| Market Size (2026) | USD 5.32 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

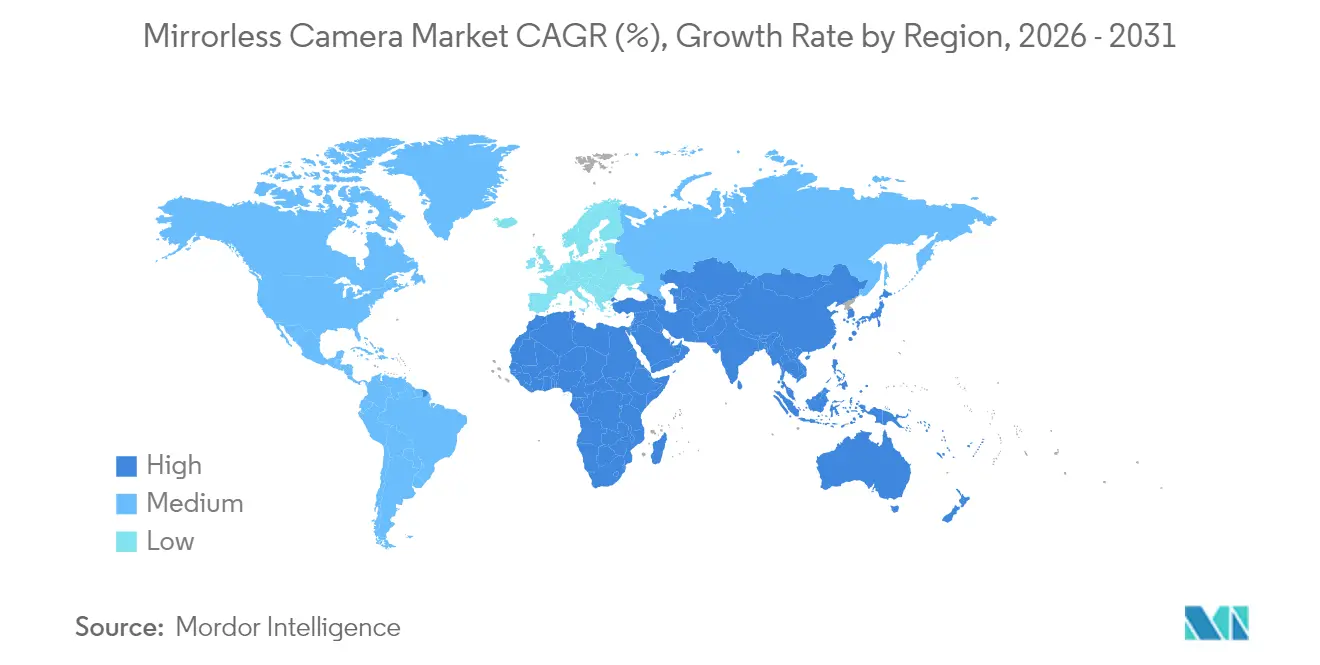

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

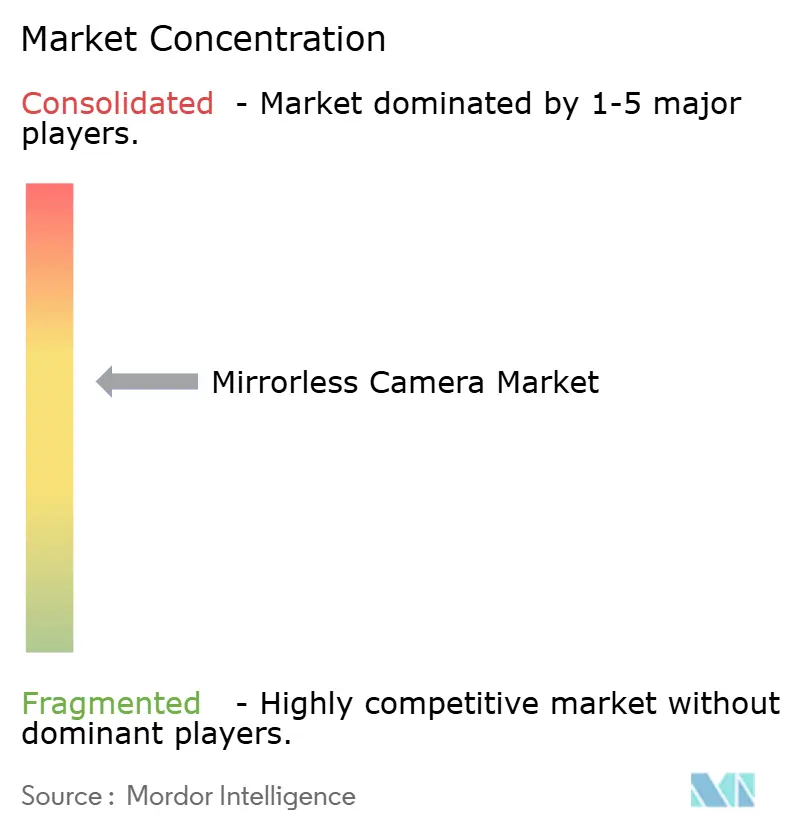

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mirrorless Camera Market Analysis by Mordor Intelligence

The mirrorless camera market size was valued at USD 5.02 billion in 2025 and estimated to grow from USD 5.32 billion in 2026 to reach USD 7.12 billion by 2031, at a CAGR of 6.00% during the forecast period (2026-2031). Growing demand for hybrid-shooting equipment, quick lens ecosystem expansion, and the EU USB-C mandate have accelerated the shift from DSLR to mirrorless systems. Price segmentation shows mid-range bodies occupying the largest revenue share, while premium models record the fastest growth as manufacturers abandon low-margin entry tiers. Asia remains the dominant production and consumption hub, yet the Middle East now delivers the highest regional CAGR owing to government film-incentive programs. Competitive dynamics continue to intensify after Nikon’s USD 223 million purchase of RED Digital Cinema, a move that underscores the rising importance of professional video features. At the same time, smartphone computational photography restricts entry-level sales, forcing brands to emphasize premium differentiation and enterprise-grade video functionality.

Key Report Takeaways

- By lens type, interchangeable systems led with 86.80% of the mirrorless camera market share in 2025, while built-in lens bodies are forecast to grow at 9.08% CAGR through 2031.

- By end-user, prosumers held 47.10% revenue share in 2025; professional users exhibit the fastest 6.22% CAGR to 2031.

- By video resolution, up-to-4K models commanded 61.20% share of the mirrorless camera market size in 2025 and above-6K/8K units are advancing at 10.18% CAGR through 2031.

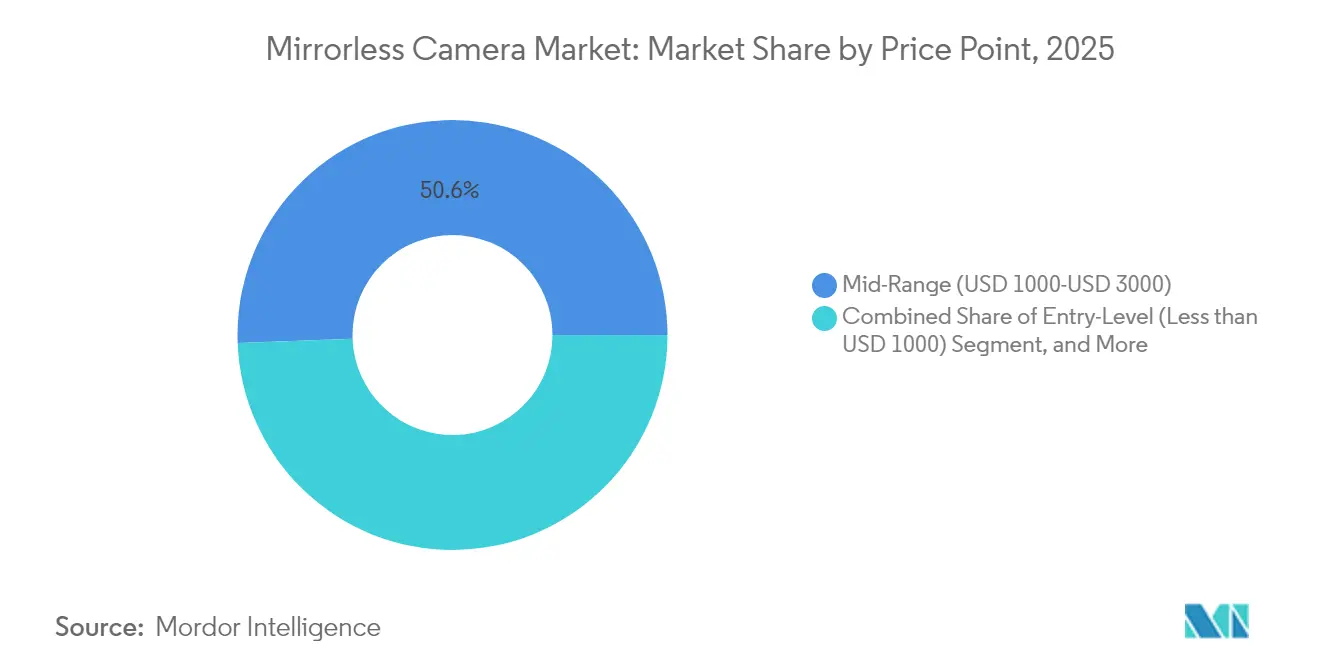

- By price point, mid-range bodies captured 50.60% share of the mirrorless camera market size in 2025, while systems priced above USD 3,000 expand at 8.76% CAGR through 2031.

- By distribution channel, offline retail retained 68.10% revenue share in 2025; online sales record a 9.12% CAGR through 2031.

- By geography, Asia led with 35.80% share in 2025 and the Middle East posts the strongest 9.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mirrorless Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming demand for 4K/6K hybrid-shooting models among content creators | +1.80% | North America, Europe | Medium term (2-4 years) |

| Surging adoption of full-frame bodies by wedding and event professionals | +1.20% | Europe, spill-over to North America | Short term (≤ 2 years) |

| Corporate and education sector shift to mirrorless live-streaming set-ups | +0.90% | North America, expanding to APAC | Medium term (2-4 years) |

| Government film-incentive programs fuelling high-end purchases | +0.70% | Middle East | Long term (≥ 4 years) |

| Rapid lens-road-map expansion by Japanese OEMs | +1.40% | Global | Short term (≤ 2 years) |

| Transition of broadcast broadcasters from ENG camcorders to mirrorless | +0.60% | APAC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Demand for 4K/6K Hybrid-shooting Models Among Content Creators

The creator economy now expects 4K and 6K recording as standard, prompting brands to design bodies that switch seamlessly between stills and video. Canon’s EOS R1, announced in May 2024, brings oversampled 8K capture, high frame-rate 4K, and refined subject-tracking autofocus to meet these expectations. Such specifications explain why above-6K/8K models post a 10.4% CAGR. Nikon’s acquisition of RED Digital Cinema adds cinema-grade codecs and sensor expertise, broadening Z-mount appeal for professional video creators. [1]Nikon Corporation, “Nikon to Acquire US Cinema Camera Manufacturer RED.com, LLC,” nikon.com As content platforms prioritize UHD delivery, buyers future-proof their equipment, accelerating refresh cycles across North America and Europe.

Surging Adoption of Full-Frame Bodies by Wedding and Event Professionals

European wedding photographers are migrating from DSLRs to full-frame mirrorless units that deliver silent shutters, superb low-light performance, and dual card redundancy. The EU USB-C mandate triggered accelerated DSLR retirement, pushing demand toward new mirrorless lines. [2]DSLR Bodies, “Remember This Date: December 28, 2024,” dslrbodies.com Professionals tolerate premium pricing because lighter bodies reduce fatigue during 10-hour events, and clients expect instant RAW-to-social turnaround. This dynamic lifts high-end segment revenue and sets visible equipment standards that prosumers then emulate.

Corporate and Education Sector Shift to Mirrorless for Live-Streaming Set-ups

North American firms and universities have standardized mirrorless cameras for board-room broadcasts, investor calls, and hybrid classrooms. Bodies offering USB-C video output, unlimited recording, and native streaming presets enable broadcast-quality output without dedicated crews. Procurement heads value total ownership savings over bulky studio rigs, driving bulk orders that buoy mid-range body volumes. Manufacturers now sell education bundles with capture cards and software licenses to cement brand lock-in across campuses.

Government Film-Incentive Programs Fuelling High-End Purchases

Saudi Arabia’s Vision 2030 and the UAE media free zones reimburse up to 35% of local production spend, but only if crews source equipment in-country. Production companies therefore secure top-tier mirrorless cinema kits to satisfy audit rules and attract international co-producers. The policy funnel boosts regional high-end sales, explaining the Middle East’s 9.7% CAGR and reinforcing the segment’s 8.9% global growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flagship-smartphone computational photography cannibalising entry-level sales | -1.30% | APAC consumer markets | Short term (≤ 2 years) |

| Supply-chain volatility in CMOS and IBIS components affecting ASPs | -0.80% | Global manufacturing | Medium term (2-4 years) |

| Steep learning curve limiting adoption by first-time hobbyists | -0.50% | Developed markets | Long term (≥ 4 years) |

| Import tariff escalations on optics in South America | -0.30% | South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Flagship-Smartphone Computational Photography Cannibalising Entry-Level Sales

Premium smartphones now stack dozens of exposures in milliseconds, rivalling APS-C sensor output for casual use. CIPA’s January 2025 statistics show compact camera shipments rebounding 11%, while entry-level mirrorless units inch forward only 5%, a gap attributed to smartphone convenience. In high-penetration APAC markets, shoppers skip sub-USD 1,000 cameras, forcing brands to steer users into pricier mid-range lines where hardware advantages remain obvious.

Supply-Chain Volatility in CMOS and IBIS Components Affecting ASPs

Concentrated sensor fabs and geopolitically exposed supply routes push average selling prices higher. Industry data indicate camera ASPs doubling over five years as firms prioritize premium bodies to preserve margins. Sony’s public admission of production hurdles underscores market-wide exposure. Scarcity encourages firms to allocate scarce parts to SKUs above USD 3,000, shrinking choice for value-oriented consumers and tempering overall shipment growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lens Type: Interchangeable Systems Drive Innovation

Interchangeable bodies yielded 86.80% of mirrorless camera market revenue in 2025. They dominate because professionals demand optical flexibility across sports, portrait, and cinema assignments. Built-in lens cameras, while only a niche today, achieve 9.08% CAGR on the back of compact premium concepts such as Fujifilm’s GFX100RF, a 102 MP large-format unit with an integrated 35 mm F4 optic announced in March 2025. Canon’s pledge to add 15 RF optics in 2024 illustrates how a vibrant lens roadmap deepens switching costs and shortens refresh cycles.

Interchangeable systems also attract third-party makers like Sigma, which release RF and Z-mount primes that expand creative options and nudge owners to upgrade bodies to exploit faster AF and stabilization algorithms. Yet built-in lens design gains may lure travelers and vloggers who prize simplicity, hinting at future convergence where single-optic bodies serve as high-end everyday companions alongside workhorse interchangeable rigs.

By End-User: Prosumers Bridge Professional Gap

Prosumers controlled 47.10% of 2025 revenue, reflecting enthusiasts who spend thousands yet shun full commercial workflows. They flock to cameras that bundle flagship autofocus, dual card slots, and 10-bit internal video at approachable prices, anchoring the mid-range where the mirrorless camera market size shows its deepest pool of buyers. Professional users grow at 6.22% CAGR because filmmakers, wedding shooters, and broadcast crews retire ENG camcorders in favor of compact systems capable of RAW video.

Nikon’s product surveys highlight content creators under 35 as the prime adoption vector; they prioritize aesthetics, weight, and direct-to-stream workflows. Meanwhile, casual hobbyists drift toward phones, squeezing the low end. Brands therefore market accessories-vertical grips, context-aware menus, AI subject tracking-to persuade prosumers that stepping up to USD 2,000 bodies secures professional-grade reliability without studio overhead.

By Video Resolution: Ultra-High Definition Drives Premium Growth

Up-to-4K units retained 61.20% share of the mirrorless camera market in 2025. They satisfy most viewing platforms while controlling file sizes. The 4K-to-6K tranche forms a transition zone where manufacturers concentrate R&D, packing oversampled sensors that keep moiré low and dynamic range high. Above-6K/8K models post the 10.18% CAGR, spurred by cinema and streaming studios that demand future-proof capture.

Canon’s EOS R1 will deliver 8K 60 fps and subject AI fine-tuned for sports and news, scaling the resolution ladder without compromising rolling-shutter performance. Fujifilm’s forthcoming GFX ETERNA likewise targets large format video for high-budget productions. These launches reinforce a bifurcation where smartphones cover casual stills and mid-tier hybrid bodies, while UHD mirrorless rigs dominate professional creation.

By Price Point: Mid-Range Dominance Faces Premium Pressure

Mid-range equipment priced USD 1,000-USD 3,000 captured 50.60% of mirrorless camera market revenue in 2025. This band concentrates the most active feature competition: 10-bit 4:2:2 internal codecs, 6K oversampling, and 7-stop IBIS. Supply pits Sony, Canon, and Nikon in a cadence of annual refreshes to maintain share. High-end units above USD 3,000 however expand 8.76% annually, buoyed by professionals and wealthy enthusiasts upgrading to stacked sensors and flagship AF.

Tariff hikes of 24-46% on imported bodies entering the United States and selective South American duties tighten premiums further, nudging production shifts toward ASEAN to mitigate costs. Rising ASPs double in five years as scarce CMOS inventory favors high-margin SKUs, reinforcing the premiumization path where fewer purchases yield higher revenue per unit.

By Distribution Channel: Digital Transformation Accelerates

Brick-and-mortar outlets kept 68.10% revenue share in 2025 because shoppers still prefer hands-on trials before paying four-digit sums. In-store staff guide lens compatibility and rental test drives, adding consultative value. Yet online portals post a 9.12% CAGR to 2031 as high-resolution 3-D configurators and live chat shrink the need for physical inspection. Younger creators research on social video, then transact during flash sales, boosting e-commerce conversion.

Brands pursue omnichannel approaches: flagship stores host workshops, while websites offer same-day pickup at partner dealers. China’s 213% surge in compact shipments during January 2025 signals the potency of livestream shopping in camera retail. As AI search aids narrow model choices, the channel gap will narrow, but tactile testing ensures physical stores remain influential for premium bodies.

Geography Analysis

Asia accounted for 35.80% of global revenue in 2025, anchored by Japanese manufacturing and a resurgent Chinese consumer base. Tourism rebound across the region lifted shipment volumes, with camera units transported to duty-free zones as souvenirs for global travelers. Regional award programs such as Japan’s BCN Awards underline fierce domestic rivalry, where Sony and Nikon captured incremental share in 2025.

Europe holds roughly one-quarter of worldwide shipments and experiences a regulatory inflection after the December 2024 USB-C mandate rendered legacy DSLR chargers obsolete. Professional wedding photographers accelerated mirrorless upgrades to capitalize on silent shutters and social-media friendly workflows, cementing full-frame dominance. Sustainability metrics also sway European buyers, who value lower energy consumption in mirrorless bodies compared with DSLR equivalents.

The Middle East delivers the fastest 9.54% CAGR through 2031. Government rebates that reimburse equipment purchases for qualifying productions motivate local rental houses and studios to stock the latest high-end systems. These policies align with broader diversification goals in Saudi Arabia and the UAE, building creative clusters that attract Netflix, Amazon, and local broadcasters.

North America encounters price headwinds from tariff escalations, forcing brands to reassess supply roots and possibly adopt regional assembly to protect margins. Education and corporate live-streaming demand partially offsets consumer softness. South America lags amid steep optics duties and currency volatility, which hinder adoption despite deep social-media creator communities that aspire to professional gear.

Competitive Landscape

Canon leads the mirrorless camera market with a 46.5% share across interchangeable-lens segments, leveraging an EOS R lineup that stretches from beginner bodies to the forthcoming R1 flagship. Song’s mirrorless leadership claim hinges on high-volume APS-C lines and dominating global image-sensor supply, a vertical integration that targets a 60% sensor market footprint by 2025. Nikon narrows the gap by absorbing RED Digital Cinema, immediately acquiring RAW codec IP and fostering crossover lenses that invite still shooters into pro video.

Market participants converge on AI autofocus, human pose recognition, and cloud-connected firmware. Third-party lens makers like Sigma and Tamron bolster ecosystem attractiveness, while smartphone vendors erode bottom-tier demand through computational imaging leaps. Supply chain resilience becomes a competitive differentiator, spurring brands with diversified fabs to secure sensor allocation and keep mid-range launches on schedule. Patent portfolios in stacked sensors and phase-detection AF define the moat that separates incumbents from newcomers.

Mirrorless Camera Industry Leaders

Canon Inc.

Sony Group Corp.

Nikon Corp.

FUJIFILM Holdings Corp.

Panasonic Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fujifilm launched the FUJIFILM GFX100RF, a 102 MP large-format body with a built-in 35 mm F4 lens, weighing 735 g.

- February 2025: Canon confirmed its 22nd consecutive year at No. 1 in global interchangeable-lens sales, backed by 15 new RF lenses.

- January 2025: BCN Awards honored Sony and Nikon for notable Japanese share gains.

- November 2024: Fujifilm announced development of its first filmmaking camera, the GFX ETERNA, for 2025 release.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the mirrorless camera market as factory-built, interchangeable or fixed-lens digital still cameras in which the optical viewfinder is replaced by an electronic display, and the image is captured on a solid-state sensor. Units sold as camera-lens kits as well as body-only sales are included.

Scope Exclusion: Stand-alone lenses, action cams, and smartphone clip-on modules lie outside this scope.

Segmentation Overview

- By Lens Type

- Built-in/Static Lens

- Interchangeable Lens

- By End-User

- Professional (Commercial Studios, Media Houses)

- Prosumer/Enthusiast

- Amateur/Hobbyist

- By Video Resolution

- Up to 4K

- 4K - 6K

- Above 6K/8K

- By Price Point

- Entry-Level (Less than USD 1000)

- Mid-Range (USD 1000 - USD 3000)

- High-End (Above USD 3000)

- By Distribution Channel

- Offline Retail (Brand and Specialty Stores)

- Online Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regional photo-equipment distributors, retail buyers, pro-photographer guild heads, and rental-house managers across Asia, North America, and Europe. These dialogues validated sell-through ratios, assessed gray-market leakage, and refined the online-to-offline channel weights that secondary data could not capture alone.

Desk Research

We mapped historical unit shipments and average selling prices using public releases from CIPA, the Consumer Technology Association, and country customs dashboards such as U.S. ITC DataWeb. Trade-body newsletters and peer-reviewed optics journals helped track sensor advances, while company 10-Ks and investor decks revealed channel mix and regional demand shifts. Subscription datasets in D&B Hoovers and Volza supported revenue normalization across currency and warranty terms. This list is illustrative; many other reputable sources underpinned the evidence base.

Market-Sizing & Forecasting

Top-down modeling began with CIPA shipment volumes reconstructed into factory-gate value, which are then split by sensor class, price band, and geography. Results are cross-checked through sample bottom-up roll-ups of leading supplier revenues and selective channel audits to temper bias. Variables such as full-frame penetration, ASP progression by sensor size, lens-attach rates, replacement cycles among content creators, disposable income growth, and smartphone substitution index feed a multivariate regression that projects demand to 2030. Where data gaps appeared, for example, in Middle East e-commerce sell-out, survey findings guided proportional adjustments.

Data Validation & Update Cycle

Every output passes a two-level analyst review, anomaly flags trigger re-contact of sources, and currency conversions are benchmarked against IMF averages. Reports refresh yearly, with mid-cycle updates if material events occur. Before shipment, an analyst performs a final pass so clients receive the latest view.

Why Mordor's Mirrorless Camera Baseline Commands Reliability

Published estimates often diverge, and that is because firm-level choices on product scope, channel coverage, and refresh cadence rarely align.

Key gap drivers include whether kits and refurbished units are merged, if estimates use retail or factory value, and how smartphone cannibalization is treated. Mordor's model anchors on shipped-unit evidence, applies fresh ASP audits each quarter, and benefits from continuous primary validation, whereas other publishers may rely on broader digital-camera pools or dated cost curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.02 B (2025) | Mordor Intelligence | - |

| USD 6.80 B (2024) | Global Consultancy A | Combines mirrorless with hybrid DSLR bodies and applies retail mark-ups |

| USD 4.40 B (2023) | Industry Association B | Uses distributor revenues, limited online channel capture, older base year |

These contrasts show why, by grounding the baseline in verifiable shipments and timely ASP evidence, Mordor Intelligence delivers a balanced, transparent figure that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the mirrorless camera market?

The mirrorless camera market size stands at USD 5.32 billion in 2026 and is forecast to reach USD 7.12 billion by 2031, reflecting a 6.00% CAGR.

Which region leads mirrorless camera sales?

Asia holds 35.80% of global revenue thanks to its manufacturing base and strong consumer demand.

Why are professionals choosing mirrorless over DSLR?

Silent shutters, lighter bodies, better low-light performance, and regulatory shifts such as the EU USB-C directive are driving professionals toward mirrorless systems.

How are smartphones affecting camera sales?

Advanced computational photography in flagship phones is cannibalising entry-level camera demand, pushing traditional brands to focus on higher-value segments.

Which segment shows the fastest growth?

Cameras capable of recording above 6K/8K video exhibit the highest 10.18% CAGR as content creators seek future-proof resolution and cinema-grade features.

What impact did Nikon’s acquisition of RED Digital Cinema have on the market?

The deal enhances Nikon’s video credentials, intensifies competition in professional segments, and signals the growing importance of cinema-grade capabilities in mirrorless platforms.

Page last updated on: