Intelligent Traffic Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.89 Billion |

| Market Size (2031) | USD 21.08 Billion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Traffic Management System Market Analysis by Mordor Intelligence

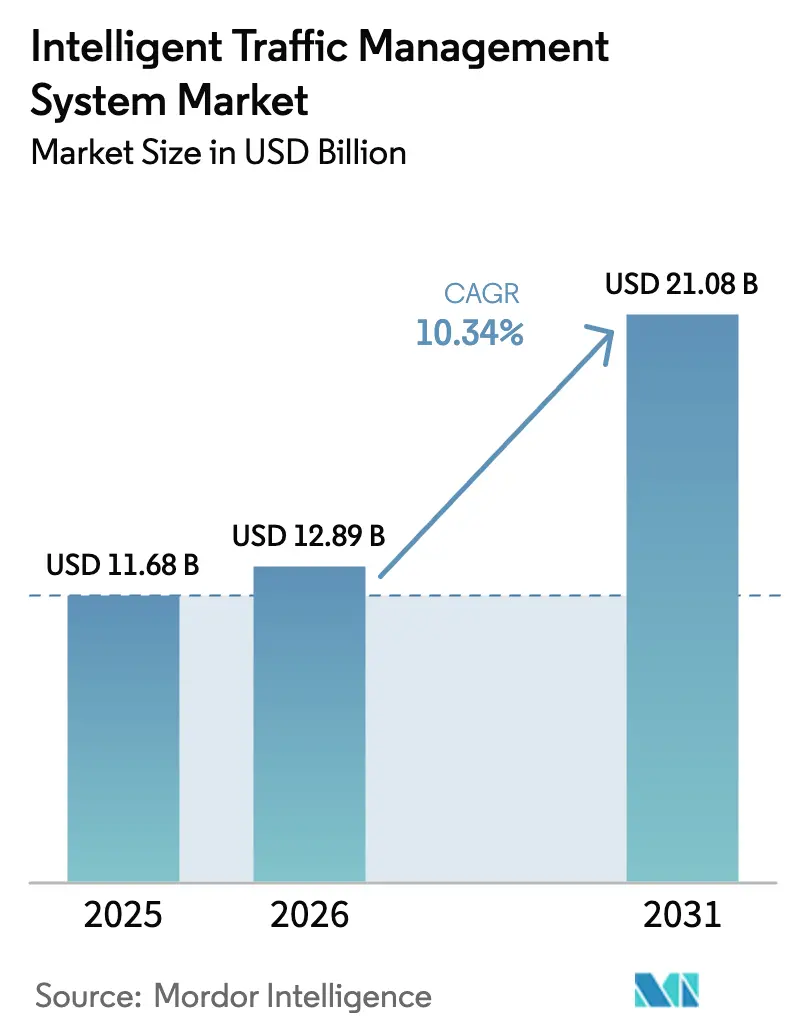

The intelligent traffic management system market size is expected to grow from USD 11.68 billion in 2025 to USD 12.89 billion in 2026 and is forecast to reach USD 21.08 billion by 2031 at 10.34% CAGR over 2026-2031. Growth rests on three pillars: rapid roll-outs of AI-based adaptive signal control across U.S. Sun-Belt metros, sustained EU TEN-T funding for cooperative-ITS projects, and China’s nationwide automatic number-plate recognition mandate. Revenue momentum also reflects congestion-pricing programs in tier-1 cities and Nordic Vision Zero safety targets, both of which intensify demand for real-time enforcement solutions. Hardware still anchors most city spending, yet cloud-hosted analytics accelerate as municipalities seek scalable deployments, while probe-vehicle data and mmWave radar enlarge the toolkit for predictive operations. Competitive intensity is rising because incumbents such as Siemens Mobility and Kapsch TrafficCom now face AI-native entrants that promise faster software iterations and lower.

Key Report Takeaways

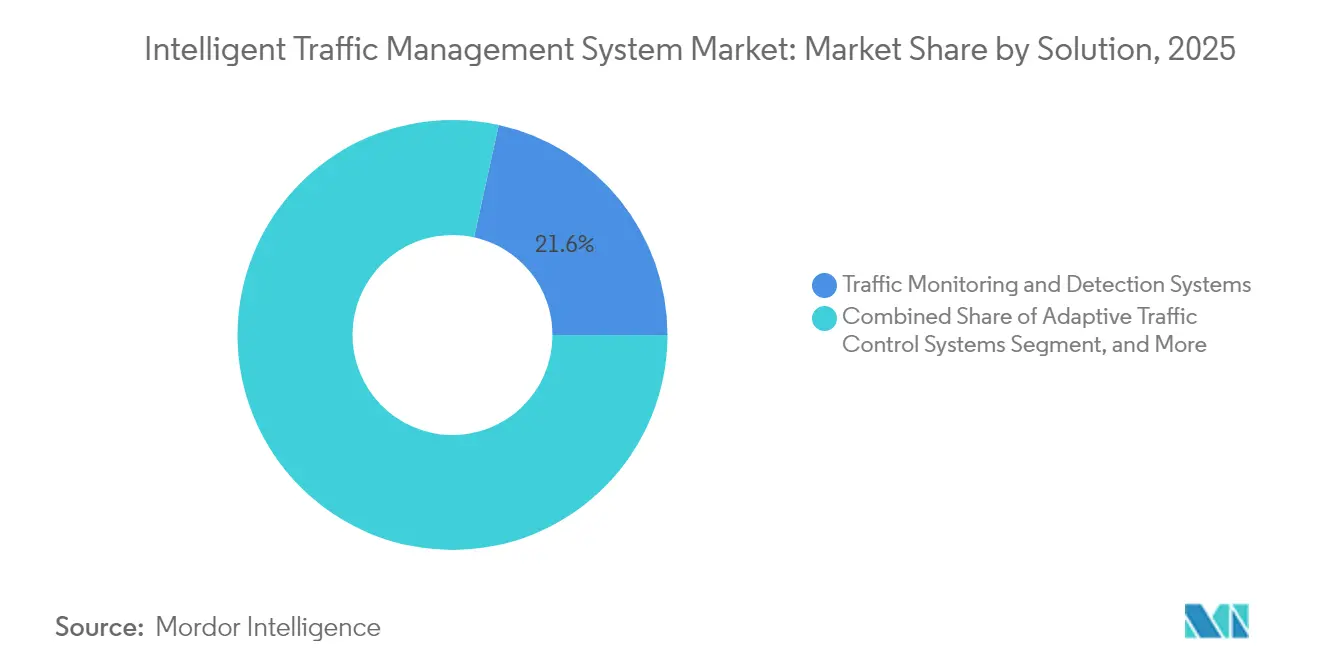

- By solution, Traffic Monitoring and Detection Systems led with 21.55% of intelligent traffic management system market share in 2025, whereas Adaptive Traffic Control Systems are projected to expand at an 11.28% CAGR to 2031.

- By component, hardware accounted for 50.78% share of the intelligent traffic management system market size in 2025, while managed and cloud services are forecast to grow at 13.55% to 2031.

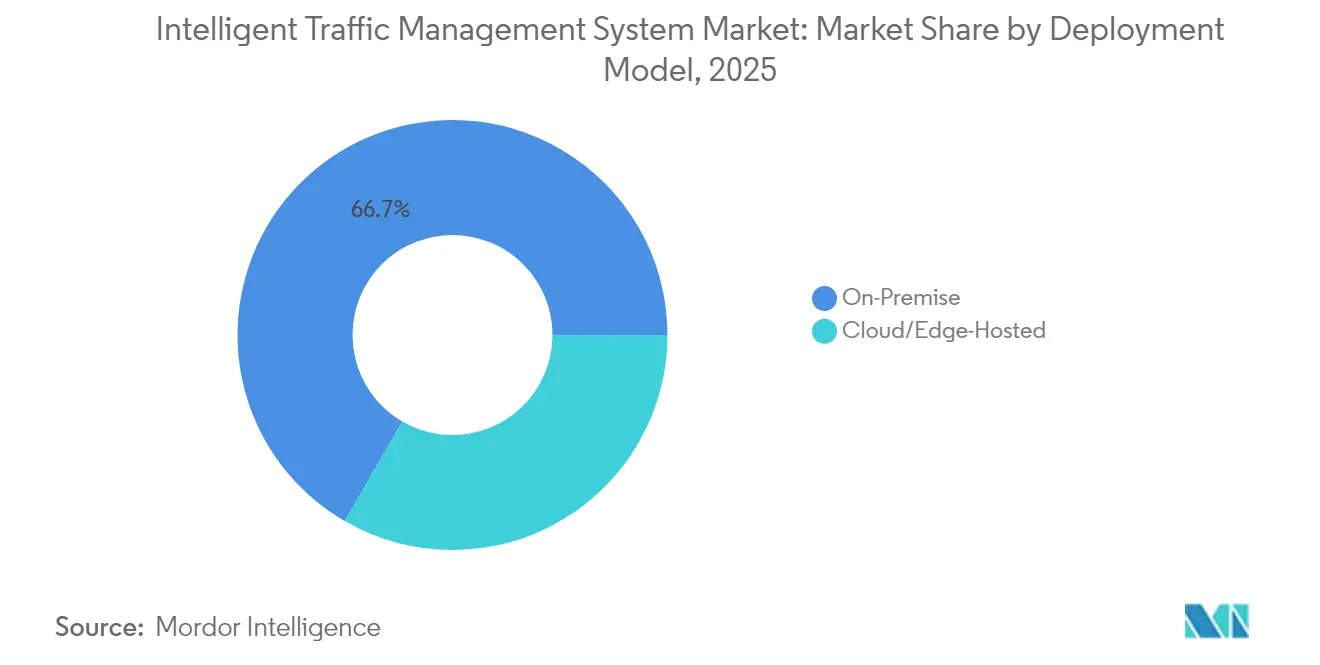

- By deployment model, on-premise platforms held 66.65% of intelligent traffic management system market share in 2025; cloud/edge-hosted alternatives are pacing at 14.92% CAGR.

- By end-use environment, parking and intermodal hubs captured 40.62% of intelligent traffic management system market size in 2025; urban intersections and arterials lead growth at 14.12% CAGR.

- By geography, North America retained leadership with 33.25% revenue share in 2025, whereas Asia-Pacific is set to register the quickest 11.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intelligent Traffic Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven predictive adaptive signal control adoption in U.S. Sun-Belt metros | +1.8% | North America | Medium term (2-4 years) |

| EU TEN-T urban-node funding for cooperative-ITS deployments | +1.5% | Europe | Medium term (2-4 years) |

| Connected-vehicle probe data integration into municipal ATMS | +2.1% | Global | Long term (≥ 4 years) |

| China MPS 2023 mandate for nationwide ANPR enforcement | +1.2% | China | Short term (≤ 2 years) |

| Congestion-pricing platforms in tier-1 cities | +0.9% | North America & Europe | Medium term (2-4 years) |

| Vision Zero safety targets in Nordic countries | +0.7% | Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-driven predictive adaptive signal control adoption in U.S. Sun-Belt metros

Sun-Belt cities are shifting from pre-timed sequences to machine-learning engines that refine green times every few seconds, easing recurring bottlenecks during rush hours.[1]Federal Highway Administration, “Next Generation of Traffic Management Systems and Centers: A Primer,” highways.dot.gov A federal infrastructure grant program now reimburses up to 80% of installation costs, turning adaptive control into the default specification for new intersections. Municipalities value the ability to ingest video, radar and connected-vehicle telemetry in one optimization layer, which improves travel-time reliability without widening roads. Vendors differentiate on cloud-hosted dashboards and cybersecurity compliance, giving small IT teams the confidence to scale networks across hundreds of signals.

EU TEN-T urban-node funding for cooperative-ITS deployments

The TEN-T budget earmarks multi-year grants that cover roadside-unit procurement and cross-border systems testing, shrinking payback periods for European cities.[2]C-Roads Platform, “C-Roads Brochure,” c-roads.eu Austria’s ASFINAG alone deployed 525 ITS-G5 units so that trucks can receive advance warnings about slow-moving traffic. Coordinated funding aligns firmware standards between countries, enabling freight carriers to cross several jurisdictions without swapping communication protocols. The certainty of support has prompted suppliers to pre-certify hardware for pan-European use, trimming engineering costs for each new roll-out.

Connected-vehicle probe data integration into municipal ATMS

Probe-vehicle feeds now augment loop detectors in cities such as Rotterdam, where port-access corridors use speed and heading data from thousands of trucks to fine-tune signal offsets during peak import windows. Because the marginal cost per new data point approaches zero once connectivity is embedded in passenger cars, forecast accuracy improves as the connected-fleet penetration rises. Early adopters note faster incident detection: abrupt multi-lane slowdowns surface on dashboards within 15 seconds, well ahead of 911 calls.

China MPS 2023 mandate for nationwide ANPR enforcement

China’s 2023 regulation obliges local authorities to link every roadside ANPR camera to a central violation database, sparking a procurement wave for high-resolution sensors, GPUs and encrypted backhaul. Shanghai expanded coverage to bus-only lanes, boosting seat-belt compliance and lane discipline while freeing police for priority-response duties. Domestic integrators bundle analytics and cloud storage, lowering total life-cycle cost and smoothing multi-city replicability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget volatility and procurement delays in LATAM municipalities | −0.8% | Latin America | Short term (≤ 2 years) |

| Lack of interoperability standards for C-V2X/V2I stacks | −1.1% | Global | Medium term (2-4 years) |

| Cyber-security compliance costs under EU NIS2 and U.S. TSA rules | −0.6% | North America & Europe | Short term (≤ 2 years) |

| mmWave spectrum constraints for roadside radar in Asian megacities | −0.4% | Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget volatility and procurement delays in LATAM municipalities

Fluctuating exchange rates and patchy tax receipts complicate tender scheduling for mid-tier Latin American cities, often stretching award cycles beyond two years. Even where pilot projects have cut travel times by 25%, administrators struggle to lock multi-year service contracts because cyber-security budgets remain thin. Limited local standards also lengthen bid evaluations, forcing vendors to customize integration scopes for each municipality.

Lack of interoperability standards for C-V2X/V2I stacks

Competing firmware profiles in the 5.9 GHz band mean that a truck equipped for Japanese DSRC cannot always talk to roadside units in California, raising vehicle OEM costs and suppressing fleet uptake.[3]5G Automotive Association, “White Paper on ITS Spectrum Utilization,” 5gaa.org Regional spectrum decisions fragment the ecosystem further, and hardware retrofits after production prove costly. Without harmonization, cross-border freight corridors cannot capitalize fully on collision-avoidance messages, dampening expected safety gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Monitoring Systems Lead Market Evolution

Traffic Monitoring and Detection Systems accounted for 21.55% of intelligent traffic management system market share in 2025. Municipalities buy wide-area awareness first, then layer optimization and enforcement once data pipelines mature. The intelligent traffic management system market size linked to adaptive traffic control is set to grow at an 11.28% CAGR, reflecting city interest in AI-enabled timing plans that curtail average intersection delay. Thermal cameras and LiDAR improve accuracy at night, while machine-learning classifiers now tag vehicle classes with 90% precision. Integration among monitoring, signal control and driver information modules raises return on investment because congestion metrics feed straight into dynamic-message signs that reroute flows during incidents.

Adaptive Traffic Control Systems form the fastest-moving niche as software continually refines phase orders rather than relying on engineer-scheduled plans. Their rise also underpins heightened demand for enforcement cameras; when a city synchronizes red-light timing with adaptive phases, violation detection needs the same refresh cycles. Corridors that share data across adjacent agencies report smoother freight movement, underscoring how monitoring lays the foundation for wider regional mobility management.

By Component: Hardware Dominance Faces Cloud Disruption

Hardware still captured 50.78% of intelligent traffic management system market size in 2025 because sensors, controllers and field cabinets remain mandatory for any deployment. Yet software and managed services now dictate differentiation. Cities that migrate dashboards to cloud subscriptions trim on-premise server costs and gain 24/7 vendor-managed updates. The shift opens doors to new entrants that deliver AI models as over-the-air upgrades, reducing capital outlay and accelerating feature releases, especially around incident prediction and multimodal prioritization.

Edge analytics appliances reconcile the latency demands of connected-vehicle safety messages with the processing burden of computer-vision tasks. Vendors increasingly supply controller-agnostic firmware so that existing cabinets can ingest AI modules without trenching new fiber. Over the forecast horizon, intelligent traffic management system market prospects hinge on blending low-cost field hardware with centralized orchestration, a mix that lowers lifecycle expense and softens procurement barriers for medium-size cities.

By Deployment Model: Cloud Migration Accelerates

On-premise installations held 66.65% share in 2025, reflecting entrenched procurement norms and data-sovereignty rules. Cities handling sensitive violation images still opt for local storage. Nonetheless, cloud and edge-hosted platforms are advancing at 14.92% CAGR as telecom operators bundle secure backhaul and as U.S. TSA directives push encrypted, patch-managed environments.Hybrid topologies take root: sub-second safety loops run locally, while planning dashboards reside in public clouds that crunch multi-year archives.

Software-as-a-Service pricing converts large up-front capex into predictable operating budgets, attractive for municipalities with debt ceilings. Automated penetration-test reports also satisfy NIS2 auditors, further tilting new bids toward hosted offerings. The intelligent traffic management system market therefore mirrors broader smart-city software trends, where cloud scale and AI-assisted analytics reshape value capture.

By End-Use Environment: Intermodal Hubs Drive Innovation

Parking and intermodal hubs controlled 40.62% share in 2025 because these nodes face the densest mixture of private cars, buses, freight and micromobility. Operators deploy occupancy sensors, curb-side cameras and payment APIs to orchestrate quick turnarounds, lifting asset utilization. Urban intersections and arterials now represent the fastest-growing arena, with a 14.12% CAGR, driven by pedestrian safety mandates and the way connected-vehicle data illuminates conflicts in real time. Vision Zero municipalities integrate near-miss analytics that flag hotspots where cyclists and trucks intersect.

In hubs, managers exploit 5G-enabled dashboards to guarantee seamless transfers between rail and last-mile services, an evolution that demands interoperability between ticketing, parking and signal systems. On arterials, adaptive signal groups coordinate phase splits across contiguous corridors, shaving travel times for emergency vehicles and public buses. These contexts illustrate how the intelligent traffic management system market pivots from isolated intersections toward corridor-wide orchestration.

Geography Analysis

North America retained 33.25% revenue in 2025, buoyed by Infrastructure Investment and Jobs Act allocations and state mandates specifying adaptive signal control on new corridors. The region also benefits from mature vendor support, making lifecycle maintenance budgets easier to justify. Canada’s transit-oriented development policies and Mexico’s border-freight digitization projects further diversify demand across metropolitan tiers.

Europe commands a robust installed base nurtured by TEN-T and C-Roads. Harmonized technical specifications allow fleets to receive travel-time advisories uninterrupted from Rotterdam to Vienna. NIS2 has raised minimum cyber-resilience thresholds, pushing agencies to refresh aging controllers with encrypted firmware and intrusion-detection modules. Nordic nations showcase safety gains under Vision Zero, proving that enforcement-centric deployments can halve fatalities through speed and seat-belt compliance improvements.

Asia-Pacific is posting a 11.98% CAGR through 2031. China’s vehicle-road-cloud pilot in Beijing connects 7,000 base stations to roadside edge boxes, enabling sub-second advisory messages to autonomous shuttles. India’s GPS-satellite tolling sidesteps gantry construction, a model well suited to dense tier-II cities. Spectrum allocation constraints mean that megacities such as Tokyo and Seoul experiment with hybrid millimeter-wave and 4G fallback links to maintain roadside radar fidelity during rain, an innovation likely to ripple across ASEAN markets.

Competitive Landscape

The intelligent traffic management system market remains moderately fragmented. The top five suppliers account for roughly 45% of 2024 revenue, leaving room for midsize specialists. Acquisition activity continues: Swarco announced plans to absorb a French traffic-technology unit for EUR 27 million, expanding its lane-control and signage catalog. Siemens Mobility leverages its rail-signalling heritage to pitch long-term service contracts, while Kapsch TrafficCom bundles tolling, enforcement and corridor management into single control rooms.

AI-native firms differentiate through cloud-first architectures. They ship containerized signal-timing engines that self-calibrate via federated learning, appealing to cities lacking in-house data-science staff. Partnerships tighten ecosystems; edge-chip vendors work with signal-head manufacturers so cameras and radar share wiring harnesses. This vertical integration compresses deployment timelines from years to months, a competitive lever when stimulus grants impose hard completion deadlines.

Cyber-security marks a new battleground. Vendors now embed secure-boot and over-the-air patching to comply with TSA Surface Directives. Those lacking ISO 27001 certification face exclusion from high-profile bids. Consequently, firms with internal security-operation centers command premium maintenance fees, tipping revenue mixes toward annuities. Despite rising competition, client stickiness stays high once a platform underpins 1,000 plus intersections, because switching entails controller refits and operator retraining.

Intelligent Traffic Management System Industry Leaders

Transcore Inc.

TomTom International BV

Miovision Technologies Incorporated

Econolite Inc.

Kapsch Trafficom AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kapsch TrafficCom won a USD 1.4 million order to modernize Hawaii’s Tetsuo Harano Tunnel control system, extending a three-decade partnership with the state DOT.

- February 2025: Parsons reported USD 6.8 billion revenue for fiscal-year 2024, noting double-digit growth in intelligent transportation contracts.

- February 2025: Siemens Mobility secured a EUR 2.8 billion framework with Deutsche Bahn to supply modern control and safety technology.

- December 2024: Swarco began exclusive talks to acquire Lacroix’s traffic-technology division, a move that will deepen market penetration in French-speaking regions

- November 2024: Kapsch TrafficCom debuted satellite tolling for India, repurposing the solution proven in Norway and Bulgaria.

Global Intelligent Traffic Management System Market Report Scope

The Intelligent Traffic Management System is a solution that integrates real-time data analysis with advanced machine learning algorithms. The study tracks the revenue accrued through various players globally selling intelligent traffic management system types. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The Intelligent traffic management System market is segmented by solution (traffic signal control system, traffic enforcement camera system, traffic monitoring system, and Intelligent driver information system), component (surveillance cameras, video walls, traffic controllers and signals, and others), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Adaptive Traffic Control Systems |

| Traffic Signal Control Systems |

| Traffic Monitoring and Detection Systems |

| Enforcement Camera and ANPR Systems |

| Dynamic Message/Driver Information Systems |

| Integrated Corridor and Incident Management Platforms |

| Hardware (Sensors, Controllers, Cameras, VMS) |

| Software (Central Management, Edge Analytics, API) |

| Services (Consulting, Integration, Managed/Cloud) |

| On-Premise |

| Cloud/Edge-Hosted |

| Urban Intersections and Arterials |

| Freeways and Expressways |

| Tunnels and Bridges |

| Parking and Intermodal Hubs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Solution | Adaptive Traffic Control Systems | ||

| Traffic Signal Control Systems | |||

| Traffic Monitoring and Detection Systems | |||

| Enforcement Camera and ANPR Systems | |||

| Dynamic Message/Driver Information Systems | |||

| Integrated Corridor and Incident Management Platforms | |||

| By Component | Hardware (Sensors, Controllers, Cameras, VMS) | ||

| Software (Central Management, Edge Analytics, API) | |||

| Services (Consulting, Integration, Managed/Cloud) | |||

| By Deployment Model | On-Premise | ||

| Cloud/Edge-Hosted | |||

| By End-Use Environment | Urban Intersections and Arterials | ||

| Freeways and Expressways | |||

| Tunnels and Bridges | |||

| Parking and Intermodal Hubs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the intelligent traffic management system market?

The market generated USD 12.89 billion in 2026 and is projected to reach USD 21.08 billion by 2031.

Which solution segment holds the largest revenue share?

Traffic Monitoring and Detection Systems led with 21.55% market share in 2025.

Why are cloud-hosted platforms gaining traction?

They cut on-premise server costs, enable automatic software updates, and ease compliance with new cybersecurity rules.

Which region is expected to grow fastest through 2031?

Asia-Pacific is forecast to expand at a 11.98% CAGR due to large-scale deployments in China and India.

How are procurement delays impacting Latin America?

Budget volatility extends tender cycles, slowing the rollout of advanced traffic management despite strong pilot-project results.

What technology underpins the fastest-growing solution segment?

AI-driven adaptive traffic control uses machine-learning algorithms to adjust signal timing in real time, supporting the 11.28% CAGR forecast for this segment

Page last updated on: