Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

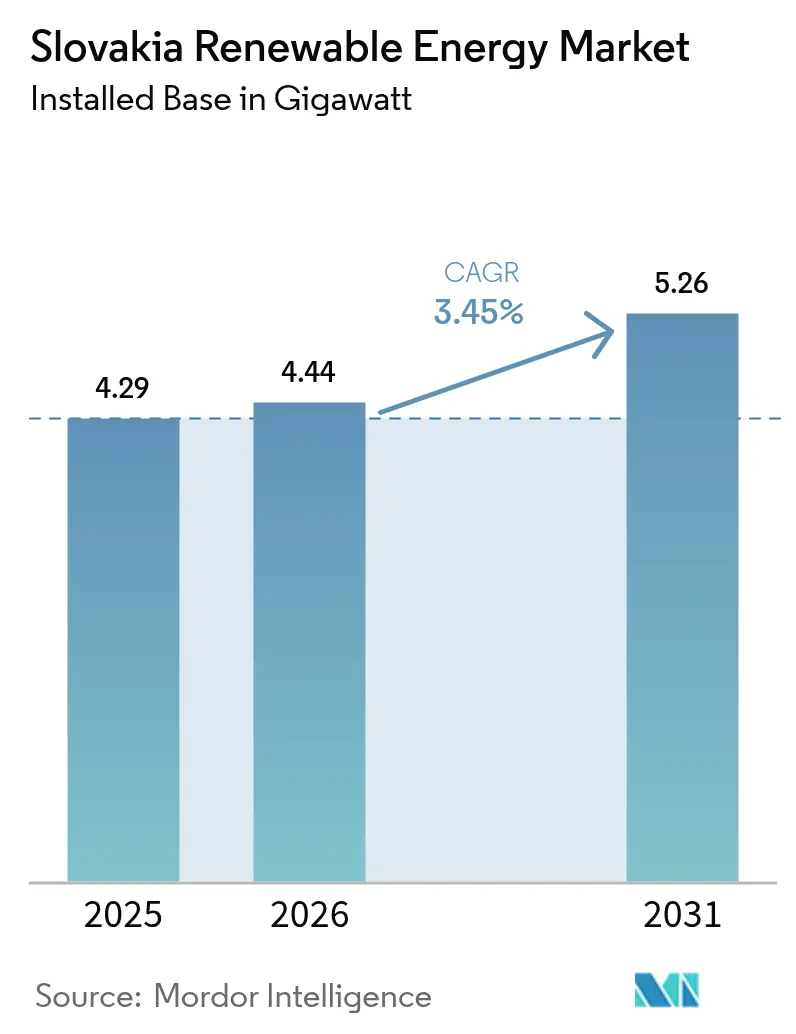

| Base Year Market Size (2025) | 4.29 gigawatt |

| Market Volume (2026) | 4.44 gigawatt |

| Market Volume (2031) | 5.26 gigawatt |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Slovakia Renewable Energy Market Analysis by Mordor Intelligence

Slovakia Renewable Energy Market size in 2026 is estimated at 4.44 gigawatt, growing from 2025 value of 4.29 gigawatt with 2031 projections showing 5.26 gigawatt, growing at 3.45% CAGR over 2026-2031.

Momentum arises from EU Fit-for-55 and Renewable Energy Directive (RED III) compliance requirements, escalating climate-linked funding streams, and strategic grid reinforcements that ease historical interconnection bottlenecks. The market’s moderate but steady growth also reflects Slovakia’s unique energy architecture in which nuclear plants supply nearly two-thirds of domestic electricity, creating a “nuclear lock-in” that structurally caps the share of intermittent renewables. Hydropower leverages mature infrastructure and topography to preserve its leadership position, while falling solar photovoltaic (PV) levelized cost of electricity (LCOE) ignites a new build cycle and attracts foreign technology partnerships. Corporate power-purchase agreements (PPAs) are accelerating as heavy industry seeks price stability amid carbon-pricing expansion, and recently amended environmental-impact-assessment (EIA) rules shorten permitting pathways, signaling a more supportive regulatory stance.

Key Report Takeaways

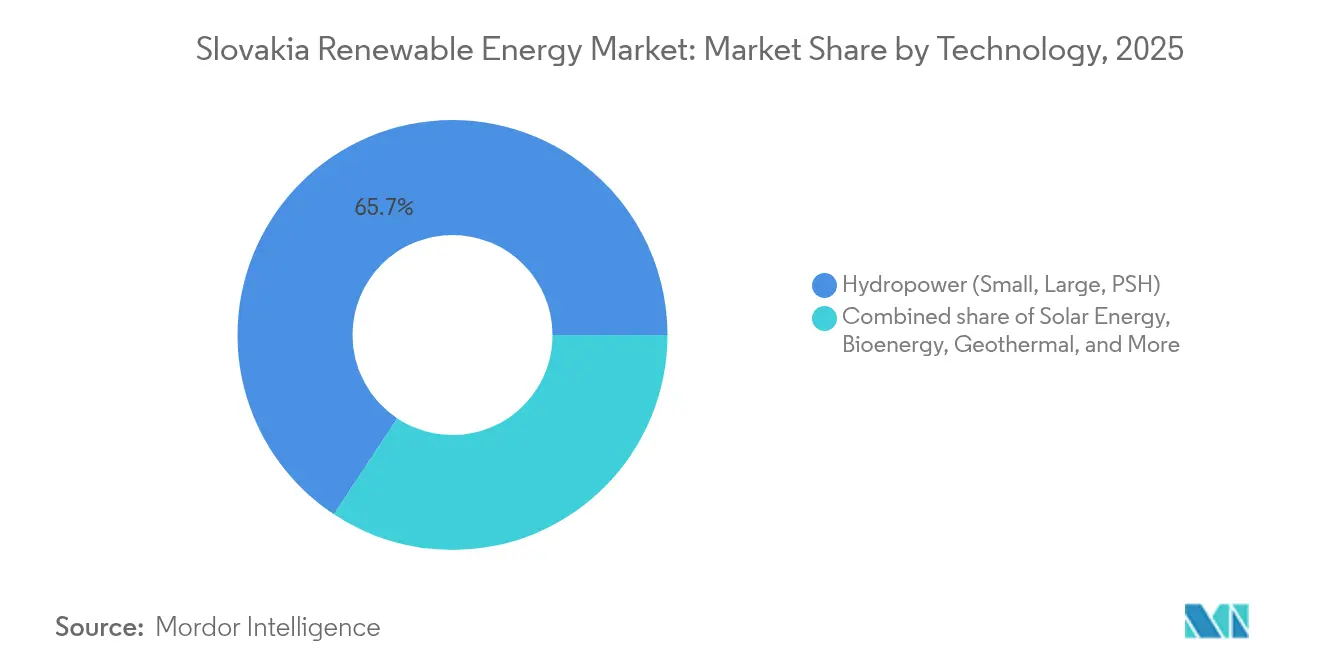

- By technology, hydropower commanded 65.70% of Slovakia's renewable energy market share in 2025, whereas solar energy is forecast to grow at a 8.75% CAGR through 2031.

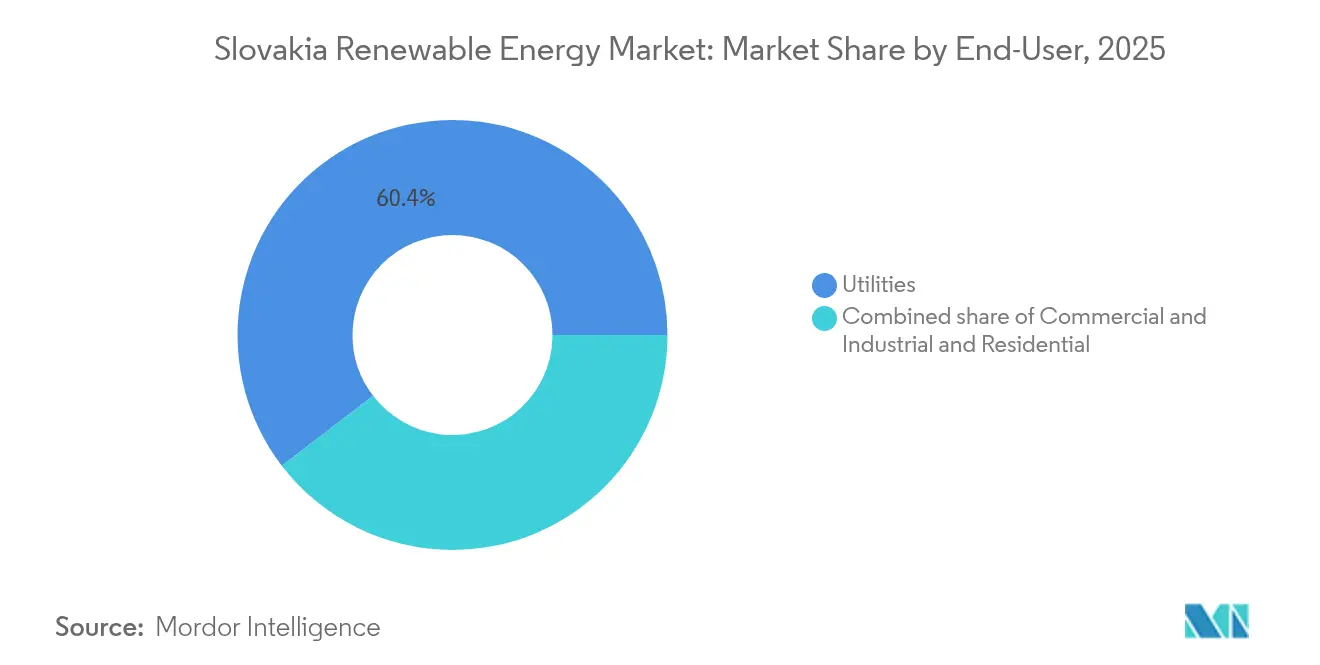

- By end-user, utilities held 60.40% of the Slovakia renewable energy market size in 2025, while commercial and industrial applications are projected to expand at a 7.35% CAGR between 2026 and 2031

- Európska energetická a priemyselná holding-owned Slovenské elektrárne, EPH, and SEPS together controlled about 57.20% of installed capacity in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovakia Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Fit-for-55 & RED III compliance pressures | +1.2% | EU-wide, concentrated in Slovakia | Medium term (2-4 years) |

| Declining LCOE of solar PV & on-shore wind | +0.8% | Global, with regional Slovak benefits | Short term (≤ 2 years) |

| EU funded grid-interconnection upgrades | +0.6% | Central Eastern Europe, Slovakia focus | Long term (≥ 4 years) |

| Rising corporate PPAs from heavy industry | +0.5% | National, concentrated in industrial regions | Medium term (2-4 years) |

| Pumped-storage upgrades for grid flexibility | +0.3% | National, mountainous regions | Long term (≥ 4 years) |

| Agrivoltaic pilots on land-consolidation farms | +0.2% | Rural Slovakia, pilot regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Fit-for-55 & RED III Compliance Pressures Drive Accelerated Deployment

Slovakia must raise renewable energy to 23% of final consumption by 2030 under its updated National Energy and Climate Plan, a target that narrowly trails the European Commission’s 24% guidance and the REPowerEU ambition of 42.5%. The looming gap intensifies project pipelines, and infringement proceedings for slow permitting hastened the December 2024 EIA Act overhaul that tightens statutory deadlines and lifts capacity thresholds subject to full assessments. Carbon-pricing expansion via the EU Emissions Trading System (ETS) and scheduled ETS2 launch for buildings and transport in 2027 will push electricity demand higher, spurring renewable additions as clean electrification becomes the least-cost compliance route.[1]OECD Economy Surveys, "Addressing housing market challenges in the Slovak Republic," oecdecoscope.blog Administrative fines up to EUR 1.6 million embed a powerful enforcement mechanism that raises the opportunity cost of non-compliance for developers and utilities, reinforcing momentum across the Slovakia renewable energy market.

Declining LCOE Creates Competitive Advantage for Solar and Wind Technologies

Average utility-scale solar PV costs fell below EUR 40/MWh in 2024, enabling 274 MW of new capacity, triple the yearly average of the prior decade, once the 2021 “stop-status” grid-connection freeze was lifted. Sekisui Chemical’s memorandum with the Economy Ministry to localize lightweight perovskite PV production underscores investor confidence, with ¥10 billion (USD 68 million) earmarked for a pilot plant. Wind development regained traction, evidenced by 942 MW under environmental assessment, though permitting spans multiple agencies, and community opposition persists.[2]Publications Office, “Regulation (EU) 2022/869 on guidelines for trans-European energy infrastructure,” eur-lex.europa.eu As cost parity extends to hybrid projects that blend PV, wind, and storage, developers can arbitrage complementary generation profiles, moderating grid-balancing penalties that have historically dampened intermittent uptake in the Slovakia renewable energy market.

EU-Funded Grid Infrastructure Upgrades Enable Regional Integration

Slovakia’s inclusion in the North–South Interconnection (NSI) East corridor prioritizes a fourth 400 kV CZ–SK interconnector (500 MW) targeted for 2035 commissioning, a direct response to current congestion that limits renewable dispatch. Projects of Common Interest (PCI) status accelerates permitting and unlocks Connecting Europe Facility grants that cover up to 50% of eligible costs. Complementary smart-grid schemes, ACON with the Czech Republic and Danube InGrid with Hungary, modernize distribution automation, raising distributed-generation hosting capacity. National TSO SEPS released 170 MW of additional PV and wind connection rights in 2024, yet still lags the EU-mandated 70% cross-border capacity availability benchmark. Pumped hydro upgrades at Čierny Váh enhance upward and downward regulation reserves, providing the flexibility needed to integrate intermittent additions and sustaining grid stability for the Slovakia renewable energy market.

Corporate Power-Purchase Agreements Emerge from Industrial Energy-Security Concerns

Slovak heavy industry, notably automotive and metal producers, intensified renewable procurement to hedge volatile wholesale prices after the 2022 gas crisis. Utility-scale auctions transitioned from feed-in tariffs to feed-in premiums, aligning remuneration with market signals and creating depth for bilateral PPAs. Cross-border virtual PPAs, such as the agreement between T-Mobile Czech Republic and Slovak Telekom, illustrate how corporates lock in multi-year pricing while sidestepping residual domestic regulatory hurdles. Demand is further fueled by looming Scope 3 supply-chain mandates under the EU’s Corporate Sustainability Reporting Directive, encouraging Tier 1 suppliers to secure traceable clean electricity. Bankability of deals improves as lenders discount counterparty risk tied to carbon exposure, solidifying PPAs as a mainstream offtake route in the Slovak renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & limited cross-border capacity | -0.9% | National grid, cross-border points | Medium term (2-4 years) |

| Lengthy multi-agency permitting cycles | -0.7% | National, all project types | Short term (≤ 2 years) |

| Sparse local component supply chain | -0.4% | National, concentrated in western industrial regions | Medium term (2-4 years) |

| Eco-activism opposing small hydro projects | -0.3% | Regional, mountainous areas with sensitive ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion Constrains Renewable Integration Despite Infrastructure Investments

A nuclear-heavy generation mix shapes grid-dispatch protocols that favor large, stable output, leaving little residual headroom for intermittent sources at critical nodes. While SEPS has allocated fresh capacity, sections of the 400 kV backbone remain constrained, and the EU-imposed 70% transmission-capacity-allocation rule exposes compliance risks. Interconnection points with the Czech Republic (Lanzhot) and Ukraine (Velké Kapušany) experience seasonal congestion that forces curtailment or redispatch of renewable output, reducing revenue certainty for project sponsors.[3]Taylor Wessing, “Oil & Gas Laws and Regulations in Slovakia 2024,” ceelegalmatters.com Distribution grids, predominantly operated by SPP-Distribúcia, also require substantial reinforcement to accommodate two-way power flows from rooftop PV and community projects. Unless grid digitalization and capacity upgrades keep pace, the Slovakia renewable energy market will face diminished growth prospects relative to its policy potential.

Multi-Agency Permitting Cycles Create Development Timeline Uncertainty

Renewable projects navigate approvals across 72 district offices with overlapping jurisdiction, often duplicating document requests and prolonging decision cycles past 30 months.[4]Marián Bošanský and Marek Mariak, “Environment & Climate Change Laws and Regulations Slovakia 2025,” iclg.com The December 2024 EIA Act amendment raises screening thresholds and imposes time-bound consultation windows, but practical implementation remains untested. Some sectoral laws restrict administrative appeals, funneling grievances directly to courts, which can add 6-12 months before a final investment decision. Non-transferability of certain licenses complicates project-financing structures that rely on special-purpose vehicles, and shifting municipal zoning plans introduces further unpredictability. These frictions elevate financing costs and compress the viable pipeline, tempering the otherwise positive trajectory of the Slovak renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hydropower Leadership and Solar Acceleration Reshape the Mix

Hydropower represented 65.70% of the renewable capacity within the Slovakia renewable energy market share in 2025, capitalizing on established dams along the Váh and Danube rivers. The segment benefits from predictable runoff patterns and existing pumped-storage capability that also supplies ancillary services. However, incremental expansion is largely limited to efficiency uprates and small-hydro refurbishments. Solar energy, while starting from a lower base, posted the highest growth, with utility-scale additions driving a projected 8.75% CAGR to 2031. This acceleration positions PV to chip away at hydropower’s dominance and raise the Slovakia renewable energy market by more than 0.58 GW over six years.

The wind segment has only 3 MW installed but boasts a 942 MW pipeline under assessment, indicating pent-up potential should permitting hurdles ease. Bioenergy advances through biomethane retrofits of legacy agricultural digesters, illustrated by EnviTec’s Bierovce and Ožďany plants that deliver grid-quality gas. Geothermal emerges as an untapped resource, with Košice’s EUR 56.2 million project on track for 30 MWt by 2028, aided by Just Transition funding. Marine renewables are excluded from domestic build-out owing to Slovakia’s landlocked geography, yet local firms participate in EU ocean-energy supply chains through Horizon programs, diversifying revenue streams without affecting domestic generation totals.

By End-User: Utilities Retain Scale Advantage While Industrial Offtake Gains Traction

Utilities accounted for 60.40% of the Slovakia renewable energy market size in 2025, anchored by Slovenské elektrárne’s fleet and the territorial distribution monopolies of ZSE, SSE, and VSE. Their grid access, balance-sheet strength, and obligation to serve create a natural advantage in tender participation and project financing. Nonetheless, the commercial and industrial (C&I) segment is projected to clock a 7.35% CAGR, propelled by decarbonization mandates cascading through automotive, steel, and electronics supply chains.

Residential adoption lags due to electricity retail tariffs that remain 3.5 times higher than gas on an energy-equivalent basis, dampening heat-pump economics despite generous Green Households vouchers. Recovery and Resilience Plan grants earmark EUR 528 million to retrofit 30,000 homes, potentially nudging rooftop PV and heat-pump uptake. Meanwhile, virtual PPAs enable multinational telecom and technology firms to procure renewable electricity across borders, demonstrating new pathways for demand aggregation beyond traditional utility structures, and intensifying competition within the Slovakia renewable energy market.

Geography Analysis

Slovakia’s central European location positions it as a transit hub in the continental grid, yet its own renewable integration is hampered by the nuclear-weighted baseload that occupies transmission headroom. Western regions, home to automotive clusters around Bratislava and Trnava, drive C&I renewable demand through corporate decarbonization targets, while hosting rooftop PV growth supported by mature distribution grids. Hydropower assets cluster along rivers traversing mountainous northern and central zones, where topographical features enable both run-of-river and pumped-storage installations, stabilizing frequency and voltage across the Slovakia renewable energy market.

Eastern districts benefit from EU Just Transition funds earmarked for coal-phase-out and industrial diversification, as exemplified by the Košice geothermal concession that leverages deep hydrothermal reservoirs to supply district heating. Rural southern counties exhibit high solar insolation and expansive agricultural land suitable for agrivoltaics, aligning with pilot programs that co-locate PV with crop production. Cross-border interconnectors with Austria, Hungary, Poland, and the Czech Republic deliver both export and import flexibility, but also expose domestic renewables to curtailment when congestion protocols prioritize nuclear dispatch.

National participation in the Hydrogen Interconnection (HI) East corridor will unlock low-carbon-hydrogen trade routes post-2030, complementing renewable electricity with green molecules for hard-to-abate sectors. Landlocked geography precludes coastal resource exploitation, but Slovak engineering firms contribute components to tidal- and wave-energy demonstrators in other EU states, capturing ancillary value while maintaining focus on domestic renewable generation assets. As regional grid codes converge under the European Network of Transmission System Operators for Electricity, Slovak grid operators must harmonize balancing-reserve requirements, thereby elevating the technical sophistication of the Slovak renewable energy market.

Competitive Landscape

Market structure remains moderately concentrated: Slovenské elektrárne provides 71% of national electricity, largely from nuclear, whereas hydropower, biomass, and emerging solar capacity diversify generation but do not yet disrupt incumbent dominance. Regional distributors ZSE (E.ON-controlled), SSE, and VSE retain exclusive service areas, influencing connection timelines and tariff structures that shape renewable project economics. Foreign technology partnerships increasingly define competitive differentiation, illustrated by Sekisui Chemical’s perovskite PV venture and InoBat’s battery alliance with Gotion Hi-Tech, which together localize high-value manufacturing capability.

Niche innovators broaden the landscape: Solargis supplies granular irradiation data that optimizes PV siting, while GA Drilling’s geothermal tools target hard-rock reservoirs, reducing drilling cost curves. EU Important Projects of Common European Interest (IPCEI) grants reduce capital-expenditure hurdles for first-of-a-kind facilities, enabling domestic firms to scale alongside incumbents rather than confront insurmountable entry barriers. Corporate PPAs shift bargaining power toward large industrial offtakers, encouraging international utilities and traders to enter Slovakia’s market to aggregate demand and backstop supply.

Grid-modernization contracts open new revenue streams for digital-solution providers, as SEPS and distribution operators deploy advanced metering and automated switchgear to comply with EU cybersecurity and interoperability rules. Although incumbents maintain strategic advantages in legacy assets and customer bases, technological convergence, capital inflows, and evolving policy frameworks signal a gradual transition toward a more pluralistic and competitive Slovak renewable energy market.

Slovakia Renewable Energy Industry Leaders

-

Slovenské elektrárne, A.S.

-

Axpo Holding AG

-

ČEZ Slovensko s.r.o.

-

Západoslovenská energetika (ZSE/E.ON)

-

GreenWay Infrastructure s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Slovakia enacted EIA Act amendments to accelerate renewable-project permitting, raising capacity thresholds and shortening review cycles.

- June 2025: Prime Minister Robert Fico announced that Slovakia is set to ink an intergovernmental deal with the US, clearing the path for Westinghouse Electric Company to establish a new nuclear reactor unit at the current Bohunice site.

- June 2024: InoBat began battery-cell production in Voderady, making Slovakia the fifth European nation with certified cell output.

- February 2024: Sekisui Chemical signed an MoU to explore perovskite PV manufacturing in Slovakia with a planned ¥10 billion investment.

Slovakia Renewable Energy Market Report Scope

Renewable energy is a form of energy obtained from a source that can be replenished over time and leaves a negligible carbon footprint on the environment upon utilization. Renewable energy sources include solar, wind, geothermal, biomass, water, and tides. Renewable energy is often termed an alternative energy source as it is an alternative to fossil fuels. The market sizing and predictions for the segment have been made based on installed capacity (in GW). The Slovakia renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Slovakia renewable energy market in 2026?

Installed renewable capacity reached 4.44 GW in 2026, led by hydropower’s 65.70% share.

What CAGR is expected for Slovak renewables through 2031?

Aggregate capacity is projected to grow at a 3.45% CAGR, hitting 5.26 GW by 2031.

Which segment grows fastest within Slovak renewables?

Solar PV is forecast to expand at a 8.75% CAGR thanks to falling costs and improved permitting.

Why are corporate PPAs gaining traction in Slovakia?

Heavy industry seeks long-term price stability and carbon-compliance benefits amid EU ETS expansion.

What limits large-scale wind deployment in Slovakia?

Lengthy multi-agency permitting and public opposition constrain the 942 MW project pipeline.

How will grid upgrades influence renewable growth?

New interconnectors and smart-grid projects add capacity headroom, enabling more solar and wind integration.

Page last updated on: