Sleeping Aids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

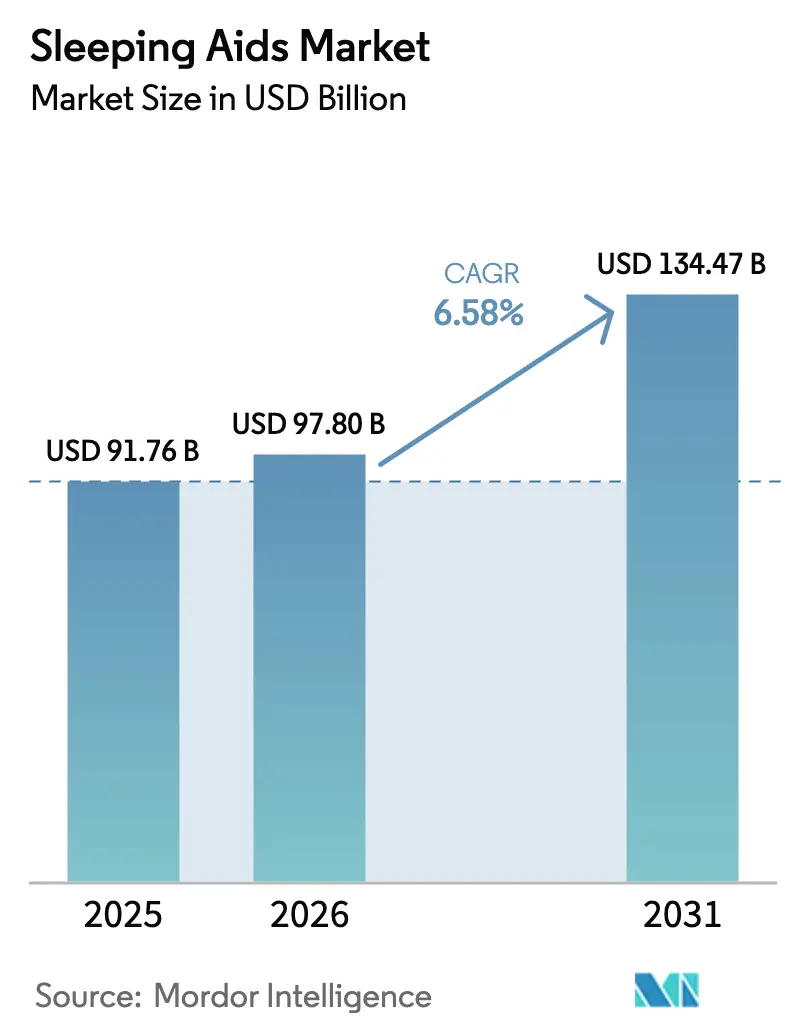

| Market Size (2026) | USD 97.80 Billion |

| Market Size (2031) | USD 134.47 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

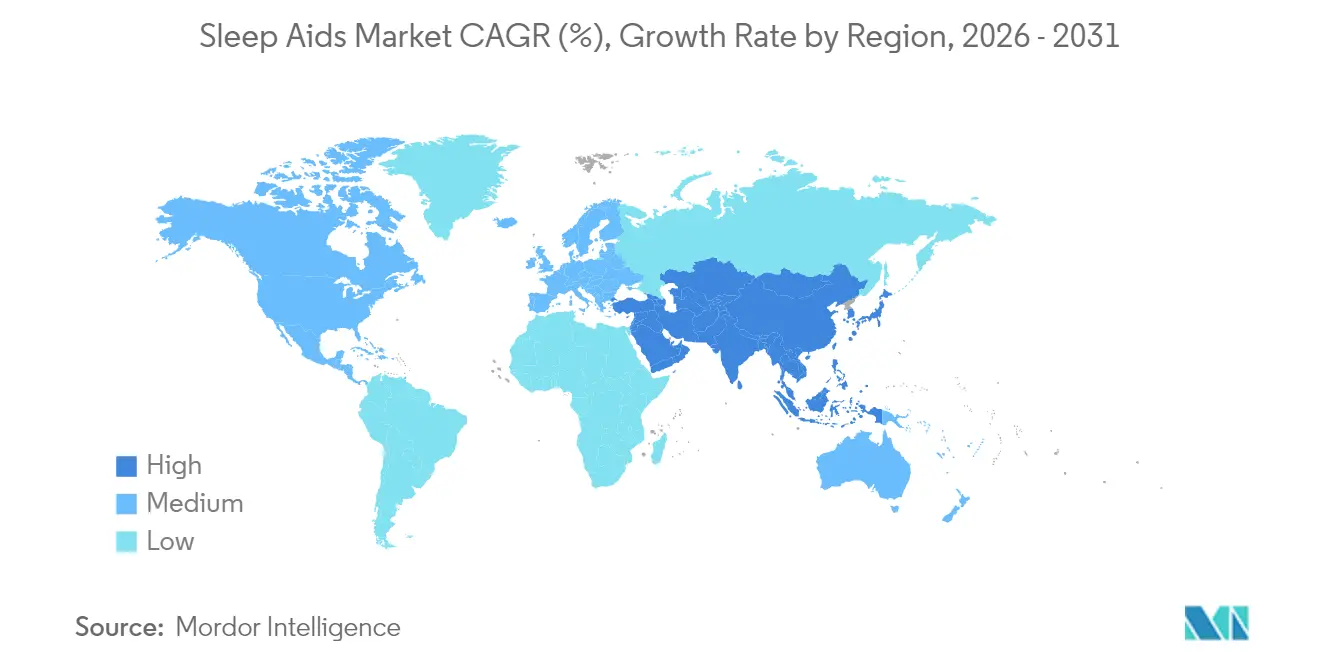

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sleeping Aids Market Analysis by Mordor Intelligence

The Sleeping Aids Market size is expected to increase from USD 91.76 billion in 2025 to USD 97.80 billion in 2026 and reach USD 134.47 billion by 2031, growing at a CAGR of 6.58% over 2026-2031.

Demand accelerates as global insomnia and sleep-breathing conditions affect nearly 2.5 billion people, especially among seniors whose insomnia rates are 40% higher than younger cohorts, prompting both pharmaceutical innovation and data-driven non-drug interventions. Corporate wellness programs, insurance reimbursement for PAP and oral devices, and an exploding smart-device ecosystem reinforce structural growth opportunities while venture investment fuels next-generation AI mattresses and wearables. Parallel restraint factors include safety concerns over prescription hypnotics, counterfeit supplements on e-commerce sites, and price sensitivity in emerging economies, yet these headwinds only partially offset strong demand catalysts.

Key Report Takeaways

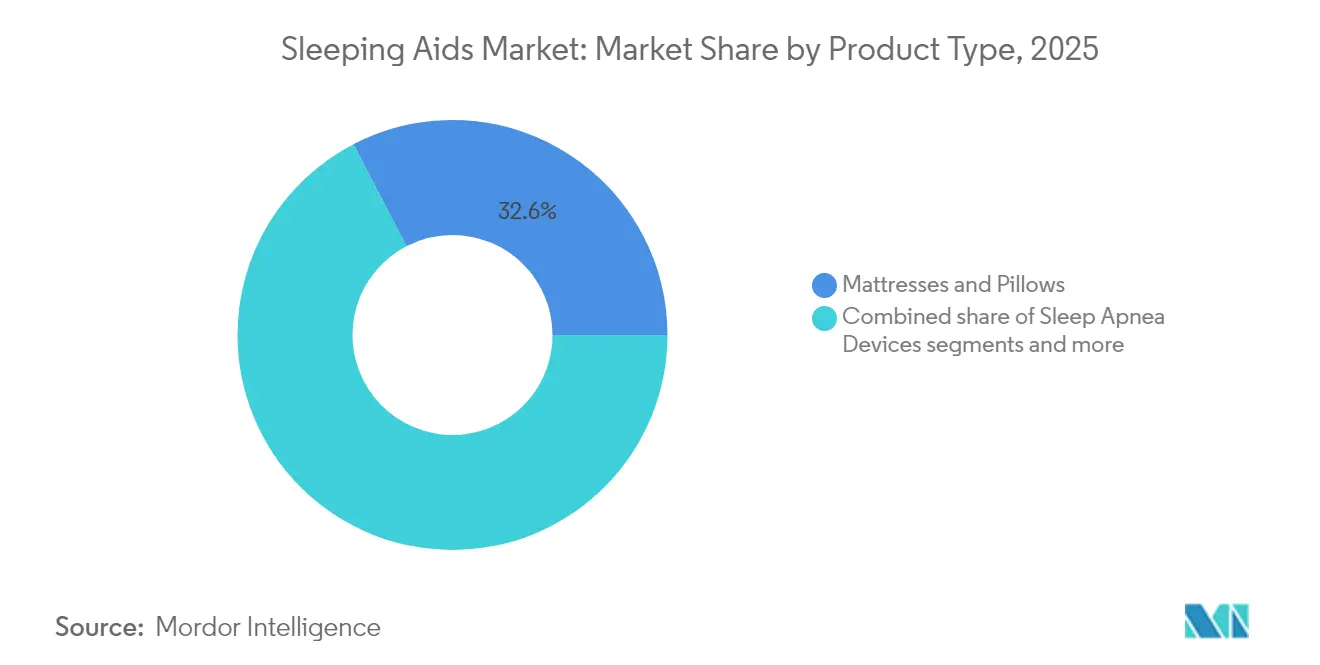

- By product category, mattresses & pillows led with 32.62% revenue share in 2025; smart sleep monitoring devices are projected to expand at a 7.05% CAGR to 2031.

- By sleep disorder, insomnia captured a 39.10% share of the sleeping aids market size in 2025 while sleep apnea treatment records the fastest 7.63% CAGR through 2031.

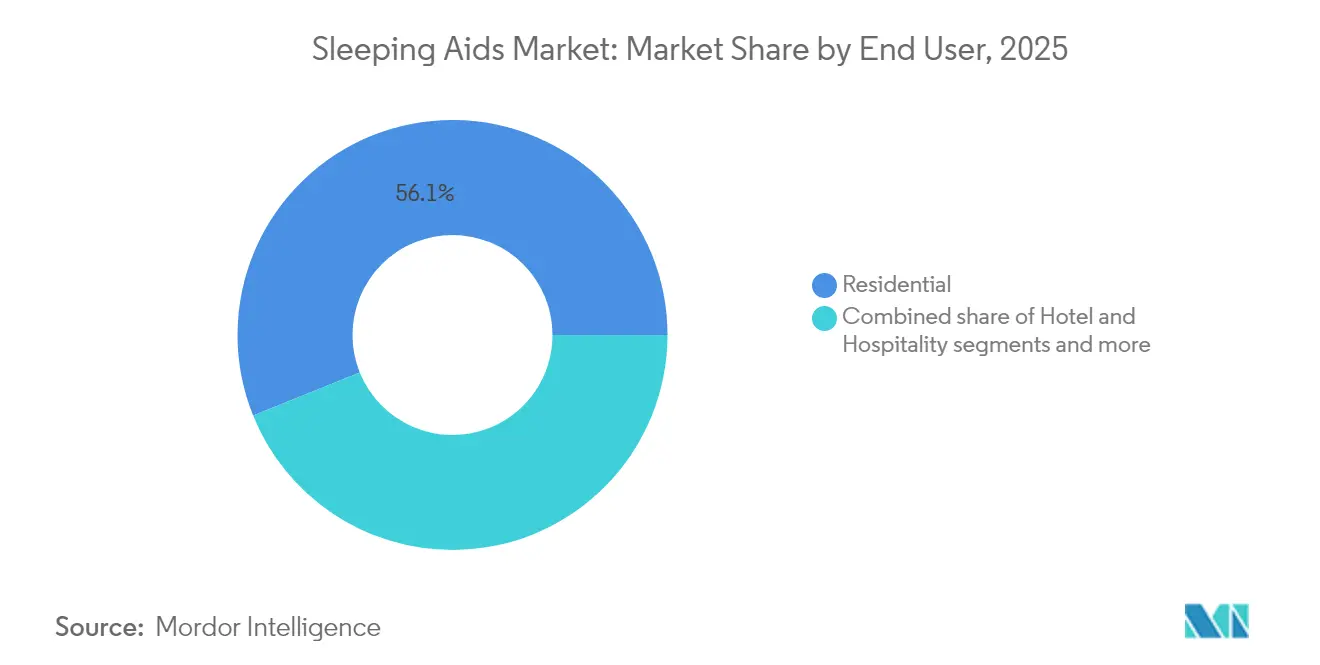

- By end user, residential applications held 56.10% of the sleeping aids market share in 2025, whereas hotel & hospitality use cases advance at an 8.21% CAGR over 2026-2031.

- By geography, North America commanded 41.85% share in 2025; Asia-Pacific is growing at a 9.02% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sleeping Aids Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of insomnia among aging populations | +1.2% | Global, with highest concentration in North America & Europe | Long term (≥ 4 years) |

| Growing availability of OTC melatonin & natural supplements | +0.8% | Global, particularly strong in North America & Asia-Pacific | Medium term (2-4 years) |

| Surge in smart-sleep technology adoption (IoT beds & trackers) | +1.5% | North America & EU leading, rapid expansion in APAC | Medium term (2-4 years) |

| Corporate wellness programs adding sleep solutions | +0.6% | Primarily North America & Europe, emerging in urban APAC | Medium term (2-4 years) |

| Insurance reimbursement expansion for PAP & oral devices | +0.9% | North America & Europe, gradual expansion to developed APAC markets | Long term (≥ 4 years) |

| Hotel "sleep-tourism" packages boosting premium bedding demand | +0.4% | Global luxury markets, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Insomnia Among Aging Populations

An expanding cohort of adults aged 65 plus—set to double by 2030—elevates long-run demand in the sleeping aids market. Clinical data link poor sleep to 23% higher cardiovascular risk and 31% greater diabetes complications, pushing healthcare systems to fund preventive sleep programs. Pharmaceutical pipelines shift toward orexin-receptor antagonists that block wakefulness instead of inducing broad sedation, ensuring safer profiles for seniors. Parallel hardware innovation embeds temperature and posture sensors in smart mattresses to counter thermoregulation changes that disturb 78% of seniors. These converging medical and technology responses secure durable revenue streams for companies serving the sleeping aids market.

Growing Availability of OTC Melatonin & Natural Supplements

Melatonin supplement revenues are forecast to quintuple between 2022-2032, yet assays show deviations up to 478% between labeled and actual dosages, sparking regulatory alerts. Premium, third-party-tested formulations now command 40-60% price premiums, while herbal alternatives such as valerian and L-theanine gain traction among consumers seeking hormone-free options. In India, rising adoption of botanical sleep aids lifted prescription-volume for sleep-related products by 8% after COVID-19. This demand diversification adds incremental sales but also intensifies competition, compelling brands to emphasize transparency and clinical validation within the sleeping aids market.

Surge in Smart-Sleep Technology Adoption (IoT Beds & Trackers)

Smart mattresses now integrate up to 23 sensors that modulate firmness, elevation, and temperature using AI-driven algorithms. Early adopters report 27% higher subjective sleep quality and 29% faster onset within 90 nights. Award-winning models such as the HEKA AI Mattress feature sixth-generation neural networks that flag cardiovascular anomalies, while Eight Sleep’s thermoregulation platform is credited with 40% quicker sleep initiation among elite athletes. Ecosystem integration allows beds to synchronize with HVAC and lighting controls, positioning the sleeping aids market for cross-category bundling opportunities.

Corporate Wellness Programs Adding Sleep Solutions

Employers lose an estimated USD 3,156 per worker annually to sleep-related productivity drag. Corporations increasingly subsidize smart beds, coaching apps, and on-site screenings, delivering measurable ROI via reduced absenteeism. Pioneering hospitality concepts, including Equinox Hotels’ Sleep Lab, function as real-world demonstrations of integrated sleep environments and influence enterprise buyers. Millennial and Gen Z talent pools—73% of whom prioritize comprehensive wellness benefits—amplify demand for employer-supported sleep programs, bolstering revenues across the sleeping aids market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reported side-effects & dependency fears over prescription drugs | -0.7% | Global, particularly pronounced in North America & Europe | Medium term (2-4 years) |

| Patent cliffs for blockbuster hypnotics | -0.5% | Primarily North America & Europe, limited impact in emerging markets | Short term (≤ 2 years) |

| Price sensitivity in emerging economies | -0.9% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Counterfeit supplements on e-commerce channels | -0.3% | Global e-commerce platforms, highest impact in unregulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reported Side-Effects & Dependency Fears Over Prescription Drugs

Generic zolpidem variants now dominate scripts but face heightened scrutiny after reports of memory impairment and complex sleep behaviors. Physicians pivot to behavioral therapies such as CBT-I, while health insurers increasingly require non-drug trials before invasive procedures. Public awareness that melatonin offers limited help for chronic insomnia further erodes confidence in pharmacological fixes, nudging consumers toward tech-enabled solutions and fueling substitution effects inside the sleeping aids market.

Patent Cliffs for Blockbuster Hypnotics

Expired patents on legacy hypnotics accelerate generic entry, compressing revenue and reducing pharma R&D appetite. While lower prices widen access in cost-sensitive regions, the innovation gap leaves room for AI wearables and environmental interventions to gain share until next-generation molecules emerge post-2032. The temporary drug pipeline lull shifts investor capital toward device makers and software platforms across the sleeping aids market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Monitoring Drives Innovation Wave

The mattresses & pillows segment retained 32.62% of the sleeping aids market share in 2025, driven by consumer loyalty to trusted comfort brands and aggressive omni-channel strategies. However, rising demand for AI-embedded beds propels average selling prices to USD 2,000-5,000, enhancing revenue despite slower unit growth. The smart sleep monitoring devices segment is projected to outpace all others at a 7.05% CAGR, underpinned by medical acceptance of remote-patient monitoring and seamless integration with mobile apps. Within the sleeping aids market size for connected devices, CPAP systems increasingly feature Bluetooth modules that upload compliance data to clinicians, boosting therapeutic outcomes and payer reimbursement rates. Hybrid innovations blur category lines—for example, mattress toppers that combine sleep tracking, thermal regulation, and massage—expanding addressable spend per household.

Traditional medications experience margin compression from generic rivalry, while supplements yield mixed results as efficacy scrutiny intensifies. The “other devices & accessories” niche benefits from this shift, with smart pillows and scent diffusers pairing with AI analytics to craft personalized sleep environments. Collectively, convergence across categories positions the sleeping aids market for multiproduct ecosystem sales that lift lifetime customer value and reduce churn.

By Sleep Disorder: Apnea Treatment Accelerates

Insomnia accounted for 39.10% of 2025 segment revenues, underscoring its prevalence and diversity of interventions. Nonetheless, the sleeping aids market size for sleep apnea solutions is forecast to grow fastest at 7.63% CAGR, supported by earlier diagnostics and evolving reimbursement. Oral appliance therapy gains traction after new payment codes, and connected CPAP devices from ResMed and Philips deliver data-driven compliance nudges, raising long-term effectiveness. Restless legs syndrome (RLS) and narcolepsy remain niche but clinically significant: heightened physician education and availability of wearable diagnostics expand the patient pool.

Artificial intelligence now analyzes multivariate sleep data to identify divergent disorders, enabling tailored regimens that range from orexin antagonists to positional therapy wearables. Such precision medicine increases efficacy, reduces side-effects, and advances patient satisfaction, reinforcing premium pricing opportunities across the sleeping aids market.

By End User: Hospitality Segment Surges

Residential customers supplied 56.10% of 2025 value owing to direct-to-consumer mattress brands, smart bed subscriptions, and the pandemic-driven focus on home wellness. Growth continues as manufacturers introduce firmware updates that unlock new features, extending product lifecycles. Medical end users—hospitals and sleep labs—adopt smart beds with pressure sensors that cut nurse workloads and reduce pressure-ulcer incidence, deepening institutional penetration.

The hotel & hospitality segment is the expansion standout, logging an 8.21% CAGR. Luxury chains deploy branded sleep programs, neuroscience-backed rituals, and AI bedding to justify rate premiums and urge customer loyalty. Corporate wellness centers, senior-living communities, and transportation operators comprise the “others” category, each motivated by safety, productivity, or comfort mandates. Collectively, diversified end-user adoption underscores the resilience of the sleeping aids market.

Geography Analysis

North America captured 41.85% of 2025 value thanks to advanced reimbursement systems, high disposable income, and a vibrant R&D ecosystem. The United States anchors growth through prolific smart-bed marketing and over 650 Sleep Number showrooms that maintain direct engagement. Canada leverages universal healthcare that reimburses sleep studies and CPAP devices, while Mexico’s middle class spurs demand for entry-level foam mattresses. Market maturation, however, nudges leading brands to seek incremental growth overseas while upping service revenues at home.

Asia-Pacific posts the quickest 9.02% CAGR and is expected to overtake Europe before 2030. India illustrates unmet need: 93% of adults feel sleep-deprived and average 6.55 hours nightly, propelling sales of both herbal aids and connected devices. China’s government health initiatives support large-scale screening, while Japan’s aging society adopts tech-assisted bedding to counter insomnia linked to long work hours. South Korea’s sleeping aids market size, estimated at KRW 1-1.5 trillion, exemplifies regional willingness to pay for premium foam pillows and anti-microbial bedding. Europe remains a steady contributor, buttressed by strict safety regulations that encourage clinically validated innovation. Northern European nations adopt smart beds fastest, whereas Southern Europe leans toward botanical supplements aligned with wellness lifestyles. South America and the Middle East & Africa show nascent potential; distributors partner with micro-finance providers to overcome price barriers and widen access to essential sleep products.

Competitive Landscape

Moderate fragmentation typifies the sleeping aids market as legacy bedding manufacturers consolidate while tech disruptors introduce AI-centric platforms. Tempur Sealy’s USD 5 billion acquisition of Mattress Firm (now Somnigroup) creates an integrated USD 8 billion sales powerhouse with end-to-end control of design, production, and retail distribution. ResMed sustains leading sleep-apnea device share, aided by digital health add-ons that increased Q2 FY2025 revenue to USD 1.3 billion and lifted gross margin to 58.6%.

Startups thrive by merging neuroscience and AI. Eight Sleep serves more than 100 elite athletes, validating physical-recovery benefits that resonate with affluent consumers, while Somnee’s EEG headbands outperform pharmaceutical sleeping aids in clinical trials and secured USD 10 million seed extension funding. Competitive intensity shifts toward full-stack solutions—hardware, software, and coaching—that deliver measurable health outcomes. This capability gap raises entry barriers, favoring firms with strong data science, regulatory experience, and consumer-marketing prowess.

Sleeping Aids Industry Leaders

Cadwell

Compumedics Limited

DeVilbiss Healthcare LLC

Merck & Co., Inc

Natus Medical Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tempur Sealy completed its USD 5 billion Mattress Firm acquisition, rebranded as Somnigroup International, and pledged carbon neutrality by 2040

- June 2025: Somnee raised USD 10 million to advance EEG-based AI sleep headbands after clinical validation versus melatonin and zolpidem

Global Sleeping Aids Market Report Scope

As per the scope, a sleep aid is a treatment that uses devices or supplemental or herbal compounds to help induce the onset of sleep and to ensure that a patient stays asleep. Sleep aids are most popular among people who have chronic sleep disturbances, particularly insomnia.

The sleeping aids market is segmented by product, sleep disorder, and geography. By product, the market is segmented into mattresses and pillows, sleep laboratory services, medication, and other products. By sleep disorder, the market is segmented into insomnia, sleep apnea, and other sleep disorders. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.

| Mattresses & Pillows |

| Sleep Apnea Devices |

| Medications |

| Supplements |

| Smart Sleep Monitoring Devices |

| Other Devices & Accessories |

| Insomnia |

| Sleep Apnea |

| Restless Legs Syndrome |

| Narcolepsy |

| Others |

| Residential |

| Medical (Hospitals & Sleep Labs) |

| Hotel & Hospitality |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Mattresses & Pillows | |

| Sleep Apnea Devices | ||

| Medications | ||

| Supplements | ||

| Smart Sleep Monitoring Devices | ||

| Other Devices & Accessories | ||

| By Sleep Disorder (Value) | Insomnia | |

| Sleep Apnea | ||

| Restless Legs Syndrome | ||

| Narcolepsy | ||

| Others | ||

| By End User (Value) | Residential | |

| Medical (Hospitals & Sleep Labs) | ||

| Hotel & Hospitality | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the sleeping aids market and its expected 2031 size?

The sleeping aids market stands at USD 97.8 billion in 2026 and is forecast to reach USD 134.47 billion by 2031, growing at a 6.58% CAGR.

Which product category is growing fastest?

Smart sleep monitoring devices exhibit the highest growth, registering a 7.05% CAGR through 2031.

Why is Asia-Pacific expanding quicker than other regions?

Acute sleep-health crises, rising healthcare spending, and rapid tech adoption propel Asia-Pacific to a 9.02% CAGR despite price-sensitive segments.

How are hotels capitalizing on sleep trends?

Luxury chains launch neuroscience-backed programs, adaptive bedding, and circadian lighting that raise room rates and expand the hotel & hospitality share of the sleeping aids market.

What impact do new reimbursement policies have?

Expanded coverage for PAP therapy and oral appliances lowers patient costs, driving higher device adoption and encouraging providers to shift toward non-invasive treatments.

How severe are side-effect concerns with prescription sleep drugs?

Reports of dependency and cognitive impairment push physicians toward behavioral therapy and smart-device alternatives, curbing growth for traditional hypnotics.

Page last updated on: