Sleep Disorders Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

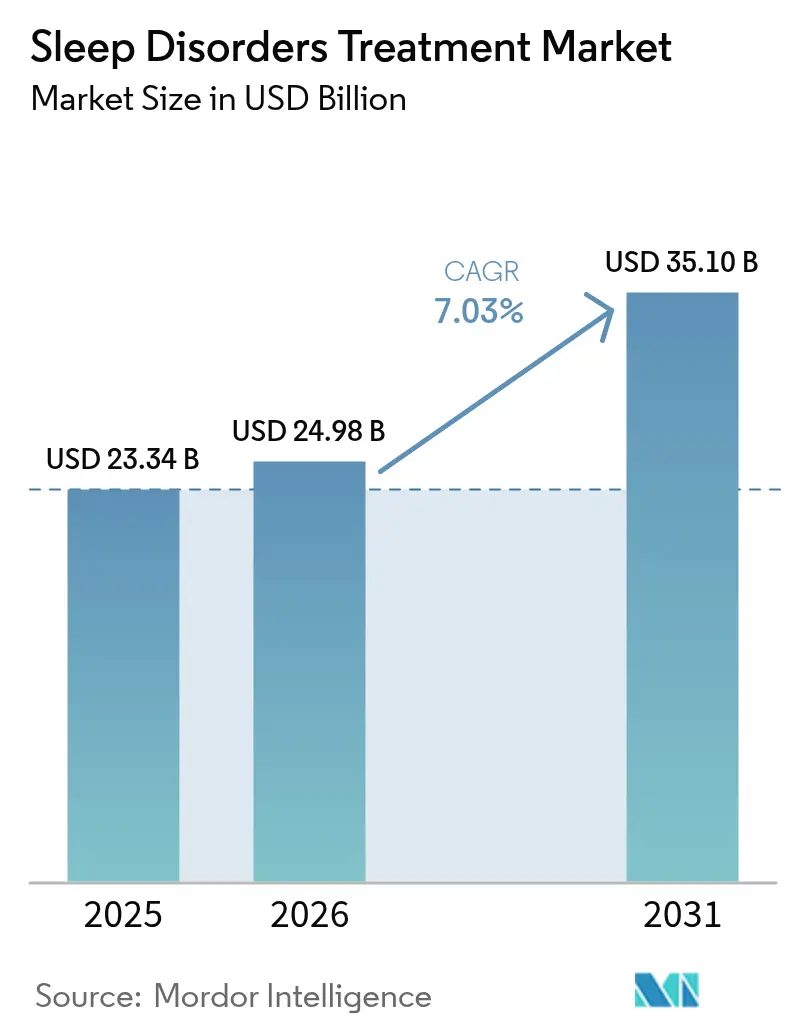

| Market Size (2026) | USD 24.98 Billion |

| Market Size (2031) | USD 35.1 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sleep Disorders Treatment Market Analysis by Mordor Intelligence

The sleep disorder treatment market size was valued at USD 23.34 billion in 2025 and estimated to grow from USD 24.98 billion in 2026 to reach USD 35.10 billion by 2031, at a CAGR of 7.03% during the forecast period (2026-2031). Rising prevalence of insomnia, obstructive sleep apnea (OSA) and narcolepsy in both advanced and emerging economies, coupled with breakthrough pharmacology such as dual-orexin receptor antagonists (DORAs) and the December 2024 approval of tirzepatide for OSA, underpin sustained revenue growth. Digital health integration is widening patient reach through AI-enabled diagnostics and adherence monitoring while reimbursement reforms are pulling digital therapeutics such as SleepioRx into mainstream care pathways. Competitive intensity is rising as device leaders like ResMed face pharmaceutical challengers that now offer first-in-class metabolic agents and next-generation hypnotics. At the same time, consumer demand for convenient purchasing options is shifting prescription volumes toward online pharmacies, reinforcing omnichannel strategies across the entire sleep disorder treatment market.

Key Report Takeaways

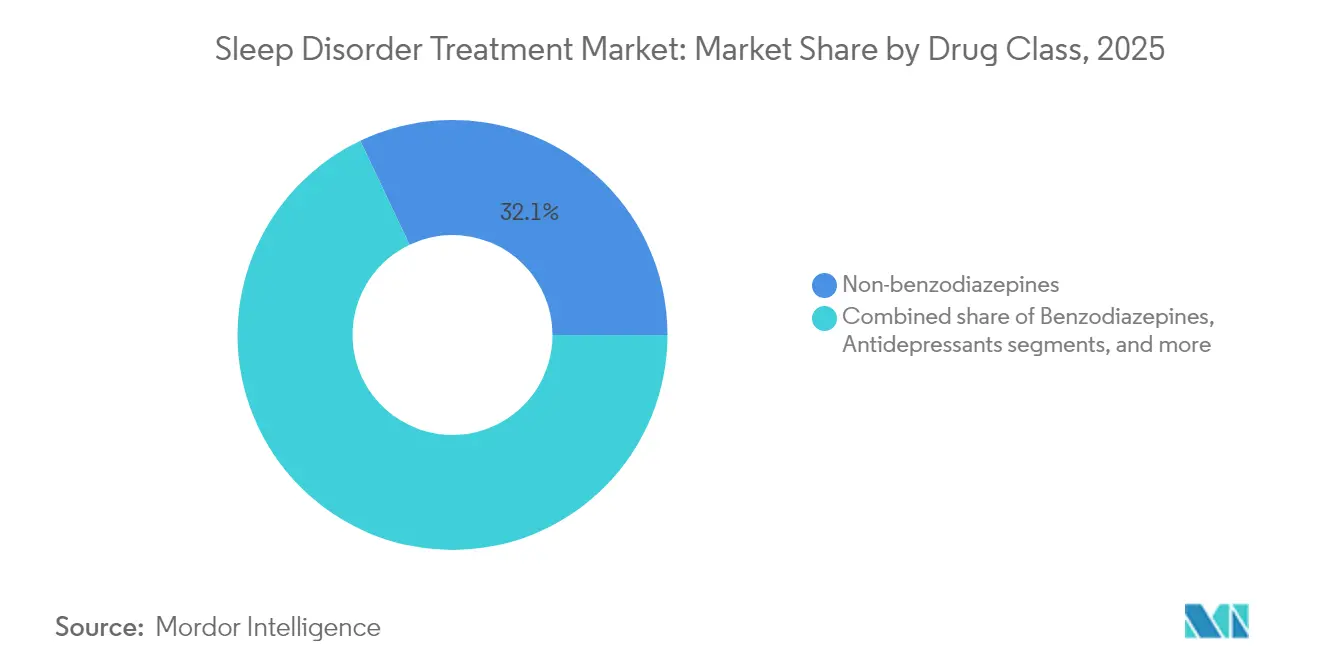

- By drug class, non-benzodiazepines led with 32.06% revenue share in 2025, while DORAs are projected to expand at a 9.52% CAGR through 2031.

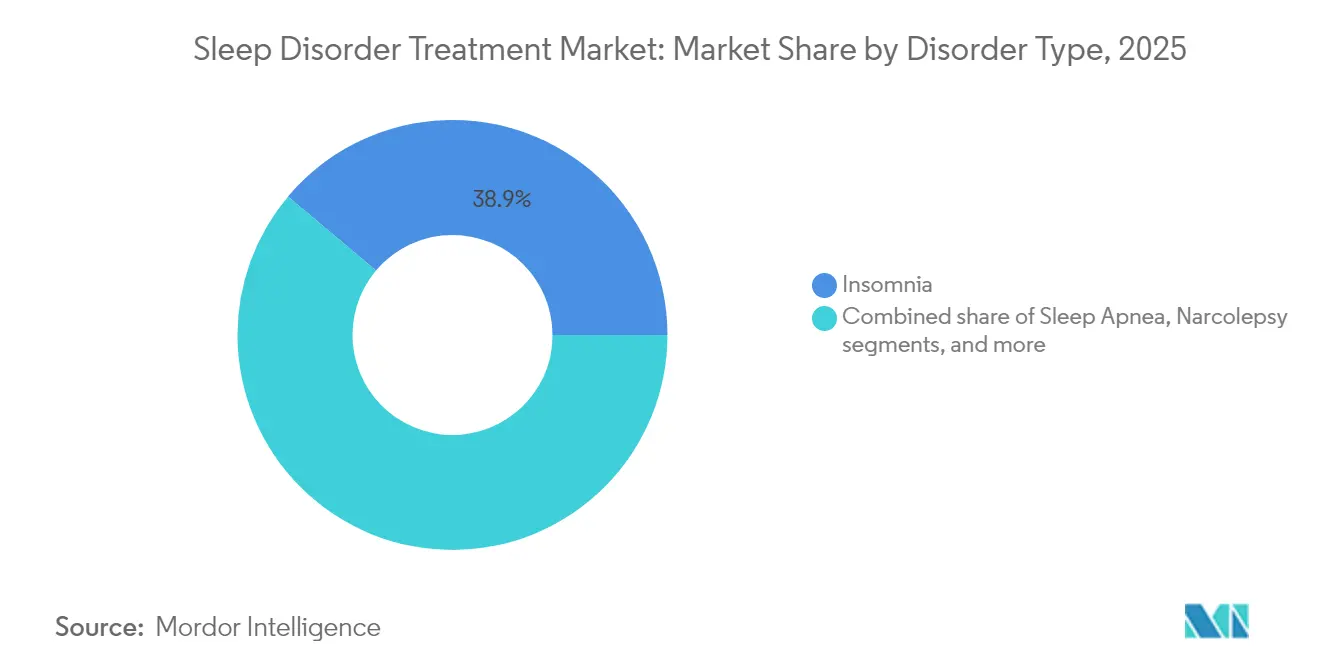

- By disorder type, insomnia dominated with 38.86% of the sleep disorder treatment market share in 2025; narcolepsy therapies hold the fastest trajectory at a 9.78% CAGR to 2031.

- By distribution channel, retail pharmacies retained 41.98% share of the sleep disorder treatment market size in 2025, whereas online pharmacies are advancing at a 10.18% CAGR through 2031.

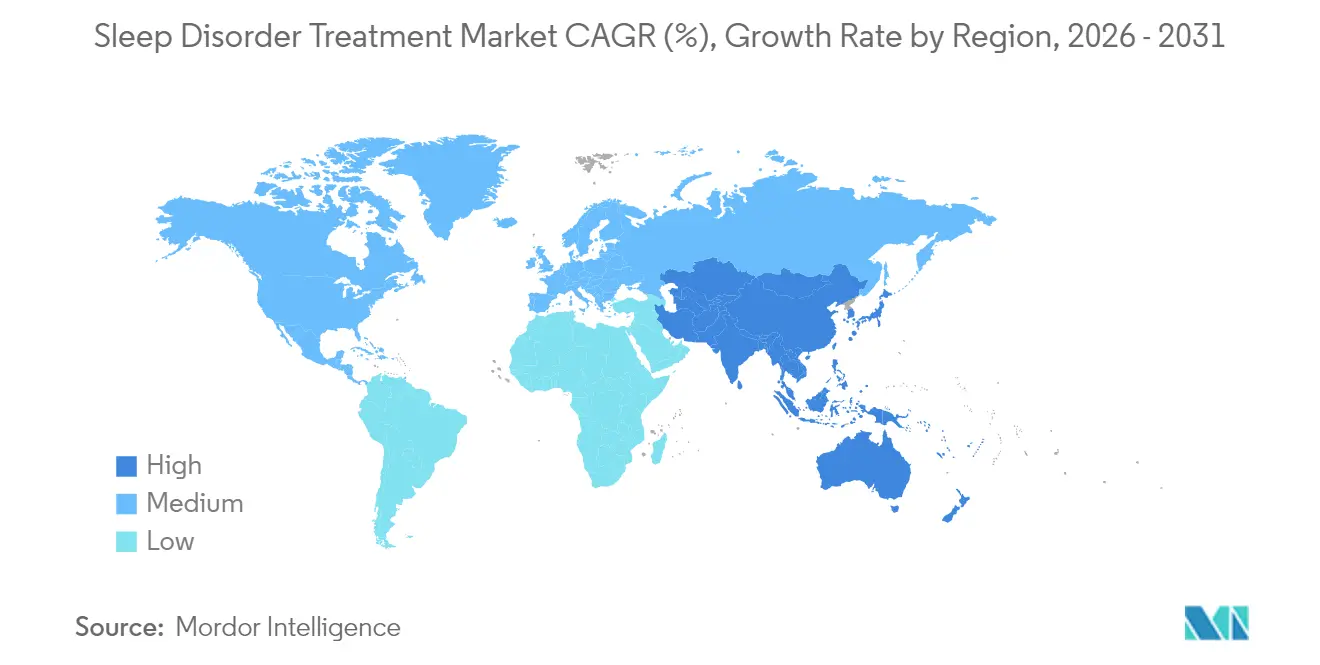

- By geography, North America captured 42.35% of the sleep disorder treatment market in 2025; Asia-Pacific is forecast to grow at an 8.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sleep Disorders Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global burden of insomnia & OSA driven by ageing, obesity and mental-health stressors | 1.80% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Enhanced screening and public-awareness programs accelerating diagnosis rates | 1.20% | APAC core; spill-over to MEA | Medium term (2-4 years) |

| Launch of novel pharmacological classes expanding therapeutic options | 2.10% | North America & EU; expanding to APAC | Short term (≤ 2 years) |

| Continuous innovation in device-based & digital therapeutics improving outcomes | 1.50% | Global; early adoption in developed markets | Medium term (2-4 years) |

| AI-powered sleep-data analytics enabling earlier personalised interventions | 0.90% | North America & EU | Long term (≥ 4 years) |

| Employer and insurer-led sleep-wellness initiatives widening reimbursement | 0.70% | North America; expanding to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Insomnia & Sleep Apnea Driven by Ageing, Obesity and Mental-Health Stressors

An estimated 30 million to 90 million Americans live with OSA, yet only 6 million have been formally diagnosed, illustrating a deep pool of untreated need that sustains the sleep disorder treatment market. The obesity epidemic intensifies OSA incidence, and December 2024 FDA clearance of tirzepatide created the first pharmacologic pathway for obese OSA patients, linking metabolic control to respiratory improvement[1]U.S. Food and Drug Administration, “Zepbound (tirzepatide) Approved for Obstructive Sleep Apnea,” fda.gov. Pandemic-era anxiety and depression elevated chronic insomnia across every major region, with DORAs showing 87.5% response rates in psychiatric populations and reinforcing clinician confidence in newer mechanisms. ResMed now monitors 28 million cloud-connected devices and captures 20 billion nights of sleep data that feed proprietary AI engines, scaling personalised therapy adjustments in real time. Among older adults, preference is shifting to non-invasive, digitally delivered programs such as SleepioRx—cleared by FDA in August 2024—which reduce pill burden while maintaining durable efficacy.

Enhanced Screening and Public-Awareness Programs Accelerating Diagnosis Rates

System-wide screening protocols are raising detection in primary care and consumer settings. Samsung’s collaboration with Stanford Medicine embeds algorithmic sleep-apnea screening in smartphones, signalling a move from laboratory polysomnography to home-based triage. In February 2024 the FDA cleared EnsoData’s pulse-oximetry AI platform, enabling lower-cost identification of OSA risk in resource-limited environments. Japan’s first insomnia drug approval in a decade—QUVIVIQ in September 2024—followed national media campaigns that highlighted untreated sleep disorders affecting 20% of adults and spurred physician education. Start-ups such as Sleep Cycle launched clinical studies in June 2025 to validate smartphone-based apnea screening, potentially reaching rural communities lacking specialty clinics. FDA clearance of ResMed’s NightOwl home test adds medical-grade support to direct-to-consumer pathways, shortening time-to-therapy and expanding the sleep disorder treatment market.

Launch of Novel Pharmacological Classes Expanding Therapeutic Options

DORAs represent the most consequential advance in sleep pharmacotherapy since benzodiazepines. Daridorexant, lemborexant and suvorexant consistently demonstrate fewer complex sleep behaviours and less next-day impairment than Z-drugs, as shown in FDA Adverse Event Reporting System analyses. China’s May 2025 approval of DAYVIGO (lemborexant) opens an addressable base of 172.5 million adult insomnia patients, illustrating the scale of opportunity when safety concerns are mitigated. Next-generation agonists are moving swiftly: Takeda’s oveporexton produced significant Phase 2b gains in narcolepsy type 1, while Alkermes’ alixorexton targets idiopathic hypersomnia in Phase II/III trials[2]Takeda Pharmaceutical Company, “Oveporexton Phase 2b Data Published,” takeda.com. The pipeline further includes seltorexant, an orexin-2 antagonist positioned for major depressive disorder with co-morbid insomnia, blurring traditional indication boundaries and enlarging the sleep disorder treatment market footprint. High compliance rates—87% in long-term cohorts—underscore the clinical goodwill earned by these agents, driving formulary inclusion and insurer acceptance.

Continuous Innovation in Device-Based and Digital Therapeutics Improving Outcomes & Adherence

Device developers are redefining adherence, historically the Achilles heel of CPAP therapy. In February 2024 the FDA cleared Neurovalens’ Modius Sleep, a head-worn neuromodulator that influences circadian centres without pharmaceuticals and delivers measurable gains in sleep efficiency within six weeks. Researchers at University of Cincinnati introduced VortexPAP, which stabilises airway pressure without a tight facial interface, promising relief for users who abandon conventional masks. Digital therapeutics command growing mindshare: SleepioRx’s cognitive-behavioural algorithm achieves healthy-sleep benchmarks in 76% of users, validating non-drug pathways that reduce adverse-event liabilities. Implantables are broadening choices for CPAP-intolerant cohorts, with Nyxoah’s Genio tongue stimulator gaining its first UK use case in December 2024 and leveraging Bluetooth control for patient-tailored therapy. Real-time data streaming from ResMed’s AirSense line reached 87% compliance when automated coaching was layered onto nightly data dashboards, showcasing how AI can convert raw signals into behaviour change that sustains the sleep disorder treatment market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns & dependency risks tied to long-term hypnotics | -0.80% | Global; highest scrutiny in EU & North America | Long term (≥ 4 years) |

| High cost of branded drugs & advanced devices limiting access in LMICs | -1.10% | APAC emerging markets, MEA, Latin America | Medium term (2-4 years) |

| Poor patient adherence to CPAP therapy and behavioural regimens undermining efficacy | -0.90% | Global; pronounced in North America & Europe | Medium term (2-4 years) |

| Boom in unregulated OTC/nutraceutical sleep aids diverting patients from evidence-based care | -0.60% | Global; rising in North America & APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety Concerns and Dependency Risks Associated with Long-Term Hypnotic Pharmacotherapy

Regulators are tightening oversight of traditional hypnotics, curbing label expansions and encouraging safer alternatives. In March 2024 the FDA issued a complete-response letter to Vanda’s HETLIOZ jet-lag supplement, signalling unwillingness to tolerate vague benefit-risk profiles in sleep medicine[3]Federal Register, “Complete Response Letter for HETLIOZ,” federalregister.gov. Benzodiazepines and Z-drugs continue showing higher incidences of complex behaviours such as sleep-driving, prompting guideline revisions that prioritise non-pharmacologic or DORA-based approaches. American Academy of Sleep Medicine 2024 guidance on restless-legs syndrome substitutes calcium-channel ligands for dopamine agonists to cut impulse-control disorders and augmentation risks. Real-world data confirm daridorexant’s lower serious adverse-event frequency; regulators across North America, Europe and APAC cite these findings when green-lighting wider indications. In parallel, auricular vagus-nerve stimulation has produced clinically meaningful sleep-quality gains without pharmacology, offering a drug-free refuge for risk-averse patients and reinforcing diversification within the sleep disorder treatment market.

High Cost of Branded Drugs and Advanced Devices Limiting Access in Low- and Middle-Income Regions

Pricing remains a formidable barrier beyond high-income markets. DORAs maintain premium positioning and have limited generic competition, making them aspirational therapies in South Asia and Sub-Saharan Africa despite strong clinical performance. Cloud-connected CPAP systems from ResMed demand capital outlays plus subscription fees that exceed average monthly income in many LMICs, curbing volume penetration although technical superiority is recognised. Insurance gaps aggravate disparity; Medicare debates on covering tirzepatide for OSA highlight how reimbursement policy drives real-world uptake, yet analogous coverage does not exist in most emerging economies. Online pharmacies soften price friction by boosting generic visibility; the global e-pharmacy sector touched USD 98.8 billion in 2022, though controlled-substance rules complicate cross-border fulfilment. Public systems can offset cost hurdles, illustrated by the UK National Health Service offering Sleepio without charge, a precedent that could be replicated in other tax-funded health models if robust cost-effectiveness evidence becomes available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: DORAs Challenge Traditional Hypnotic Dominance

Non-benzodiazepines held 32.06% of the sleep disorder treatment market in 2025 as clinicians balanced familiarity with improved safety over benzodiazepines. Despite that anchor, DORAs are growing at 9.52% CAGR and are forecast to erode historical share as guidelines elevate orexin-based therapy to first-line status for chronic insomnia. Real-world pharmacovigilance confirms fewer residual cognitive effects and lower dependency signals, a combination that encourages payers to include DORAs on preferred tiers, thereby reinforcing volume growth within the sleep disorder treatment market.

Second-line classes remain relevant. Benzodiazepines are preserved for acute, severe insomnia when rapid onset is critical, though physicians now cap prescription lengths to mitigate dependence. Off-label antidepressants satisfy complex insomnia with comorbid mood disturbance, while melatonin receptor agonists dominate paediatric niches where neurodevelopmental safety outweighs speed. Pipeline momentum stays concentrated in orexin biology: Takeda’s oveporexton and Alkermes’ alixorexton promise once-daily oral dosing that could simplify current multi-dose oxybate regimens. These forces together keep the sleep disorder treatment market size for pharmacologic segments on a durable expansion path through 2031.

By Disorder Type: Narcolepsy Treatments Drive Innovation Pipeline

Insomnia disorders represented 38.86% of the sleep disorder treatment market size in 2025 owing to ubiquitous lifestyle, psychiatric and circadian contributors. Penetration of digital interventions such as SleepioRx and increasing employer wellness programmes signal that insomnia will remain the anchor indication; however, growth moderates as non-drug approaches divert some volume from legacy hypnotics. The December 2024 tirzepatide approval reshaped OSA management, creating the first drug-based alternative to CPAP and unlocking cardiometabolic-oriented care pathways that accelerate integrated management of obesity and sleep breathing disorders.

Narcolepsy accounts for a smaller base but rises fastest at 9.78% CAGR. Advancements in orexin-2 agonism address the fundamental neurochemistry deficit rather than symptom suppression, enticing venture and strategic capital even amid broader biotech volatility. FDA’s October 2024 nod for paediatric sodium oxybate broadened the treated population, while Avadel’s once-nightly LUMRYZ, granted seven years of orphan exclusivity, signals regulatory encouragement of differentiated formulations. These factors collectively ensure narcolepsy’s outsized contribution to incremental revenue inside the sleep disorder treatment market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Retail pharmacies maintained 41.98% share in 2025, leveraging in-person counselling, immediate fulfilment and broad insurer networks. High foot-traffic locations ensure consistent prescription volume, especially for chronic therapy refills. Hospital and sleep-clinic pharmacies anchor complex cases requiring titration of high-risk agents or synchronous device setups, yet they face capacity limits that incentivise remote models.

Online pharmacies are scaling at a 10.18% CAGR, benefitting from privacy, home delivery and transparent pricing that appeal to working-age adults managing chronic insomnia or OSA. Telehealth-based verification bridges regulatory compliance, and insurers increasingly reimburse virtual visits, shrinking friction further. Sunrise’s December 2024 acquisition of Dreem Health illustrates vertical integration of diagnostic wearables and digital care platforms, enabling entire diagnosis-to-dispense journeys to stay in-app and boosting lifetime engagement metrics. As a result, channel shifts will redistribute margins but expand overall access, fortifying the sleep disorder treatment market over the forecast horizon.

Geography Analysis

North America commanded 42.35% of the sleep disorder treatment market in 2025, supported by sophisticated payer systems that fast-track breakthrough therapies and by high public awareness of sleep’s impact on cardiometabolic health. FDA approvals for tirzepatide and multiple DORAs exemplify the regulator’s openness to novel mechanisms. Employer-driven wellness benefits, including subsidised Sleepio licences and CPAP subscription models, are normalising proactive sleep management. ResMed’s Q3 FY2025 revenue climbed 8% to USD 1.3 billion, reflecting robust demand for cloud-connected devices that integrate with electronic health-record workflows, thereby reinforcing adherence and reducing downstream hospitalisations.

Asia-Pacific is the fastest rising territory at 8.22% CAGR through 2031. China alone hosts 172.5 million insomnia sufferers, catalysing product localisation and broad-based formulary negotiations following DAYVIGO’s approval in May 2025. Japan’s September 2024 endorsement of QUVIVIQ broke a decade-long drought in novel insomnia therapies, sparking renewed clinician education campaigns and boosting prescription volume. South Korea’s Phase 3 daridorexant trial underscores regional regulatory momentum, while universities accelerate fundamental research, such as light-sensitive somnogen molecules under development at University of Tsukuba. Rising middle-class income and government initiatives to modernise sleep labs underpin sustained premium adoption, making Asia-Pacific the engine for volume and revenue expansion of the sleep disorder treatment market.

Europe maintains steady growth on the back of universal coverage and coordinated regulatory processes through the European Medicines Agency. Idorsia’s first-mover role with QUVIVIQ exploited EU-wide mutual recognition to build share before Merck’s Belsomra and Eisai’s Dayvigo entered, and public procurement emphasises price-volume agreements that favour drugs with proven safety and health-economic benefits. The UK National Health Service’s system-wide rollout of Sleepio free of charge exemplifies how digital therapeutics can penetrate large public systems and drive cost offsets, potentially unlocking similar models continent-wide. Multidisciplinary clinics such as Switzerland’s Sleep House Bern pilot fast triage pathways that could set new standards for European sleep-care delivery. Collectively, these trends keep Europe’s contribution to the sleep disorder treatment market resilient despite mature baseline adoption.

Competitive Landscape

The competitive landscape is moderately consolidated. ResMed anchors device leadership with 10.24% revenue share and an 11.27% year-on-year growth rate, propelled by a proprietary data lake encompassing billions of nightly usage records. This data fuels algorithm-guided pressure adjustments and patient-facing coaching, increasing device compliance to 87% relative to sub-60% industry norms. Such outcomes confer durable competitive advantage through payer contracts that link reimbursement to adherence performance.

Pharmaceutical innovators are challenging device incumbents by leveraging mechanistic advances. Idorsia, Takeda and Jazz Pharmaceuticals each allocated double-digit R&D budgets to orexin modulation technologies that can rival CPAP in certain phenotypes. Jazz’s USD 1.59 billion acquisition of Sumitomo’s late-stage narcolepsy asset in June 2025 signals escalating deal sizes as large-cap firms race to secure differentiated pipelines. Digital-first entrants such as Big Health forge alternative payor pathways; their SleepioRx product bypasses dispensing fees, eroding pharmacy channel margins while creating new data exhaust that payors value for population analytics.

Strategic alliances between consumer-electronics giants and academic centres, notably Samsung–Stanford for AI sleep-apnea detection, foreshadow cross-industry convergence that may redraw competitive boundaries. New players in metabolic medicine—Eli Lilly with tirzepatide, Novo Nordisk with semaglutide Phase 3 OSA studies—extend competition beyond traditional sleep firms. Pediatric indications represent open white space; Harmony Biosciences’ 24% planned revenue bump to USD 820–860 million in 2025 reflects momentum in niche populations and underscores opportunities for companies that can navigate orphan-drug pathways.

Sleep Disorders Treatment Industry Leaders

Eisai Co., Ltd.

Merck & Co.

Jazz Pharmaceuticals

Pfizer Inc.

ResMed Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Jazz Pharmaceuticals acquired global rights (ex-Japan/China/APAC) to Sumitomo Pharma’s late-stage sleep-disorder candidate in a USD 1.59 billion deal.

- May 2025: Eisai secured Chinese approval for DAYVIGO (lemborexant) for adult insomnia, addressing an estimated 172.5 million patient pool.

- May 2025: Takeda published positive Phase 2b results for oveporexton (TAK-861) in the New England Journal of Medicine, paving the way for Phase 3 studies in narcolepsy type 1.

- January 2025: Harmony Biosciences projected 2025 revenue of USD 820–860 million after preliminary 2024 sales of USD 714 million, outlining six Phase 3 programmes.

- December 2024: FDA approved Zepbound (tirzepatide) as first pharmacologic therapy for moderate-to-severe OSA in obese adults based on Phase III data showing large reductions in apnea events and body weight.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the sleep disorders treatment market as revenue generated from prescription drugs, approved devices, and clinically validated digital therapeutics used to diagnose or manage insomnia, obstructive sleep apnea, narcolepsy, restless-legs syndrome, circadian rhythm disruptions, and related conditions across 17 key countries. According to Mordor Intelligence, home-use testing kits and connected CPAP systems are counted once, at the manufacturer's selling price, while follow-up services are out of scope.

Scope exclusion: Direct-to-consumer wellness apps that are not cleared by regulators as medical devices are excluded.

Segmentation Overview

- By Drug Class

- Benzodiazepines

- Non-benzodiazepines

- Dual Orexin Receptor Antagonists

- Antidepressants

- Melatonin Receptor Agonists

- Other Drug Class

- By Disorder Type

- Insomnia

- Sleep Apnea

- Narcolepsy

- Circadian Rhythm Disorders

- Other Disorder Types

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Sleep Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts conducted interviews and short surveys with pulmonologists, neurologists, retail pharmacists, device distributors, and payor advisers across North America, Europe, and Asia-Pacific. Insights on therapy adherence, pricing shifts, and upcoming reimbursement revisions closed data gaps and validated secondary findings.

Desk Research

We begin each project by mapping the universe of publicly available evidence. Key inputs come from tier-one health agencies such as the CDC, NIH, WHO, EMA, and Australia's TGA, trade bodies like the American Academy of Sleep Medicine and the European Sleep Research Society, and customs shipment dashboards that reveal PAP device flows. Company 10-Ks, drug trial registries, peer-reviewed journals, and reputable media updates supply trend signals and launch timelines.

This stage is strengthened by Mordor Intelligence's access to paid databases, including Dow Jones Factiva for news velocity, D&B Hoovers for manufacturer revenues, and Questel for patent intensity, which help triangulate competitive footprints and pipeline risk.

The sources listed are illustrative; many additional publications and datasets were reviewed to round out the evidence stack.

Market-Sizing & Forecasting

A blended top-down build, rooted in prevalence statistics, diagnosed patient funnels, and treatment penetration, creates the first cut, which is then cross-checked with selective bottom-up roll-ups of leading drug and device revenues. Critical variables include apnea prevalence by BMI band, CPAP adherence decay, average selling price drift of DORAs, and e-pharmacy share expansion. Multivariate regression, supported by expert consensus on input trajectories, drives the 2025-2030 forecast. Assumptions are adjusted where bottom-up samples diverge beyond acceptable variance thresholds.

Data Validation & Update Cycle

Model outputs pass three filters: historical back-casting, peer-benchmark review, and anomaly flags triggered by quarterly market events. Analysts revisit outliers before sign-off. Reports refresh annually, with interim updates when material regulatory or launch events occur, ensuring clients receive the latest calibrated view.

Why Mordor's Sleep Disorders Treatment Baseline Commands Reliability

Published numbers on this market often differ because firms choose distinct product baskets, pricing ladders, and refresh cadences.

We acknowledge these divergences upfront and outline the typical causes so users can decide which estimate best serves their decision.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.34 B (2025) | Mordor Intelligence | - |

| USD 27.60 B (2024) | Global Consultancy A | Counts mattresses and consumer wearables, uses 2022 ASPs rolled forward |

| USD 30.46 B (2025) | Trade Journal B | Assumes universal reimbursement uptake and higher CPAP adherence |

| USD 19.88 B (2025) | Regional Consultancy C | Excludes digital therapeutics and DORA class drugs |

The comparison shows that scope breadth and pricing logic explain most disparities. By grounding every assumption in verifiable clinical use and transparent variables, Mordor Intelligence delivers a dependable baseline suited for strategic planning.

Key Questions Answered in the Report

What is the current size of the sleep disorder treatment market?

The market is valued at USD 24.98 billion in 2026 and is projected to reach USD 35.10 billion by 2031.

Which therapeutic class is growing the fastest?

Dual-orexin receptor antagonists are expanding at a 9.52% CAGR due to superior safety and efficacy.

How large is North America’s share of the sleep disorder treatment market?

North America accounts for 42.35% of global revenue, reflecting mature reimbursement systems and early adoption of innovative therapies.

Why are online pharmacies important to future growth?

Online channels are scaling at a 10.18% CAGR because they offer privacy, convenience and price transparency that resonate with working-age patients.

What makes tirzepatide significant for obstructive sleep apnea?

Approved in December 2024, tirzepatide is the first drug to treat moderate-to-severe OSA in obese adults, offering an alternative to device-based therapy.

Which region is expected to grow the fastest through 2031?

Asia-Pacific leads with an 8.22% CAGR, driven by large untreated populations and recent approvals of novel pharmacotherapies.

Page last updated on: