Europe Dental Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

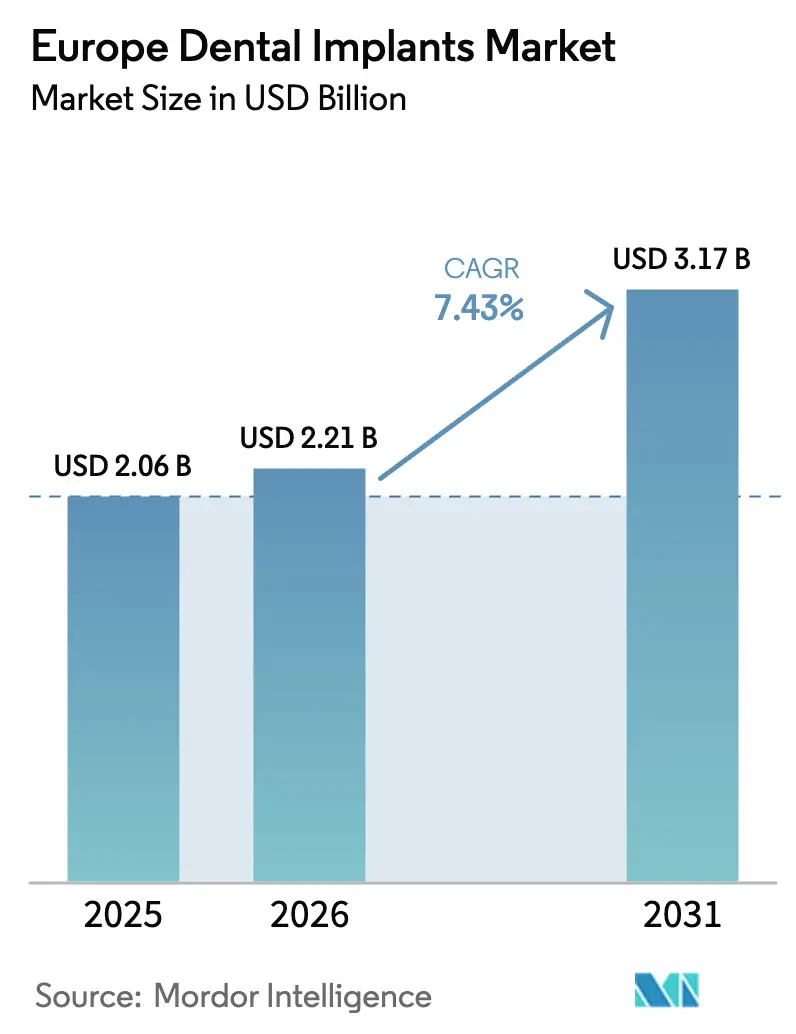

| Base Year Market Size (2025) | USD 2.06 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

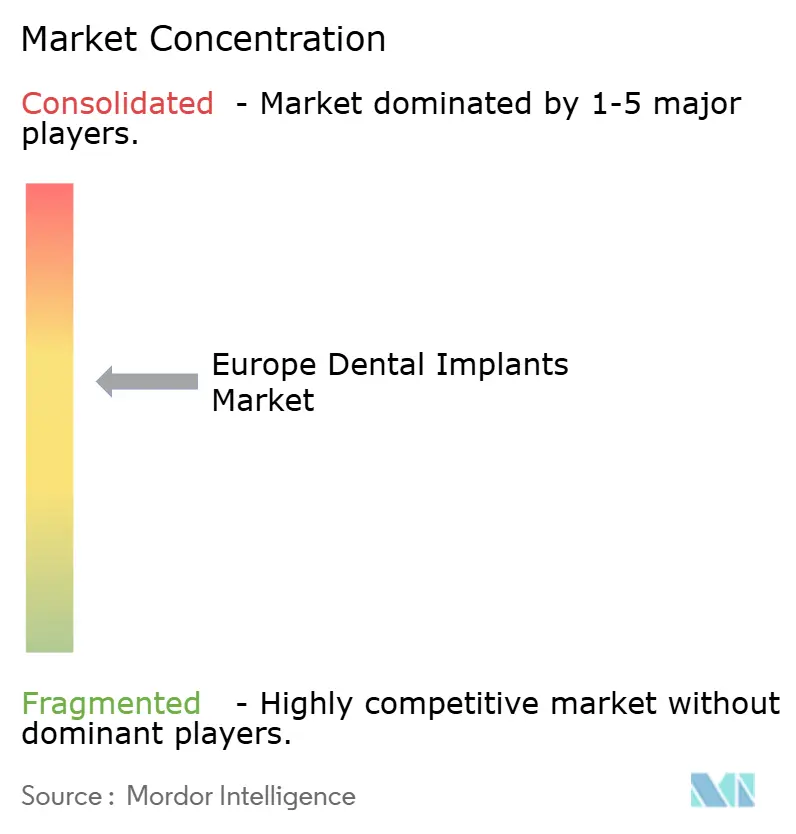

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Dental Implants Market Analysis by Mordor Intelligence

The Europe dental implants market size is expected to grow from USD 2.06 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 3.17 billion by 2031 at 7.43% CAGR over 2026-2031. Demand is fueled by an expanding elderly population that is retaining natural dentition for longer yet presenting with complex restorative needs, wider acceptance of digitally-enabled treatment workflows, and the rapid rollout of standardized clinical protocols by dental service organization (DSO) chains across Western Europe. Accelerated consolidation among practices is creating scale economies in procurement, training, and patient acquisition, which in turn lifts procedure volumes and shortens learning curves for new adopters. Simultaneously, value-segment implants priced 30-40% below premium systems are unlocking latent demand in cost-sensitive cohorts, especially in Southern and Eastern Europe, while the gradual inclusion of implant coverage in private dental policies further eases affordability constraints. On the supply side, manufacturers are intensifying investment in cloud-based planning platforms, intraoral scanning, and AI-supported design tools that collectively cut chair time by up to 50% and reduce remake rates, reinforcing the business case for clinics to adopt implants at scale.

Key Report Takeaways

- By country, Germany led with 27.12% of the Europe dental implants market share in 2025, whereas the United Kingdom is projected to expand at a 9.86% CAGR through 2031.

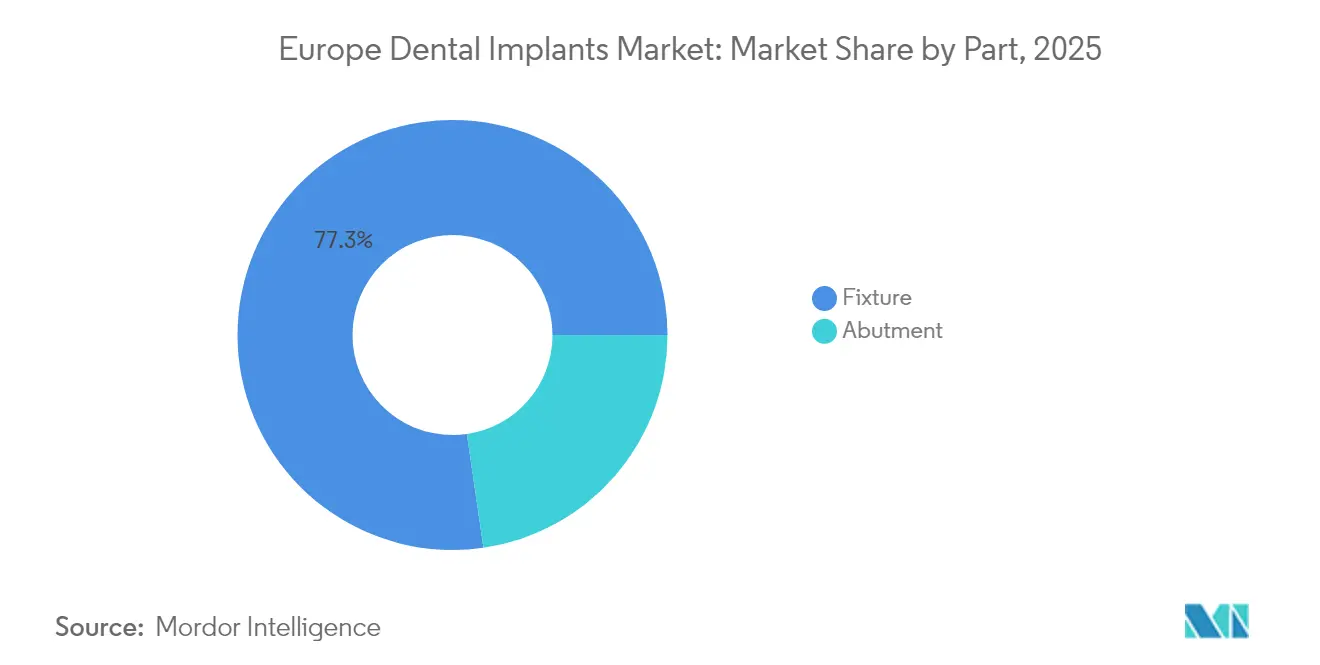

- By part, fixtures captured 77.30% revenue share in 2025; transosteal implants are forecast to grow at an 8.39% CAGR to 2031.

- By material, titanium held 84.35% of the 2025 Europe dental implants market size, while zirconium is advancing at an 10.98% CAGR through 2031.

- By procedure, two-stage systems accounted for 59.35% share in 2025, yet single-stage alternatives record the highest projected CAGR at 9.18% through 2031.

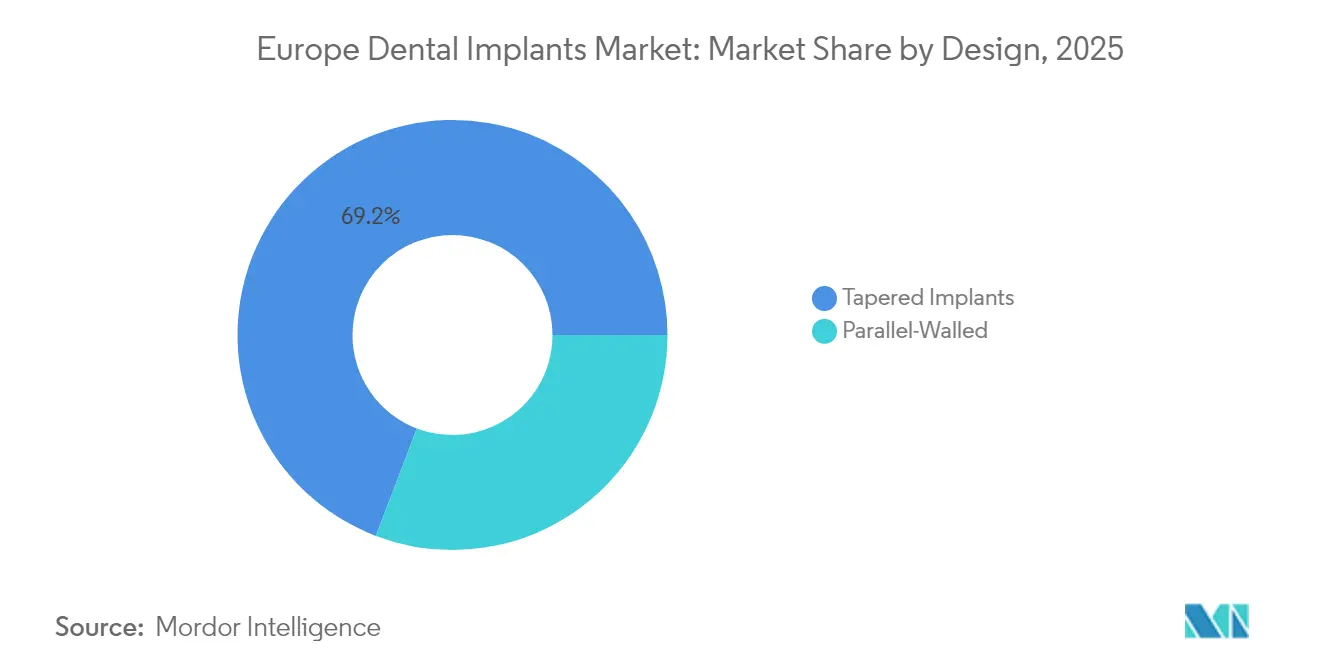

- By design, tapered variants commanded 69.20% share in 2025; parallel-walled implants are growing at an 7.92% CAGR through 2031.

- By price point, premium systems represented 64.10% of the Europe dental implants market size in 2025, but value implants are expected to accelerate at a 10.08% CAGR to 2031.

- By end-user, DSOs and independent clinics together controlled 67.80% share in 2025, while hospitals post a 8.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dental Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consolidation of DSO chains | +1.8% | Western Europe (DE, UK, FR) | Medium term (2-4 years) |

| Rising edentulous elderly population | +2.1% | Italy, Spain, Germany, France | Long term (≥ 4 years) |

| End-to-end digital workflows | +1.5% | Germany, UK, Nordics | Medium term (2-4 years) |

| Value-segment implants | +1.2% | Eastern & Southern Europe | Short term (≤ 2 years) |

| Growing private dental insurance coverage | +0.9% | UK, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of DSO Chains Standardizing Implant Protocols

Consolidation under large DSOs is transforming practice economics by unifying clinical pathways, negotiating volume-based supplier contracts, and rolling out proprietary education programs that accelerate general-dentist adoption of implants[1]Envista Holdings Corporation, “Leadership Appointments,” sec.gov. Straumann Group, for example, disclosed multiple framework agreements in Italy that guarantee minimum annual purchase volumes and joint-branding initiatives with leading chains. Such arrangements replace fragmented buying with centralized procurement, lowering per-unit implant costs by 15-20% and embedding brand loyalty early in a clinician’s career path. DSOs also leverage sophisticated marketing and financing packages that present implants as routine care rather than premium elective services, thereby widening patient conversion rates. As consolidation broadens from the Nordics into Germany, France, and Spain, DSO protocols are expected to set de facto clinical standards that expand the Europe dental implants market well beyond historical referral-based volumes.

Rising Edentulous Elderly Population Across Western & Southern Europe

Europe’s population aged 65 and above will rise from 147 million in 2025 to 171 million by 2035, with edentulism prevalence surpassing 30% in several Mediterranean countries. Oral disability increasingly links to nutritional insufficiency and cardiovascular comorbidities, prompting policymakers to position implants as part of healthy-aging strategies rather than purely cosmetic care. Italy already reports 12.8% complete tooth loss among seniors, and projections suggest a doubling of total edentulous cases by 2040, creating sustained procedure demand. Coupled with higher life expectancy, implants must now deliver 25-30 years of functional service, underpinning interest in long-term data and premium brands that justify lifetime value. Expanded reimbursement pilots in Germany and the UK for geriatric patients underscore this demographic-driven tailwind.

End-to-End Digital Workflows (Intraoral Scanners and Cloud Planning)

Workflows that integrate intraoral scanners, AI-assisted planning, and chairside milling reduce appointment counts by up to two visits and cut total treatment time nearly in half, an efficiency gain that resonates with both clinicians and patients. Straumann AXS and Nobel Biocare DTX Studio exemplify ecosystems that translate scan data into surgical guides within hours, raising placement accuracy and minimizing prosthetic adjustments. Evidence from in-vitro studies shows whole-arch deviation trimmed by 40% when AI algorithms refine point clouds before guide fabrication. The resulting predictability enables immediate-load protocols that shorten edentulous rehabilitation, directly lifting implant penetration.

Value-Segment Implants Boosting Penetration in Cost-Sensitive Cohorts

Implants priced 30-50% below premium brands are winning share in regions where household disposable income trails EU averages by 20% or more, such as Hungary, Poland, and Portugal. Straumann’s Anthogyr and Envista’s Alpha-Bio lines occupy this value tier, offering surfaces machined on legacy premium platforms yet marketed under distinct branding to avoid core cannibalization. Dental tourism has grown 14% annually into Budapest, where a full-arch case can cost EUR 5,500 (USD 6,280) versus EUR 11,000 (USD 12,560) in Germany, underpinning double-digit unit growth in the value segment. As clinical evidence narrows perceived performance gaps, value implants are anticipated to command one in three placements by the end of the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay for digital equipment | -0.7% | Southern & Eastern Europe | Short term (≤ 2 years) |

| Limited public reimbursement | -1.1% | Pan-Europe (especially UK, ES, IT) | Medium term (2-4 years) |

| Stringent EU-MDR 2027 evidence requirements | -0.9% | All EU member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay for Digital Implantology in Independent Clinics

Initial investment for a comprehensive digital setup, including scanner, planning software, and milling unit, sits between EUR 65,000-120,000 (USD 74,200-137,000) per operatory—an outlay that independent clinics struggle to amortize given average annual revenues under EUR 450,000 (USD 513,600) in Southern Europe. Surveys show 58% awareness of intraoral scanners among practitioners yet usage rates below 25% principally due to cost barriers and perceived lab incompatibility. The widening technology gap risks concentrating advanced procedures within DSO networks, indirectly capping regional procedure growth.

Limited Public Reimbursement for Elective/Aesthetic Implant Cases

Public insurance across most EU states reimburses only functional tooth replacement for extensive edentulism, leaving the majority of single-tooth and aesthetic indications fully self-funded. In Romania, privately funded care represents 90% of oral-health expenditure, and similar patterns persist in Spain and Italy, narrowing the payer pool to affluent patients or those with supplemental insurance. This reimbursement gap perpetuates socioeconomic disparities in access and limits upside in lower-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Part: Fixtures Reinforce Core Revenue as Transosteal Outpaces

Fixtures accounted for 77.30% of 2025 revenues within the Europe dental implants market, underpinning every restorative design from single crowns to full-arch bridges. Their dominance stems from indispensability and high material value relative to abutments or surgical guides. Transosteal implants, although small in absolute value, are progressing at an 8.39% CAGR, leveraged in atrophic mandibular cases where alternative anchorage is limited. Advanced thread geometries—most recently 5.5 mm depths generating insertion torque of 54 Ncm—improve stability in osteoporotic bone and extend the candidate pool among elderly patients. Over the forecast period, research-driven refinements such as micro-roughened apexes and bioactive coatings will elevate average selling prices, sustaining fixtures as the prime revenue engine of the Europe dental implants market.

Emerging surgical protocols now couple denser thread profiles with resonance-frequency analysis to tailor drilling speeds, enhancing immediate-load eligibility. At the same time, abutment innovation—ranging from pink-colored titanium dioxide to zirconia-titanium hybrids—improves peri-implant mucosal integration and aesthetics, indirectly supporting higher case acceptance. These enhancements consolidate the perception of fixtures as a technology category in constant evolution rather than a commoditized commodity, allowing manufacturers to defend margin even as unit volumes migrate toward the value tier.

By Material: Titanium’s Stronghold Faces Zirconium’s Aesthetic Pull

Titanium implants retained 84.35% share of the 2025 Europe dental implants market, backed by robust survival data spanning up to 30 years. Europe dental implants market size for titanium products is projected to reach USD 2.51 billion by 2031, reflecting a steady 6.32% CAGR in that material class. Zirconium, however, is scaling faster at 10.98% annually, buoyed by zero-metal optics and reduced galvanic corrosion risk, essential for anterior restorations and metal-sensitive patients. Survival rates between 55-100% underscore material viability, with newer one-piece designs exceeding 95% at five years. Manufacturers are investing in surface-roughening techniques using laser-microtexturing to enhance osseointegration, narrowing any clinical performance gap with titanium.

Regenerative dentistry research points to zirconia’s ability to attract a denser connective-tissue collar, potentially lowering late-stage peri-implantitis. As long-term data accrue, clinicians may adopt a material-agnostic approach, selecting titanium for posterior load-bearing sites and zirconia for high-smile-line zones, diversifying revenue sources for suppliers.

By Procedure Type: Single-Stage Momentum Builds Against Two-Stage Norm

Conventional two-stage techniques still command 59.35% share owing to perceived predictability, yet single-stage approaches are accelerating at 9.18% CAGR, the fastest within the procedure taxonomy. Immediate and early loading protocols rely on high primary stability metrics—ISQ ≥70 and torque ≥45 Ncm—now attainable with tapered macro-designs and hydrophilic surfaces. Europe dental implants market share for single-stage systems is expected to rise to nearly 47% by 2031, marking a structural pivot toward patient-centric speed. Meta-analyses indicate comparable survival between early and conventional loading, eroding clinician reservations and enabling higher chairside productivity.

Further expansion comes from digital navigational surgery, wherein guided osteotomies minimize micromotion, a key determinant of immediate-load success. Insurers exploring bundled payments favor single-stage protocols that shorten restorative cycles, potentially unlocking incremental reimbursement and further fueling adoption.

By Design: Tapered Dominance Modified by Parallel-Walled Precision

Tapered implants occupy 69.20% of placements by optimizing thread-to-bone contact in extraction sockets and narrow ridges, generating the high insertion torque vital for immediate loading. Yet parallel-walled cylinders, prized for uniform stress distribution in dense cortical zones, grow at 7.92% CAGR through 2031. Europe dental implants market size attributable to parallel-walled devices is forecast at USD 1.01 billion by 2031, reflecting widening surgeon familiarity and refined drilling protocols.

Studies show no significant stability differential at one-year follow-up; however, tapered implants exhibit marginally lower crestal bone loss, consolidating their leadership. Hybrid systems combining apical taper with a cylindrical coronal third are entering the market, promising versatile biomechanics suited to mixed bone densities.

By Price Point: Value Tier Scales as Premium Brands Reconfigure Portfolios

Premium implants held 64.10% share in 2025 on back of lifetime data and bundled digital ecosystems, though their CAGR moderates to 4.92%, lagging the overall Europe dental implants market. Conversely, value products expand at 10.08%, driven by economically diverse patient bases and heightened clinician price sensitivity amid inflationary pressures. Multi-brand strategies allow top suppliers to capture full spectrum demand without diluting flagship equity. For instance, Straumann’s Anthogyr and Osstem’s signature lines coexist across European distributors, each targeting distinct price-elasticity profiles.

Enhanced surface engineering borrowed from premium lines flows downstream after patent expirations, boosting clinical confidence in value implants and compressing perceived risk premiums. As a result, implant purchasing may mirror airline seat economics: a tiered portfolio satisfying both budget and premium preferences within the same practice.

By End-User: DSOs Sustain Volume Ramp While Hospitals Broaden Complexity

DSO-controlled and independent clinics represent 67.80% of procedures in 2025, reflecting dentistry’s primary care orientation. Hospitals, though smaller in share, log 8.98% CAGR, underpinned by integration of oral-maxillofacial departments and capacity to manage medically compromised patients, such as those on bisphosphonate therapy. Academic centers steer product innovation, exemplified by the University of Melbourne’s rectangular-block implant devised for ultra-thin mandibular crests. Digital registries under creation in Norway and Sweden will feed real-world data back to manufacturers, reinforcing evidence-based refinement in both hospital and clinic environments.

Geography Analysis

Germany anchors 27.12% of 2025 Europe dental implants market revenue, propelled by a dentist density of 85 per 100,000 inhabitants, twice the EU average, and by sophisticated insurance add-ons that subsidize functional implants. Continued growth remains steady but moderates as the market approaches maturity and competitive pricing narrows margins for premium brands. Despite saturation, advanced digital uptake and early adoption of new materials keep Germany a bellwether for technological diffusion across the continent.

The United Kingdom, fueled by post-Brexit regulatory agility and surging private dental plans, recorded the fastest regional CAGR of 9.86%, outpacing continental peers by more than 240 basis points. DSO penetration is accelerating, with large chains standardizing implant packages that combine financing and same-day placement options, broadening accessibility. Favorable demographic momentum—namely a rising working-age population prioritizing aesthetics—supports this outsized trajectory.

France, Italy, and Spain collectively represent roughly one-third of the Europe dental implants market, each shaped by distinct reimbursement structures. France benefits from partial social-security support for functional edentulism, sustaining a balanced premium-value mix. Italy, fragmented across north-south economic divides, demonstrates pockets of high adoption in Lombardy and Veneto, while Spain leverages dental tourism, particularly in Barcelona and Malaga, to attract pan-European patients seeking cost-effective full-arch solutions. The “Rest of Europe,” including Poland, Hungary, and the Nordics, offers disparate growth paths: Hungary leverages low procedure costs to lure patients from Austria and Germany, whereas Sweden exhibits near-saturation but pioneers registry-based outcome monitoring that will inform continental quality standards.

Competitive Landscape

Market leadership remains moderately concentrated: Straumann Group, Dentsply Sirona, and Nobel Biocare (Envista) together command a significant share, while Osstem and ZimVie comprise the next tier. Straumann increased its Europe dental implants market share from 32% in 2023 to roughly 35% in 2024, aided by accretive acquisitions, multi-brand segmentation, and deepening DSO alliances. Dentsply Sirona focuses on closed-loop digital ecology via its CEREC workflow, appealing to clinics seeking a single-vendor solution. Envista’s Nobel Biocare, under new leadership with former Colosseum Dental head Stefan Nilsson, is repositioning around “premium simplicity,” widening its price ladder while reinforcing the All-on-4 franchise.

Asian challengers Osstem and Dentium gain footholds in value-sensitive markets by offering comprehensive kits priced 30% below incumbents yet boasting CE marks and robust clinical libraries translated into multiple European languages. ZimVie differentiates with the TSX implant emphasizing primary stability across variable bone densities, seeking premium slots in immediate extraction protocols. Competitive vectors now pivot less on implant micro-geometry and more on cloud-based case planning, chairside workflows, and longitudinal data capture—areas where resource-rich leaders maintain advantage. Nonetheless, price competition within the mid-tier intensifies as DSOs exert purchasing leverage, compelling even premium brands to field secondary lines.

Europe Dental Implants Industry Leaders

Institut Straumann AG

Envista Holdings Corporation (Nobel Biocare)

Dentsply Sirona Inc.

Osstem Implant Co.

ZimVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: RevBio secured multi-country ethical approvals to commence a pivotal trial for its biomaterial that accelerates implant stabilization, a prerequisite for CE marking and European launch.

- March 2025: Mikrona Group acquired Dental Axess, integrating digital-dentistry expertise into its orthodontic equipment portfolio to broaden service offerings across DSO clients.

Europe Dental Implants Market Report Scope

As per the scope of the report, dental implants are artificial replacements for tooth roots that can be surgically inserted in the jawbone. The European dental implants market is segmented by part, material, and geography. By part, the market is segmented into fixtures and abutments. By fixture, the market is segmented into endosteal implants, subperiosteal implants, transosteal implants, and intramucosal implants. By material, the market is segmented into titanium implants and zirconium Implants. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. The report offers market size and forecasts for the European dental implants market in value (USD) for the above segments.

| Fixture | Endosteal Implants |

| Subperiosteal Implants | |

| Transosteal Implants | |

| Abutment |

| Titanium Implants |

| Zirconium Implants |

| Two-Stage Implants |

| Single-Stage Implants |

| Tapered Implants |

| Parallel-Walled Implants |

| Premium Implants |

| Value / Non-Premium Implants |

| Dental Clinics & DSOs |

| Hospitals |

| Academic & Research Institutes |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Part | Fixture | Endosteal Implants |

| Subperiosteal Implants | ||

| Transosteal Implants | ||

| Abutment | ||

| By Material | Titanium Implants | |

| Zirconium Implants | ||

| By Procedure Type | Two-Stage Implants | |

| Single-Stage Implants | ||

| By Design | Tapered Implants | |

| Parallel-Walled Implants | ||

| By Price Point | Premium Implants | |

| Value / Non-Premium Implants | ||

| By End-user | Dental Clinics & DSOs | |

| Hospitals | ||

| Academic & Research Institutes | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe dental implants market?

The market is valued at USD 2.21 billion in 2026 and is forecast to reach USD 3.17 billion by 2031.

Which material dominates implant placements in Europe?

Titanium accounts for about 84.35% of placements, although zirconium is growing faster at an 10.98% CAGR.

Why are DSO chains important to implant growth?

DSOs standardize protocols, negotiate bulk purchases, and provide in-house training, raising procedure volumes across their networks.

Which European country is expanding fastest in implant adoption?

The United Kingdom shows the highest CAGR at 9.86% through 2031, driven by greater private insurance coverage and DSO expansion.

How is digital dentistry affecting implant workflows?

Integrated scanning and cloud planning trim chair time by up to 50% and boost placement accuracy, encouraging wider clinician uptake.

Are value-segment implants affecting premium brands?

Yes, value implants expanding at 10.08% CAGR through 2031 are drawing cost-sensitive patients, prompting premium suppliers to launch multi-brand portfolios.

Page last updated on: