Cell-Free DNA Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.37 Billion |

| Market Size (2031) | USD 22.08 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

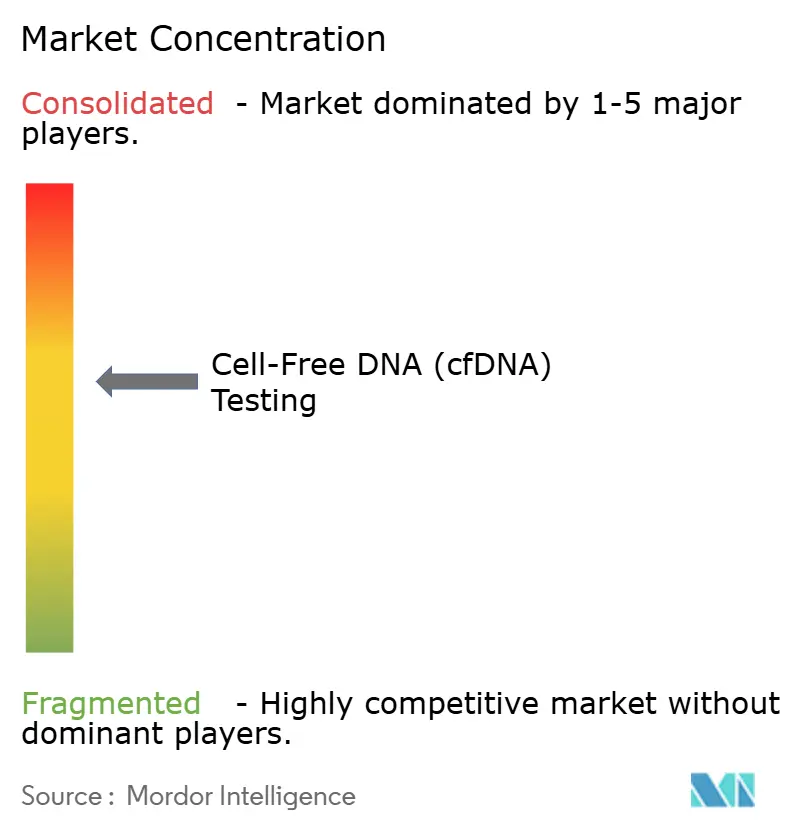

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell-Free DNA Testing Market Analysis by Mordor Intelligence

The global cell-free DNA testing market size in 2026 is estimated at USD 12.37 billion, growing from 2025 value of USD 11.01 billion with 2031 projections showing USD 22.08 billion, growing at 12.33% CAGR over 2026-2031. Universal non-invasive prenatal testing (NIPT) recommendations, lower sequencing costs, and landmark regulatory approvals such as the FDA nod for the Shield blood test have widened clinical acceptance.[1]Center for Devices and Radiological Health, “Shield – P230009,” fda.govOncology continues to anchor revenues, but transplant monitoring and multi-cancer early detection expand the clinical horizon as payer policies mature. Technology suppliers are translating research-grade platforms into diagnostic workflows, helping laboratories shorten turnaround times and improve sensitivity. At the same time, cyber-biosecurity safeguards and harmonised pre-analytic standards remain pivotal to sustaining clinician trust and payer confidence.

Key Report Takeaways

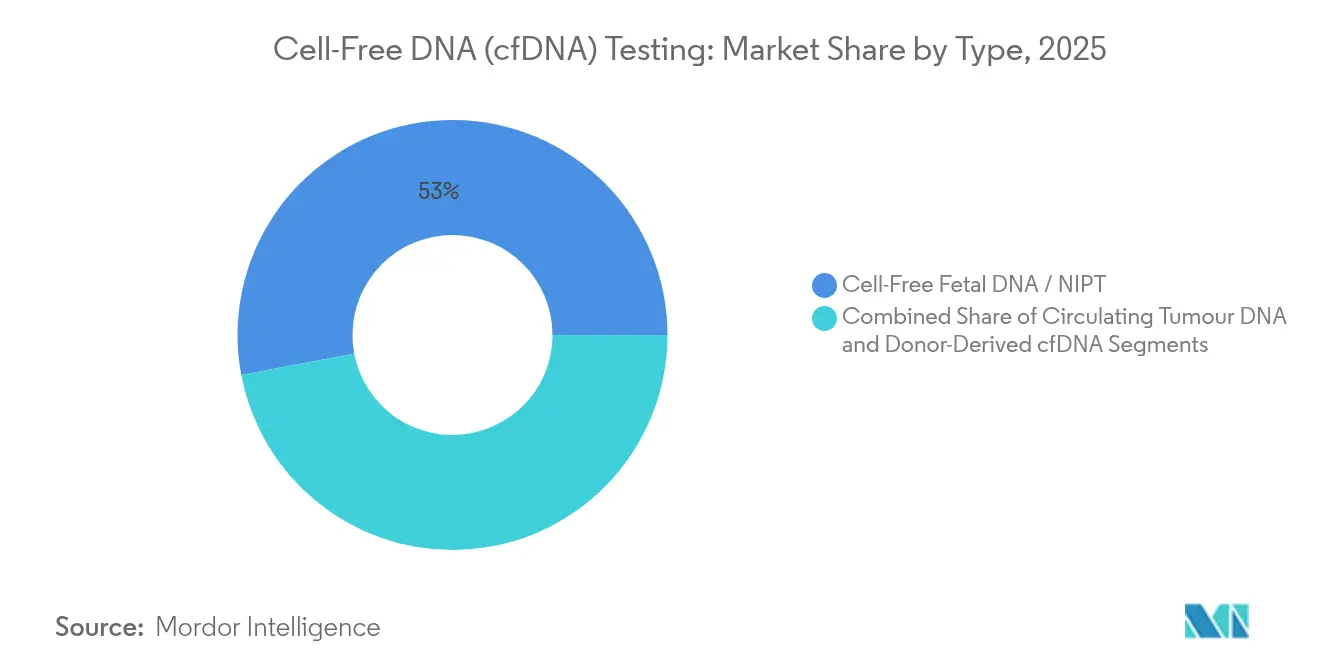

- By type, cell-free fetal DNA held 52.98% of the cell-free DNA testing market share in 2025, while donor-derived cfDNA is projected to grow at a 15.02% CAGR through 2031.

- By technology, massive parallel shotgun sequencing led with 43.92% revenue share in 2025; digital PCR is set to climb at a 14.35% CAGR to 2031.

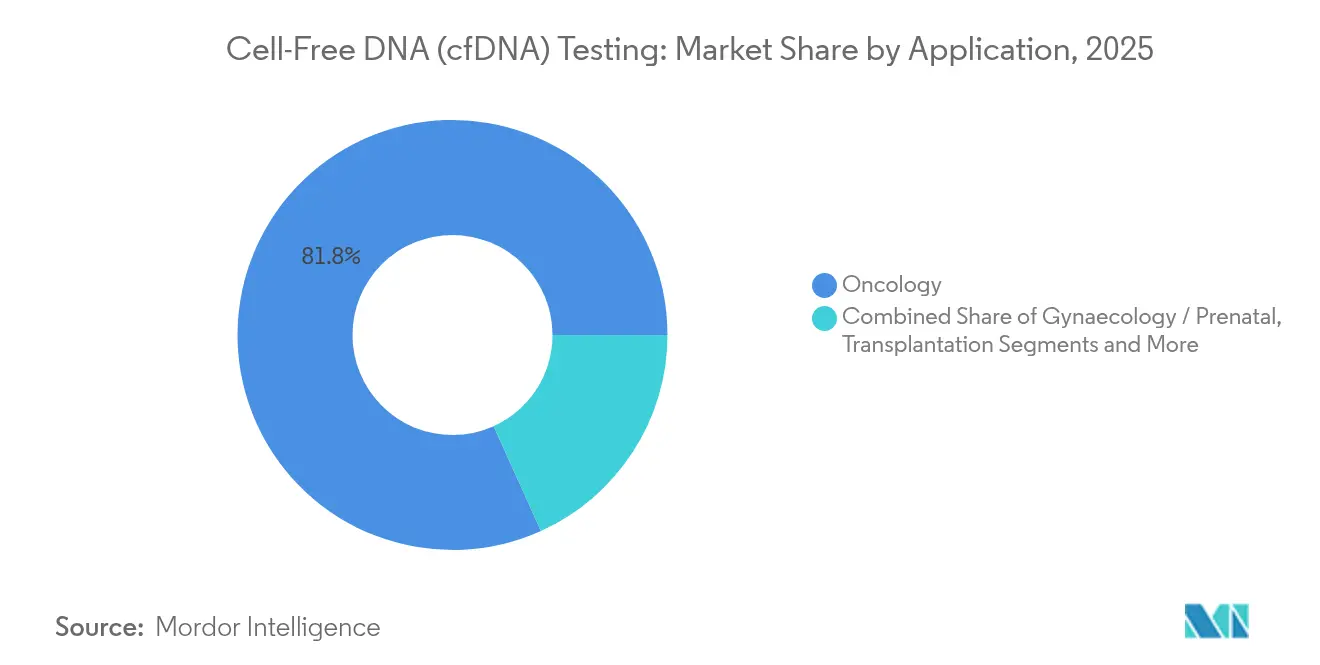

- By application, oncology accounted for 81.75% share of the cell-free DNA testing market size in 2025, whereas transplantation is poised for 15.95% CAGR over the forecast period.

- By end user, clinical laboratories captured 51.08% revenue in 2025; research and academic institutes post the quickest growth trajectory at 14.42% CAGR.

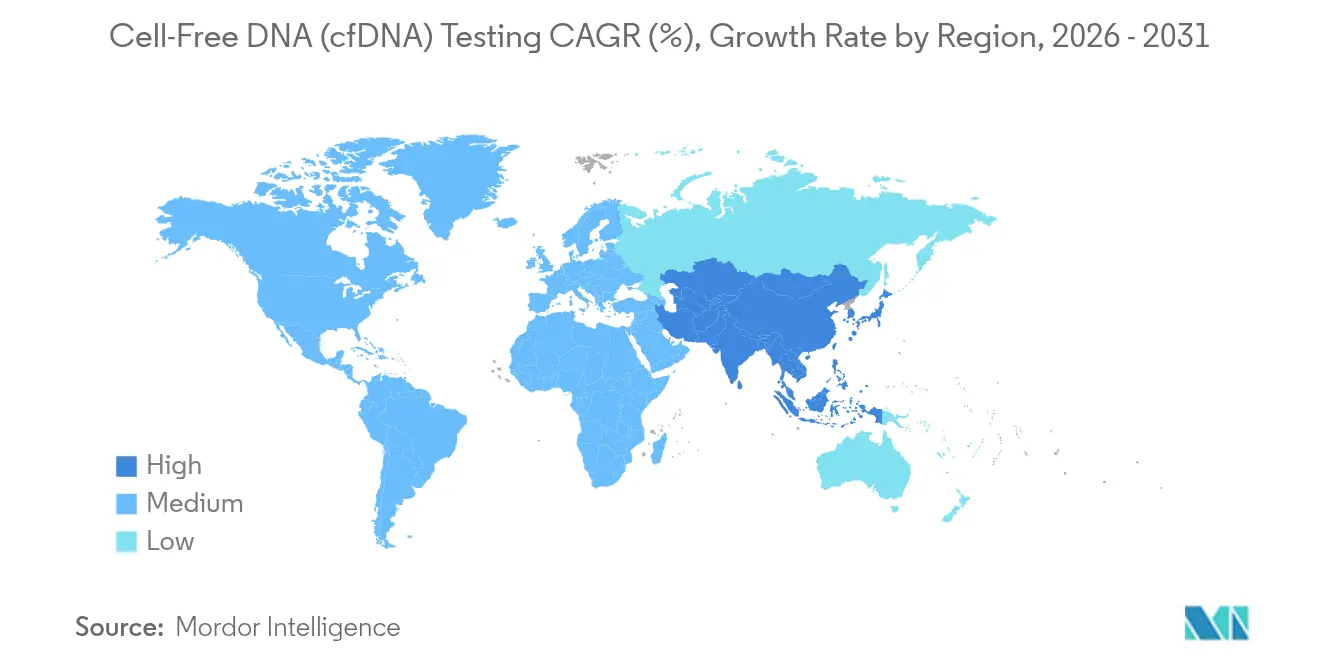

- By geography, North America commanded 47.96% of the cell-free DNA testing market in 2025, while Asia-Pacific advances at a 14.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell-Free DNA Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Universal NIPT becomes first-line prenatal screen | +2.1% | North America, Europe, gradually global | Short term (≤ 2 years) |

| Liquid biopsy integrated into routine oncology care | +3.2% | North America, Europe | Medium term (2-4 years) |

| Rapid fall in next-generation sequencing cost | +2.8% | APAC, emerging markets | Medium term (2-4 years) |

| Regulatory wave of cfDNA companion-diagnostic approvals | +1.9% | North America, Europe, expanding to APAC | Long term (≥ 4 years) |

| Long-fragment cfDNA enables tissue-of-origin mapping | +1.7% | Developed markets | Long term (≥ 4 years) |

| AI triage rescues non-reportable NIPT samples | +1.5% | High-volume laboratories worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Universal NIPT becomes first-line prenatal screen

Guidelines released by the American College of Obstetricians and Gynecologists remove age-based restrictions and elevate NIPT to a universal offering, expanding the testable population three- to fourfold in many developed countries. Detection rates for trisomy 21 reach 99.7% with a 0.04% false-positive rate, sharply outperforming serum screening. Health systems expect meaningful declines in invasive procedures, yet must update prior-authorisation workflows and counselling protocols to absorb higher front-end testing volumes.

Liquid biopsy integrated into routine oncology care

Medicare local coverage determinations now include at least one circulating tumor DNA (ctDNA) indication, and private insurers have broadened policies accordingly.[2]Michael P. Douglas, “Coverage Policies for ctDNA Tests,” jnccn.org ctDNA monitoring detects minimal residual disease months before imaging, enabling earlier therapeutic intervention. FDA clearance of a blood-based colorectal cancer screen sets a precedent for population-level applications that will diversify revenue streams and boost test volumes.

Rapid fall in next-generation sequencing cost

Whole-genome sequencing fell to roughly USD 600 in 2024 and is on course to approach USD 200-500 by 2026, lowering the economic barrier for cfDNA assays. Although consumables are cheaper, bioinformatics and quality-control still drive up to 70% of total cost, underscoring the need for efficiency gains in data analysis.

Regulatory wave of cfDNA companion-diagnostic approvals

The FDA reclassified DNA-based minimal residual disease tests as Class II devices, shortening review cycles and encouraging drug–diagnostic codevelopment.[3]U.S. Federal Register, “Classification of DNA-Based Test To Measure Minimal Residual Disease,” federalregister.gov Illumina’s TruSight Oncology Comprehensive kit exemplifies broad pancancer claims that could ignite new companion-diagnostic pipelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of harmonised pre-analytic standards | −1.8% | Global, more severe in emerging markets | Medium term (2-4 years) |

| Reimbursement gaps for multi-cancer early detection | −2.3% | Price-sensitive regions worldwide | Long term (≥ 4 years) |

| cfDNA cyber-biosecurity risks | −1.2% | Privacy-regulated regions | Short term (≤ 2 years) |

| Competition from low-cost serum or ultrasound screens | −0.8% | APAC, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of harmonised pre-analytic standards

Variations in collection tubes, processing times, and storage temperatures can triple cfDNA yield variability, eroding assay reproducibility. A nine-variant reference panel is a first step toward standardisation, yet adoption differs among laboratories.

Reimbursement gaps for multi-cancer early detection

Payers hesitate to fund broad screening in asymptomatic populations, citing cost-effectiveness uncertainties despite high specificity and moderate sensitivity metrics. Longitudinal outcome data and budget-impact models remain limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fetal Screening Leads while Transplant Gains Momentum

Cell-free fetal DNA retained 52.98% of 2025 revenues within the cell-free DNA testing market, buoyed by universal screening guidance and expansion into microdeletions and single-gene disorders. AI-driven bioinformatics cut redraw rates and improve laboratory efficiency, reinforcing the segment’s volume advantage. Circulating tumor DNA holds the next-largest slice, underpinned by reimbursement support for treatment monitoring. Donor-derived cfDNA, though a smaller contributor today, is forecast to expand at 15.02% CAGR. DEFINE-HT results showed cfDNA predicting heart-graft dysfunction three times better than biopsy, a milestone that propels transplant monitoring into mainstream care. The cell-free DNA testing market size for donor-derived assays is projected to widen rapidly as Medicare reaffirmed coverage, creating predictable reimbursement pathways.

Growing clinical confidence fuels uptake across kidney, heart, and lung transplants. Commercial offerings such as AlloSure Kidney and AlloSure Heart highlight favourable economics with USD 2,841 and USD 2,753 reimbursements, respectively. This financial certainty positions transplant monitoring to challenge prenatal screening’s dominance over the next decade.

By Technology: Sequencing Stronghold Meets Digital PCR Surge

Massive parallel shotgun sequencing secured 43.92% cell-free DNA testing market share in 2025 owing to broad genomic coverage and mature clinical validation. It remains indispensable for detecting structural variants and copy-number alterations. Nevertheless, digital PCR is charting a 14.35% CAGR, propelled by single-molecule sensitivity and absolute quantification advantages. A novel KRAS exon 2 drop-off assay reached 97.22% sensitivity and 100% specificity, illustrating clinical-grade performance.

Digital PCR’s streamlined workflow and affordable instrumentation open doors for smaller laboratories. Simultaneously, targeted sequencing keeps relevance in focused oncology panels, and emerging long-read sequencing illuminates methylation and fragmentomic signatures that short-read methods miss. The cell-free DNA testing market size allocated to digital PCR platforms is expected to accelerate on the back of heightened demand for rapid, cost-efficient monitoring.

By Application: Oncology Dominates yet Transplantation Accelerates

Oncology contributed 81.75% of 2025 revenue, reflecting entrenched use of ctDNA for therapy selection and disease surveillance. FDA guidance endorsing ctDNA endpoints in curative-intent drug trials further entrenches adoption. Despite this dominance, transplantation is the fastest-growing application at 15.95% CAGR, driven by evidence that cfDNA anticipates rejection earlier than biopsy. The cell-free DNA testing market size for transplantation is anticipated to reach meaningful scale by 2031 as payers align reimbursement with outcome advantages.

Gynecological and prenatal testing maintains steady demand thanks to universal NIPT, whereas infectious-disease and autoimmune applications remain nascent. Multi-cancer early detection, leveraging fragmentomics and methylation, represents a transformational yet reimbursement-constrained adjacency.

By End User: Laboratories Consolidate while Academia Expands

Clinical laboratories controlled 51.08% of 2025 revenue in the cell-free DNA testing market, benefiting from high-volume operations, established payer contracts, and CLIA-certified workflows. Consolidation trends gather pace as large networks integrate sequencing, digital PCR, and informatics. Research and academic institutes are growing at 14.42% CAGR, using cfDNA assays to support biomarker discovery and clinical trials.

Hospitals and birthing centres remain important but stable consumers; however, decentralised test kits such as AlloSeq are shrinking result times to 24 hours, making in-house testing economically feasible. As new applications surface, specialised laboratories and academic medical centres will capture early-stage testing before diffusing to reference labs.

Geography Analysis

North America commanded 47.96% of global revenue in 2025, reflecting FDA-approved assays, broad Medicare coverage, and sophisticated laboratory networks. The Shield colorectal cancer screen and AlloSure reimbursement rates illustrate payer willingness when clinical benefit is clear. Yet denial rates for genetic cancer tests rose to 27.4% in 2024, spotlighting evolving payer criteria and documentation demands.

Asia-Pacific is projected to register a 14.65% CAGR, the fastest worldwide. Expanding genomics infrastructure in China, India, and Southeast Asia enables laboratories to offer ctDNA tests that achieved 84.4% detection rates for recurrence in regional studies. Japan’s CIRCULATE program underscores governmental commitment to residual-disease research and adoption of whole-genome cfDNA assays.

Europe shows stable, moderate growth. National health systems facilitate uniform coverage, though market entry is complicated by divergent country-level regulations. Germany, France, and the United Kingdom lead utilisation, but smaller markets advance more slowly due to limited sequencing capacity.

South America and the Middle East & Africa remain emerging zones. Investment in tertiary care centres and public-private partnerships is expanding access to precision diagnostics, yet reimbursement and clinician awareness lag. Ultrasound and serum markers continue to dominate prenatal screening, slowing cfDNA penetration. The cell-free DNA testing market size across these regions will grow once economic scaling drives per-test costs down.

Competitive Landscape

The industry displays moderate consolidation. Illumina, Natera, and Guardant Health leverage extensive clinical evidence and regulatory know-how to defend share positions. Natera posted USD 502 million Q1 2025 revenue, up 37%, illustrating robust demand for its test portfolio. Illumina’s diagnostic-centric transition and collaboration with Tempus AI reflect a pivot from research to clinical revenue streams.

Strategic initiatives increasingly revolve around clinical trials that demonstrate actionable outcomes and payer savings. CareDx’s DEFINE-HT heart-transplant study validated donor-derived cfDNA as a superior predictor of rejection, reinforcing its transplant franchise. Companies also court pharmaceutical allies to co-develop companion diagnostics, a pathway eased by new FDA guidance.

White-space opportunities remain in multi-cancer screening and infectious-disease testing. Start-ups such as Oxford Nanopore advance long-read sequencing formats, while molecular diagnostics firms like BillionToOne extend panel breadth to cover additional hereditary disorders. As intellectual-property landscapes mature and cost curves fall, smaller innovators may capture niche applications before consolidation absorbs them.

Cell-Free DNA Testing Industry Leaders

Illumina, Inc.

F. Hoffmann-La Roche Ltd

Natera, Inc.

Thermo Fisher Scientific

Guardant Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BillionToOne launched an expanded UNITY Fetal Risk Screen covering five ACOG-recommended and nine additional recessive conditions.

- April 2025: Natera reported DEFINE-HT trial results showing Prospera Heart cfDNA predicts graft dysfunction three times better than biopsy.

- April 2025: Illumina partnered with Tempus AI to apply artificial intelligence across new cfDNA disease areas.

- March 2025: CareDx began commercial AlloSure testing for all pediatric heart transplant and simultaneous pancreas–kidney recipients.

Global Cell-Free DNA Testing Market Report Scope

Cell-free DNA testing analyzes non-cellular DNA in biological samples, primarily to identify genomic variants linked to hereditary or genetic disorders.

The Cell-free DNA (cf-DNA) testing market is segmented into type, technology, application, and geography. By type, the market is segmented into cell-free fetal DNA (NIPT), circulating tumor DNA, and donor-derived cell-free DNA. By technology, the market is segmented into massive parallel shotgun sequencing (MPSS), targeted massive parallel sequencing (t-MPS), and single nucleotide polymorphism (SNP). By application, the market is segmented into gynecology, oncology, transplantation, and others. The other applications includes infections, cardiovascular disease, and genetic abnormalities. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America. The report offers the value (in USD) for the above segments.

| Cell-Free Fetal DNA (NIPT) |

| Circulating Tumour DNA (ctDNA) |

| Donor-Derived cfDNA (Transplant) |

| Massive Parallel Shotgun Sequencing (MPSS) |

| Targeted MP Sequencing (t-MPS) |

| Single-Nucleotide Polymorphism (SNP) |

| Digital PCR / ddPCR |

| Gynaecology / Prenatal |

| Oncology |

| Transplantation |

| Infectious Disease & Others |

| Clinical Laboratories |

| Hospitals & Birthing Centres |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Cell-Free Fetal DNA (NIPT) | |

| Circulating Tumour DNA (ctDNA) | ||

| Donor-Derived cfDNA (Transplant) | ||

| By Technology | Massive Parallel Shotgun Sequencing (MPSS) | |

| Targeted MP Sequencing (t-MPS) | ||

| Single-Nucleotide Polymorphism (SNP) | ||

| Digital PCR / ddPCR | ||

| By Application | Gynaecology / Prenatal | |

| Oncology | ||

| Transplantation | ||

| Infectious Disease & Others | ||

| By End User | Clinical Laboratories | |

| Hospitals & Birthing Centres | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the cell-free DNA testing market?

The market stands at USD 12.37 billion in 2026 and is forecast to hit USD 22.08 billion by 2031, reflecting a 12.33% CAGR.

Which segment grows fastest in the cell-free DNA testing market?

Donor-derived cfDNA for transplant monitoring posts the quickest rise, advancing at a 15.02% CAGR through 2031.

Why are sequencing costs so important to market growth?

Sequencing now costs about USD 600 and is trending lower, making cfDNA assays affordable for more laboratories and driving wider clinical use.

How large is North America’s share of global revenue?

North America held 47.96% of global revenue in 2025, supported by FDA approvals and stable reimbursement.

What technologies are challenging massive parallel sequencing?

Digital PCR is gaining ground due to absolute quantification, high sensitivity, and lower capital costs, growing at 14.35% CAGR.

What is the main reimbursement hurdle for multi-cancer early detection?

Payers require long-term cost-effectiveness evidence before fully covering asymptomatic population screening, delaying widespread uptake.

Page last updated on: