Solder Paste Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solder Paste Market Analysis by Mordor Intelligence

The Solder Paste Market size is projected to expand from USD 1.91 billion in 2025 and USD 1.97 billion in 2026 to USD 2.32 billion by 2031, registering a CAGR of 3.32% between 2026 and 2031. Adoption of lead-free alloys, miniaturization of surface-mount components, and the rapid scale-up of electric-vehicle power-electronics lines are reinforcing steady volume gains across the solder paste market. Stricter RoHS timelines in the European Union, coupled with China’s RoHS 2.0 inspections, are accelerating the transition toward both lead-free and halogen-free chemistries, pushing formulators to engineer wider reflow windows that still comply with volatile-organic-compound caps. Asia-Pacific remains the production epicenter, yet reshoring in Mexico and the United States is lifting North-American demand for high-reliability pastes qualified under International Automotive Task Force (IATF) 16949. At the same time, AI-enabled solder-paste inspection is trimming wastage by around 20%, shaving total consumable costs while lengthening stencil life at high-volume sites.

Key Report Takeaways

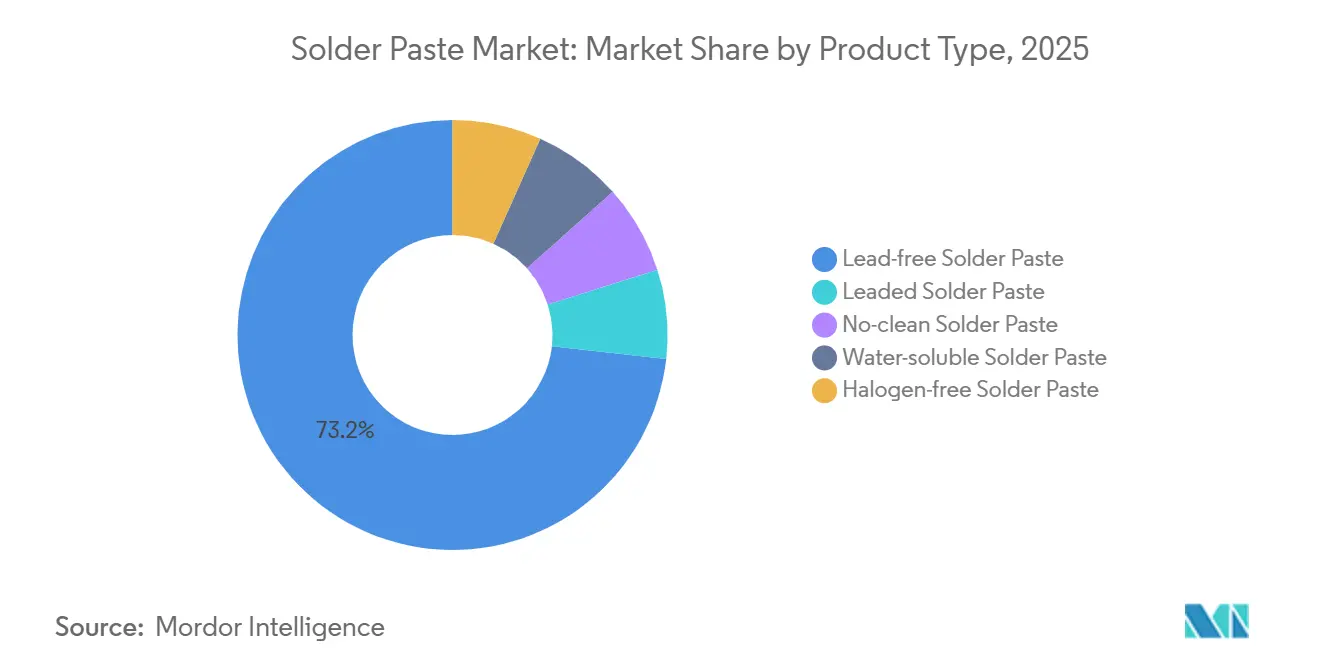

- By product type, lead-free solder paste captured 73.22% of the solder paste market share in 2025, while halogen-free solder paste is projected to grow at a 3.66% CAGR through 2031.

- By application, surface-mount technology accounted for 38.89% of the solder paste market share in 2025, while micro-electronics and advanced packaging is projected to grow at a 3.78% CAGR through 2031.

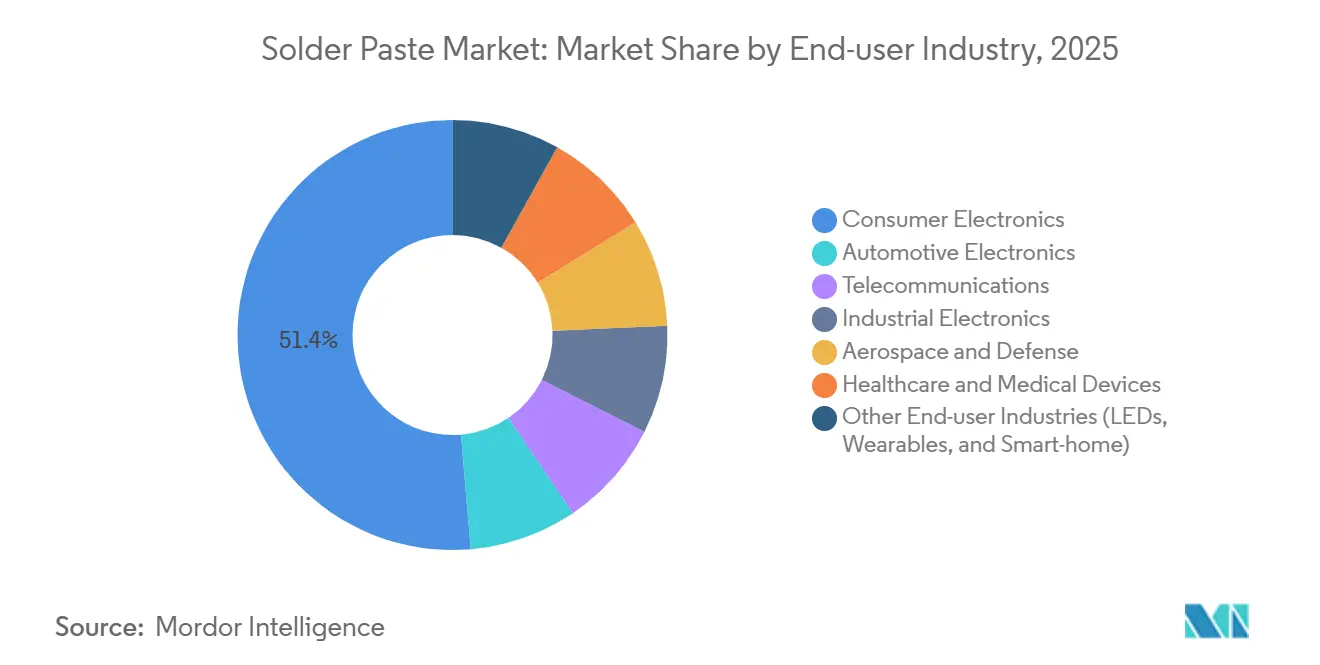

- By end-user industry, consumer electronics accounted for 51.35% of the 2025 solder paste market size, while automotive electronics is slated for a 9.03% CAGR to 2031.

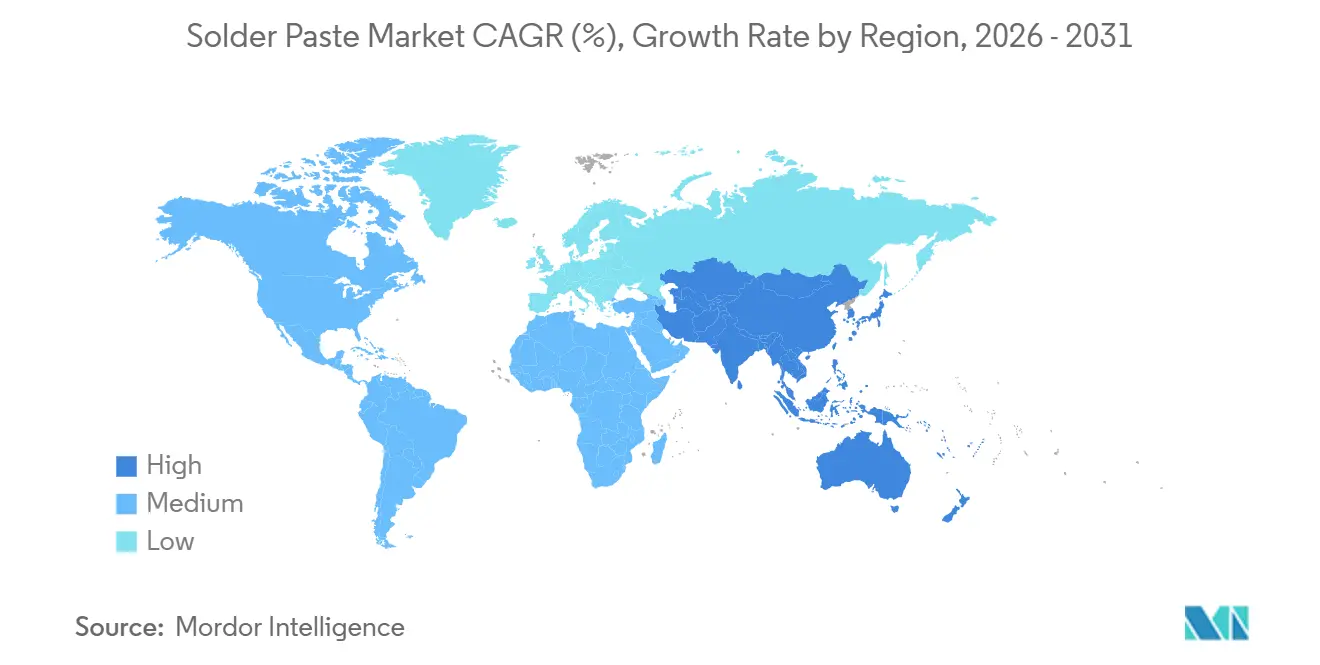

- By geography, Asia-Pacific commanded 41.25% revenue in 2025 and is advancing at a 9.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solder Paste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization and ultra-fine-pitch component adoption | +0.9% | Global, with concentration in APAC (China, South Korea, Taiwan) and early adoption in North America consumer-electronics hubs | Medium term (2-4 years) |

| SMT line capacity expansions across EMS hubs | +0.8% | APAC core (China, India, Vietnam, Thailand, Malaysia), spill-over to Mexico and Eastern Europe | Short term (≤ 2 years) |

| Regulatory push toward lead-free and halogen-free alloys | +0.7% | EU and UK (RoHS enforcement), North America (state-level mandates), China (RoHS 2.0), Japan (J-Moss) | Long term (≥ 4 years) |

| High-reliability pastes for EV power modules and ADAS | +0.6% | Global, with peak demand in Germany, China, United States, South Korea automotive corridors | Medium term (2-4 years) |

| AI-enabled inline printing analytics demanding extended stencil life | +0.3% | North America and EU advanced-manufacturing sites, expanding to APAC tier-1 EMS providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Miniaturization And Ultra-Fine-Pitch Component Adoption

Wearable and smartphone brands now place 01005-metric passives and 008004-imperial resistors that require Type 6 and Type 7 powders defined in IPC J-STD-005B for reliable aperture filling[1]IPC, “J-STD-005B Solder Paste Specifications,” ipc.org. Apple’s adoption of 008004 capacitors in the A18 Bionic forced EMS providers to qualify halogen-free Type 6 pastes with 48-hour tack time, lifting average stencil orders for laser-cut foils by 22% in 2025. Stencil smoothness below 80 µm is now essential to curb solder-balling on pads narrower than 200 µm. Jet-dispensing systems have emerged for micro-LED assembly, where SHENMAO’s PF606-P266J delivers 25 µm deposits that stencils cannot match. As a result, the solder paste market is seeing a technology bifurcation: conventional printing dominates broader SMT, while jet-based deposition captures extreme pitches below 50 µm.

SMT Line Capacity Expansions Across EMS Hubs

More than 1,200 new SMT (Surface Mount Technology) lines came online in 2025, 68% of them in Asia-Pacific, adding roughly 216 metric tons of incremental paste demand at full utilization. Vietnam and India are the standout gainers, drawing notebook and smartphone assembly that formerly resided in China. Harman International’s USD 42 million automotive-infotainment plant in Maharashtra demonstrates the pivot toward local EV electronics builds. Every greenfield line consumes close to 180 kg of paste yearly, amplifying the baseline growth of the solder paste market. Looking ahead, Goertek’s USD 390 million Vietnam campus, slated for Q2 2027, signals continued investment in Southeast-Asian SMT ecosystems.

Regulatory Push Toward Lead-Free And Halogen-Free Alloys

EU directives 2025/1802, /2363, and /2364 abolish the remaining high-temperature-solder exemptions by December 2027, pressing automotive and aerospace suppliers to transition to Innolot and 90ISC alloys well before that deadline[2]European Commission, “Directive 2025/2363,” europa.eu. China’s RoHS 2.0 inspections began in January 2026 with penalties up to CNY 300,000 (USD 43,000) for non-compliance. Consequently, halogen-free pastes are projected to rise from 19% of lead-free volume in 2025 to roughly 28% by 2031. Indium12.9HF’s less than 10% voiding in 0.5-mm-pitch BGAs (ball grid arrays) recently won the 2026 IPC NPI (New Product Introduction) Award, underscoring how innovation now centers on flux chemistry alongside alloy tweaks. Collectively, these measures nudge the solder paste market toward chemistries that satisfy both reliability and environmental metrics.

High-Reliability Pastes For EV Power Modules And ADAS

Electric-vehicle traction inverters face 1,000-3,000 thermal cycles between -40°C and +175°C, surpassing SAC305’s fatigue limits after 800 cycles. Silver-sintering materials such as mAgic DAF exhibit shear strengths above 40 MPa and thermal conductivity over 150 W/m·K, tripling SAC405 performance. Infineon’s AURIX TC4x ADAS controllers specify voiding under 15%, steering EMS partners toward closed-loop print-to-reflow controls. The automotive IPC-A-610JA addendum, published September 2025, further tightens head-in-pillow limits, intensifying demand for pastes that maintain consistent solder-volume deposition. These requirements channel a premium segment inside the broader solder paste market where reliability eclipses cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC and sustainability compliance costs | -0.5% | North America (California, northeastern states), EU (Industrial Emissions Directive), China (Air Pollution Prevention and Control Law) | Short term (≤ 2 years) |

| Process-window shrinkage with T6/T7 powders in high-humidity climates | -0.3% | Southeast Asia (Vietnam, Thailand, Malaysia, Philippines, Indonesia), coastal China, India during monsoon season | Medium term (2-4 years) |

| Limited dross-recycling infrastructure hindering circularity goals | -0.2% | Global, with acute gaps in APAC EMS facilities and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC And Sustainability Compliance Costs

Halogen-free fluxes emit 18% more VOCs during peak reflow than halogenated chemistries per the 2024 U.S. EPA lifecycle review. California’s Rule 1144, effective January 2026, halves allowable emissions to 25 g/L of flux, obliging EMS plants to install oxidizers costing USD 500,000-750,000 per line. The EU Industrial Emissions Directive now demands continuous emissions monitoring for electronics plants producing over 10 million boards yearly. Although Stannol’s SP6500 recycled paste cuts embodied carbon by 87%, its 12% price premium limits broad uptake. These added costs compress margins, tempering near-term growth in sections of the solder paste market.

Process-Window Shrinkage With T6/T7 Powders In High-Humidity Climates

IEEE research shows solder-balling incidents double above 60% relative humidity when deposits fall below 100 µm. Vietnam’s monsoon pushes ambient humidity beyond 75%, forcing air-handling retrofits that add USD 0.08 per board in energy overheads. Benchmark Electronics’ Penang line installed desiccant dehumidifiers in 2025 to stabilize paste tack, highlighting the extra capex required in tropical plants. Tight ±3°C reflow windows for Type 7 pastes elevate risk when conveyor speed drifts, compelling investments in 12-zone ovens like BTU International’s Pyramax that cost USD 320,000 each. Such process-control burdens narrow the appeal of ultra-fine powders for price-sensitive operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lead-Free Dominance Meets Halogen-Free Momentum

Lead-free solder paste held 73.22% of the solder paste market share in 2025. SAC305 remains the standard alloy, yet its 217°C liquidus challenges heat-sensitive substrates. Halogen-free solder paste, propelled by telecom and automotive qualification cycles, is projected to climb at a 3.66% CAGR during the forecast period (2026-2031). Demand for ultra-low-temperature blends such as OM-220, reflowing at 180°C, is rising in flexible OLED displays, underscoring diversification within the solder paste market size for product-type categories. Meanwhile, aerospace maintains limited use of eutectic SnPb under Annex III exemptions that persist until at least 2031.

No-clean chemistries captured a significant portion of lead-free shipments in 2025 as EMS providers trimmed wash equipment and water bills. Water-soluble pastes retain medical-device niches where ionic cleanliness under 1.56 µg/cm² is mandatory. Kester’s TSF-6502 supports implantable devices that endure gamma-irradiation sterilization. Halogen-free products such as Indium12.9HF mitigate chloride-induced corrosion on gold contacts in humid regions, alleviating a failure mode that once stalled 5G small-cell rollouts. Collectively, evolving flux chemistries continue to recast the solder paste market landscape by product type.

By Application: SMT Leads, Micro-Electronics Accelerates

The surface-mount segment captured 38.89% volume in 2025, anchoring the broader solder paste market size. High-speed smartphone and notebook lines dominate this bucket, though void specifications for 0.4-mm-pitch BGAs now run under 15%, pushing tighter print controls. Micro-electronics and advanced packaging are forecast to outpace at 3.78% CAGR through 2031, driven by chiplet and 2.5D/3D integration. TSMC’s CoWoS process needs Type 7 powders for 40 µm pitch bumps, while Intel’s Foveros Direct maintains SAC305 on substrate attach even as hybrid bonding handles die-to-die interconnects. Ball-grid-array uses approximately 18% of paste consumption, face shrinking void limits that keep process engineers leaning on closed-loop SPI data.

Through-hole soldering persists in industrial controls where pin-in-paste reduces steps by 40% on mixed-technology boards. Selective soldering represents a niche portion of global paste volume but is indispensable for automotive body-control units that demand robust connector joints. Wave soldering’s share is confined to power-distribution boards and certain defense electronics that would require multi-year MIL re-qualification to convert. These trends collectively define application-level shifts inside the solder paste market.

By End-user Industry: Consumer Electronics Leads, Automotive Surges

Consumer electronics retained 51.35% share of the solder paste market in 2025 as 1.4 billion smartphones continued to ship yearly. However, automotive electronics is projected to climb at 9.03% CAGR as EV architectures demand up to 3,000 solder joints per vehicle. Power-module void limits below 5% and temperature swings to +175°C necessitate high-reliability pastes, creating premium pockets within the solder paste market size. Telecommunications infrastructure contributed about a small portion of the market revenue, with base-station power amplifiers requiring SAC405 for 20-year outdoor lifetimes.

Industrial automation sticks to longer refresh cycles but layers on IEC 61508 functional-safety paperwork that favors traceable paste lots. Aerospace and defense continue to pay premium pricing for MIL-STD-883 qualifications. Medical devices prefer water-soluble chemistries validated under ISO 10993. LED lighting, wearables, and smart-home electronics exhibited brisk unit growth that requires Type 6 powders for 01005 passives in compact footprints.

Geography Analysis

Asia-Pacific captured 41.25% revenue in 2025 and is forecast to post the fastest 9.01% CAGR to 2031, reinforcing the region’s primacy in the solder paste market. Samsung’s USD 3 billion Pyeongtaek P4 fab will add 12-layer high-bandwidth-memory packaging by 2027, alone needing 420 tons of paste annually. LG Innotek’s USD 408 million Gumi expansion for automotive camera substrates further cements Korea’s tilt into ADAS hardware. India’s electronics output reached USD 115 billion in 2025 under its Production-Linked Incentive scheme, funneling SMT investments to Tamil Nadu and Karnataka. Vietnam, flush with USD 1.8 billion in 2025 EMS inflows, is fast becoming a secondary pole for the solder paste market in Asia.

North America’s market share in 2025 was buoyed by reshored automotive-electronics, aerospace, and Class III medical-device builds. Mexico’s Guadalajara-Tijuana corridor exported USD 126 billion in electronics in 2025, adopting halogen-free pastes to satisfy OEM sustainability metrics. In Europe, German tier-1s completed Innolot and 90ISC qualification in anticipation of the 2027 lead exemption sunset. Bosch’s Reutlingen fab added silicon-carbide power devices in Q3 2025, elevating low-void paste needs for inverter assembly.

South America and the Middle East and Africa together comprised least share. Brazil’s electronics sector leans on Manaus Free-Trade-Zone incentives that localize SMT for smartphones. Saudi Arabia earmarked USD 2 billion in 2025 for PCB and packaging capacity under Vision 2030, nurturing a regional node in the solder paste market. South Africa’s automotive OEMs consumed roughly 180 tons of paste in 2025, with future growth tied to EV localization mandates.

Competitive Landscape

The solder paste market is moderately concentrated. Vertical integration is reshaping dynamics: SHENMAO’s July 2025 purchase of PMTC adds a jet-dispenser line that locks customers into bundled consumable-equipment ecosystems. AIM Solder’s February 2025 acquisition of Canfield Technologies pulled wave-soldering preforms into its portfolio, broadening its reach beyond paste. Sustainability differentiators also matter; Stannol’s SP6500, with 85% recycled alloy, aligns with EU Scope-3 reporting and commands premium bids. Stringent IPC-J-STD-005B, -004C, and the automotive J-STD-001JA addendum keep qualification costs high, deterring new entrants and reinforcing incumbent positions inside the solder paste market.

Solder Paste Industry Leaders

Henkel AG & Co. KGaA

MacDermid Alpha Electronics Solutions

Senju Metal Industry Co., Ltd.

Indium Corporation

Kester

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Indium Corporation received a Circuits Assembly New Product Introduction (NPI) Award for Indium12.9HF, a halogen-free solder paste engineered for cost-effective, low-silver alloys, including SAC105 and SAC0307.

- June 2025: KOKI Company Ltd. introduced the SB6NX58-G850 solder paste, featuring a solid-solution-strengthened solder alloy. The paste reduces microstructural transformation at solder joints and provides enhanced thermal-mechanical resistance. This makes it suitable for applications in automotive and industrial equipment operating in demanding environments.

Global Solder Paste Market Report Scope

Solder paste is a mixture of tiny, powdered solder alloy particles and flux used to connect electronic components to printed circuit boards (PCBs). It acts as a temporary adhesive to hold surface-mount (SMT) components in place, then melts under heat.

The solder paste market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into lead-free solder paste, leaded solder paste, no-clean solder paste, water-soluble solder paste, and halogen-free solder paste. By application, the market is segmented into surface-mount technology (SMT), through-hole technology, ball grid array (BGA) and chip scale package (CSP) assembly, wave and reflow soldering, and micro-electronics and advanced packaging. By end-user industry, the market is segmented into consumer electronics, automotive electronics, telecommunications, industrial electronics, aerospace and defense, healthcare and medical devices, and other end-user industries (LEDs, wearables, and smart-home). The report also covers the market size and forecasts for solder paste in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Lead-free Solder Paste |

| Leaded Solder Paste |

| No-clean Solder Paste |

| Water-soluble Solder Paste |

| Halogen-free Solder Paste |

| Surface-Mount Technology (SMT) |

| Through-hole Technology |

| Ball Grid Array (BGA) and Chip Scale Package (CSP) Assembly |

| Wave and Reflow Soldering |

| Micro-electronics and Advanced Packaging |

| Consumer Electronics |

| Automotive Electronics |

| Telecommunications |

| Industrial Electronics |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Other End-user Industries (LEDs, Wearables, and Smart-home) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Lead-free Solder Paste | |

| Leaded Solder Paste | ||

| No-clean Solder Paste | ||

| Water-soluble Solder Paste | ||

| Halogen-free Solder Paste | ||

| By Application | Surface-Mount Technology (SMT) | |

| Through-hole Technology | ||

| Ball Grid Array (BGA) and Chip Scale Package (CSP) Assembly | ||

| Wave and Reflow Soldering | ||

| Micro-electronics and Advanced Packaging | ||

| By End-user Industry | Consumer Electronics | |

| Automotive Electronics | ||

| Telecommunications | ||

| Industrial Electronics | ||

| Aerospace and Defense | ||

| Healthcare and Medical Devices | ||

| Other End-user Industries (LEDs, Wearables, and Smart-home) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the solder paste market be by 2031?

The Solder Paste Market size is projected to expand from USD 1.91 billion in 2025 and USD 1.97 billion in 2026 to USD 2.32 billion by 2031, registering a CAGR of 3.32% between 2026 and 2031.

Which region is growing the fastest in solder paste demand?

Asia-Pacific is expected to post the highest CAGR at 9.01% through 2031, driven by new fabs and EMS expansions.

Why is automotive electronics important for solder paste suppliers?

EV inverters and ADAS modules need high-reliability joints that fuel a 9.03% CAGR for automotive paste consumption.

What is driving adoption of halogen-free solder pastes?

Upcoming RoHS deadlines and OEM sustainability scorecards are moving halogen-free formulations toward a higher share by 2031.

Page last updated on: