Silicon Capacitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

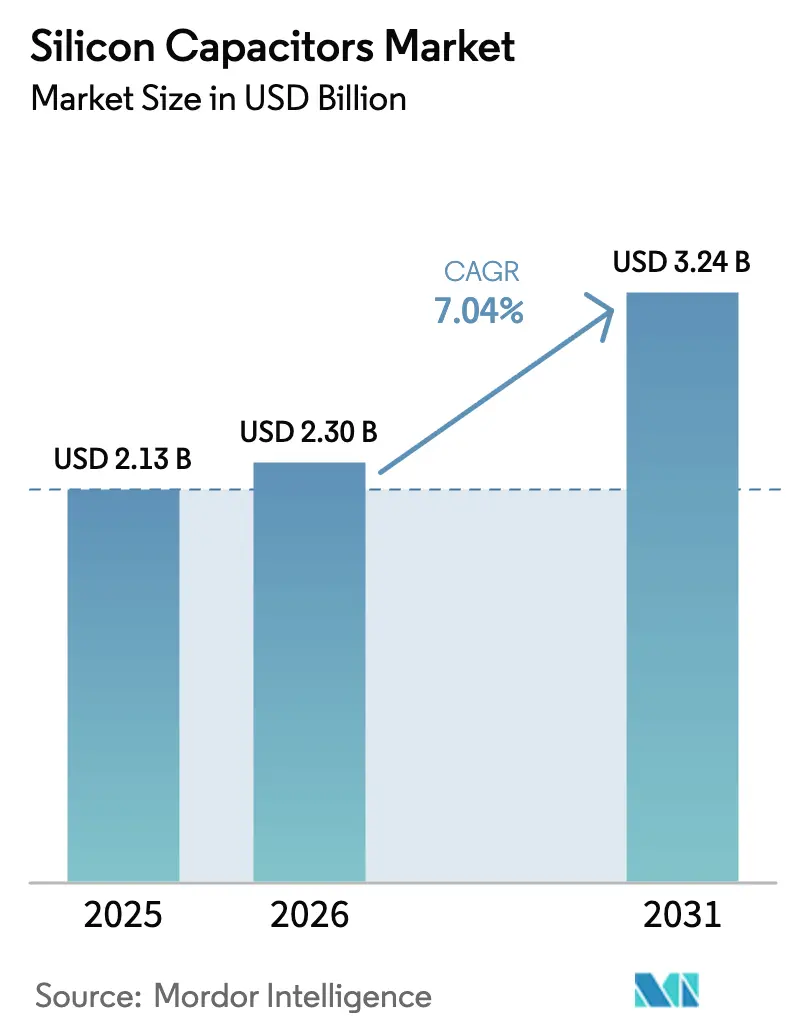

| Market Size (2026) | USD 2.30 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

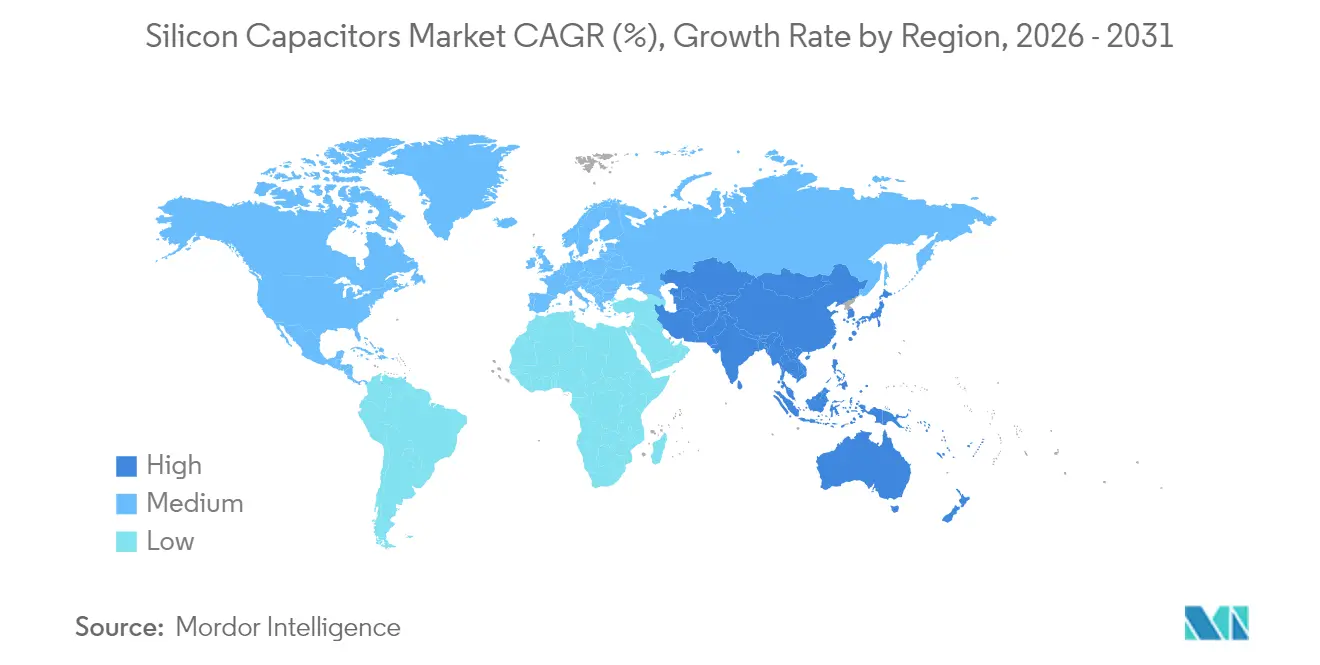

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Capacitors Market Analysis by Mordor Intelligence

The silicon capacitors market size was valued at USD 2.13 billion in 2025 and is estimated to grow from USD 2.30 billion in 2026 to reach USD 3.24 billion by 2031, at a CAGR of 7.04% during the forecast period 2026-2031. Heterogeneous chiplet architectures in artificial-intelligence accelerators, the proliferation of 5G and 6G radio-frequency front ends, and accelerating automotive electrification are redirecting demand away from discrete ceramic solutions toward monolithic silicon-based passive integration. Wafer-level fan-out and chip-scale packaging formats dominate smartphone and wearable shipments, while module-level system-in-package designs are rapidly expanding in electric vehicles and AI servers. Deep-trench structures remain the revenue leader, yet metal-insulator-metal variants are emerging as the performance benchmark for wide-bandgap power modules, and regional subsidy programs are shortening lead times and diversifying supply chains. Leakage-current penalties, premium silicon-on-insulator wafer pricing, and high-temperature reliability limits continue to temper penetration in cost-sensitive Internet-of-Things nodes.

Key Report Takeaways

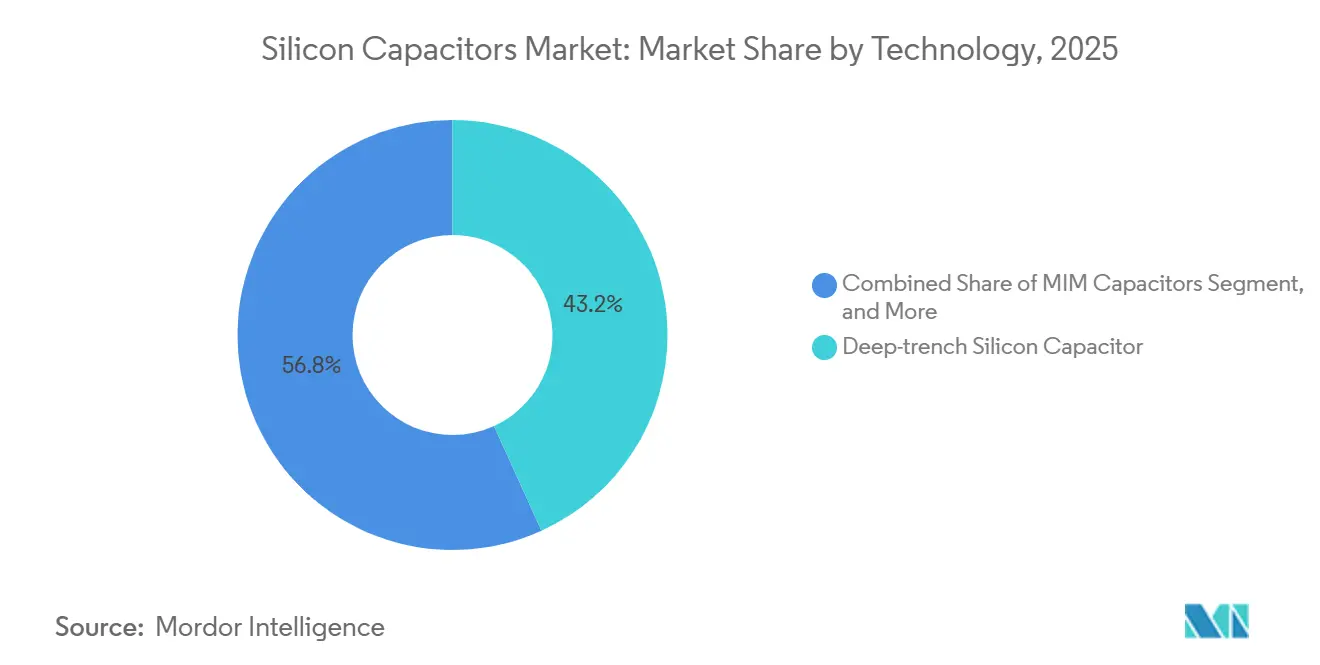

- By technology, deep-trench silicon capacitors led with 43.20% of the silicon capacitors market share in 2025, while metal-insulator-metal devices are forecast to grow at a 9.29% CAGR to 2031.

- By packaging level, wafer-level formats captured 49.39% of the revenue share in 2025; module-level system-in-package integration is projected to grow at a 9.09% CAGR through 2031.

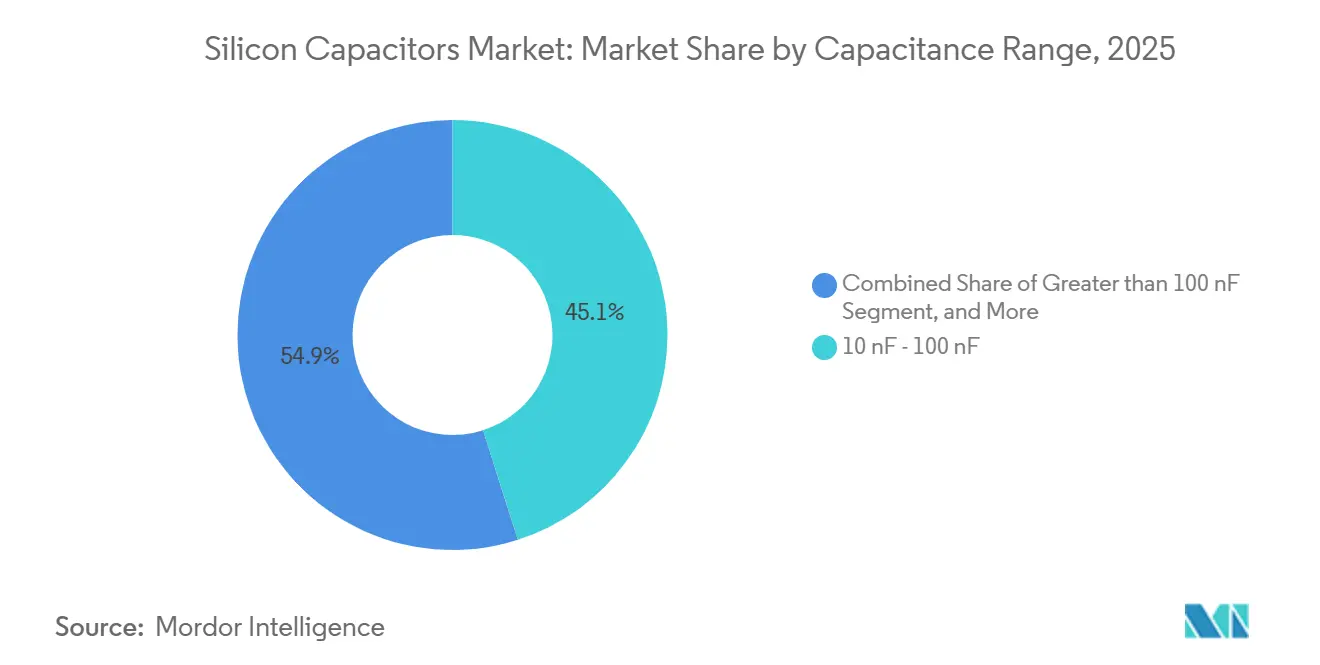

- By capacitance range, the 10-100 nanofarad band accounted for 45.08% of the silicon capacitors market size in 2025; values above 100 nanofarads are expanding at a 7.89% CAGR to 2031.

- By end-user application, consumer electronics and wearables held 32.39% revenue share in 2025, whereas automotive demand is the fastest growing at an 8.81% CAGR to 2031.

- By geography, China retained a 42.64% share of 2025 shipments, while India is anticipated to register the highest regional CAGR of 10.24% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicon Capacitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for miniaturized passive components in EV power-train and ADAS systems | +1.80% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Proliferation of 5G/6G RF front-end modules requiring ultra-broadband decoupling capabilities | +1.50% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Heterogeneous chiplet packaging evolution driving embedded silicon IPD integration in AI accelerators and memory stacks | +1.40% | North America, Taiwan, South Korea | Medium term (2-4 years) |

| Adoption of deep-trench 3D capacitor technology enabling higher capacitance density | +1.20% | Global, early adoption in automotive and aerospace | Long term (≥ 4 years) |

| On-shore semiconductor subsidy programs boosting local silicon capacitor foundry investments | +0.90% | United States, Europe, India | Long term (≥ 4 years) |

| Reliability requirements exceeding 175°C for down-hole drilling and aerospace electronics | +0.60% | North America, Middle East, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Miniaturized Passive Components in EV Power-Train and ADAS Systems

Electric-vehicle traction inverters and advanced driver-assistance system hubs increasingly specify silicon capacitors to meet sub-50-picohenry inductance targets that ceramic devices cannot reach within the same footprint. Tesla’s 2025 Hardware 4 computer embeds twelve silicon metal-insulator-metal capacitors per dual-die package to suppress 300-ampere transients, achieving 99.7% rejection at 10 MHz.[1]Tesla Investor Relations, “2025 Investor Day Presentation,” tesla.com BYD’s Seal sedan integrates deep-trench capacitors inside its 800-volt silicon-carbide inverter, reducing parasitic inductance by 40% and supporting 20 kHz switching.[2]BYD Company, “Seal Sedan European Launch,” byd.com Bosch’s fifth-generation radar sensor stabilizes local-oscillator phase noise below −100 dBc-Hz by embedding wafer-level capacitors on the 77 GHz transceiver die.[3]Robert Bosch GmbH, “Bosch Mobility Annual Report 2025,” bosch-mobility-solutions.com Continental’s 2026 zone-controller platform consolidates fifteen ECUs and requires more than 200 silicon capacitors per processor to maintain voltage integrity.[4]Continental AG, “Domain Controller Press Release 2026,” continental.com Global automotive silicon-capacitor unit demand tripled between 2023 and 2025 as electrification roadmaps intensified.

Proliferation of 5G-6G RF Front-End Modules Requiring Ultra-Broadband Decoupling Capabilities

Fifth- and sixth-generation front-end architectures need flat impedance from 100 MHz to 6 GHz, a span that forces ceramic designs to stack multiple dielectric codes. Skyworks’ Sky5 platform ships with eighteen integrated silicon capacitors, trimming insertion loss by 0.3 dB and boosting transmit linearity by 1.5 dB. Qualcomm’s 2025 Snapdragon X80 modem integrates twenty-two metal-insulator-metal capacitors on a 4 nm node to stabilize millimeter-wave beam-forming bursts. Ericsson’s Massive-MIMO arrays embed wafer-level capacitors inside radio units to hold intermodulation distortion below −50 dBc, enabling 200 MHz carrier aggregation. 3GPP Release 19 mandates sub-5 ns transient response at 6 GHz, further entrenching silicon solutions. Unit shipments of RF-integrated passive devices topped 15 billion in 2025, with silicon variants rising to 12% share.

Heterogeneous Chiplet Packaging Evolution Driving Embedded Silicon IPD Integration

Artificial-intelligence accelerators and high-bandwidth memory stacks embed silicon capacitors inside organic interposers and bridges to keep rail noise below 10 mV during terabit-per-second data transfers. Intel’s Ponte Vecchio GPUs use 200-plus deep-trench capacitors per bridge tile to stabilize 600-watt compute bursts. AMD’s MI300X packages twelve compute chiplets and eight HBM dies around 1,500 metal-insulator-metal capacitors, cutting network impedance to 0.5 mΩ. TSMC’s chip-on-wafer-on-substrate process inserts capacitors into redistribution layers, shrinking inductance by 60%. Micron’s HBM3E stacks require fifty capacitors per 16 GB module to preserve signal integrity at 9.6 Gbps-pin. By 2025, 40% of the 85 million chiplet processors shipped contained embedded silicon capacitors.

Adoption of Deep-Trench 3D Capacitor Technology Enabling Higher Capacitance Density

Deep-trench structures deliver 50-100 nF mm-² by etching 50:1 aspect-ratio columns that multiply surface area. Murata’s IPDiA unit ramped 60 nF mm-² production in 2025 for 48-V DC-DC converters. STMicroelectronics’ VIPower M0-7 ICs integrate deep-trench capacitors to handle 100-A load dumps, removing twelve external ceramics and saving USD 0.80 per unit. Fraunhofer IPMS prototypes hit 120 nF mm-² using hafnium-oxide dielectrics while maintaining sub-1 µA leakage. Empower Semiconductor embeds four deep-trench capacitors in each EP70xx regulator, achieving 95% efficiency at 10 MHz. Global deep-trench capacity rose 35% in 2025 to 8 billion units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High leakage current and limited capacitance density compared to multilayer ceramic capacitors | -1.20% | Global | Short term (≤ 2 years) |

| Premium pricing owing to specialized SOI wafers and TSV processing requirements | -0.90% | Global, acute in cost-sensitive consumer IoT | Medium term (2-4 years) |

| Foundry capacity bottlenecks for ≥200 mm IPD production lines | -0.60% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Thermo-mechanical stress limitations above 200°C restrict adoption in SiC power modules | -0.40% | Automotive and industrial segments in Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Leakage Current and Limited Capacitance Density Compared to Multilayer Ceramic Capacitors Constrain Adoption

Silicon MOS capacitors leak 10-100 nA mm-² at 5 V bias, up to 100-times higher than X7R ceramics, draining standby budgets in battery-powered wearables. KYOCERA AVX measured an 8–12-hour runtime penalty in smartwatches when silicon devices replaced ceramics. IEEE IEDM 2024 data showed 50 nA leakage for 100 nF silicon parts versus 0.5 nA for ceramics, attributing losses to interface traps. Production density plateaued at 60 nF mm-³ in 2025, well below the 150-200 nF mm-³ of leading ceramics. Knowles aims for sub-10 nA leakage using hafnium-zirconium-oxide by 2027, but volume qualification is two years away. Elevated leakage accelerates dielectric breakdown at 85 °C, cutting median life from ten to three years in harsh under-hood placements.

Premium Pricing Owing to Specialized SOI Wafers and TSV Processing Requirements Limiting Cost-Sensitive Applications

Silicon-on-insulator wafers cost USD 800-1,200 per 200 mm blank, versus USD 200-300 for standard CMOS, lifting die cost three- to four-fold. Through-silicon-via steps add USD 15-25 per 300 mm wafer, keeping silicon capacitors viable mainly in automotive, RF, and data-center devices where bill-of-materials ceilings exceed USD 50. Massachusetts Bay Technologies prices 100 nF dies at USD 0.08-0.12 in 10 k lots, versus USD 0.01-0.02 for ceramics, a six-times spread. Microchip reported a 12-15% IC cost uptick when embedding silicon capacitors, acceptable for automotive but not for white-goods designs targeting 20% annual savings. Average IPD line utilization sat at 68% in 2025, below the 85% break-even threshold, prolonging the price gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: MIM Architectures Gain Traction in Wide-Bandgap Power Modules

Metal-insulator-metal capacitors are projected to grow at a 9.29% CAGR through 2031, the fastest pace among technologies within the silicon capacitors market. Infineon’s 1,200 V CoolSiC modules integrate six MIM capacitors per half-bridge to tame 50 V ns-¹ edges, pushing inverter efficiency to 98.5%. Deep-trench devices retained 43.20% revenue in 2025 by servicing automotive 48 V rails and smartphone processors; however, yield challenges beyond 200 mm constrain further scaling. MOS structures persist in legacy RF tuning roles, and MIS variants carve niche share in radiation-hardened aerospace electronics.

MIM designs favor planar thin-film stacks that minimize equivalent-series-resistance and stabilize performance beyond 150 °C, key for gallium-nitride amplifiers. MACOM’s 28 GHz GaN-on-silicon PA embeds on-die MIM capacitors, boosting power-added efficiency by five points. Industry momentum signals a balanced landscape in which deep trench retains high-density leadership while MIM captures wide-bandgap niches, collectively shaping the next-generation silicon capacitors market size.

By Packaging Level: Module-Level Integration Accelerates with System-in-Package Adoption

Wafer-level packages held 49.39% share in 2025 thanks to smartphone volume economics, yet module-level system-in-package formats are expanding at a 9.09% CAGR through 2031. Apple’s S9 SiP embeds fourteen capacitors within a six-layer substrate, shaving 0.4 mm in thickness and extending battery life to 36 hours. Die-level flip-chip adoption is limited to data-center GPUs where the silicon capacitors market size supports sub-100 pH targets, whereas interposer-level 2.5D carriers dominate AI accelerators requiring terabit bandwidth.

Samsung Electro-Mechanics plans embedded-capacitor ball-grid-array substrates for 5 nm logic dies by 2027, aiming at a 30% impedance cut. Discrete 0201 and 01005 silicon capacitors remain relevant for retrofit PCB designs, representing 15-20% of unit volume. The convergence of fan-out and SiP architectures positions hybrid packaging to optimize cost, performance, and thermals across the silicon capacitors market.

By Capacitance Range: High-Value Bands Lift with AI and EV Compute Density

The > 100 nF segment is forecast to advance at a 7.89% CAGR as electric-vehicle battery management and AI servers demand localized bulk energy. NVIDIA’s 2025 Blackwell GPU integrates more than 200 capacitors above 100 nF inside the package substrate to stabilize 1,000 W bursts. The 10-100 nF range secured 45.08% market share in 2025, straddling smartphone PMICs and industrial IoT gateways.

Texas Instruments specifies 150-200 nF values in 2025 automotive battery monitors to filter 1 MHz noise, a capacitance unreachable with sub-100 nF silicon parts. RF front ends and radar sensors continue to use < 10 nF values for bandwidth control, capturing 20-25% of units despite lower revenue. Divergent design targets are therefore segmenting the silicon capacitors market share between high-density power domains and low-value RF islands.

By End-User Application: Automotive Electrification Outpaces Consumer Device Growth

Automotive demand is projected to grow at an 8.81% CAGR, moving from 32 capacitors per vehicle in 2020 to more than 300 by 2030 as 48 V mild hybrids, 800 V drivetrains, and zonal architectures proliferate. European Union CO₂ mandates and California’s ACC II regulations accelerate content growth. Consumer electronics held 32.39% share in 2025 but faces saturation and lengthening replacement cycles, muting growth to mid-single digits.

Telecommunications equipment, spanning 5G base stations and data-center servers, adds 50-60 million capacitors annually, representing 20-25% of shipments. Aerospace and defense, though sub-10% of revenue, command 2-3x price premiums due to radiation hardening and 200 °C operation in programs such as the F-35 avionics upgrade. Healthcare and industrial IoT remain niche due to leakage constraints and cost sensitivities yet select PLC and robotic controllers adopt silicon capacitors for EMI immunity.

Geography Analysis

China maintained 42.64% of 2025 shipments, leveraging vertically integrated OEMs and state-backed IPD foundries clustering around Shenzhen and Shanghai. Domestic smartphone and electric-vehicle volumes anchor the silicon capacitors market size, while government subsidies offset equipment depreciation. North America represented nearly one-fifth of revenue, underpinned by United States CHIPS Act grants that earmark USD 1.5 billion for advanced packaging lines, thereby shortening lead times for automotive-grade parts.

Europe captured about 16% share, driven by STMicroelectronics’ and Infineon’s 200 mm expansions in France and Germany catering to car makers seeking supply-chain resilience. India, though still below 10% share, is the fastest-growing geography at a 10.24% CAGR thanks to a USD 10 billion incentive pool and Tata Electronics’ 300 mm fab in Dholera targeting 50,000 wafer starts per month by 2027. Japan and South Korea, traditional capacitor powerhouses, saw share erosion as cost pressures shifted volume to Southeast Asia, while Saudi Arabia’s NEOM initiative and United Arab Emirates’ hub vision seed early pilot lines for harsh-environment silicon capacitors. South America remains embryonic, with Brazil importing over 95% of demand despite fledgling localization efforts.

Competitive Landscape

The silicon capacitors market is moderately concentrated: Murata Manufacturing, KYOCERA AVX, STMicroelectronics, Skyworks Solutions, and Vishay Intertechnology jointly held an estimated 55-60% revenue share in 2025. Murata’s acquisition of IPDiA deepened vertical integration for automotive 48 V systems, while STMicroelectronics partnered with X-FAB in 2025 to co-develop SiC-compatible capacitors for 1,200 V traction inverters. Empower Semiconductor’s patent on monolithic buck regulators with embedded deep-trench capacitors illustrates a shift toward point-of-load integration.

Emerging foundries such as Massachusetts Bay Technologies and ELOHIM undercut incumbents’ non-recurring engineering quotes by 20-30%, winning industrial IoT and wearable sockets. Technology competition centers on volumetric density and leakage: Fraunhofer’s 120 nF mm-² hafnium-oxide prototype doubles today’s production benchmark, while hafnium-zirconium ferroelectrics aim for sub-10 nA leakage by 2027. Lead-time reduction has become a strategic differentiator, with automotive-grade qualification cycles compressing from 26 to 16 weeks after 2024 foundry expansions. Consequently, competition is migrating from price to design-service speed and application-specific IP, especially in gallium-nitride RF power amplifiers and silicon-photonics transceivers, where silicon capacitors unlock 5-point efficiency gains.

Silicon Capacitors Industry Leaders

Murata Manufacturing Co. Ltd.

Vishay Intertechnology Inc.

Skyworks Solutions Inc.

Empower Semiconductor

TSMC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ROHM launched high-power-density SiC molded modules in HSDIP20, paving the way for compact on-board chargers in electric vehicles.

- March 2025: Murata introduced Digital Envelope Tracking PMICs that cut RF power consumption by 25% in 5G devices, validated with Rohde & Schwarz instrumentation.

- March 2025: ROHM’s EcoGaN 650 V HEMTs were adopted by Murata Power Solutions for 5.5 kW AI-server front-end supplies.

- March 2025: Mazda and ROHM began joint GaN component development for next-generation EVs, seeking vehicle-level demos by FY 2025.

Global Silicon Capacitors Market Report Scope

The Silicon Capacitors Market Report is Segmented by Technology (MOS Capacitors, MIS Capacitors, Deep-Trench Silicon Capacitors, MIM Capacitors), Packaging Level (Die-Level, Wafer-Level, Interposer-Level, Module-Level/SiP, Discrete SMD), Capacitance Range (Less than 10 nF, 10-100 nF, Greater than 100 nF), End-User Application (Automotive, Consumer Electronics and Wearables, IT and Telecommunications, Aerospace and Defense, Healthcare, Industrial IoT and Smart Manufacturing, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| MOS Capacitors |

| MIS Capacitors |

| Deep-Trench Silicon Capacitors |

| MIM Capacitors |

| Die-Level (On-Chip / Bare Die / Flip-Chip) |

| Wafer-Level (WLCSP, Fan-Out) |

| Interposer-Level (2.5D / 3D Integration / TSV) |

| Module-Level / System-in-Package (SiP) |

| Discrete Surface-Mount Devices (SMD / Chip-Scale) |

| Less than 10 nF |

| 10 nF - 100 nF |

| Greater than 100 nF |

| Automotive |

| Consumer Electronics and Wearables |

| IT and Telecommunications |

| Aerospace and Defense |

| Healthcare |

| Industrial IoT and Smart Manufacturing |

| Other End-user Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| France | |

| Germany | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Technology | MOS Capacitors | |

| MIS Capacitors | ||

| Deep-Trench Silicon Capacitors | ||

| MIM Capacitors | ||

| By Packaging Level | Die-Level (On-Chip / Bare Die / Flip-Chip) | |

| Wafer-Level (WLCSP, Fan-Out) | ||

| Interposer-Level (2.5D / 3D Integration / TSV) | ||

| Module-Level / System-in-Package (SiP) | ||

| Discrete Surface-Mount Devices (SMD / Chip-Scale) | ||

| By Capacitance Range | Less than 10 nF | |

| 10 nF - 100 nF | ||

| Greater than 100 nF | ||

| By End-user Application | Automotive | |

| Consumer Electronics and Wearables | ||

| IT and Telecommunications | ||

| Aerospace and Defense | ||

| Healthcare | ||

| Industrial IoT and Smart Manufacturing | ||

| Other End-user Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the silicon capacitors market between 2026 and 2031?

The market is projected to grow at a 7.04% CAGR during 2026-2031.

Which technology segment is expanding fastest?

Metal-insulator-metal capacitors are forecast to rise at a 9.29% CAGR through 2031, driven by wide-bandgap power modules.

Why are automotive applications gaining importance?

Electrification and ADAS architectures are doubling silicon-capacitor content per vehicle, lifting automotive demand at an 8.81% CAGR.

Which geography shows the highest future growth?

India is expected to post a 10.24% CAGR to 2031, supported by a USD 10 billion semiconductor incentive program.

What is the main restraint limiting penetration in wearables?

High leakage current, up to 100-times that of multilayer ceramics, shortens battery life in low-power devices.

How concentrated is supplier power?

Five leading vendors account for roughly 55-60% of revenue, indicating moderate market concentration.

Page last updated on: