Plastic Film Capacitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

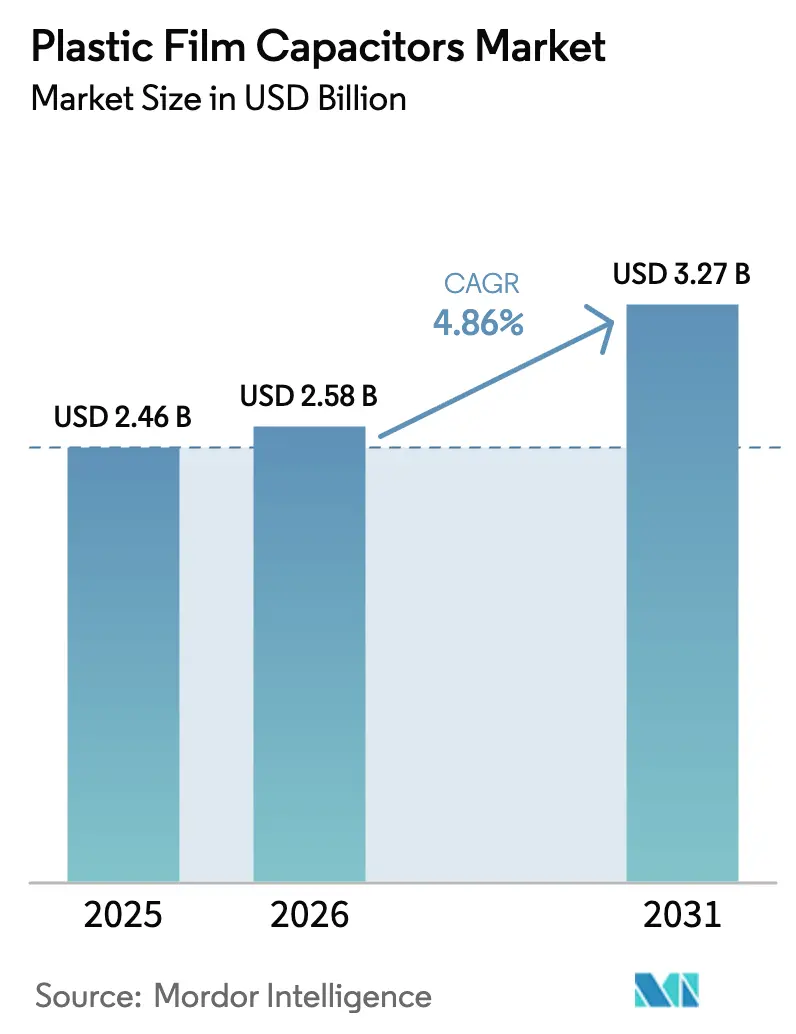

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Plastic Film Capacitors Market Analysis by Mordor Intelligence

The plastic film capacitors market size is expected to grow from USD 2.46 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 3.27 billion by 2031 at 4.86% CAGR over 2026-2031. Robust demand in e-mobility powertrains, renewable-energy converters, and 5G infrastructure anchors this growth, while polypropylene continues to dominate commercial volumes. Rising adoption of SiC/GaN power devices is shifting design priorities toward low-ESR, high-frequency performance, encouraging material innovation and higher-voltage designs. Regional production incentives in Asia-Pacific, India’s USD 24 billion PLI scheme, and Brazil’s BRL 186.6 billion (USD 35.09 billion) digitalization drive are accelerating localized capacity additions, tempering supply-chain concentration risks. Competition remains moderate but intensifying: legacy leaders such as TDK and Vishay face agile specialists that tailor form factors for next-generation traction inverters and grid-scale filters.[1]Source: TDK Corporation, “1st Quarter Fiscal 2024 Performance Briefing,” tdk.comResin and aluminum price swings remain the most immediate margin threat, yet vertical integration and hedging strategies are helping large vendors buffer volatility.

Key Report Takeaways

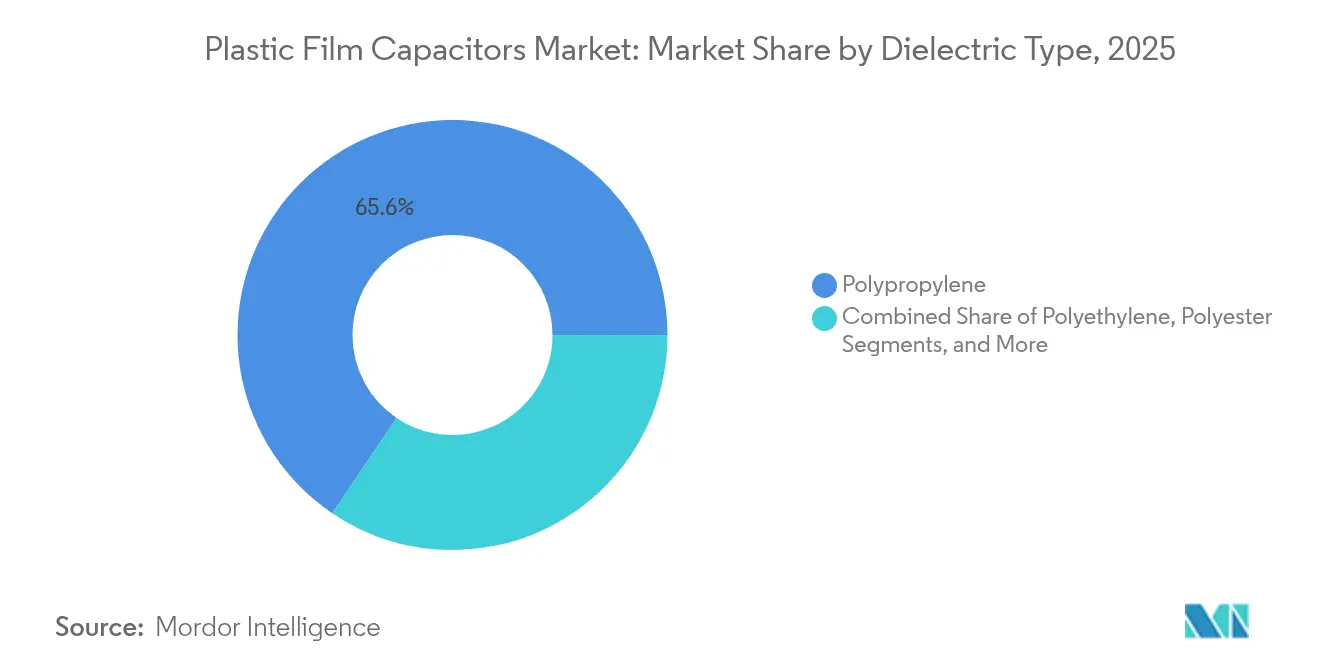

- By dielectric type, polypropylene held 65.55% of the plastic film capacitors market share in 2025, while polyphenylene sulfide is projected to rise at a 5.63% CAGR through 2031.

- By voltage rating, the 100–1,000 V range accounted for 53.35% of the plastic film capacitors market size in 2025; ratings above 1,000 V lead growth at a 4.72% CAGR.

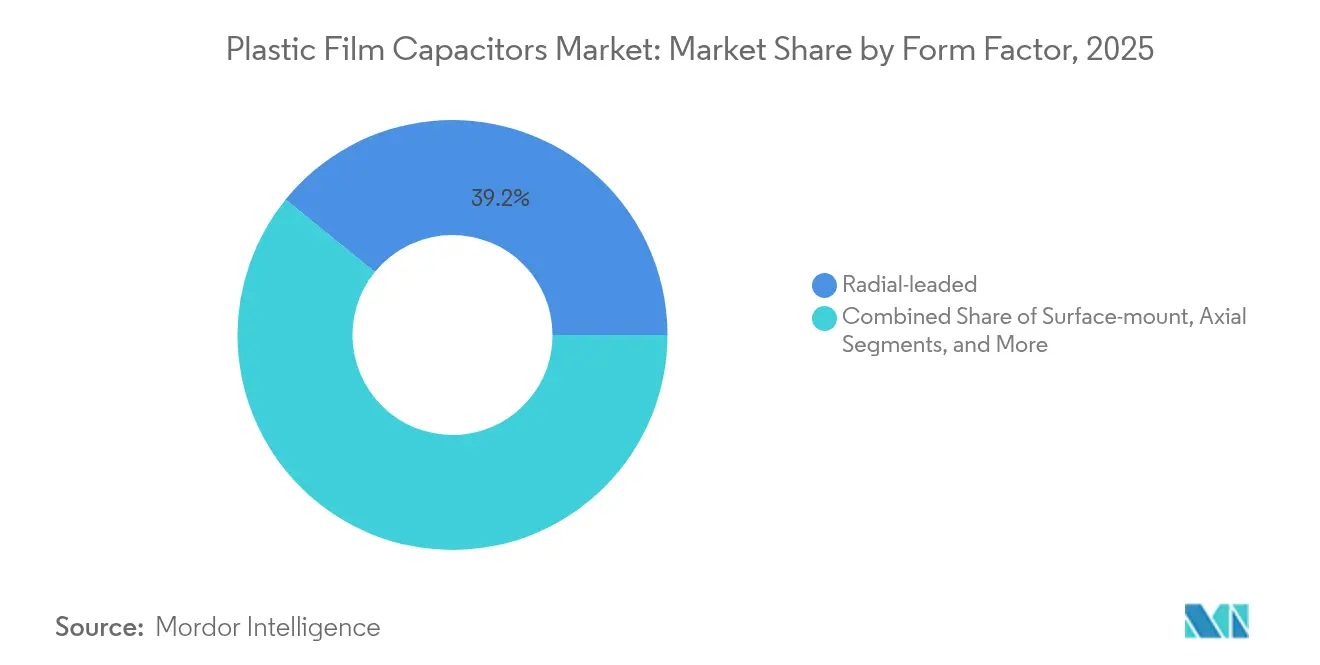

- By form factor, radial-leaded designs led with 39.15% revenue share in 2025, whereas stack and box packages exhibit the fastest expansion at 5.24% CAGR to 2031.

- By application, automotive captured 30.75% of the plastic film capacitors market share in 2025, and renewable-energy uses are advancing at a 5.93% CAGR through 2031.

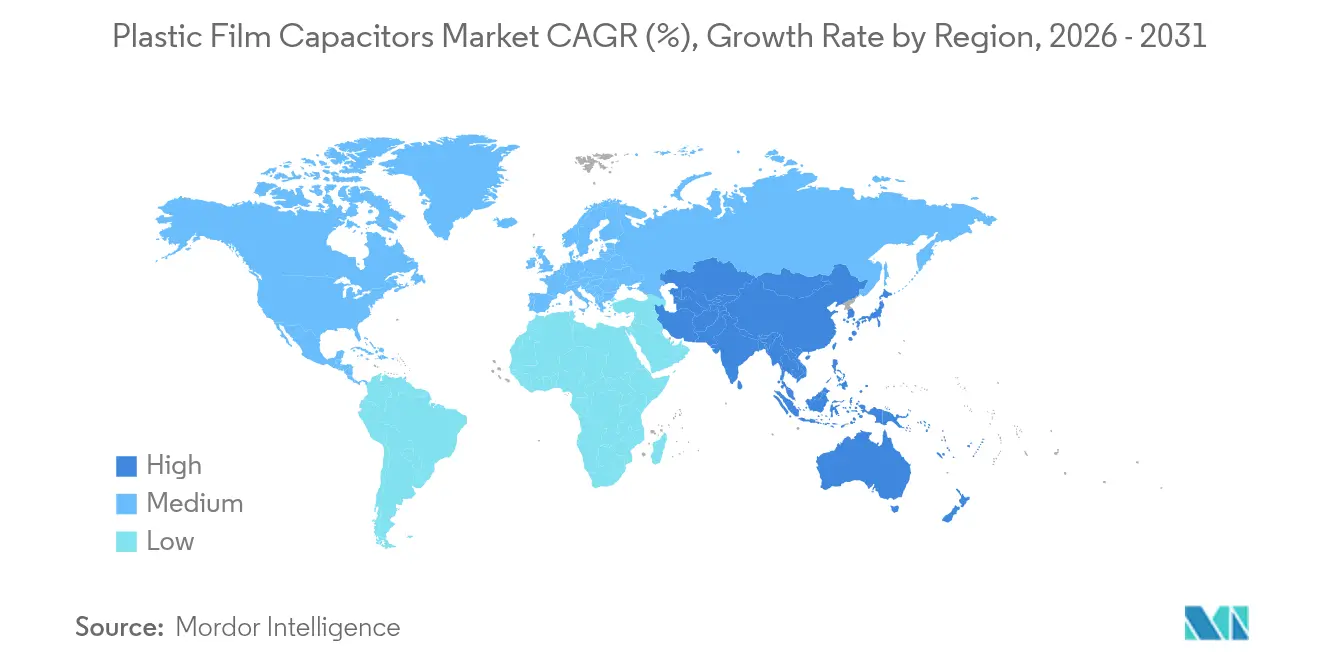

- By geography, Asia-Pacific commanded 43.80% of the plastic film capacitors market size in 2025 and is progressing at a 6.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Film Capacitors Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| DC-link demand for EV traction inverters | +1.2% | Global, China-Europe-the United States. | Medium term (2-4 years) |

| Shift toward SiC/GaN power devices | +0.8% | Asia-Pacific, North America | Long term (≥4 years) |

| Grid-scale renewable DC filters | +0.9% | Europe, China | Medium term (2-4 years) |

| 5G base-station miniaturization | +0.4% | Asia-Pacific, North America | Short term (≤2 years) |

| Government localization mandates | +0.6% | India, Brazil | Long term (≥4 years) |

| Circular-economy push for PP film recycling | +0.3% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in DC-link Demand for EV Traction Inverters

Electric vehicles multiply capacitor content per car by up to five times, as every traction inverter, onboard charger, and auxiliary converter requires high-capacitance DC-link banks. TDK’s xEVCap line targets this need with ripple-current endurance and 105 °C operation, shipping in volume from its Gravataí plant.[2]Source: TDK Electronics, “xEVCap Series Overview,” tdk-electronics.tdk.com Automakers pledging 50% electric sales by 2030 lock in multi-year visibility for capacitor procurement as battery pack voltages climb from 400 V to 800 V architectures. The plastic film capacitors market benefits directly, since film devices exhibit self-healing behavior critical to inverter reliability over 15-year vehicle lifetimes. Supply-chain depth is widening as India and Brazil court EV-component investors with fiscal incentives, reducing geographic risk for OEMs. As charging infrastructure scales, auxiliary DC filters in fast-chargers further reinforce volume momentum.

Rapid Shift Toward SiC/GaN Power Devices

Wide-bandgap semiconductors operate above 20 kHz, forcing designers to favor low-ESR dielectrics. Polypropylene retains leadership because of low losses, but nanocomposite PPS films with boron-nitride fillers now deliver triple energy density at 200 °C without dielectric breakdown, broadening design latitude for aerospace and industrial drives.[3]Source: Nature Communications, “High-Temperature Polymer Nanocomposites,” nature.com Declining SiC device prices unlock mainstream industrial retrofits, where 2–3% efficiency gains translate into lower electricity bills and carbon footprints. Power-module makers increasingly list film capacitors on qualified material sheets, diverting share from aluminum electrolytics in high-frequency roles. The trend compresses development cycles as OEMs co-design capacitors and power modules to meet EMI, thermal, and life targets simultaneously. Suppliers able to metallize ultra-thin films while maintaining partial-discharge margins gain a cost-performance edge.

Grid-scale Renewable Integration Requiring High-voltage DC Filters

Solar and wind farms necessitate 1,000 V-plus DC filters with 20-year lifespans, aligning component life with PV module warranties. Brazil’s smart-grid roadmap, co-funded by JICA, calls out switched capacitor banks as critical for voltage regulation across vast transmission corridors. [4]Source: Japan International Cooperation Agency, “Brazil Smart Grid Technical Report,” jica.go.jp Metallized polypropylene meets utility needs through self-healing and stable capacitance under thermal cycling, outperforming ceramic or electrolytic alternatives. Large projects demand thousands of parts per substation, generating lumpy but lucrative orders. Policy mandates for renewable share targets in Europe and China sharpen procurement cycles, offering suppliers headroom for premium pricing. As battery-energy-storage systems proliferate, high-voltage film capacitors also service DC-bus smoothing in megawatt-scale inverters, reinforcing secular demand.

Miniaturization Pressure from 5G Base Stations

Network equipment vendors race to shrink power-conversion footprints within dense radio units. DC/DC converter modules now integrate stack or box film capacitors that pack higher volumetric capacitance and shed heat efficiently, enabling slimmer antenna-mast enclosures.[5]Source: Monolithic Power Systems, “5G DC/DC Module Solutions,” monolithicpower.com5G rollouts in China, South Korea, and the U.S. push equipment counts into the millions, sustaining near-term volume. Higher operating frequencies amplify EMI concerns, making low-ESR film capacitors essential for stability. Surface-mount MLCCs compete below 100 V, but film technology prevails in 200–600 V rails that feed power amplifiers. Rapid replacement cycles in telecom sites also favor components with predictable aging curves and field-replaceable formats.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Polypropylene and aluminum price volatility | -0.7% | Global, Asia-Pacific hubs | Short term (≤2 years) |

| BOPP film extrusion concentration | -0.5% | Global, China-centric | Medium term (2-4 years) |

| Fire-safety compliance costs in e-mobility | -0.4% | North America, Europe | Medium term (2-4 years) |

| MLCC competition below 100 V | -0.6% | Consumer electronics | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polypropylene and Aluminum Prices

Polypropylene resin accounts for nearly half of capacitor Bill-of-Materials, leaving profitability exposed to petrochemical cycles. In early 2024, prices spiked before easing as additional refinery streams came online, squeezing quarterly margins for second-tier producers. Aluminum foil costs followed energy-price swings, further complicating forecasting. Large vendors hedge through multi-quarter contracts and own film extrusion lines, but smaller firms lack leverage, raising consolidation pressure. Sudden commodity jumps risk lengthening customer lead times as vendors reprioritize allocations toward higher-margin orders. Although resin prices stabilized by late 2025, commodity super-cycles remain an ever-present threat.

Supply-Chain Concentration in BOPP Film Extrusion

Natural disasters, trade sanctions, or logistics blockades therefore ripple rapidly through capacitor supply chains. European capacity additions, such as a recent 36,000-tonne line in Germany, help diversify sourcing, but equipment lead times exceed 18 months. Custom metallization and inline plasma treatments needed for high-voltage grades further restrict the qualified supplier pool. Vendors mitigating risk through dual sourcing and in-house metallization enjoy tighter quality control yet incur higher capital intensity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Polypropylene Retains Scale While PPS Climbs into High-Heat Niches

Polypropylene held 65.55% of the plastic film capacitors market share in 2025, a result of favorable cost-to-performance ratios and mature extrusion know-how. The segment generated the bulk of the plastic film capacitors and is set to expand steadily alongside mainstream automotive inverters. PPS films, meanwhile, are charted to grow 5.63% annually, boosted by aerospace and under-hood EV electronics that demand 150 °C endurance. Nanocomposite research validates PPS’s ability to withstand 500 MV/m breakdown stress while maintaining dielectric stability to 200 °C. OEMs gravitate toward PPS for turbo-charged SiC modules where polypropylene derates aggressively above 105 °C. Despite higher material cost, total system savings accrue by eliminating auxiliary cooling or increasing power density.

Polyethylene and polyester continue to service cost-sensitive lighting ballasts and motor-run capacitors, but face substitution from slimmer polypropylene grades. PTFE persists in microwave and RF filters for aerospace thanks to ultralow dissipation factors. Advanced aramid-fiber composites under development target missiles and space power buses operating beyond 200 °C, yet commercial uptake remains niche. ESG priorities are nudging the polypropylene mainstream toward bio-circular feedstocks that cut scope-3 emissions without altering performance, potentially defending its volume advantage well into the forecast horizon.

By Voltage Rating: Mid-Voltage Remains Core as >1 kV Builds Momentum

The 100–1,000 V band captured 53.35% of the plastic film capacitors market size in 2025, catering to EV traction, industrial drives, and telecom power shelves. Design-for-manufacture partnerships keep unit costs competitive, safeguarding volume. Above 1,000 V, penetration is rising at a 4.72% CAGR on the back of solar inverters and HVDC converters connecting wind clusters to grids. High-voltage devices leverage thicker films and edge-folded metallization to deter partial discharge, supporting premium ASPs and double-digit margins. Below 100 V, ceramic encroachment intensifies, yet audio, lighting, and premium SMPS designers still specify film for its benign failure mode and low microphonics.

Forthcoming 800 V EV platforms will gradually shift content into the 600–1,200 V bracket, expanding addressable opportunities. IEC 61071 updates expected in 2026 will codify thermal-cycling and humidity tests more stringently, likely favoring established suppliers with proven dielectric formulations.

By Form Factor: Stack and Box Designs Shrink Volume Without Sacrificing Performance

Radial-leaded parts maintained 39.15% of 2025 revenue, protected by after-market serviceability and legacy through-hole PCB footprints. However, space-constrained EV chargers and 5G radios propel stack and box packages, which condense capacitance by interleaving foils vertically within molded housings. The plastic film capacitors market enjoys a 5.24% CAGR in this sub-segment as module makers embed capacitors directly onto DBC substrates, slashing loop inductance and thermal resistance. Surface-mount offerings answer mid-range density targets but carry solder-reflow stress penalties that require thicker end-spray layers.

Axial cans linger in railway and oil-and-gas gear where mechanical shock profiles dictate symmetric leadouts. Yet the cost of bespoke winding machinery curtails fresh axial capacity builds. In aggregate, form-factor evolution mirrors the electronics industry’s pivot toward 3D packaging and co-packaged power, encouraging capacitor suppliers to co-locate design teams with module houses for faster layout iterations.

By Application: Automotive Dominates Today; Renewables Deliver the Next Leg of Growth

Automotive seized 30.75% of plastic film capacitors market share in 2025 as global xEV sales cleared 15 million units. Each inverter embeds multiple 400–800 V film banks that smooth battery ripple currents up to 600 A. In 2026, automotive demand alone is worth more than USD 793.5 million, and safety-critical functional-safety specs ensure robust ASPs even amid commodity pressure. Renewable-energy systems follow closely, delivering the fastest 5.93% CAGR as utility-scale PV and onshore wind integrate grid-code-mandated DC filters. Capital deployment into energy-storage farms adds another high-voltage-hungry use case.

Telecommunications, buoyed by 5G densification, sustains solid mid-single-digit growth, while industrial automation and HVAC inverters contribute a steady base load. Consumer electronics remain susceptible to MLCC substitution, constraining growth. Aerospace, defense, and medical segments together account for less value but secure a disproportionate profit share because of tight qualification regimes and low failure-tolerance service environments.

Geography Analysis

Asia-Pacific controls 43.80% of 2025 revenue and leads the plastic film capacitors market at a 6.42% CAGR through 2031. China’s cluster of BOPP extruders supplies domestic component winders and exports film worldwide, underpinning cost leadership. India’s USD 24 billion PLI outlay accelerates local capacitor winding and end-device assembly, creating intra-regional supply redundancy. Japan sustains its reputation for premium automotive and industrial grades, leveraging decades of dielectric process know-how. South Korea’s semiconductor fabs spur demand for high-frequency capacitors in power-management units, while Southeast Asian nations attract capacity relocation tied to China-plus-one strategies.

North America remains a technology adopter rather than a volume producer but boasts strong demand in EVs, aerospace, and data-center renewables. Federal incentives under the Inflation Reduction Act are stimulating new battery and inverter lines, indirectly boosting domestic capacitor needs. Europe emphasizes quality and sustainability; German automotive suppliers co-develop stack capacitor arrays with TDK and WIMA to optimize 800 V drive units. RoHS and REACH compliance acts as a natural barrier to low-cost entrants, stabilizing pricing.

South America’s profile is rising as Brazil’s BRL 186.6 billion (USD 35.09 billion) digitalization plan and PADIS incentives cultivate semiconductor and passive production. TDK’s Gravataí site already exports more than 80% of its 600 million units, proving regional competitiveness. The Middle East and Africa are nascent but not negligible. Solar mega-projects such as Saudi Arabia’s NEOM and South Africa’s REIPPP program require large DC-filter banks, drawing global suppliers keen to diversify revenue streams. Currency volatility and infrastructure gaps remain obstacles, but declining PV-levelized costs bode well for gradual adoption.

Competitive Landscape

The plastic film capacitors market features moderate fragmentation. The top five suppliers hold significant market share, giving space for nimble specialists to exploit application niches. TDK leads automotive traction, leveraging in-house film lines and global application-engineering hubs. Vishay strengthened its European high-voltage portfolio by acquiring Birkelbach in late 2024, suggesting continued tactical mergers and acquisitions. Panasonic and Nichicon concentrate on consumer and industrial standard parts, defending share with cost-optimized automated winding.

Specialists such as KEMET (Yageo) and WIMA target high-pulse, high-frequency roles in power modules and audio equipment. Contract manufacturers in Taiwan and mainland China bustle at the low end, supplying white-label capacitors to lighting and appliance brands. Technological differentiation now tilts toward dielectric engineering nanocomposite films, edge-folded electrodes, and solid-resin encapsulation to boost partial-discharge inception voltage. Vendors with materials research and development assets and vertical integration can amortize tooling faster and achieve superior field-failure rates.

Strategically, leading companies invest in regional duplication of critical processes. TDK operates metallization plants in Japan, Europe, and Brazil, while Vishay is evaluating U.S. extrusion to align with reshoring incentives. Sustainability is emerging as a soft competitive moat; suppliers publishing cradle-to-gate carbon footprints are favored in automotive RFQs. Overall, rivalry is intensifying, but technical hurdles and certification cycles continue to moderate price warfare.

Plastic Film Capacitors Industry Leaders

-

Panasonic Holdings Corporation

-

Vishay Intertechnology Inc.

-

KEMET Corporation (Yageo Group)

-

TDK Corporation

-

KYOCERA AVX Components Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Vishay closed the acquisition of Birkelbach GmbH to expand high-voltage film capacitor capabilities for European renewable-energy customers.

- August 2024: TDK released its integrated report detailing the ModCap series that employs bio-circular polypropylene films, allocating 30% of its three-year capex to passive components.

- June 2024: Quantic Electronics broadened the distribution of MIL-qualified film capacitors across North America’s aerospace and defense sector.

- March 2024: TDK reported year-on-year growth in film capacitor revenue despite ICT softness, citing sustained EV and renewable demand in its fiscal Q1 briefing.

Global Plastic Film Capacitors Market Report Scope

The market is defined by the revenue generated from the sale of plastic film capacitors across applications, which include automotive, telecommunications, industrial, aerospace and defense, consumer electronics, and medical, among other applications.

The plastic film capacitors market is segmented by type (polypropylene, polyethylene, polyester and other types (PTFE, PPS, etc.)), applications (automotive, telecommunications, industrial, aerospace & defense, consumer electronics, medical, and other applications), and geography (Americas, Europe, Middle East and Africa, Asia Pacific [excl. Japan & Korea], and Japan & Korea). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Polypropylene |

| Polyethylene |

| Polyester |

| Polytetrafluoroethylene (PTFE) |

| Polyphenylene Sulfide (PPS) |

| Other Dielectric Types |

| <100 V |

| 100V – 1,000 V |

| >1,000 V |

| Radial-leaded |

| Surface-mount |

| Axial |

| Stack and Box |

| Automotive (xEV, Charging) |

| Telecommunications (5G, Datacentre) |

| Industrial Drives and Inverters |

| Aerospace and Defense |

| Consumer Electronics |

| Medical Devices |

| Renewable Energy (PV, Wind) |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Dielectric Type | Polypropylene | ||

| Polyethylene | |||

| Polyester | |||

| Polytetrafluoroethylene (PTFE) | |||

| Polyphenylene Sulfide (PPS) | |||

| Other Dielectric Types | |||

| By Voltage Rating | <100 V | ||

| 100V – 1,000 V | |||

| >1,000 V | |||

| By Form Factor | Radial-leaded | ||

| Surface-mount | |||

| Axial | |||

| Stack and Box | |||

| By Application | Automotive (xEV, Charging) | ||

| Telecommunications (5G, Datacentre) | |||

| Industrial Drives and Inverters | |||

| Aerospace and Defense | |||

| Consumer Electronics | |||

| Medical Devices | |||

| Renewable Energy (PV, Wind) | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the plastic film capacitors market in 2026?

The plastic film capacitors market size is USD 2.58 billion in 2026, on course for USD 3.27 billion by 2031.

What is the forecast growth rate through 2031?

Revenue is projected to increase at a 4.86% CAGR over 2026-2031.

Which dielectric material dominates commercial volumes?

Polypropylene holds 65.55% market share thanks to cost efficiency and robust electrical performance.

Which end-use segment buys the most film capacitors today?

Automotive applications lead with 30.75% share, mainly for EV traction inverters and chargers.

Which region offers the fastest capacity expansion opportunities?

Asia-Pacific grows fastest at a 6.42% CAGR, supported by China’s scale and India’s PLI incentives.

What main risk could constrain near-term supplier margins?

Polypropylene resin price volatility and BOPP film concentration remain the most immediate threats.

Page last updated on: