SWIR Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

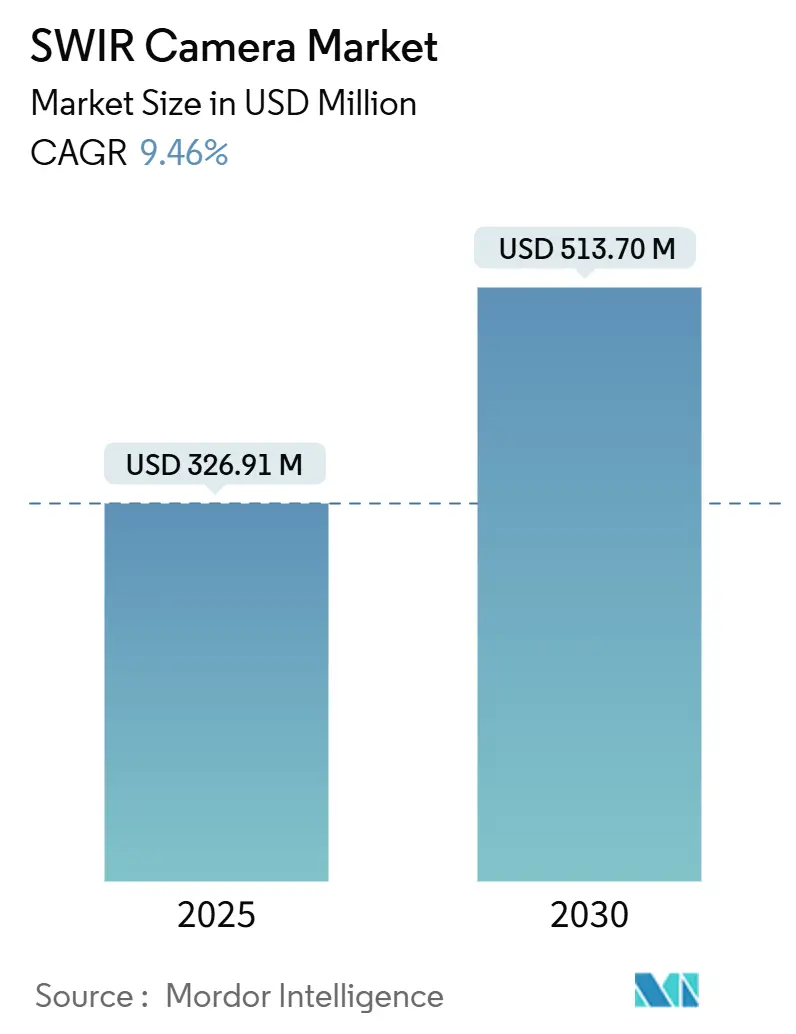

| Market Size (2025) | USD 326.91 Million |

| Market Size (2030) | USD 513.70 Million |

| Growth Rate (2025 - 2030) | 9.46% CAGR |

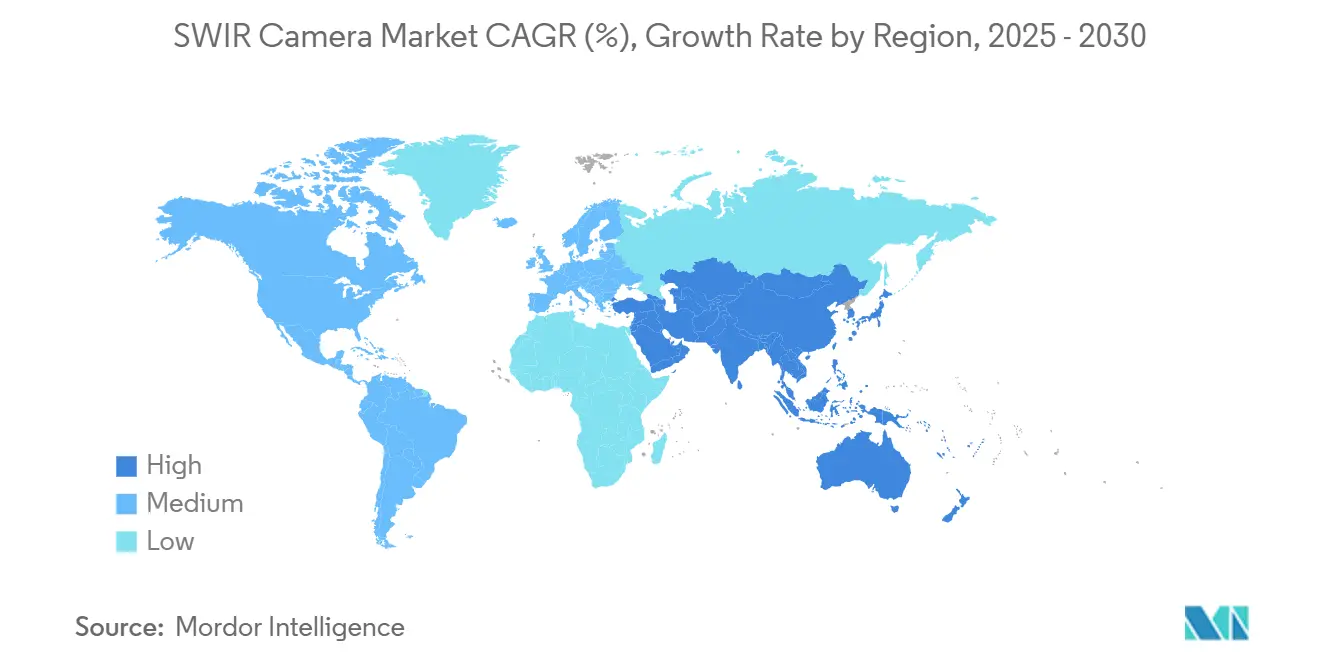

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SWIR Camera Market Analysis by Mordor Intelligence

The shortwave infrared (SWIR) camera market size reached USD 326.91 million in 2025 and is projected to expand to USD 513.70 million by 2030, representing a 9.46% CAGR over the forecast period. Robust momentum flowed from the technology’s migration beyond defense toward semiconductor inspection, plastic‐recycling compliance, and farm-level hyperspectral imaging. Manufacturers have intensified investment in colloidal-quantum-dot sensors that approach the cost structures of visible cameras while sustaining the spectral penetration advantages unique to shortwave infrared. Edge-AI integration, accelerating industrial automation upgrades, and regulatory pressure to improve waste-sorting accuracy collectively reinforced demand. Competitive positioning hinged on vertical integration, detector innovation, and access to ITAR-free supply chains amid tightening export controls.

Key Report Takeaways

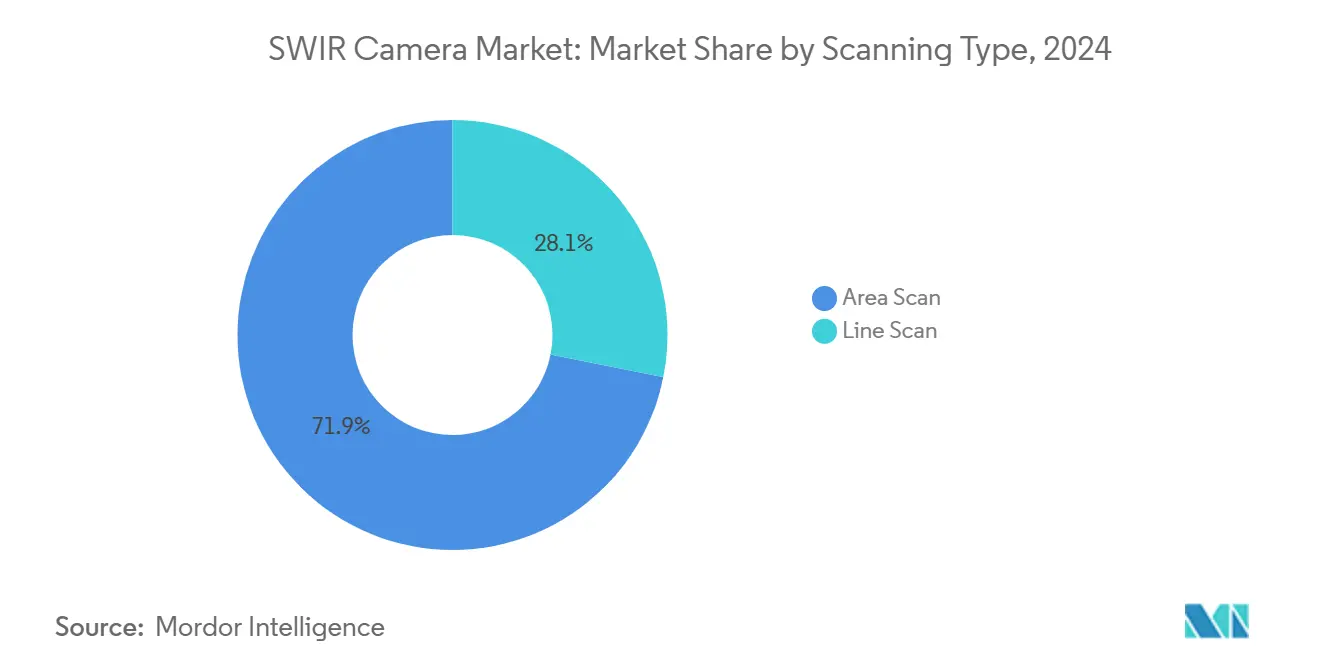

- By scanning type, area scan solutions delivered 71.87% of the shortwave infrared (SWIR) camera market share in 2024; line scan systems are projected to grow at a 10.78% CAGR.

- By detector technology, Indium Gallium Arsenide (InGaAs) maintained an 82.76% share of the shortwave infrared (SWIR) camera market in 2024, whereas Colloidal Quantum Dot (CQD) and Type-II Superlattice are set to expand at a 11.34% CAGR.

- By application, industrial inspection held 39.14% of the shortwave infrared (SWIR) camera market share in 2024, while agricultural monitoring advanced at an 11.14% CAGR through 2030.

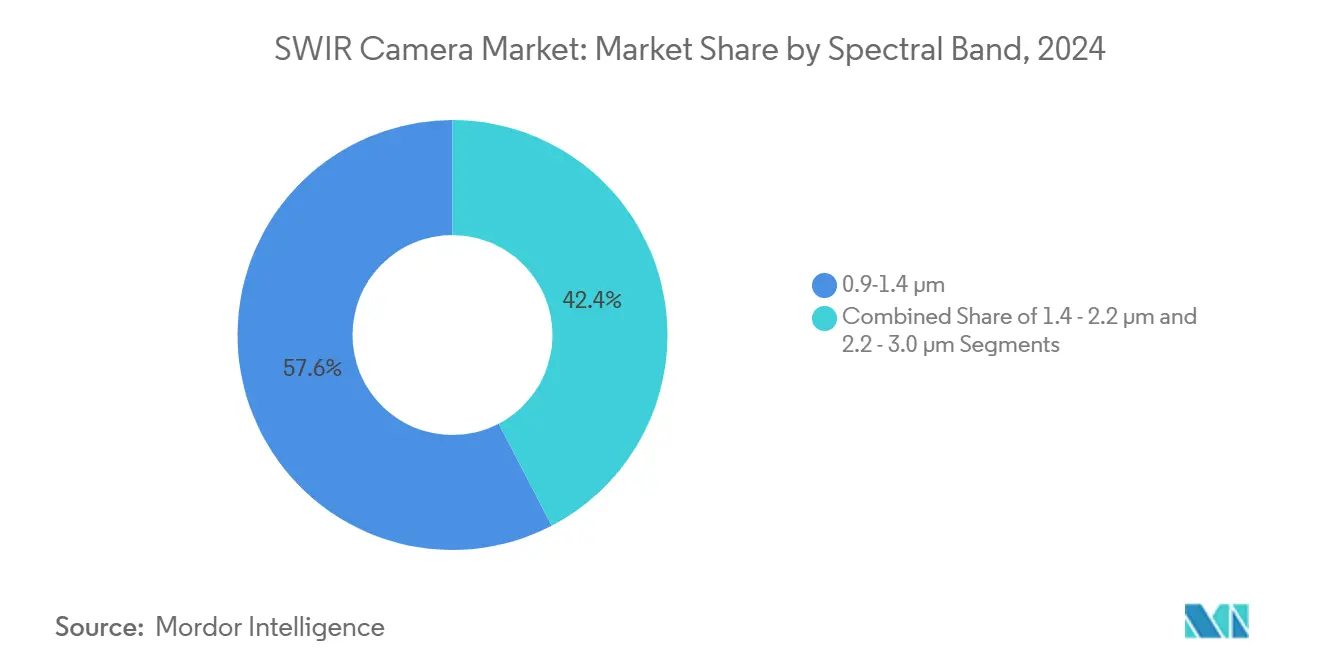

- By spectral band, the 0.9-1.4 µm range captured 57.64% of the shortwave infrared (SWIR) camera market share in 2024; the 2.2-3.0 µm band is forecast to accelerate at an 11.21% CAGR.

- By platform, fixed and mounted systems commanded 54.78% of the shortwave infrared (SWIR) camera market share in 2024; however, UAV/ drone-integrated Payloads are poised for a 10.67% CAGR.

- By geography, North America led the shortwave infrared (SWIR) camera market with 37.15% of the market share in 2024, while the Asia-Pacific region is projected to grow at a 11.28% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SWIR Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption in semiconductor wafer inspection | +1.8% | Global, concentrated in Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Defense night-vision system upgrades | +1.5% | North America and Europe, spillover to allied nations | Long term (≥ 4 years) |

| Regulations mandating NIR sorting for plastic recycling | +1.2% | Europe and North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| Growth of hyperspectral crop-health imaging | +1.0% | Global, early adoption in precision agriculture regions | Medium term (2-4 years) |

| Maturation of colloidal-quantum-dot (CQD) SWIR sensors | +0.9% | Global, led by North America and Europe R&D centers | Long term (≥ 4 years) |

| Edge-AI integration lowering processing latency | +0.8% | Global, concentrated in industrial automation markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption in semiconductor wafer inspection

By 2025, leading fabs relied on SWIR cameras to pinpoint subsurface defects once masked in visible imagery.[1]New Imaging Technologies, “Lisa SWIR – The Ultimate Tool for Semiconductor Inspection,” automate.org Continuous transitions to 300 mm and 450 mm wafers heightened the stakes for yield protection, making short-wave infrared inspection indispensable for volume production. New Imaging Technologies’ NSC1801 sensor delivered 60 kHz line rates that aligned with high-throughput lithography lines, while smaller pixel architectures reduced cost per site tested. Consolidation around mega-fabs intensified quality metrics, elevating SWIR cameras from optional add-ons to baseline process tools. Standardization efforts by equipment vendors further smoothed integration and shortened payback cycles.

Defense night-vision system upgrades

Modernization programs funded by NATO allies retrofitted legacy goggles and riflescopes with dual-band modules marrying thermal and SWIR imagery. Programs such as LRAS3 demonstrated the tactical edge obtained when targets hidden in fog or battlefield smoke reappeared in the SWIR channel. Sensor Unlimited’s Hinted SWIR technology leveraged eye-safe laser illumination to preserve covert operations, an attribute thermal systems lacked. Export-control segmentation created sheltered domestic demand while encouraging ITAR-free variants for broader allied distribution. Procurement roadmaps running through 2030 underscored the long-tail revenue visibility for suppliers.

Regulations mandating NIR sorting for plastic recycling

European Union circular-economy directives effective 2025 compelled waste operators to install advanced spectroscopic sorters able to distinguish polymer grades invisible to visible cameras.[2]SAE Media Group, “Army Researchers Enable Night Lethality,” techbriefs.com Source: Sensors Unlimited, “Plastic Sorting,” sensorsinc.com Line-scan SWIR solutions with 1,024-element arrays resolved black plastics, bridging a critical gap that had depressed recovery values. Accuracy improvements approaching 99.99% reduced contamination fees and sustained higher recycled-resin pricing. Capital-investment certainty grew as compliance deadlines loomed, providing a stable replacement cycle every five to seven years. Comparable legislation progressed through Canadian and U.S. states, widening the addressable base.

Growth of hyperspectral crop-health imaging

UAV-mounted SWIR payloads enabled growers to identify viral stress in potatoes and other high-value crops weeks before visible symptoms emerged. Machine-learning models trained on 400-1,000 nm datasets achieved recall rates of 0.831, guiding variable-rate inputs that trimmed fertilizer consumption and boosted yields. Declining sensor and drone costs lowered entry barriers for service providers bundling analytics and spraying recommendations. Climate volatility magnified the ROI of early disease detection, drawing interest from insurers and ag-credit lenders that subsidized technology adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export controls on dual-use infrared technology | -1.4% | Global, most restrictive in United States allied markets | Long term (≥ 4 years) |

| High InGaAs wafer fabrication costs | -1.2% | Global, concentrated in high-volume applications | Medium term (2-4 years) |

| Thermal-noise management limits on UAV payloads | -0.8% | Global, critical for mobile applications | Short term (≤ 2 years) |

| Competitive encroachment from extended-visible and LiDAR systems | -0.9% | Global, varying by application segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export controls on dual-use infrared technology

Proposed updates to Category XII placed additional focal-plane arrays under ITAR, limiting shipment of high-resolution SWIR modules to non-allied territories. Compliance added licensing delays and legal costs that hampered small exporters. Suppliers such as Xenics responded by launching ITAR-free camera lines, though performance tradeoffs persisted. The regulatory patchwork encouraged production moves to European foundries, seeking friend-shored status and smoother export approval. Over time, the extra friction modestly dampened global CAGR yet simultaneously drove innovation in open-export architectures.

High InGaAs wafer fabrication costs

Indium-gallium-arsenide substrates priced near USD 5,000 per wafer kept bill-of-materials high for mainstream machine-vision systems. Research into reusable GaAs templates hinted at cost relief, but commercial volumes remained tentative in 2025. Consequently, InGaAs adoption clustered in value-dense segments such as wafer inspection or military optics, leaving price-sensitive consumer devices untapped. The gap spurred rapid scaling of colloidal-quantum-dot processes that capitalized on standard CMOS lines and dramatically lower wafer input costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scanning Type: Line Scan Fuels High-Speed Inspection

Line-scan architectures served narrow but expanding use cases where conveyor or web geometry dominated. Although area-scan cameras delivered versatile full-frame capture and retained 71.87% revenue in 2024, the shortwave infrared (SWIR) camera market registered a 10.78% CAGR for line-scan through 2030. New Imaging Technologies’ Lisa SWIR platform underscored the trend, pairing 2,048-pixel arrays with 60 kHz line rates that synced seamlessly with semiconductor and recycling conveyors. Improvements in defect-bonding reduced dead pixels, establishing production yields rivaling area-scan economics. Manufacturers increasingly selected scanning architecture based on process flow rather than optical limitation, a shift that broadened procurement criteria.

Area-scan models remained vital across surveillance, R&D, and scientific imaging, where full-scene context outweighed raw throughput. Suppliers diversified pixel sizes and cooling options, ensuring performance parity with emerging line-scan offerings. The interplay between scanning types fostered healthy competition that drove universal gains in sensitivity and dynamic range.

By Detector Technology: Quantum Dots Challenge the Status Quo

InGaAs remained the incumbent with 82.76% shortwave infrared (SWIR) camera market share in 2024, supported by decades of defense heritage and mature supply chains. Nonetheless, colloidal-quantum-dot sensors delivered an 11.34% CAGR outlook as manufacturers such as STMicroelectronics unveiled 60% quantum efficiency devices at 1.62 µm pixel pitches priced for consumer tiers. Quantum-dot compatibility with 300 mm silicon fabs collapsed cost structures, positioning the technology for smartphone face recognition, automotive cabin monitoring, and emerging AR wearables. Type-II superlattice detectors captured niche scientific and space payloads, leveraging band-gap engineering to extend spectral reach past 3 µm.

While cost advantages weighed in favor of quantum dots, adoption curves hinged on long-term stability, dark current performance, and radiation hardness benchmarks. Tier-one OEMs initiated dual-sourcing strategies that balanced proven InGaAs reliability against disruptive pricing from nanomaterial entrants.

By Application: Agriculture Surges Beyond Traditional Industrial Bases

Industrial inspection anchored 39.14% of 2024 revenue, yet crop-health monitoring led growth at 11.14% CAGR. Machine-vision OEMs bundled multispectral algorithms into turnkey drones and ground rovers, lowering the agronomic expertise threshold for farmers. Surveillance and security progressed steadily on defense budgets, whereas medical imaging pursued vascular-contrast advantages in dentistry and dermatology. Research laboratories exploited expanding detector bandwidths to explore quantum optics and materials science with unprecedented signal-to-noise performance.

Diversification reduced historical reliance on defense procurement cycles and insulated suppliers from geopolitical spending fluctuations. Consequently, the shortwave infrared (SWIR) camera market demonstrated broader economic resilience and attracted venture funding aimed at precision-agriculture analytics and smart-manufacturing startups.

By Spectral Band: Extended Range Unlocks Niche High-Value Cases

The mainstream 0.9-1.4 µm band accounted for 57.64% usage in 2024 due to ready InGaAs availability and established calibration protocols. However, gas-sensing, thermal-imaging, and chemical-analysis tasks demanded 2.2-3.0 µm coverage, yielding an 11.21% CAGR through 2030. Aalto University’s germanium photodiodes raised responsivity by 35% at 1.55 µm, hinting at hybrid material stacks that could straddle mid-IR boundaries cost-effectively.[3]Aalto University, “Novel Photodiode Design Boosts Responsivity,” phys.org Wider spectral options empowered OEMs to tailor cameras precisely to absorptive features of specific gases or polymers, optimizing SNR and reducing algorithmic overhead.

The middle 1.4-2.2 µm band balanced performance and detector cost for applications like moisture analysis in pharmaceuticals and wood products. As detector technology commoditized, spectral-band selection increasingly aligned with application ROI rather than hardware availability.

By Platform: UAV Miniaturization Outpaces Fixed Installations

Fixed installations retained 54.78% share of 2024 revenue, powering established inspection, recycling, and surveillance roles where acoustic camera systems can complement SWIR cameras by identifying sound-based anomalies alongside thermal and optical signatures. Yet drone payloads advanced at a 10.67% CAGR as thermoelectric cooling and phase-change materials mitigated heat buildup in compact airframes. Sensor vendors optimized readout circuits for sub-1.5 W power draw, extending flight endurance without sacrificing frame rate or sensitivity. Portable handheld units filled tactical gaps for field reconnaissance and lab research, leveraging battery advances to reserve full-shift autonomy.

Platform convergence emerged where modular camera cores migrated interchangeably between fixed mounts and UAV gimbals, simplifying logistics and harmonizing software stacks. Integrators capitalized on shared hardware to spread R&D costs across multiple deployment modes.

Geography Analysis

North America held 37.15% of 2024 revenue, anchored by defense budgets, semiconductor capacity, and early adoption in precision agriculture. Onsemi’s acquisition of SWIR Vision Systems and Hamamatsu’s purchase of BAE Systems Imaging Solutions consolidated critical detector IP under regional control. Export regulations sheltered domestic players from certain overseas competitors while fueling R&D into ITAR-free alternatives. The region’s mature OEM ecosystem sustained replacement cycles despite inflationary pressure.

Asia-Pacific recorded the fastest 11.28% CAGR, catalyzed by semiconductor investment in China, memory fabs in South Korea, and agricultural-tech pilots across India and Southeast Asia. Local governments promoted self-reliance in imaging components, channeling subsidies toward quantum-dot and germanium detector startups. Japanese precision equipment makers integrated SWIR modules into metrology tools, leveraging historic optics leadership.

Europe advanced on regulatory urgency around circular-economy directives and climate adaptation. Lynred’s EUR 85 million Grenoble expansion aimed to raise regional detector capacity 50% by 2025, safeguarding supply for ESA and defense programs. Cross-border projects harmonized standards for plastic-sorting infrastructure, supporting stable demand irrespective of macroeconomic headwinds.

Competitive Landscape

Teledyne Technologies, Hamamatsu Photonics, Sony Group, and onsemi represented the most vertically aligned suppliers, collectively controlling 48% of 2024 revenue. Teledyne’s USD 1,502.3 million Q4 2024 sales underscored diversified exposure across defense, space, and industrial machine vision. Acquisitions of Micropac Industries and pending Excelitas assets extended control over mixed-signal ASICs and optics. Hamamatsu deepened its opto-semiconductor portfolio through BAE Systems Imaging Solutions, broadening access to medical and scientific OEMs.

Disruptive entrants such as Emberion raised EUR 6 million to scale nanomaterial imagers priced an order of magnitude below InGaAs peers. Valeo and Teledyne FLIR partnered on automotive thermal perception, signaling long-term bets on multispectral fusion for ADAS safety. Competitive advantage increasingly derived from software ecosystems; Lynred’s LTB suite accelerated sensor integration while locking in customers through tailored calibration routines.

Export-control uncertainty and cost pressure encouraged OEMs to dual-source detectors, softening any single supplier’s dominance. The resulting balance fostered innovation yet kept pricing rational, defining a moderately concentrated environment.

SWIR Camera Industry Leaders

Teledyne Technologies Incorporated

Hamamatsu Photonics K.K.

Sony Corporation

Lynred

Allied Vision Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hamamatsu Photonics completed acquisition of BAE Systems Imaging Solutions, expanding CMOS and SWIR capabilities.

- November 2024: Lynred delivered infrared detectors for ESA’s MTG mission, securing 20-year operational support.

- October 2024: Imperx introduced a new SWIR camera family targeting machine-vision lines.

- July 2024: Teledyne FLIR won a USD 15 million contract to supply ThermoSight HISS-XLR sights to a NATO partner.

Global SWIR Camera Market Report Scope

The Shortwave Infrared (SWIR) Camera Market Report is Segmented by Scanning Type (Area Scan, and Line Scan), Detector Technology (Indium Gallium Arsenide (InGaAs), Mercury Cadmium Telluride (MCT), Colloidal Quantum Dot (CQD) and Type-II Superlattice), Application (Industrial Inspection, Surveillance and Security, Scientific Research, Medical and Life-Sciences, Agricultural Monitoring, Other Application), Spectral Band (0.9 - 1.4 µm, 1.4 - 2.2 µm, 2.2 - 3.0 µm), Platform (Fixed / Mounted Systems, Handheld and Portable Cameras, UAV / Drone-Integrated Payloads), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Area Scan |

| Line Scan |

| Indium Gallium Arsenide (InGaAs) |

| Mercury Cadmium Telluride (MCT) |

| Colloidal Quantum Dot (CQD) and Type-II Superlattice |

| Industrial Inspection |

| Surveillance and Security |

| Scientific Research |

| Medical and Life-Sciences |

| Agricultural Monitoring |

| Other Application |

| 0.9 - 1.4 µm |

| 1.4 - 2.2 µm |

| 2.2 - 3.0 µm |

| Fixed / Mounted Systems |

| Handheld and Portable Cameras |

| UAV / Drone-Integrated Payloads |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Scanning Type | Area Scan | ||

| Line Scan | |||

| By Detector Technology | Indium Gallium Arsenide (InGaAs) | ||

| Mercury Cadmium Telluride (MCT) | |||

| Colloidal Quantum Dot (CQD) and Type-II Superlattice | |||

| By Application | Industrial Inspection | ||

| Surveillance and Security | |||

| Scientific Research | |||

| Medical and Life-Sciences | |||

| Agricultural Monitoring | |||

| Other Application | |||

| By Spectral Band | 0.9 - 1.4 µm | ||

| 1.4 - 2.2 µm | |||

| 2.2 - 3.0 µm | |||

| By Platform / Form Factor | Fixed / Mounted Systems | ||

| Handheld and Portable Cameras | |||

| UAV / Drone-Integrated Payloads | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the shortwave infrared (SWIR) camera market in 2030?

The market is forecast to reach USD 513.70 million by 2030, reflecting a 9.46% CAGR between 2025 and 2030.

Which region is expected to grow the fastest through 2030?

Asia-Pacific is on track for an 11.28% CAGR, led by semiconductor capacity expansion and agricultural-tech adoption.

Which application segment is expanding most rapidly?

Agricultural monitoring is advancing at an 11.14% CAGR thanks to hyperspectral imaging for crop-health diagnostics.

How dominant are InGaAs detectors today?

InGaAs retained 82.76% share of 2024 revenue, although quantum-dot alternatives are scaling quickly.

Why are line-scan SWIR cameras gaining traction?

Continuous-process industries such as wafer fabrication and recycling require high-speed line rates, driving a 10.78% CAGR for line-scan models.

What impact do export controls have on suppliers?

ITAR and related rules trim global CAGR by an estimated 1.4 percentage points while encouraging development of ITAR-free alternatives.

Page last updated on: