Short Bowel Syndrome Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

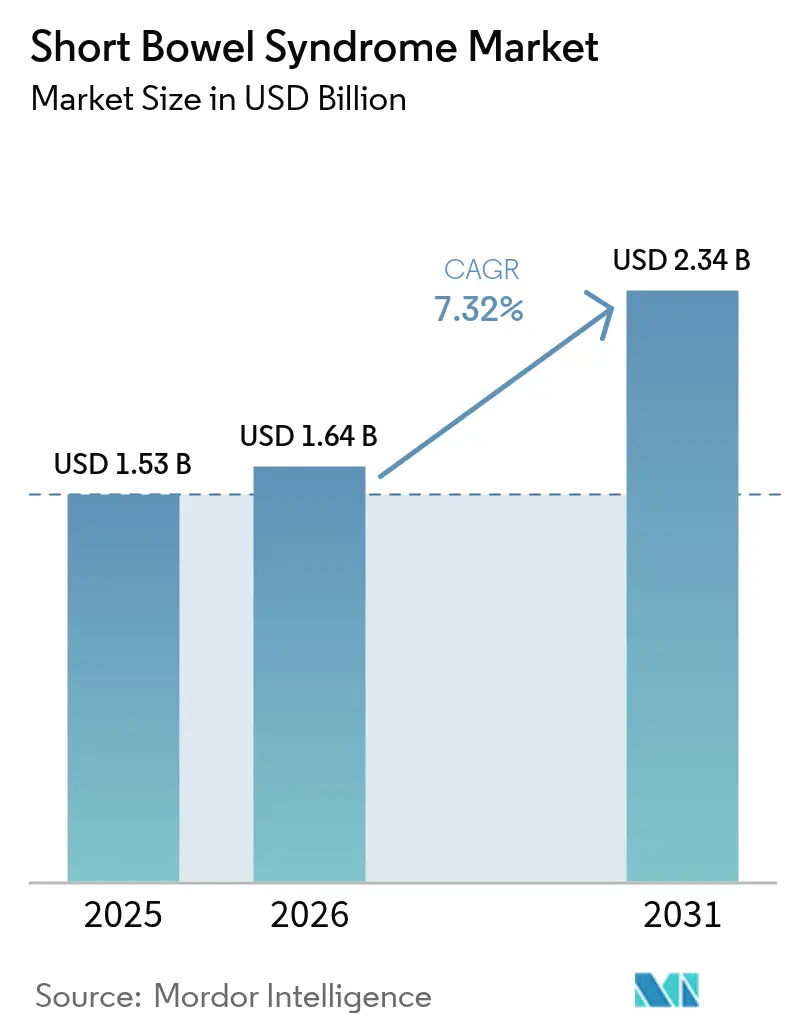

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Short Bowel Syndrome Market Analysis by Mordor Intelligence

The short bowel syndrome market size is expected to grow from USD 1.53 billion in 2025 to USD 1.64 billion in 2026 and is forecast to reach USD 2.34 billion by 2031 at 7.32% CAGR over 2026-2031. Current expansion is propelled by earlier disease recognition, faster orphan-drug approvals, and tissue-engineering breakthroughs that promise anatomical restoration rather than symptomatic relief. New ICD-10 codes introduced by the Centers for Medicare & Medicaid Services (CMS) in October 2023 are uncovering previously unreported cases and widening the treated population. At the same time, digital health platforms are making home parenteral nutrition (PN) feasible for a larger share of patients, lowering inpatient costs and improving adherence. Competitive intensity is moderate because GLP-2 analogs dominate therapy choices, yet manufacturing bottlenecks, long-term safety monitoring, and rising reimbursement scrutiny create palpable risks. Still, regulatory incentives for rare diseases and converging tissue-engineering research are reshaping the Short Bowel Syndrome market outlook over the next five years.

Key Report Takeaways

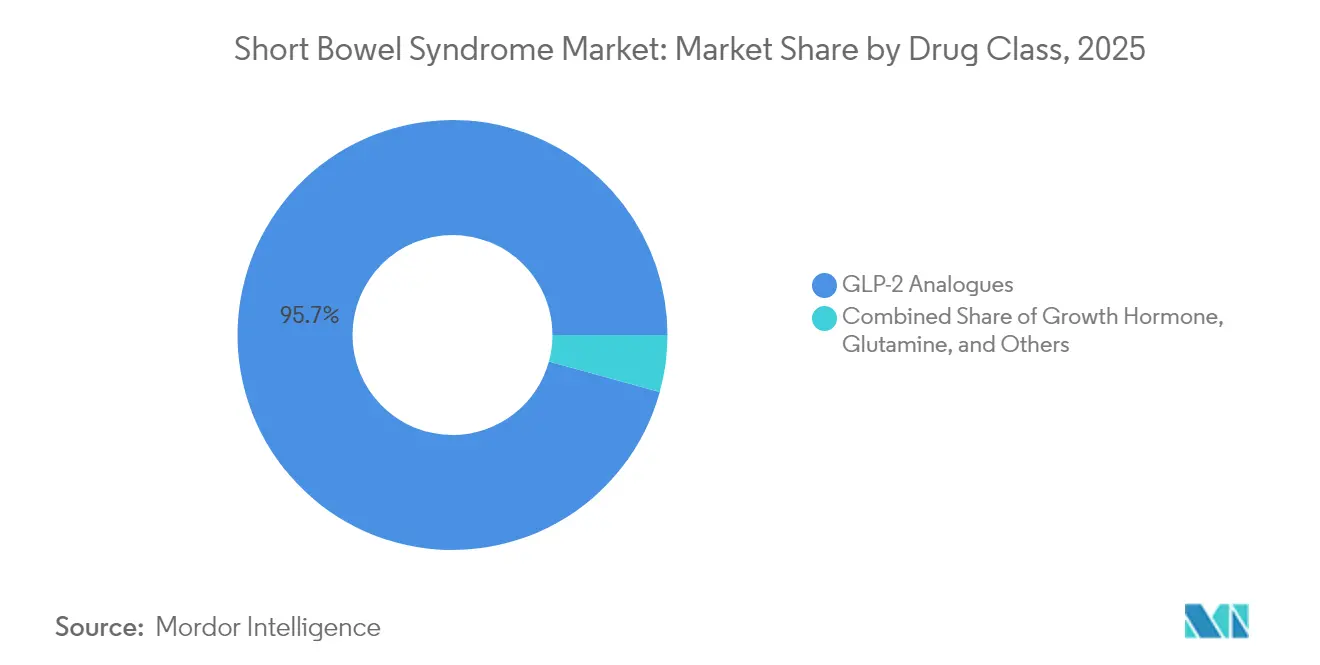

- By drug class, GLP-2 analogs led with 95.72% of Short Bowel Syndrome market share in 2025, while growth hormone therapies are projected to expand at an 7.94% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 55.93% revenue in 2025; online & others are poised for an 8.51% CAGR to 2031.

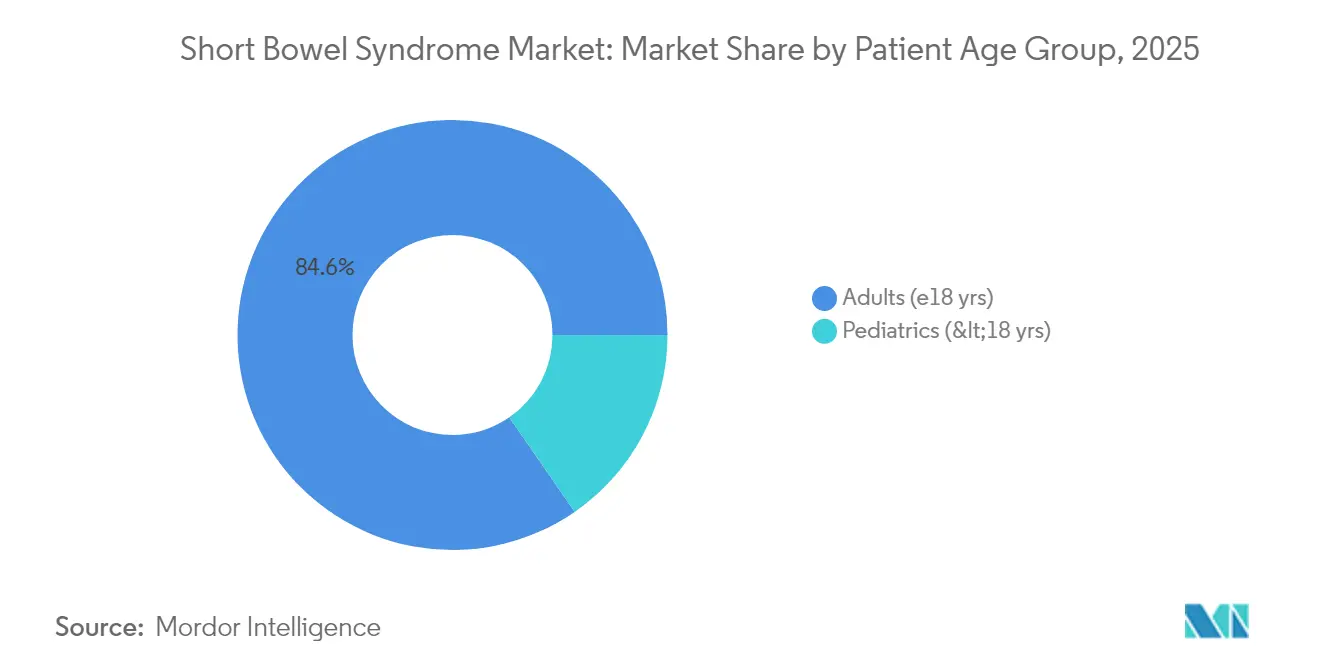

- By patient age, adults accounted for 84.62% of the Short Bowel Syndrome market size in 2025, whereas pediatrics is expected to grow at 8.72% CAGR through 2031.

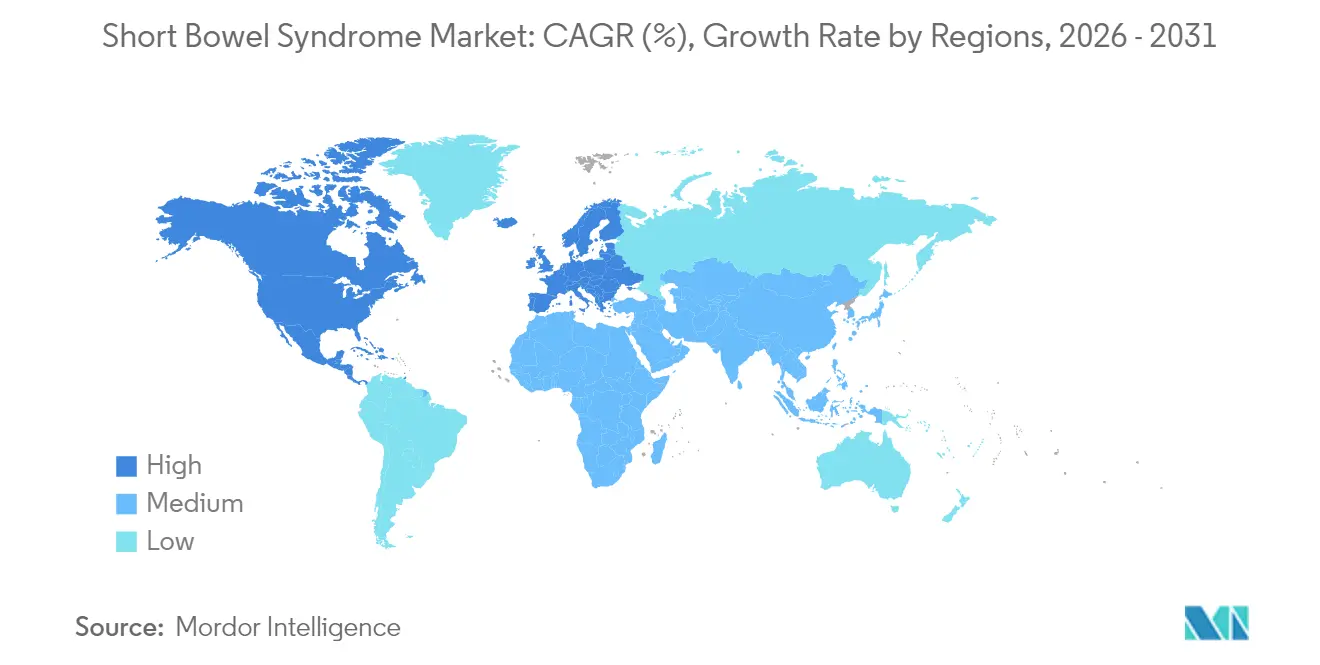

- By geography, North America commanded 42.05% revenue in 2025; Asia-Pacific is set to accelerate at a 8.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Short Bowel Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of SBS & complex GI surgeries | +1.8% | North America & Europe | Medium term (2-4 years) |

| Accelerated approvals & uptake of GLP-2 analogs | +2.1% | North America & EU, APAC | Short term (≤ 2 years) |

| Orphan-drug incentives & favorable reimbursement | +1.4% | North America & Europe | Long term (≥ 4 years) |

| Global patient-registry & NGO awareness initiatives | +0.9% | Global | Medium term (2-4 years) |

| Tissue-engineered intestine R&D breakthroughs | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Remote PN-monitoring digital platforms | +0.6% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of SBS & Complex GI Surgeries

Neonatal surgical advances have lifted survival in very low birth-weight infants, yet they have also pushed neonatal SBS incidence to 22.1 per 1,000 NICU admissions in recent cohorts [1] Journal of Pediatric Surgery Editorial Board, “Short Bowel Syndrome Epidemiology,” sciencedirect.com. Adult incidence is rising for similar reasons: oncologic and inflammatory bowel resections are now more radical, preserving life but shortening bowel length. CMS coding changes in 2023 created visibility for these additional cases, encouraging earlier referrals and stimulating demand for novel therapeutics.

Accelerated Approvals & Uptake of GLP-2 Analogs

The FDA expanded teduglutide to children aged ≥1 year and granted fast-track status to newer molecules such as apraglutide and sonefpeglutide, creating a virtuous cycle of innovation and access. Takeda’s Gattex/Revestive posted JPY 119.3 billion sales in fiscal 2024, up 28.1% year over year [2]Takeda Pharmaceutical Company Limited, “FY 2024 Full-Year Results,” takeda.com. Conversely, Zealand Pharma’s glepaglutide received a Complete Response Letter in December 2024, highlighting the market’s regulatory volatility.

Orphan-Drug Incentives & Favorable Reimbursement

U.S. Medicare covers home PN under Part B when strict criteria are met, and advocacy groups are working to update the three-decade-old policy to widen access [3]Oley Foundation Advocacy Team, “Medicare Home PN Coverage,” oley.org. In Europe, NICE endorsed teduglutide under managed-entry agreements, balancing cost effectiveness with patient need. These incentives enable premium pricing and attract continued investment even as payers demand real-world evidence of PN reduction.

Global Patient-Registry & NGO Awareness Initiatives

Registries coordinated by ESPEN and foundations such as IFFGD generate longitudinal data on safety and quality of life, expediting regulatory filings and reimbursement reviews. Awareness initiatives in emerging markets are crucial, as clinicians historically under-diagnosed SBS because they lacked dedicated codes or training.

Tissue-Engineered Intestine R&D Breakthroughs

Tissue-engineered small intestine constructs restored 98% weight recovery in animal models versus 76% for controls. Colonic SATB2 gene knock-out reprogrammed colon tissue toward small-intestinal function, improving nutrient uptake in preclinical studies. Stem-cell organoids now achieve 17% engraftment after 10 weeks, supporting first-in-human trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & limited access in LMICs | -1.3% | Primarily LMIC regions, some impact in developed markets | Long term (≥ 4 years) |

| Serious long-term safety concerns (e.g., neoplasia) | -0.8% | Global, with regulatory focus in North America & Europe | Medium term (2-4 years) |

| Peptide-manufacturing supply-chain bottlenecks | -1.1% | Global, concentrated in major manufacturing hubs | Short term (≤ 2 years) |

| Disruptive competition from microbiome & surgical innovations | -0.6% | North America & Europe leading innovation, global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Limited Access in LMICs

Total annual therapy costs exceed USD 43,000 per patient when factoring PN, monitoring, and complication management. Many LMIC health systems lack reimbursement frameworks or the cold-chain logistics for GLP-2 analogs. Manufacturers are experimenting with tiered pricing, but infrastructure constraints persist, motivating interest in low-cost peptides or simplified PN regimens.

Serious Long-Term Safety Concerns (e.g., Neoplasia)

GLP-2 analogs mandate baseline and regular colonoscopies because long-term exposure may elevate polyp risk. Hyperamylasemia and hyperlipasemia have also been reported, particularly in pediatric cohorts. Regulators now require extended post-marketing surveillance, raising trial costs and deterring smaller entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: GLP-2 Dominance Faces Innovation Pressure

GLP-2 analogs accounted for 95.72% of the Short Bowel Syndrome market in 2025, propelled by teduglutide’s robust evidence base. Growth hormone therapies, though smaller in absolute sales, are set for 7.94% CAGR through 2031 as pediatric specialists employ them to spur mucosal adaptation. Weekly and monthly GLP-2 candidates like apraglutide and sonefpeglutide seek to reduce injection burden, whereas OPKO Health and Entera Bio are developing the first oral GLP-2 peptide, a shift that could reposition the Short Bowel Syndrome market size for maintenance therapy. Competitive differentiation now centers on dosing convenience, safety, and incremental PN-reduction data to secure payer acceptance and justify premium prices.

Future uptake will hinge on real-world evidence showing durable PN reduction and manageable colonoscopic surveillance. If next-generation molecules confirm similar efficacy with fewer polyps, the Short Bowel Syndrome market could migrate quickly, fragmenting the current GLP-2 oligopoly. Conversely, any class-wide safety signal could redirect investment toward regenerative or gene-editing modalities.

By Distribution Channel: Hospital Dominance Challenged by Digital Shift

Hospital pharmacies held 55.93% revenue in 2025 because SBS management demands multidisciplinary oversight and sterile compounding. Yet online & others channels are scaling at an 8.51% CAGR as home infusion firms integrate telehealth, IoT-connected pumps, and proactive electrolyte monitoring. Studies show 86% of home PN patients own a connected device, and 63% already engage with health apps. If payers continue rewarding hospital-at-home models, the Short Bowel Syndrome market will distribute more prescriptions through specialty mail-order and digital clinics, shrinking hospital share even as volumes grow.

Retail pharmacies focus on ancillary needs such as antidiarrheals and micronutrient supplements. Their participation could expand if oral GLP-2 formulations succeed, yet stringent cold-chain and counseling requirements still favor specialty or infusion channels today.

By Patient Age Group: Adult Stability Contrasts Pediatric Dynamism

Adult patients made up 84.62% of 2025 revenue because oncologic resections and Crohn-related surgeries are more common in later life. This segment has well-defined protocols and centers of excellence, ensuring predictable penetration for every incremental therapy. However, pediatric cases are climbing fastest, with an 8.72% CAGR, due to improved neonatal survival of premature infants with necrotizing enterocolitis. A systematic review reported 36 children achieving enteral autonomy on teduglutide after 24 weeks, while 149 showed reduced PN needs. Pediatric formulations, weight-based dosing, and family-centric digital support platforms are poised to capture new value pools and diversify the Short Bowel Syndrome market share currently anchored in adult care.

Long-term safety monitoring is more stringent in children, so sponsors must generate lifetime exposure data and collaborate with registries. High efficacy in growth metrics and neurodevelopmental outcomes will be decisive for caregiver adoption and payer endorsement.

Geography Analysis

North America generated 42.05% of the Short Bowel Syndrome market in 2025, supported by specialized intestinal-failure centers, Medicare PN reimbursement, and early access to GLP-2 analogs. CMS coding updates and commercial coverage expansions ensure treatment visibility and financial viability, yet payer criteria remain stringent and require documentation of 12-month PN dependence in some plans.

Europe retains critical mass through centralized care networks and harmonized guidelines. NICE’s commercial arrangement for teduglutide and ESPEN’s multidisciplinary standards provide structure and reduce therapeutic variability. EU clinical consortia also drive first-in-human tissue-engineering trials, strengthening the region’s innovation footprint.

Asia-Pacific is the fastest-growing territory at 8.96% CAGR through 2031, driven by regulatory modernization in China and increased resection volumes tied to rising colorectal cancer incidence. China’s 2023 regulations on special-medical-purpose formula expand access to nutritionally balanced enteral feeds, complementing PN and pharmacotherapy. Japan’s inclusion in global apraglutide trials exemplifies the region’s integration into pivotal studies, accelerating time-to-approval for novel agents.

Competitive Landscape

Takeda leads with Gattex/Revestive, in fiscal 2024, affirming its entrenched GLP-2 franchise. Ironwood pivoted its portfolio in 2025 to concentrate on apraglutide, filing an NDA and downsizing non-core projects to streamline capital toward commercialization. Zealand Pharma, recovering from a CRL, is conducting additional histology studies aimed at re-filing in 2026, while Hanmi targets monthly dosing to leapfrog convenience.

Strategic moves emphasize dosing interval, safety reassurance, and integrated care platforms that track PN volume, weight, and electrolyte metrics. VectivBio (now a CSL Behring subsidiary) merged to secure global commercial muscle for its pipeline, signaling potential for further consolidation. OPKO Health and Entera Bio are collaborating on an oral GLP-2 tablet, betting that ease of administration will unlock retail channels and broaden adherence. Digital alliances are equally active: Takeda partners with remote-monitoring firms to embed catheter surveillance and infusion-pump analytics, aiming at fewer catheter-related infections.

If future data validate tissue-engineered constructs, incumbents may license or acquire regenerative start-ups to hedge against GLP-2 exposure. Manufacturing scale-up of complex biologics remains a barrier; hence, companies with peptide production capacity are well placed to capture incremental share as demand climbs.

Short Bowel Syndrome Industry Leaders

TAKEDA Inc

OxThera

VectivBio AG

Ardelyx

Nutricia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2022: VectivBio released positive interim Phase 2 data for apraglutide in adults with SBS.

- June 2022: NICE recommended Takeda’s Revestive (teduglutide) for patients aged ≥1 year with SBS under a commercial arrangement.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the short bowel syndrome therapeutics market as global sales of prescription drugs, chiefly GLP-2 analogs, growth hormone, and adjunct glutamine, used to lessen reliance on parenteral nutrition in patients with markedly reduced functional small intestine. Revenues are captured at ex-manufacturer level and converted to constant 2024 USD across 35 nations we track.

Scope exclusion: We leave out parenteral nutrition equipment, intestinal transplant services, and compounded nutritional supplements.

Segmentation Overview

- By Drug Class

- GLP-2 Analogues

- Growth Hormone

- Glutamine

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online & Others

- By Patient Age Group

- Adults (≥18 yrs)

- Pediatrics (<18 yrs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed gastroenterologists, pediatric surgeons, hospital pharmacists, payer advisers, and home-PN coordinators across North America, Europe, and Asia. These exchanges refined treated-patient pools, average dosing, emerging discounts, and realistic uptake windows.

Desk Research

We mined open clinical sources such as PubMed, Orphanet, ClinicalTrials.gov, the FDA Orphan-Drug database, and Crohn's & Colitis Foundation dashboards for prevalence curves, approval dates, and care pathways. In parallel, UN Comtrade, CMS, and Eurostat discharge files, plus cost-of-illness papers supplied utilization and price anchors, while D&B Hoovers and Dow Jones Factiva offered company-level revenue clues. The sources cited are illustrative; many other datasets underpinned validation.

Market-Sizing & Forecasting

A blended top-down and bottom-up frame funnels disease prevalence into treated cohorts, then tests results against sampled ASP × volume indications from channel checks. Totals are reconciled when variance narrows below 8 percent. Key model drivers include GLP-2 adoption rates, annual resection incidence, parenteral-nutrition days avoided, weighted drug ASP shifts, and orphan-drug exclusivity expiry. A multivariate regression with scenario analysis projects demand to 2030, with experts sense-checking inflection points.

Data Validation & Update Cycle

We run quarterly variance scans versus new prescription audits and safety alerts; outliers trigger re-contact with prior respondents before dual-analyst sign-off. Reports refresh each year and mid-cycle when material events surface, so clients receive the latest view.

Why Mordor's Short Bowel Syndrome Baseline Earns Unmatched Trust

Published SBS figures often differ because firms vary scope, currency year, and refresh pace. According to Mordor Intelligence, key gaps arise when some publishers add parenteral-nutrition hardware or restrict geography to top economies, while others assume flat ASP growth without tracking rebate erosion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.53 B (2025) | Mordor Intelligence | - |

| USD 1.65 B (2024) | Global Consultancy A | Emerging markets omitted; uniform uptake applied |

| USD 1.64 B (2024) | Regional Consultancy B | Price erosion post year 3 ignored |

| USD 2.43 B (2024) | Trade Journal C | Top-7 markets only yet compared as global |

We conclude that our disciplined scope choices, variable-level audits, and timely refresh cadence give decision-makers a balanced, transparent baseline they can replicate with confidence.

Key Questions Answered in the Report

What is the current Short Bowel Syndrome Market size?

The Short Bowel Syndrome Market is projected to register a CAGR of 7.32% during the forecast period (2026-2031)

Who are the key players in Short Bowel Syndrome Market?

TAKEDA Inc, OxThera, VectivBio AG, Ardelyx and Nutricia are the major companies operating in the Short Bowel Syndrome Market.

Which is the fastest growing region in Short Bowel Syndrome Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Short Bowel Syndrome Market?

In 2025, the North America accounts for the largest market share in Short Bowel Syndrome Market.

What years does this Short Bowel Syndrome Market cover?

The report covers the Short Bowel Syndrome Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Short Bowel Syndrome Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: