Shape Memory Polymer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

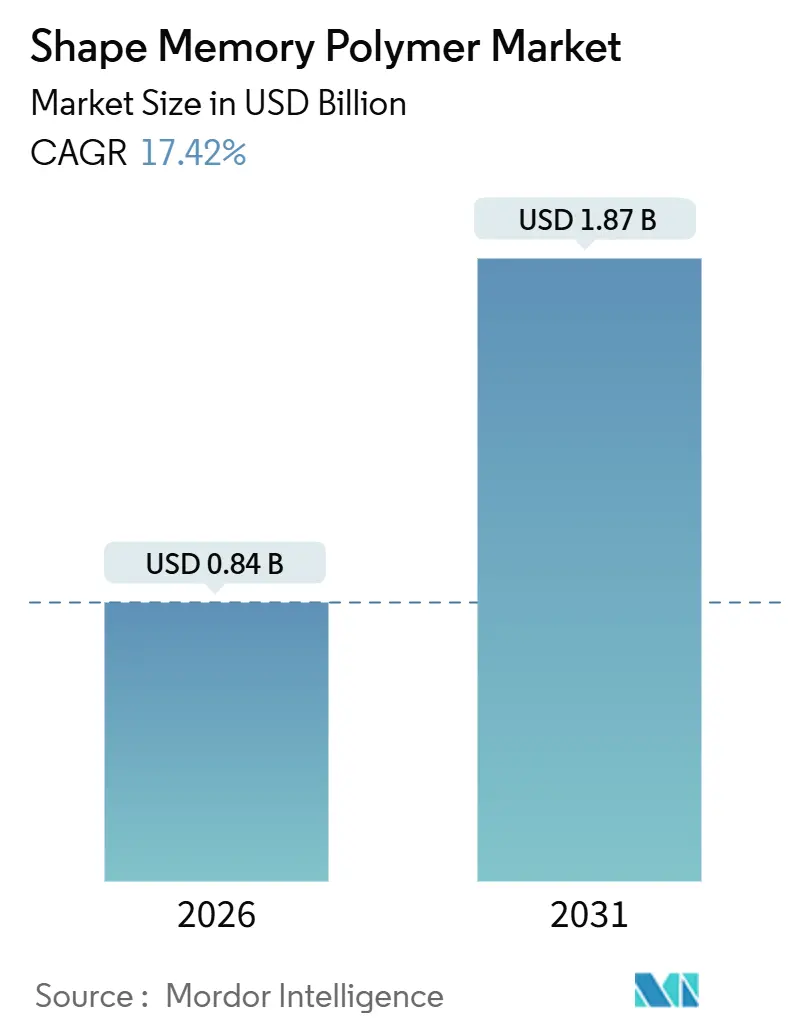

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 17.42% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shape Memory Polymer Market Analysis by Mordor Intelligence

The Shape Memory Polymer Market size is estimated at USD 0.84 billion in 2026, and is expected to reach USD 1.87 billion by 2031, at a CAGR of 17.42% during the forecast period (2026-2031). Growth is accelerating because clinical validation is nudging minimally invasive embolization devices toward mainstream use, additive manufacturing is enabling intricate geometries without tooling, and automotive battery programs are adopting thermal-switch foams to mitigate runaway events. On the demand side, aerospace engineers are iterating morphing wing structures with densities that are a fraction of shape-memory alloys, while infrastructure designers in the Asia-Pacific are trialing self-healing concrete microcapsules to curb maintenance costs. Competitive intensity remains moderate because chemical majors supply base chemistries, but specialized medical-device firms control regulatory know-how. Headline challenges include low rubbery-state stiffness and premium compounding costs, yet 4D-printing breakthroughs and regulatory momentum are easing entry barriers.

Key Report Takeaways

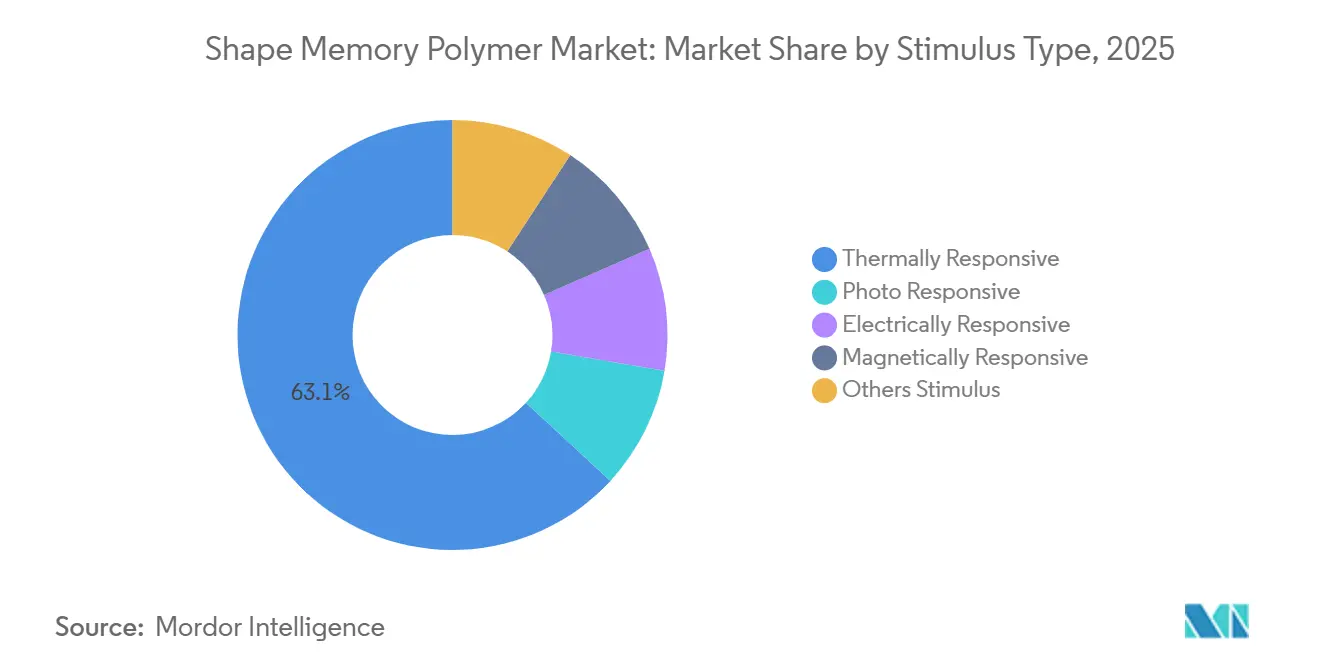

- By stimulus type, thermally responsive materials held 63.14% of the shape memory polymer market share in 2025 and are advancing at a 19.44% CAGR to 2031.

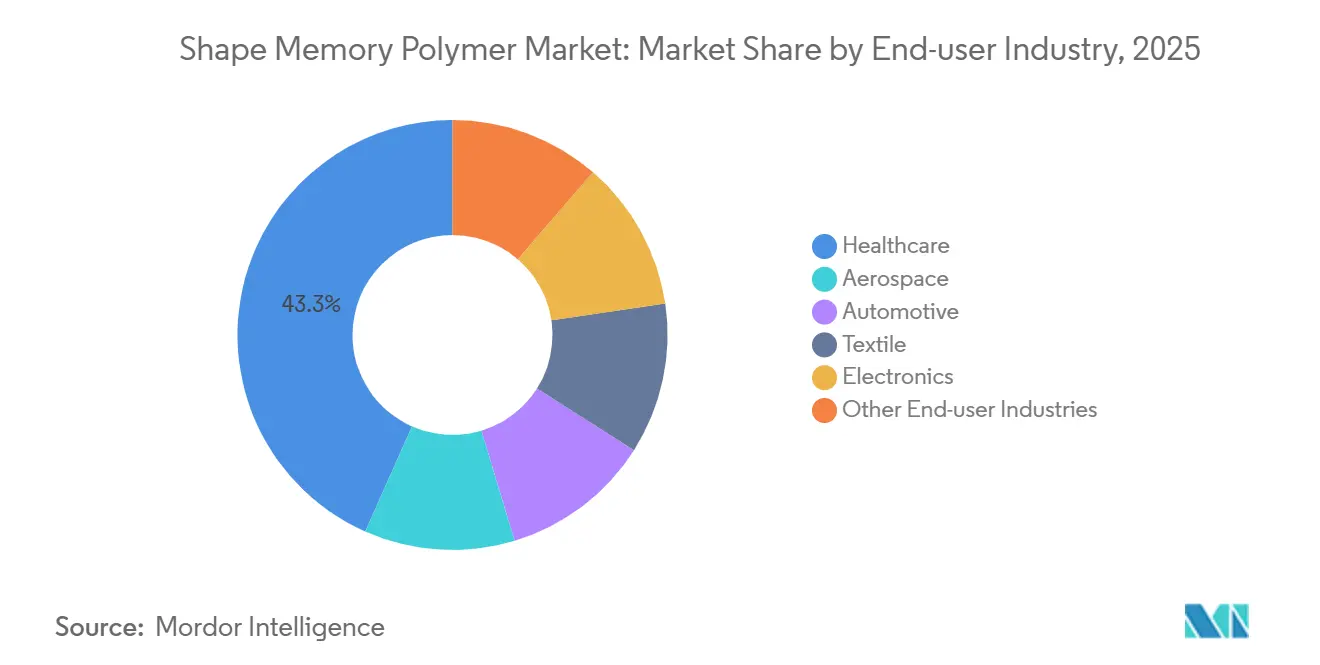

- By end-user industry, healthcare accounted for 43.34% of 2025 revenue and is expanding at a 20.11% CAGR through 2031.

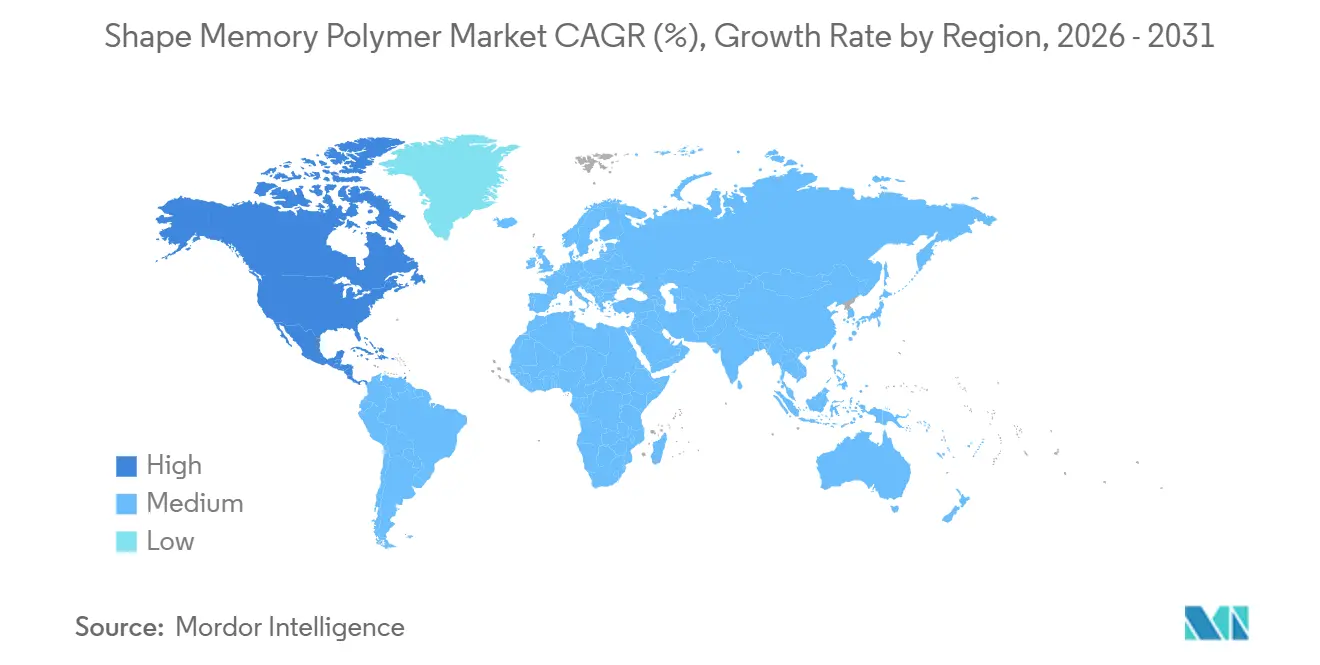

- By geography, North America represented 47.91% of 2025 revenue and is projected to scale at a 57.78% CAGR to 2031, the fastest regional trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shape Memory Polymer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing minimally-invasive medical device adoption | +4.2% | Global, with North America and EU leading regulatory approvals | Medium term (2-4 years) |

| Rapid infrastructure build-out in Asia-Pacific driving self-healing concrete demand | +2.8% | Asia-Pacific core, spillover to Middle-East | Long term (≥ 4 years) |

| Lightweight morphing-structure needs in aerospace and space exploration | +3.1% | North America and Europe, driven by NASA, ESA programs | Long term (≥ 4 years) |

| 4D printing unlocking complex, custom SMP geometries | +3.5% | Global, concentrated in research hubs and medical-device manufacturing | Short-Medium term (≤ 3 years) |

| Thermal-switch foams for EV battery-pack safety and cooling | +2.9% | Global, APAC manufacturing concentration in China, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Minimally Invasive Medical-Device Adoption

Regulators cleared multiple SMP-based embolization systems between 2024 and 2026, bolstering hospital confidence in polymer foams that shorten procedure time and promote clot formation. Shape-memory foams provide radiolucency, low radial force, and porous scaffolds that accelerate sac thrombosis, a clinical edge over metallic coils. Pilot reimbursement codes issued in 2024 eliminated a major coverage barrier, and adherence to ISO 10993 biocompatibility and FDA 21 CFR 820 quality-system rules anchors long-term safety.

Rapid Infrastructure Build-Out in Asia-Pacific Driving Self-Healing Concrete Demand

Emerging highway, port, and rail projects in China and India are testing polymer microcapsules that rupture upon cracking, releasing prepolymers that flow and harden to reseal voids, thereby suppressing water ingress and rebar corrosion. Early field trials report restored compressive strength and a marked decline in permeability, but the absence of standardized codes and the high cost of specialty capsules temper near-term rollouts.

Lightweight Morphing-Structure Needs in Aerospace and Space Exploration

NASA-funded vortex-generator programs have validated polymer morphing structures that shave mass versus nickel-titanium actuators, a compelling metric because every kilogram saved cuts launch costs. A 2024 Nature Communications study combined continuous fibers with SMP matrices, delivering flexural moduli above 10 GPa without sacrificing recovery, moving the material closer to primary-load roles[1]Nature Communications, “Continuous Fiber Reinforced Shape-Memory Polymer Composites,” nature.com.

4D Printing Unlocking Complex, Custom SMP Geometries

Additive manufacturing now prints multi-material SMP lattices that transform in programmed sequences once they cross staged temperature thresholds. Carbon’s digital-light-synthesis platform can cure SMP parts directly from CAD, sidelining molds and trimming lead times from months to days, a leap that accelerates clinical trial enrollment and aerospace prototyping.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Relatively low stiffness in rubbery state versus metals and composites | -1.8% | Global, particularly aerospace and automotive structural applications | Medium-Long term (3-5 years) |

| High production and compounding costs | -2.2% | Global, acute in emerging markets with limited specialty-polymer supply chains | Short-Medium term (≤ 3 years) |

| Water-induced premature actuation in biomedical implants | -1.1% | Global, concentrated in cardiovascular and neurovascular device segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Relatively Low Stiffness in Rubbery State Versus Metals and Composites

In 2024 lab tests, continuous carbon-fiber reinforcement elevated the flexural stiffness of unreinforced SMPs. However, this advancement came at the expense of increased material costs and heightened process complexity. Unreinforced SMPs, which soften above their glass-transition temperature, exhibit elastic moduli significantly lower than those of aluminum alloys. Meanwhile, hybrid architectures are now adept at segregating load paths, enabling polymers to actuate while metals bear the brunt of structural stresses.

High Production and Compounding Costs

Precise control of molecular weight and crosslink density drives up synthesis costs compared with commodity thermoplastics. Specialty PA12 powders for additive manufacturing command premiums because they require tight particle-size distribution and low residual monomer content. Supply-chain gaps in South America and Middle East-Africa magnify freight and tariff overheads, doubling unit prices in some pilot projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Stimulus Type: Thermal Dominance Reflects Activation Simplicity

Thermally responsive polymers captured 63.14% of the shape memory polymer market in 2025, and this cohort is forecast to expand at a 19.44% CAGR through 2031. The segment’s advantage lies in glass-transition and melting-crystallization switches that use existing heating elements, avoiding lasers or magnets. A 2021 MDPI study demonstrated melt-spun polycaprolactone-TPU fibers that delivered 99% strain recovery at 50 °C, validating durability for adaptive garments[2]MDPI, “Functionalized Polymers from Lignocellulosic Biomass,” mdpi.com.

Photo-responsive designs remain confined to thin-wall microfluidics because UV penetration fades in thick sections, while electrically responsive grades embed carbon nanotubes to induce Joule heating, a tactic that raises brittleness and complicates recycling. Magnetically responsive resins integrate nanoscale ferrites, enabling remote actuation via alternating fields, yet the extra coils inflate system cost and restrict use to surgical and aerospace niches. Moisture-activated and pH-triggered chemistries round out the portfolio, serving drug-delivery scaffolds and adaptive packaging. Overall, straightforward activation infrastructure keeps thermal grades in pole position for high-volume medical and automotive output, reinforcing their leadership in the shape memory polymer market.

By End-User Industry: Healthcare Monetizes Clinical Validation

Healthcare generated 43.34% of 2025 revenue and is advancing at a stout 20.11% CAGR through 2031, cementing its role as the growth engine of the shape memory polymer market. Polymer embolization plugs now carry FDA 510(k) clearance for peripheral obstruction and EU MDR Class III certification, creating a moat that slows metallic-coil competitors. Orthopedic trauma implants also leverage SMP hinges that expand in situ, shortening surgery times and lowering revision risk.

Aerospace ranks second, energized by NASA-Boeing morphing projects and a growing queue of satellite deployable-boom programs. Automotive engineers focus on thermal-switch foams for EV battery modules and adaptive aerodynamic flaps that deploy only at highway speeds, shaving drag without motors. Textiles exploit melt-spinning to deliver compression garments that react to body heat, while electronics researchers prototype shape-memory actuators and flexible antennas. Construction and packaging remain exploratory, awaiting standardized codes and cost-down trajectories before large-scale rollouts.

Geography Analysis

North America dominated 2025 revenue with a 47.91% slice of the shape memory polymer market and is forecast to escalate at a remarkable 57.78% CAGR through 2031. The United States hosts a vibrant ecosystem of venture investors, additive-manufacturing startups, and FDA-approved device makers. Carbon’s USD 60 million capital raise in 2025 is funding the expansion of resin libraries and print-farm capacity, a signal that domestic demand for high-performance SMP parts is outstripping supply. NASA and the Department of Defense co-finance morphing-structure programs, further cementing regional leadership. Canadian universities contribute polymer chemistry breakthroughs, while Mexico’s maturing EV supply chain presents an avenue for thermal-switch foams as nearshoring accelerates.

Asia-Pacific trails closely, propelled by China’s electric-vehicle output, Japan’s material-science expertise, and India’s infrastructure push. Japanese chemical major Asahi Kasei introduced an automotive thermoplastic elastomer in 2024 that targets lightweighting and heat management, hinting at future SMP formulations. Evonik doubled production of long-chain polyamides in Shanghai during 2025, eyeing additive-manufacturing customers in mainland China and Southeast Asia. South Korea’s battery giants LG Energy Solution and Samsung SDI are piloting polymer thermal foams for next-generation packs, although public technical data remains limited. India’s highway build-out fuels interest in self-healing concrete microcapsules, but code committees have yet to publish performance benchmarks for SMP-cement composites.

Europe occupies the third slot, buoyed by stringent MDR and REACH frameworks that favor suppliers with robust quality-management systems. Shape-memory embolization plugs gained EU MDR Class III clearance in 2025, opening the 27-state European Economic Area to polymer alternatives. Airbus is evaluating morphing trailing-edge panels fashioned from continuous-fiber SMP composites, and Germany’s Fraunhofer IAP unveiled contract research and development services for SMP synthesis and prototype fabrication in 2025. Nordic defense suppliers are assessing low-outgassing SMP hinges for small-sat dispersion, while the United Kingdom’s Catapult centers align polymer experts with aerospace primes.

South America and the Middle-East, and Africa remain nascent contributors. Brazil’s aerospace cluster around Embraer is funding feasibility work on SMP morphing flaps, but the lack of local specialty-polymer production inflates raw-material costs. Saudi Arabia’s Vision 2030 mega-projects could provide test beds for self-healing infrastructure, yet import reliance and limited testing facilities impede speed-to-market. Across both regions, regulatory pathways for medical devices are less defined, discouraging companies from prioritizing early filings.

Value Chain Analysis

The shape memory polymer (SMP) value chain starts with specialty monomers, crosslinkers, catalysts, and additives that enable tight control of molecular weight and crosslink density, followed by resin synthesis by chemical producers and specialized SMP material suppliers. Downstream, compounders and converters tailor activation temperature windows and recovery force through fillers, copolymerization, and formulation packages, then apply shape-setting and programming steps that lock in temporary shapes. Processing routes span injection molding, extrusion and melt-spinning, and additive manufacturing workflows (including photopolymer platforms) that shorten iteration cycles for intricate geometries.

Value capture concentrates in application engineering, qualification, and regulated device or mission-critical part fabrication rather than base resin alone, which pushes the ecosystem toward co-development and selective vertical integration. Medical devices add a parallel chain of design controls, biocompatibility testing, and quality-system documentation before hospital adoption. Aerospace and space programs impose outgassing and performance verification requirements that favor experienced suppliers. Bottlenecks center on the availability and cost of specialty inputs (and energy-intensive synthesis), along with access to equipment and know-how to manage SMP-specific thermal and rheological behavior. This has encouraged partnerships such as Graphy and FUGO Precision 3D (January 2026) to build scalable manufacturing infrastructure for shape-memory aligners.

Competitive Landscape

The shape memory polymer market is moderately consolidated. Vertical integration is rare; most actors specialize in resin synthesis, compounding, device fabrication, or additive-manufacturing services. Carbon’s print-farm model positions it as a platform disruptor because hospitals and aerospace OEMs can procure custom SMP parts without investment in molds or dies. White-space opportunities cluster around magnetically and electrically responsive polymers for soft robotics, as well as cellulose-nanowhisker composites that trigger with moisture rather than heat. Barriers to entry center on ISO 10993 biocompatibility for implants, ASTM E595 outgassing for spacecraft, and the statistical stability demanded by EU MDR audits, factors that collectively favor incumbents with seasoned regulatory teams.

Shape Memory Polymer Industry Leaders

BASF SE

Covestro AG

Evonik Industries AG

SMP Technologies Inc.

Composite Technology Development Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The largest near-term whitespace remains in translating SMP performance from prototypes into repeatable, qualified production in healthcare and other high-value engineered parts, where clinical evidence and manufacturing scalability support broader purchasing adoption. In endovascular medicine, Shape Memory Medical began enrollment in its FLAGSHIP study in April 2026 to evaluate a false lumen embolization system for aortic dissection. The AAA-SHAPE pivotal trial completed enrollment in July 2026, with 180 patients across 48 centers, for an SMP-based endovascular embolization technology. These milestones broaden the evidence base and create pull-through demand for medical-grade SMP foams, particularly from suppliers that can deliver consistent porosity control, sterilization compatibility, and ISO 10993-aligned materials support.

Manufacturing-led opportunities are also emerging where 4D printing consolidates multi-part assemblies into monolithic SMP components, reducing tooling needs and assembly steps for aerospace and space hardware and speeding up design iteration. Trade and technical reporting in 2026 highlighted self-deploying space structures using 4D-printed, shape-memory PEEK components for orbital mechanisms, which reinforces demand for higher-temperature SMP chemistries and qualified additive workflows. Additional whitespace sits in electrically and magnetically responsive SMPs for soft robotics and niche actuation, and in infrastructure microcapsule systems for self-healing concrete in Asia-Pacific, where field trials are active but standardized codes and cost-down pathways still constrain rollout.

Recent Industry Developments

- July 2026: Shape Memory Medical completed enrollment of 180 patients across 48 centers globally in the AAA-SHAPE pivotal trial evaluating its Impede FX RapidFill endovascular embolization technology that uses shape memory polymer. Completing enrollment advances clinical validation toward broader physician adoption and strengthens the companys position in regulated SMP-based embolization devices.

- April 2026: Shape Memory Medical began patient enrollment in the FLAGSHIP study to evaluate its investigational False Lumen Embolization (FLE) System for aortic dissection treatment. The study expands the pipeline of SMP-enabled vascular indications and increases demand for consistent, medical-grade polymer foam performance and manufacturing controls.

- January 2026: Graphy announced an exclusive strategic partnership with FUGO Precision 3D to establish mass production infrastructure for shape memory aligners using its proprietary photopolymer materials. The move targets scalable dental-manufacturing throughput and signals deeper integration of SMP formulations with dedicated production capacity for high-volume, customized devices.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from shape memory polymers (SMP) that can be deformed and then recover a programmed shape when exposed to a trigger. The sizing is split across major regions based on where SMP are sold and where they are used.

Scope exclusions: The sizing excludes shape memory alloys and other shape memory materials that are not polymer-based, even if they serve similar end uses.

Segmentation Overview

- By Stimulus Type

- Thermally Responsive

- Photo Responsive

- Electrically Responsive

- Magnetically Responsive

- Others Stimulus

- By End-user Industry

- Aerospace

- Automotive

- Textile

- Electronics

- Healthcare

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear fact base on where SMP demand comes from and what drives adoption, and then it is used to set realistic constraints for the model. We leaned on public sources such as the United States Patent and Trademark Office and similar patent offices, the US Food and Drug Administration device databases for medical use cases, NASA and other government aerospace publications, and peer-reviewed polymer science journals for material performance and readiness signals.

Alongside this, we reviewed company annual reports, investor decks, association websites, and reputable press coverage to understand product launches, capacity adds, and application priorities. When needed, paid subscriptions for company financials, patent lookups, and shipment-level trade statistics were used to cross-check revenue scale and trade flows for relevant resin and compound categories. The desk sources listed here are illustrative only, and many other public references were used to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary work was used to test the desk assumptions and adjust the numbers to what is actually shipped, qualified, and consumed, especially in healthcare, aerospace, automotive, electronics, and textile use cases. We spoke with a mix of material suppliers, compounders, converters, and downstream users, and then we validated the pricing logic and trigger types (thermal, photo, electrical, magnetic) with technical and commercial respondents across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 47% |

| Mid tier: 58% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 16% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

The core sizing uses a top-down and bottom-up logic, where demand is reconstructed from end-use pull and then checked against supply-side reality. On the top-down side, we start from end-use activity and adoption signals in healthcare devices, aerospace components, and industrial uses, then apply penetration and usage factors to arrive at an addressable consumption pool by region.

To keep the model practical, the inputs focus on a short list of variables that can be defended on a client call. Typical drivers include the share of SMP used by stimulus type (thermal versus photo or electrical), the pace of qualification cycles in aerospace and medical applications, average selling price ranges by polymer family and form factor, and regional manufacturing and import patterns that affect availability. Where public data is thin, gaps are handled through bounded assumptions that are stress-tested in interviews, then adjusted using selective bottom-up approximations such as sampled supplier revenues, channel checks, and ASP times volume builds for the most visible applications.

For forecasting, scenario analysis is used so upside and downside cases can be tied to adoption speed in healthcare and aerospace, price normalization as volumes scale, and the pace of new product development. The final trajectory is reviewed with primary experts so the drivers, not just the CAGR, stay consistent year to year.

Data Validation & Update Cycle

Validation is done by checking the modeled totals against independent signals, such as trade movement patterns, patenting intensity trends, and the pace of new application announcements, then reviewing any values that fall outside reasonable ranges. When a variance is found, the assumptions are revisited, outliers are rechecked, and respondents are re-contacted if the issue is material to the total or a key region.

Before sign-off, a multi-step analyst review is completed so the same logic is applied across regions and end uses, and the units and currency conversions are consistent. Reports are refreshed annually, with interim updates when large events occur, such as meaningful capacity changes, regulation-driven shifts in medical demand, or sharp price movements. Right before delivery, we run a quick final pass so clients receive the most current view available.

Mordor Intelligence's Shape Memory Polymer Market Sizing Compared With Other Published Estimates

Published market sizes for shape memory polymers often do not align because each publisher selects its own base year, time window, and definition of what counts as an SMP sale versus an adjacent smart polymer or shape memory material. Differences also show up when one study starts from shipment output in kilotons and then converts to value, while another starts from value and applies a separate pricing curve.

In this study, part of the spread comes from how the demand pool is tied to stimulus-type use and end-user qualification timelines, not just broad smart polymer adoption rates. This approach reduces double counting across similar functional polymers, which is a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.84 B (2026) | |

| Global Publisher A | USD 0.98 B (2024) | Uses a 2024 base year and leans on shipment output and revenue reporting together, which can lift totals when broad type and application buckets pull in overlapping demand signals. |

| Market Platform B | USD 0.90 B (2024) | Segments heavily by form and end use and projects a long forecast window, and the earlier base-year pricing assumptions can diverge if ASP changes and qualification timing are not rechecked with users. |

Looking at the table, the main differences are timing and counting rules, not a disagreement that SMP demand is growing. By keeping the scope tightly within polymer-based shape memory products and then validating key adoption and price assumptions with interviews, the final estimate stays traceable to clear variables that can be repeated in future refreshes.

Key Questions Answered in the Report

How fast is the shape memory polymer market expected to grow through 2031?

The market is forecast to post a 17.42% CAGR between 2026 and 2031, rising from USD 0.84 billion to USD 1.87 billion.

Which stimulus category leads global demand?

Thermally responsive products dominate with 63.14% share in 2025 and an anticipated 19.44% CAGR to 2031.

Why is healthcare the largest application?

Regulatory clearances for embolization plugs and orthopedic implants, coupled with new reimbursement codes, pushed healthcare to 43.34% of 2025 revenue, and the segment is growing at a 20.11% CAGR.

Which region is growing the fastest?

North America is projected to scale at 57.78% CAGR through 2031, powered by robust VC funding, FDA clarity, and defense-backed aerospace projects.

What limits broader SMP adoption in structural roles?

Low stiffness in the heated rubbery state necessitates fiber reinforcement or hybrid designs, which raises cost and process complexity.

Page last updated on: