STD Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

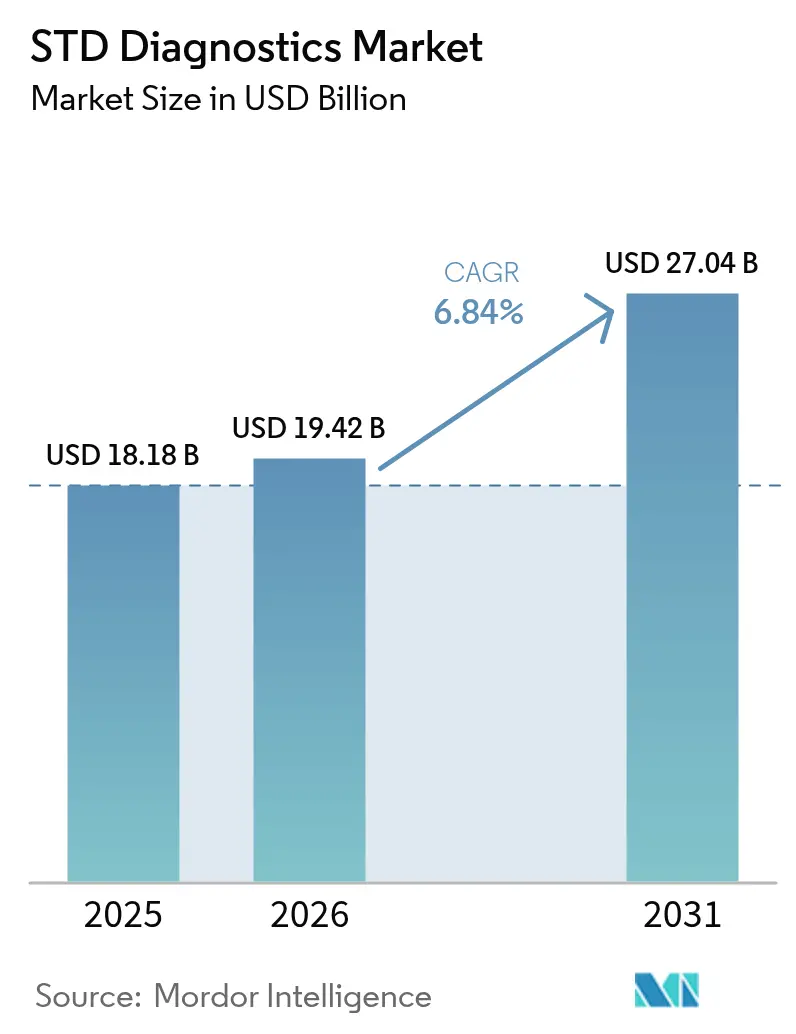

| Market Size (2026) | USD 19.42 Billion |

| Market Size (2031) | USD 27.04 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

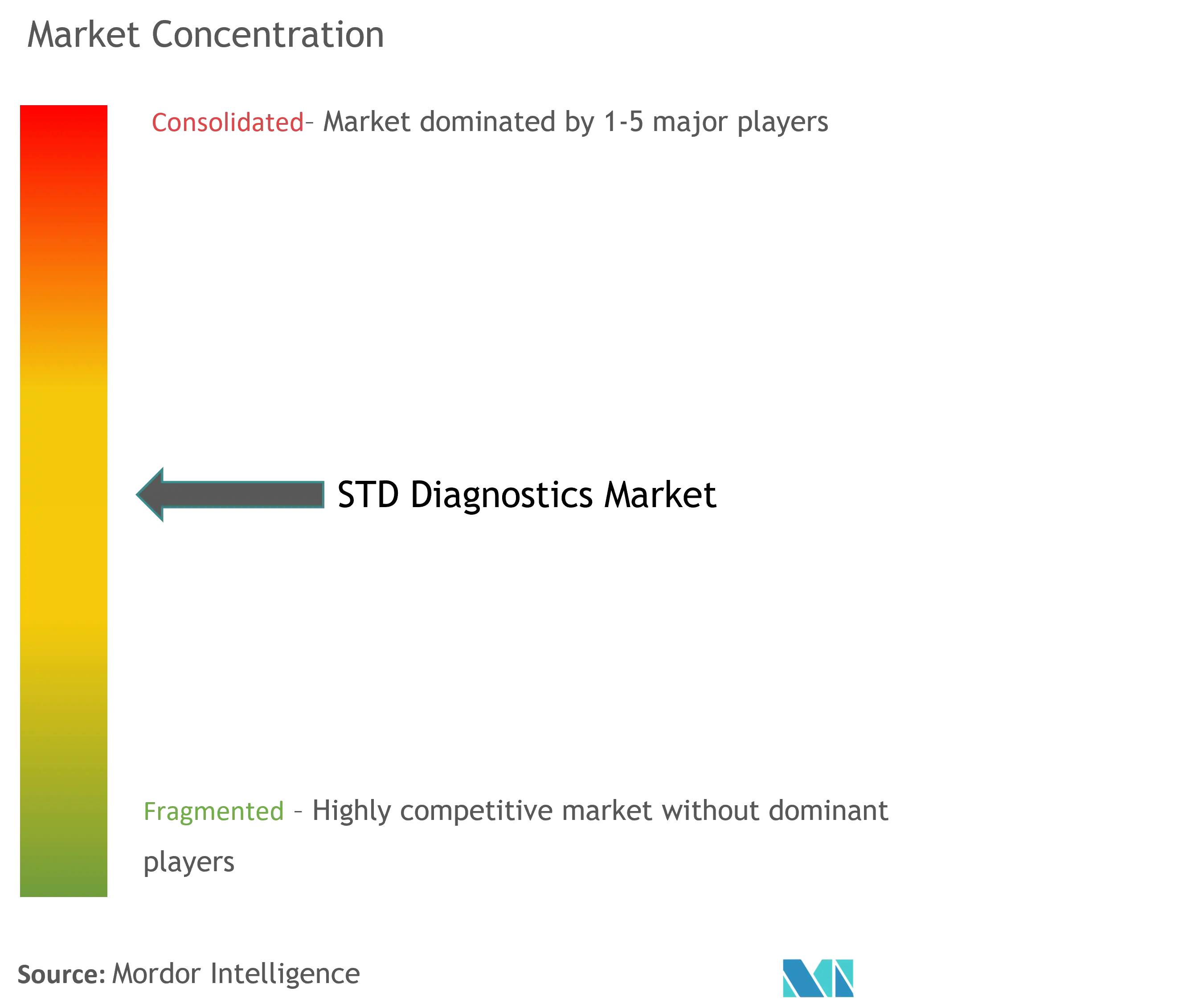

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

STD Diagnostics Market Analysis by Mordor Intelligence

The STD diagnostics market size was valued at USD 18.18 billion in 2025 and estimated to grow from USD 19.42 billion in 2026 to reach USD 27.04 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031). Growth is propelled by an 80% surge in U.S. syphilis cases—exceeding 207,000 confirmed infections in 2022—and the creation of a federal task force to curb the trend. The World Health Organization now tracks 8 million global syphilis cases for 2022, underscoring the gap to its 2030 goal of a 90% reduction in adult infections. Overall STI incidence has climbed 58.38% since 1990, with the sharpest burdens in low socio-demographic regions. Regulatory momentum continues as the FDA reclassified nucleic-acid STI assays to Class II in May 2025, shortening approval cycles for innovative platforms. Insurers updated preventive-service tables in May 2024 to guarantee zero-cost STD screening, expanding routine testing volumes. Yet 68% of individuals still cite shame and 85% fear provider judgment, fueling demand for home-based and digitally connected diagnostics.

Key Report Takeaways

- By technology, molecular diagnostics commanded 50.78% of STD diagnostics market share in 2025, while next-generation sequencing is forecast to post the fastest 9.13% CAGR through 2031.

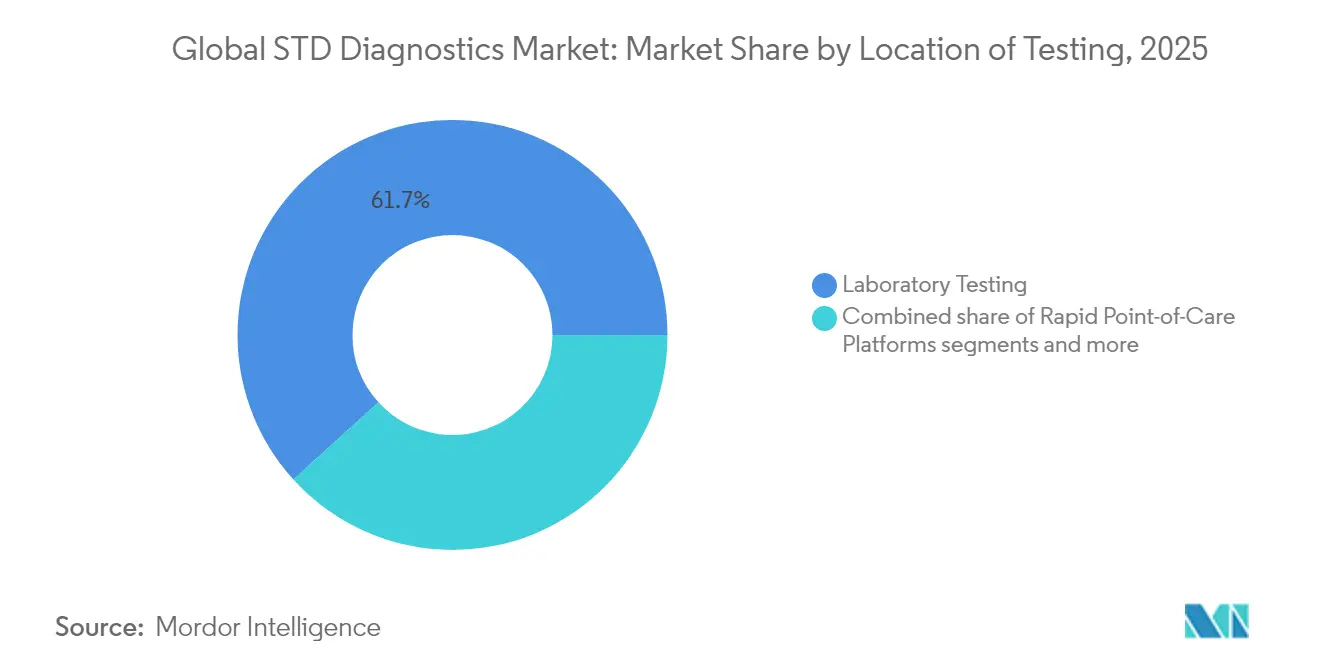

- By location, laboratory testing held 61.74% share of the STD diagnostics market size in 2025, whereas point-of-care platforms are advancing at an 8.39% CAGR to 2031.

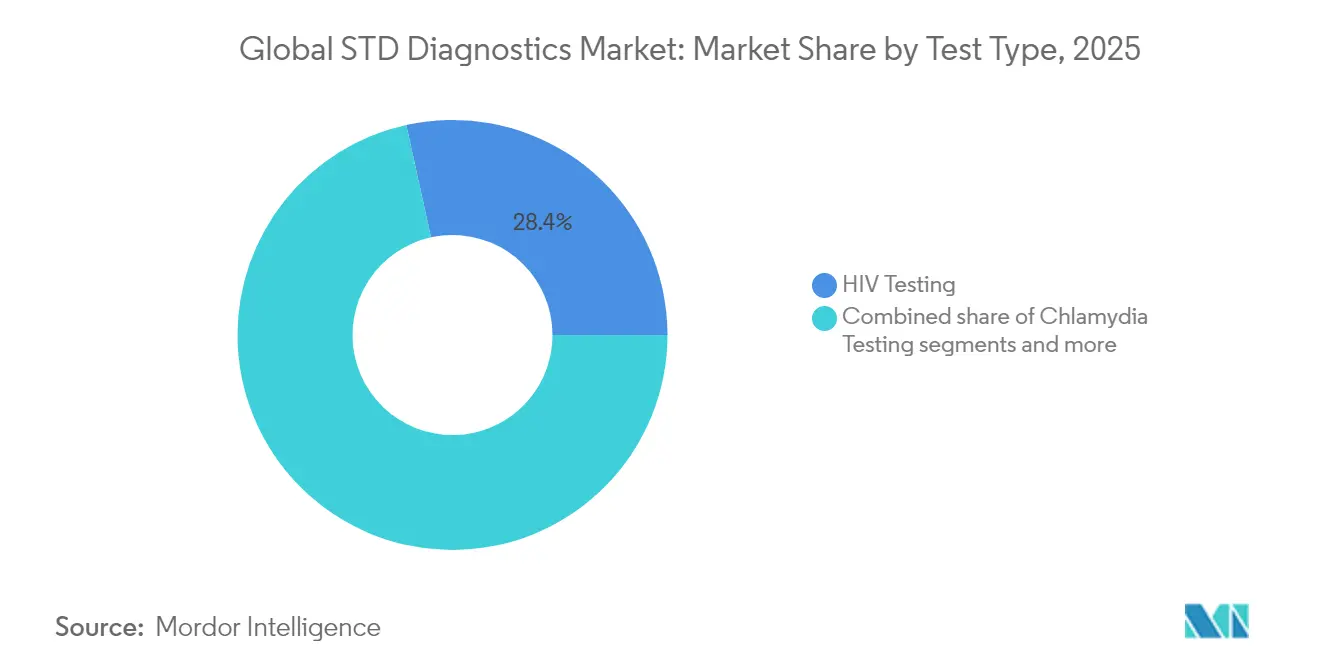

- By test type, HIV assays led with 28.45% revenue share in 2025; Mycoplasma genitalium tests are projected to expand at a 7.77% CAGR over the same horizon.

- By geography, North America dominated at 41.62% share of the STD diagnostics market in 2025, while Asia-Pacific is expected to record a 10.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global STD Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global STD incidence | +1.8% | Global, with acute impact in North America & Asia-Pacific | Long term (≥ 4 years) |

| Government-funded screening programmes | +1.5% | North America, Europe, Australia with expansion to emerging markets | Long term (≥ 4 years) |

| Advances in NAAT & rapid PoC platforms | +1.2% | Global, led by developed markets with technology transfer | Short term (≤ 2 years) |

| Home self-testing & digital connectivity | +0.9% | North America & Europe core, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Multiplex AMR panels for STI pathogens | +0.7% | Global, with priority adoption in North America & Europe | Short term (≤ 2 years) |

| Corporate pre-employment screening in EMs | +0.4% | Emerging markets, particularly Asia-Pacific & Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global STD Incidence

The World Health Organization recorded more than 1 million new sexually transmitted infection cases every day during 2024[1]World Health Organization, “Sexually Transmitted Infections (STIs),” who.int. Asymptomatic presentations account for roughly 70% of chlamydia and gonorrhea infections, so routine testing is vital to interrupt transmission. Gen Z and young millennials aged 15–24 represent nearly half of new cases, prompting health systems to integrate rapid PoC assays that deliver timely results and curb reinfection chains. The discovery of mpox as a sexually transmitted pathogen in 2024 created further diagnostic demand because clinicians need multiplex panels able to distinguish legacy STIs from emerging threats. Simultaneous detection of pathogens and resistance profiles places nucleic-acid platforms at the center of the expanding STD diagnostics market.

Government-Funded Screening Programmes

The U.S. Preventive Services Task Force broadened its screening guidance in 2024 to recommend annual chlamydia and gonorrhea tests for all sexually active individuals younger than 25[2]U.S. Preventive Services Task Force, “Chlamydia and Gonorrhea Screening,” uspreventiveservicestaskforce.org. Similar moves in Canada earmarked CAD 74 million (USD 54.8 million) to extend testing in Indigenous and remote communities. European Union member states synchronized guidelines that favor FDA-cleared or CE-marked molecular assays. These programs provide predictable procurement streams, reinforce quality benchmarks, and enlarge the STD diagnostics market size across primary care, public health, and community settings.

Advances in NAAT & Rapid PoC Platforms

Modern nucleic-acid amplification tests deliver 99.5% sensitivity for chlamydia and gonorrhea while cutting turnaround to less than 90 minutes. Eight PoC molecular platforms gained FDA clearance in 2024, a sharp jump from three clearances the prior year, aided by the agency’s breakthrough device pathway. Multiplex cartridges process urine, vaginal, and rectal samples on the same run, eliminating redundant workflows and trimming technician time. Digital interfaces automatically upload results into electronic health records, enabling faster partner notification and treatment fulfillment. Such efficiencies help shrink the 25% therapy gap observed when positive results arrive after patients have left the clinic.

Home Self-Testing & Digital Connectivity

Four over-the-counter STI kits received FDA authorization in 2024, including the LetsGetChecked Simple 2 kit for chlamydia and gonorrhea. Home sampling paired with telehealth produced 2.3 million completed STI tests in 2024, marking 40% year-on-year growth. Anonymous ordering and mail-back logistics tackle stigma head-on, particularly among digital-native consumers. Europe and Canada are rolling out accommodating regulations, while artificial-intelligence-enhanced result dashboards translate complex molecular outputs into plain-language care advice. Convenience, privacy, and on-demand virtual consults are drawing new users into the STD diagnostics market and widening its addressable population.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social stigma & low awareness | -1.4% | Global, most severe in conservative societies and rural areas | Long term (≥ 4 years) |

| Regulatory & reimbursement hurdles | -0.9% | Emerging markets and countries with complex healthcare systems | Medium term (2-4 years) |

| Skilled-lab-staff shortages in LMICs | -0.7% | Low and middle-income countries, rural areas globally | Long term (≥ 4 years) |

| Cross-reactivity-driven false positives | -0.3% | Global, particularly affecting multiplex testing adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Social Stigma & Low Awareness

Survey data show 43% of adults delay or reject STI screening for fear of judgment or privacy breaches. Cultural taboos in certain regions equate testing with promiscuity, disproportionately limiting women’s access to reproductive care. Public-health campaigns launched in 2024 re-frame screening as a routine wellness metric, yet uptake remains uneven. Anonymous home kits and app-scheduled clinic slots alleviate stigma for some users, but legal restrictions on telemedicine in several jurisdictions slow wider adoption. Ongoing school-based sex-education pilots have lifted testing rates by 25% where implemented, suggesting long-run gains once curricula scale nationally.

Regulatory & Reimbursement Hurdles

Clinical-validation studies for novel PoC devices can cost USD 2–5 million per pathogen, stretching timelines for startups. Coding discrepancies mean payers in multiple markets still reimburse only symptomatic testing, discouraging routine screens. Though the Centers for Medicare & Medicaid Services revised molecular STI codes in 2024, coverage gaps persist for multi-analyte panels, muting demand elasticity. Outside the United States, fragmented quality standards force device makers to navigate country-by-country registrations, often adding 12–18 months to launch schedules. These barriers tilt the STD diagnostics industry toward well-capitalized incumbents while delaying game-changing innovations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: HIV Testing Dominates Despite Emerging Pathogen Growth

The HIV segment collected 28.45% of 2025 revenue, underscoring entrenched policies that require routine screening in blood services, prenatal care, and high-risk populations. Syphilis anchors the number-two position thanks to prenatal mandates that aim to curb congenital infections. Chlamydia and gonorrhea testing together generated roughly one-third of total revenue, supported by annual testing advice for sexually active youth.

Mycoplasma genitalium reported the quickest 7.77% CAGR outlook through 2031, propelled by growing recognition of its role in persistent urethritis. HPV and HSV segments post steady gains as multiplex NAAT assays streamline differential diagnosis. Trichomonas benefits from same-visit PoC platforms that catch treatable infections before patients leave the clinic. Chancroid remains niche but experiences improved molecular detection accuracy, reducing historical under-diagnosis.

By Technology: Molecular Diagnostics Lead NGS Innovation

Molecular platforms retained 50.78% share in 2025, delivering rapid, highly sensitive results that support guideline-driven care. Immunoassays remain vital in lower-resource settings, yet accuracy gaps limit additional share gains.

Next-generation sequencing is set for a 9.13% CAGR thanks to simultaneous pathogen and resistance profiling, capabilities prized by surveillance bodies such as the CDC, which purchased fleet NGS systems for USD 45 million in 2024. Biosensor and microfluidic devices integrate sample prep and amplification on a chip, drawing venture funding into portable alternatives that require minimal technician skill. Cost curves remain on a downward slope, opening mid-tier labs to NGS adoption and redefining the competitive stakes within the STD diagnostics market.

By Location of Testing: Point-of-Care Disrupts Laboratory Dominance

Laboratories still processed 61.74% of specimens in 2025, but growth momentum is shifting toward decentralized formats. Point-of-care systems, advancing at an 8.39% CAGR, align with provider goals for immediate treatment initiation and with patient desire for discreet same-visit results. FDA-cleared CLIA-waived devices like cobas liat demonstrate that complex molecular workflows can fit onto countertop instruments. Telemedicine channels further expand reach by linking remote testing stations to virtual consults, lowering the need for bricks-and-mortar facilities.

Home testing remains a nascent yet explosive niche. The market witnessed its first FDA-authorized at-home multiplex panel in 2025, moving self-collection from mail-in models to real-time molecular detection. This evolution dovetails with rising e-pharmacy networks that dispense antibiotics based on verified home results, accelerating care pathways. While central labs preserve a competitive edge for culture-based susceptibility testing, the broader trend favors distributed models that minimize friction and democratize access

By End User: Home Care Segment Challenges Hospital Dominance

Hospitals and clinics captured 43.15% of the STD disgnostics market size in 2025, driven by bundled services that integrate counseling and immediate therapy. Yet the home-care channel is expanding at a 9.92% CAGR, catalyzed by legislative support for over-the-counter availability and interoperable digital platforms. Diagnostic laboratories remain indispensable for high-complexity workflows, but many are pivoting to white-label home-test fulfillment to offset volume erosion. Telehealth providers are forging direct partnerships with kit manufacturers, creating vertically integrated ecosystems that bypass traditional referral pipelines.

Corporate wellness programs in emerging markets are adding pre-employment STD panels to routine screening, further diversifying the end-user mix. Universities and community clinics are also trialing vending-machine distribution models that dispense anonymized test kits on demand. Together these trends underscore rising consumer agency, prompting incumbents to rethink value propositions beyond pure analytical accuracy toward holistic user experience.

Geography Analysis

North America commanded 41.62% of global revenue in 2025, sustained by insurance mandates that make preventive STD services cost-free and by robust federal coordination to counter the syphilis surge. High discretionary healthcare spending and rapid regulatory approvals keep the region at the innovation vanguard. Nevertheless, intra-regional gaps prevail; Southern states report above-average infection rates, signaling under-served pockets even within a mature market.

Europe follows with a stable base built on universal health coverage and pan-regional regulatory harmonization, yet faces budgetary pressure that favors cost-effective point-of-care models. Asia-Pacific is the fastest-growing territory at a forecast 10.76% CAGR, driven by urbanization, public-health investments, and an 11.6% STI prevalence among reproductive-age women in Southeast Asia. China’s anti-corruption clampdown in healthcare briefly slowed foreign diagnostic imports in 2024, but infrastructure spending across ASEAN and India is widening test access. Latin America and the Middle East & Africa together form an emerging corridor where rising awareness and mobile-health penetration offset infrastructure deficits. WHO-backed funding for integrated diagnostics and low-cost multiplex panels is steering donor capital into these regions. South Africa records the world’s highest age-standardized STI rates, making it a focal point for donor-supported pilot projects that could shape future expansion models. Overall, geographic diversification strategies will define revenue resilience for vendors competing in the global STD Diagnostics market.

Regulatory Landscape

In the United States, STD diagnostics are shaped by FDA device classification and evolving oversight of laboratory-developed tests (LDTs). In May 2025, FDA began implementation of the first stage of the LDT final rule phaseout policy, which increases compliance expectations for clinical laboratories that historically relied on LDT pathways for niche STI assays. FDA also established 21 CFR 866.3393, defining classification requirements and special controls for nucleic acid detection devices for non-viral STIs, reinforcing the shift of NAAT-based STI assays into clearer Class II-style control frameworks.

In Europe, Regulation (EU) 2017/746 (IVDR) continues to tighten evidence and post-market requirements for IVDs, with companion diagnostic processes specifically influenced by EMA guidance updates. In December 2024, EMA issued Revision 1 guidance on procedural aspects of notified body consultation for companion diagnostics, which affects test developers whose STI testing intersects with therapy selection workflows. Globally, standard-setting and clinical practice updates also steer adoption: CDC updated laboratory testing recommendations for syphilis in February 2024, while WHO released a consolidated operational handbook on STIs in February 2026 that integrates diagnostic procedures and service delivery guidance used by national programs and procurement agencies.

Value Chain Analysis

The STD diagnostics value chain covers assay design and reagent supply (primers/probes, antibodies, enzymes, controls), instrument manufacturing (bench-top molecular analyzers and rapid POC systems), regulatory and clinical validation, and commercialization through laboratory networks, public health programs, and direct-to-consumer channels. Large IVD OEMs (e.g., Roche, Abbott, BD, Hologic, DiaSorin, Danaher subsidiaries) anchor platform ecosystems, while specialized developers and partners supply assays, sample-collection devices, and connectivity layers that support home collection, telehealth ordering, and results integration.

Downstream, distribution and access increasingly depend on partnerships that connect test developers with high-reach healthcare delivery and lab fulfillment. NOWDiagnostics working with Labcorp (October 2024) to expand access to the First To Know Syphilis Test across professional and hospital settings is one example. Tia Health partnering with Molecular Testing Labs (September 2025) to launch an FDA-cleared home-collection 4-plex STI test is another, linking consumer-facing care navigation to lab-based molecular workflows. In Europe, IVDR-driven menu upgrades and local collaborations are influencing supply strategies, such as BD partnering with Certest Biotec (December 2025) to add IVDR-certified VIASURE assays for BD MAX across respiratory and STI diagnostics, and Seegene and Werfen finalizing a Spain-based NewCo framework (October 2024) to co-develop infectious disease diagnostics, supporting regionalized development and manufacturing capabilities.

Competitive Landscape

The market is moderately fragmented, with scale advantages accruing to firms that offer multipathogen portfolios and digital connectivity. Roche leverages its cobas liat platform to capture high-margin point-of-care demand, while continuous firmware updates extend usable life cycles. Thermo Fisher and Danaher subsidiaries such as Cepheid compete on assay menu breadth and cartridge throughput, fueling a technology arms race.

Strategic acquisitions are reshaping boundaries. OraSure agreed in December 2024 to acquire Sherlock Biosciences, aiming to commercialize a molecular CT/NG self-test under FDA review. Visby Medical secured landmark FDA home-testing clearance in March 2025 and filed a men’s panel two months later, underscoring its intent to build gender-specific franchises. Laboratories including Labcorp and Quest Diagnostics are evolving into omni-channel service hubs, layering logistics, data analytics, and remote sampling to protect volumes amid decentralization.

Platform differentiation now revolves around user interface, result integration, and antimicrobial resistance analytics rather than hardware alone. AI-driven triage algorithms, such as those under development for risk-based screening, promise further separation between innovators and fast followers. Suppliers that combine rapid diagnostics with seamless e-prescription workflows are well-positioned to command premium pricing and to deepen customer lock-in over the next five years

STD Diagnostics Industry Leaders

Diasorin S.p.A

Hologic, Inc

Danaher Corporation(Cephied)

Siemens Healthineers AG

Abbott

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Decentralized molecular testing is expanding beyond single-pathogen workflows into broader, faster menus that fit urgent care, community clinics, and near-patient settings. A concrete signal is the May 2026 FDA 510(k) clearance for Roche Molecular Systems cobas liat CT/NG/MG, which extends an established point-of-care molecular platform into a three-target STI NAAT and supports same-visit decision-making where loss to follow-up is common. Programs and local procurement are also pulling POC into routine service lines, including county-level initiatives purchasing rapid STI analyzers to restart or expand free testing and treatment pathways.

At-home access is widening through two complementary models: OTC testing and at-home self-collection that feeds centralized molecular labs. In June 2026, OraSure Technologies received FDA 510(k) clearance for a urine sample collection kit intended for at-home self-collection, with subsequent lab-based molecular testing using Roche systems. This tightens the linkage between consumer convenience and high-throughput lab quality. Evidence from public programs also supports whitespace for scaled implementation, including the Texas Department of State Health Services at-home testing pilot (reported in 2024), which documented that self-collection models can achieve specimen return and case identification performance comparable to clinic pathways. In parallel, health systems extending STD testing into urgent care clinics without appointments aim to reduce access friction.

Recent Industry Developments

- July 2026: Cepheid (Danaher) highlighted real-world clinical study findings for the Xpert Xpress MVP test showing higher rates of appropriate treatment within 24 hours versus standard diagnostic approaches for women with vaginal symptoms. The publication strengthens the evidence base for near-patient molecular workflows that compress the test-to-treat window and supports broader uptake of multiplex, rapid syndromic testing models in clinics.

- June 2026: Roche Molecular Systems received FDA 510(k) clearance for the cobas liat CT/NG/MG nucleic acid test, expanding the cobas liat menu into a three-target STI NAAT that includes Mycoplasma genitalium. The clearance advances same-visit molecular testing capability for high-volume STI screening and supports more standardized deployment across decentralized care sites that use CLIA-aligned POC systems.

- October 2024: NOWDiagnostics and Labcorp announced a collaboration to expand access to the First To Know Syphilis Test across professional and hospital settings in the United States. The partnership links an OTC-authorized syphilis test franchise with a major laboratory network, supporting broader distribution channels and reinforcing the role of scaled fulfillment and clinical integration in expanding screening reach.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from diagnostic tests and related consumables used to detect sexually transmitted infections, across laboratory and point-of-care settings, and reported in USD at the global level.

Scope exclusions: Treatment drugs, vaccines, and broader sexual health products that do not perform infection detection are excluded.

Segmentation Overview

- By Test Type

- Syphilis Testing

- HPV Testing

- HSV Testing

- HIV Testing

- Trichomonas Testing

- Mycoplasma Genitalium Testing

- Chancroid Testing

- Chlamydia Testing

- Gonorrhea Testing

- By Technology

- Immunoassay‐based Methods

- Molecular Diagnostics

- Next-Generation Sequencing

- Biosensor / Microfluidics & Other Emerging Platforms

- By Location of Testing

- Central & Hospital Laboratories

- Rapid Point-of-Care Platforms

- Over-the-Counter / Home Self-Testing

- By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Home Care / OTC

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For the base structure of the market, we started with public health and screening indicators and then linked them to test demand and lab capacity signals. Sources used include, for example, the US CDC STI surveillance tables, WHO and UNAIDS epidemiology updates, and national public health agency dashboards that publish testing guidance and detection trends. We also reviewed peer-reviewed journals for shifts in test accuracy, preferred sample types, and updated clinical pathways that can change test mix.

To ground the commercial side, company annual reports, investor decks, product inserts, and regulatory databases such as the US FDA device listings and clearances were referenced to understand which test formats are actively sold and where adoption is rising. In addition, we used paid subscriptions focused on company financials and intelligence, plus patent databases, to support product mapping and pricing logic where public detail was thin. These desk sources are illustrative only, and other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were captured through expert interviews and structured surveys with diagnostic labs, hospitals and clinics, public health programs, and channel-side stakeholders who see ordering patterns. We used these discussions to confirm realistic testing volumes, price ranges by platform (molecular, immunoassay, rapid), and the pace of adoption for point-of-care and home-testing pathways across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 17% | APAC: 46% |

| Mid tier: 40% | Functional/Unit leaders: 28% | EMEA: 31% |

| Smaller Players: 21% | Managers: 55% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where STI testing demand pools were reconstructed by combining surveillance and screening guidance with the practical conversion into tests performed across care settings. Once the demand pool was formed, it was translated into value using a blended price logic that reflects platform mix and the share of confirmatory testing.

Key inputs used in the model include reported STI incidence and screening recommendations, testing rates in priority cohorts, laboratory throughput and turnaround needs, technology mix shifts toward NAAT and rapid formats, and typical per-test pricing ranges by setting. Where a public series was missing for a country, we filled the gap using proxy indicators such as population by age cohort, reported positivity trends, and nearby-market testing intensity, and then rechecked the output with interview feedback. We also used selective bottom-up checks, such as sampled ASP times estimated test volumes by setting, along with channel checks on reagent and kit movement.

Forecasting relied mainly on scenario analysis, because policy-driven screening, reimbursement changes, and self-test adoption can move faster than a straight-line trend. Assumptions for incidence trend, screening intensity, and price progression were aligned to what practitioners consider feasible over the forecast window.

Data Validation & Update Cycle

Outputs were validated through multi-step checks that compare results against independent signals like disease surveillance direction, testing policy expansion, and visible platform adoption in regulated markets. Any outliers at country or regional level were reworked, and the main drivers were reviewed again so the final totals stay consistent with the underlying testing logic.

Before sign-off, a separate analyst review is completed to confirm arithmetic integrity, assumption consistency, and year-on-year reasonableness. Reports are refreshed annually, and interim updates are triggered when there are material events such as major guideline changes, new regulatory approvals, or notable shifts in screening funding. Right before delivery, we run a fresh scan so the client receives the latest updated view.

Mordor Intelligence's Sexually Transmitted Diseases Std Diagnostics Market Size Compared With Other Published Estimates

Published market values for STD diagnostics do not always match because each publisher draws the market line in a slightly different way, and then applies different testing volume and pricing assumptions. Differences also show up when one estimate is anchored to surveillance-style demand pools, while another leans more on revenue reporting or a narrower set of regions.

Diagnostic services revenue often gets included in some publications, but it sits outside Mordor Intelligence's scope, which is why our 2026 number can look higher or lower depending on how service-heavy the other estimate is. The spread also comes from how home testing is treated, whether confirmatory lab tests are double-counted, and whether pricing is converted using a single annual FX rate or a period average.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.42 B (2026) | |

| Industry Publisher A | USD 11.39 B (2025) | Includes diagnostic services and often blends testing services with product revenues, which can reduce comparability when the product-only scope is used. The base year is earlier, and the platform mix and confirmatory-testing uplift may be treated more conservatively. |

| Industry Publisher B | USD 12.26 B (2026) | Uses a broader testing definition that can mix screening program activity and home testing differently by region, and the value build can depend heavily on assumed price points rather than setting-specific price bands. Forecast starting points and FX timing can also shift the USD total. |

Overall, the table shows that most of the gap is explained by what gets counted as market revenue and how testing intensity is converted into value. By keeping the model tied to clear demand indicators and practical price logic by setting, the final figure stays traceable to repeatable steps and can be rechecked as new surveillance and guideline updates come in.

Key Questions Answered in the Report

How large will the STD diagnostics market be by 2031?

Forecasts point to USD 27.04 billion by 2031, translating to a 6.84% CAGR from 2026.

Which pathogen test currently generates the most revenue?

HIV tests led 2025 revenue, capturing 28.45% of spending.

What technology is growing the fastest?

Next-generation sequencing is projected to expand at a 9.13% CAGR through 2031.

Which region offers the highest growth potential?

Asia-Pacific is expected to record a 10.76% CAGR as infrastructure and awareness improve.

How fast is the home-testing channel expanding?

Home-care and over-the-counter kits are slated for a 9.92% CAGR, the fastest among end users.

What drives adoption of point-of-care platforms?

FDA fast-track clearances, 30-minute turnaround times, and integration with electronic health records are accelerating PoC uptake.

Page last updated on: