Semiconductor Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 86.55 Billion |

| Market Size (2031) | USD 133.87 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Semiconductor Logistics Market Analysis by Mordor Intelligence

The Semiconductor Logistics Market size was valued at USD 79.32 billion in 2025 and estimated to grow from USD 86.55 billion in 2026 to reach USD 133.87 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031).

The growth outlook reflects historic fab construction activity, government incentive programs, and intensifying demand for artificial-intelligence hardware that requires rapid, contamination-free material flows. Transportation services remain the backbone of the semiconductor logistics market, yet value-added services such as specialist packaging, export-control documentation, and compliance auditing are expanding fastest as manufacturers seek integrated supply-chain partners. Capacity investments in Class A clean-room vehicles, cold-chain networks for extreme-ultraviolet (EUV) chemicals, and AI-enabled routing platforms are reshaping competitive dynamics. At the same time, trusted-partner supply-chain policies in the United States, Europe, and Japan are redrawing traditional Asia-centric trade lanes, compelling logistics providers to establish regional hubs near new fab clusters while maintaining high service standards that align with national-security requirements.

Key Report Takeaways

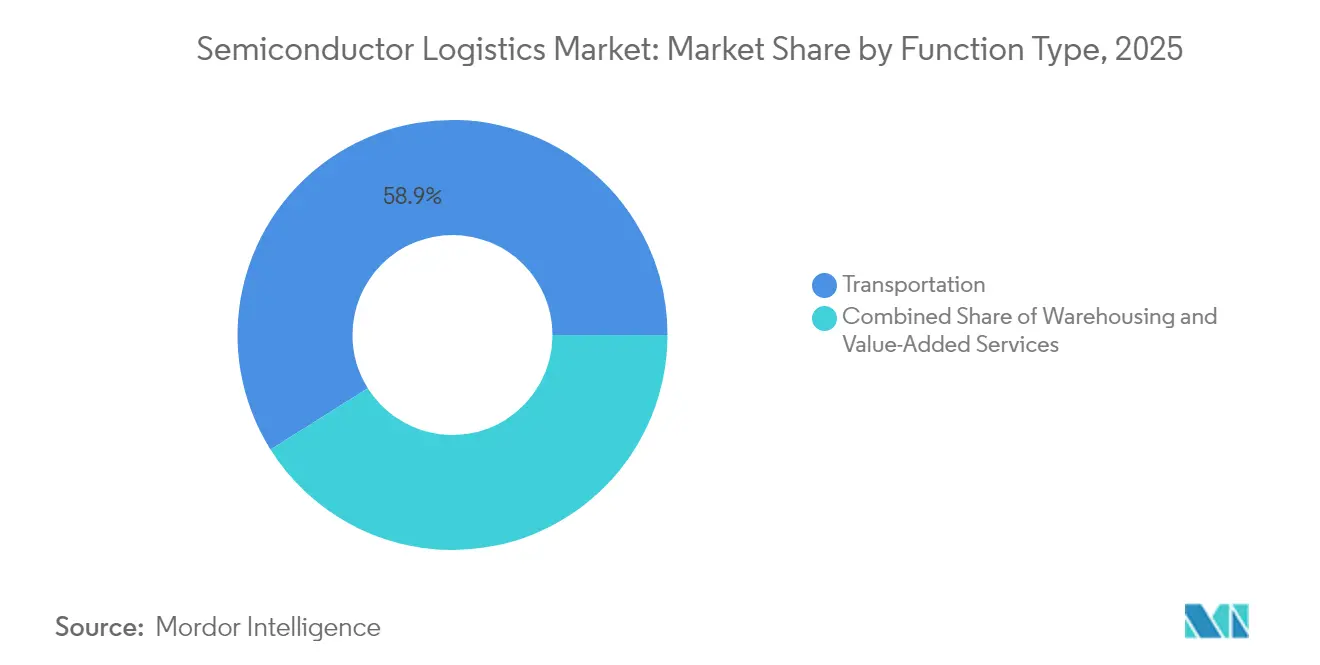

- By function, transportation controlled 58.93% of the semiconductor logistics market share in 2025. By function, value-added services are forecast to expand at a 4.08% CAGR through 2031.

- By mode of operation, non-cold-chain services commanded 76.70% of the semiconductor logistics market size in 2025. By mode of operation, cold-chain logistics is projected to advance at a 4.78% CAGR between 2026 and 2031.

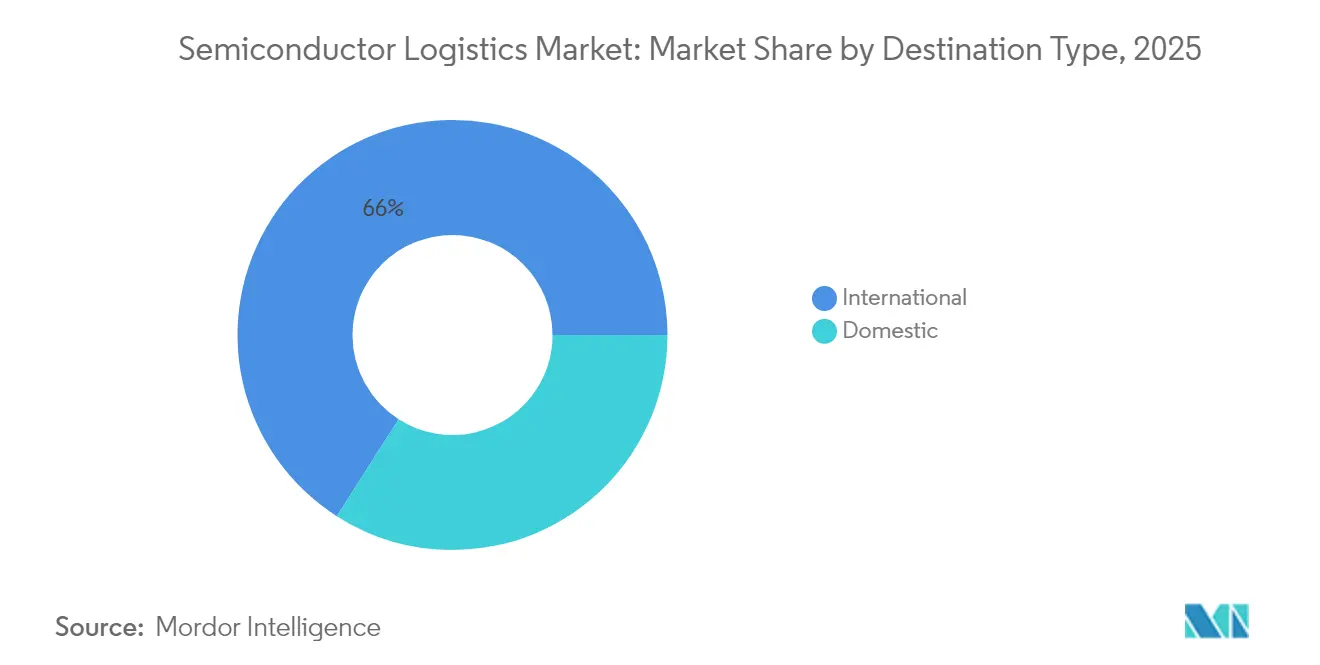

- By destination, international shipments held 65.95% of the semiconductor logistics market size in 2025, while domestic flows are growing at a 3.95% CAGR.

- By product type, finished semiconductor products accounted for 40.92% revenue in 2025; raw materials and chemicals are forecast to grow at 4.55% CAGR through 2031.

- Asia-Pacific captured 43.10% of the semiconductor logistics market share in 2025 and is set to record the highest regional CAGR of 4.85% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Semiconductor Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated fab expansion in the United States and Europe | +2.1% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Surging wafer-level packaging outsourcing in Southeast Asia | +1.8% | APAC core, secondary impact in Americas | Short term (≤ 2 years) |

| Shift toward near-foundry "milk-run" logistics models | +1.3% | Global, concentrated near major fab clusters | Medium term (2-4 years) |

| Cold-chain compliance for EUV photolithography chemicals | +1.1% | Global, emphasis on advanced node regions | Long term (≥ 4 years) |

| Government subsidies for trusted-partner supply chains | +1.7% | Americas, EU, Japan, select APAC markets | Medium term (2-4 years) |

| AI-enabled dynamic routing & ETA visibility platforms | +1.2% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Fab Expansion in the United States and Europe

Eighteen new fabs slated for 2025-2026 in the Americas, Japan, and Europe are reshaping global logistics corridors. Projects such as TSMC's Arizona campus and Intel's multi-state capacity expansions require contamination-free trucking networks to deliver ultra-high-purity gases, photoresists, and wafer pods on strict just-in-time schedules. Traditional long-haul routes are being supplemented by regional “milk-run” circuits that loop among fabs, supplier distribution centers, and specialized trans-load facilities. Logistics providers are investing in ISO Class 5-compatible trailers and on-board particulate sensing to meet these service levels. Real-estate developers are co-locating semiconductor-grade warehouses near Phoenix, Columbus, and Dresden, creating new nodes that shorten lead times and reduce air-freight reliance. The resulting demand surge for Class A trucks and certified drivers underpins a measurable uplift in the semiconductor logistics market[1]"Eighteen New Semiconductor Fabs to Start Construction in 2025, SEMI Reports." SEMI, semi.org..

Surging Wafer-Level Packaging Outsourcing in Southeast Asia

Rapid outsourcing of advanced packaging drives point-to-point lanes across Malaysia, Vietnam, and the Philippines. ASE Technology’s Penang expansion to 3.4 million ft² and 6,000 staff has tripled outbound shipments of temperature-sensitive substrates. Amkor’s USD 1.6 billion Bac Ninh facility adds 200,000 m² of clean-room space dedicated to system-in-package modules, amplifying inbound flows of lead frames, laminate, and under-fill chemicals. These projects demand bonded consolidation warehouses, ISO 14001-compliant road fleets, and 24/7 customs-broker desks to manage zone returns and partial shipments. Southeast Asian governments are streamlining free-trade-zone rules and investing in dual-view X-ray scanners at airports to accelerate clearance of semiconductor cargo, further stimulating the semiconductor logistics market[2]"CHIPS for America Awards." National Institute of Standards and Technology, nist.gov.

AI-Enabled Dynamic Routing and ETA Visibility Platforms

Logistics orchestration is shifting from manual load planning to self-learning algorithms that simulate millions of routing permutations. DHL Supply Chain has rolled out generative-AI tools that cleanse shipment data and recommend network designs within minutes, cutting average planning cycles by 80%. Multi-agent large-language models analyze historical delay patterns, real-time weather, and fab production schedules to forecast arrival times within ±5 minutes. Shippers gain full-trip temperature, humidity, and shock metrics via IoT dataloggers, mitigating excursion risk for EUV photoresists and micro-lenses. These capabilities are becoming table stakes for winning long-term contracts, prompting mid-tier forwarders to license white-label AI suites or form technology alliances. As adoption rises, AI platforms underpin efficiency gains that expand available capacity without proportional fleet growth, strengthening the semiconductor logistics market[3]"CHIPS for America: Intel Community Impact Report." National Institute of Standards and Technology, nist.gov..

Government Subsidies for Trusted-Partner Supply Chains

The CHIPS Act has disbursed USD 29.5 billion in direct project funding that ties award eligibility to resilient, domestic, or allied supply-chain participation. Texas Instruments received USD 1.61 billion to construct three fabs, triggering supplier co-location of gas farms, chemical blending stations, and spare-parts depots in Texas. European programs mirror the approach: Tax credits in Germany's Silicon Saxony and France's nano-electronics clusters require ISO 9001-certified logistics providers and end-to-end shipment traceability, accelerating awards to compliant vendors and expanding demand for semiconductor-grade logistics.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight capacity for Class A clean-room trucks and containers | -1.4% | Global, acute in advanced node regions | Short term (≤ 2 years) |

| Volatile jet-fuel surcharges on chartered freighters | -0.8% | Global, emphasis on trans-Pacific routes | Short term (≤ 2 years) |

| Persistent shortage of certified DG/ESD-trained manpower | -1.2% | Global, severe in emerging markets | Medium term (2-4 years) |

| Export-control licensing delays for China-bound tools | -0.9% | China-focused trade lanes, secondary global impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Capacity for Class A Clean-Room Trucks & Containers

Back-to-back fab announcements have outpaced specialty-fleet growth. Clean-room-equipped trailer builders report order backlogs exceeding 18 months, while operators face double-digit price inflation for ISO Class 5 liners. Some shippers charter mobile soft-wall clean rooms inside standard trailers as stop-gap measures, yet these solutions add loading complexity and reduce cube utilization. With every new advanced node requiring tighter particle thresholds, the supply-demand imbalance for specialty vehicles continues to constrain the semiconductor logistics market.

Persistent Shortage of Certified DG/ESD-Trained Manpower

The global pool of dangerous-goods and electrostatic-discharge certified personnel has failed to keep pace with fab and packaging expansion. Industry groups project a 146,000-worker gap by 2029. Certification programs through SEMI University and private academies cannot scale fast enough, leaving logistics providers to rotate limited experts across multiple regions, stretching compliance oversight. Wage escalation and poaching intensify cost pressure, reducing margin headroom despite rising shipment volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Transportation Leadership with Rapid Value-Added Uptick

Transportation services held 58.93% of the semiconductor logistics market in 2025 as fabs, OSATs, and OEMs depend on time-definite, contamination-free movement of high-value cargo. Road fleets dominate intra-regional lanes where just-in-time plant replenishment requires sub-hour transit precision, while dedicated freighters and charter flights secure global capacity for masks, EUV machines, and critical spares. Korean Air alone operates 23 wide-body freighters dedicated to semiconductors, equal to a 6% share of global capacity for this vertical. The segment’s scale gives carriers bargaining power with airports and ground handlers for priority slots and secure-tarmac clearance, reinforcing its primacy within the semiconductor logistics market size.

Value-added services posted the fastest segmental CAGR of 4.08% through 2031 as supply-chain complexity raises demand for customs brokerage, bonded warehousing, and export-control consulting. Providers that offer packaging kitting, ESD audit services, and sub-fab MRO replenishment win long-term contracts from foundries keen to minimize vendor count. As fabs outsource more non-core activities, logistics firms embed technicians on-site to manage tool-move coordination, enabling higher-margin revenue streams and diversifying away from low-yield pure transportation.

By Mode of Operation: Non-Cold-Chain Dominance, Cold-Chain Momentum

Non-cold-chain services accounted for 76.70% of the semiconductor logistics market size in 2025, covering finished chips, tooling, and mainstream materials that tolerate ambient conditions. Multi-modal hubs integrate bonded warehouses with ESD-safe staging areas to aggregate loads bound for diverse geographies, optimizing line-haul economics. Yet demand for cold-chain lanes is rising swiftly at a 4.78% CAGR as EUV photoresists, specialty gases, and advanced polymers impose tight thermal envelopes. DHL’s EUR 2 billion (USD 2.20 billion) investment in GDP-compliant hubs positions the firm to capture this specialized growth, easing a key capacity bottleneck that threatened to slow the semiconductor logistics market.

By Destination: International Complexity vs. Domestic Reshoring

International flows maintained a commanding 65.95% revenue contribution in 2025 because design, fabrication, and assembly still span several continents. Trans-Pacific lanes link Taiwan’s leading-edge fabs with U.S. design houses and Southeast-Asian OSATs, demanding rigorous export-control compliance and multi-country customs clearance mastery. Rising domestic incentives, most notably the USD 52.7 billion CHIPS Act, are reshaping part of this pattern. Domestic shipments in the United States, Europe, and Japan are growing at 3.95% CAGR as new fabs pull more inbound chemicals, spares, and finished wafers via internal corridors. Enhanced near-shoring moderates exposure to ocean-freight disruption yet places new pressure on road and rail networks to meet semiconductor-grade cleanliness and security standards.

By Product Type: Finished Goods Dominant, Raw Materials & Chemicals Surging

Finished semiconductor products represented 40.92% of 2025 revenue because high-unit-value chips travel under premium-rate regimes that guarantee speed and integrity. Handheld-device processors can exceed USD 10,000 per wafer, compelling shippers to book first-flight availability and GPS-sealed container protocols. Raw materials & chemicals, however, are expanding fastest at 4.55% CAGR through 2031 as advanced nodes multiply demand for UHP acids, slurries, and photo-initiators. Dedicated chemical logistics corridors now deploy double-lined tankers with vapor recovery and real-time pH monitoring, highlighting growing specialization inside the semiconductor logistics market.

Geography Analysis

Asia-Pacific maintains its dominant position with 43.10% market share in 2025 and leads regional growth at 4.85% CAGR through 2031, driven by its integrated semiconductor ecosystem and strategic supply chain diversification initiatives. Taiwan's foundry leadership, anchored by TSMC's 54% global market share and nearly 90% of advanced chip production, drives significant logistics flows that require specialized clean-room transportation and temperature-controlled handling for EUV chemicals. South Korea's memory dominance, led by Samsung and SK Hynix, is generating substantial logistics volumes as both expand HBM production, with Samsung increasing output 2.5 times in 2024 and SK Hynix investing KRW 10 trillion in high-end storage products. Southeast Asian markets are experiencing accelerated growth as semiconductor companies diversify operations, with Malaysia generating approximately USD 130 billion annually from semiconductor exports while Vietnam attracts major packaging investments like Amkor's USD 1.6 billion facility in Bac Ninh. The region's logistics infrastructure faces a projected USD 60 billion investment gap to meet future trade demands, with countries enhancing transport infrastructure and establishing specialized semiconductor logistics hubs to maintain competitive advantages.

North America demonstrates robust growth momentum driven by unprecedented government investment and strategic reshoring initiatives under the CHIPS Act's USD 52.7 billion allocation. TSMC's USD 65 billion Arizona investment represents the largest foreign manufacturing project in U.S. history, with three fabs creating approximately 6,000 high-tech jobs and establishing new domestic logistics corridors for advanced semiconductor production. Intel's nearly USD 90 billion domestic investment spans multiple states, supported by USD 8.5 billion in CHIPS funding, and is creating integrated logistics networks that serve automotive, defense, and AI markets. The region benefits from established logistics infrastructure and regulatory frameworks, though faces higher operational costs with U.S. facilities costing approximately 10% more to build and up to 35% higher operating costs compared to Asian counterparts. Workforce development initiatives, including Intel's USD 65 million CHIPS funding for training programs, address critical skills shortages while establishing sustainable talent pipelines for semiconductor logistics operations.

Europe emerges as a strategic growth market through coordinated industrial policy and substantial public investment in semiconductor manufacturing capabilities. Germany's Silicon Saxony region serves as a model integrated ecosystem, while the European Chips Act targets increasing regional production from sub-10% to 20% by 2030 through strategic investments in domestic manufacturing Deloitte US. Major investments include onsemi's USD 2 billion silicon carbide facility in the Czech Republic, targeting energy-efficient semiconductors for electric vehicles and renewable energy applications, with potential to generate over USD 270 million annually for Czech GDP onsemi. The region's logistics infrastructure benefits from established automotive supply chains and regulatory frameworks including GDPR and environmental certifications, while DHL's EUR 2 billion (USD 2.20 billion) health logistics investment enhances specialized transportation capabilities for semiconductor chemicals and materials. European semiconductor logistics growth aligns with sustainability mandates and circular economy principles, creating opportunities for green logistics solutions and carbon-neutral transportation networks.

Competitive Landscape

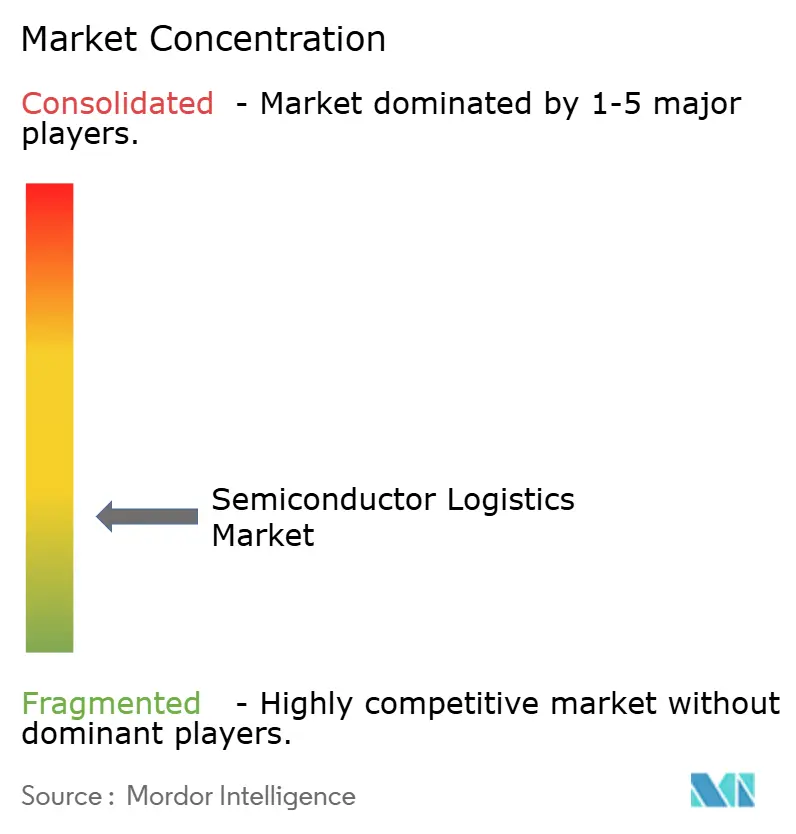

The semiconductor logistics market exhibits moderate fragmentation with increasing consolidation around specialized service providers capable of meeting stringent clean-room, temperature-control, and security requirements. Market concentration is evolving as traditional freight forwarders pivot toward semiconductor-specific solutions, while pure-play logistics companies like DHL Supply Chain and Kuehne+Nagel establish dominant positions through targeted investments in specialized infrastructure and technology platforms. DHL's EUR 2 billion (USD 2.20 billion) health logistics investment and Strategy 2030 focus on semiconductor logistics demonstrate the strategic importance of this sector, while Kuehne+Nagel's specialized sub-fab logistics services for ultra-high purity gases and chemicals position it as a critical enabler of advanced manufacturing processes. Competition intensity has heightened as logistics providers develop comprehensive semiconductor ecosystems spanning construction logistics, fab operations support, and aftermarket services, with differentiation increasingly based on technological capabilities rather than traditional cost metrics.

Strategic patterns emphasize vertical integration and technology adoption, with leading providers implementing AI-enabled dynamic routing, IoT-based cargo monitoring, and predictive analytics for supply chain optimization. Nippon Express's strategic partnership with Tive enables real-time monitoring of temperature, humidity, and shock-sensitive semiconductor cargo, exemplifying the industry's shift toward data-driven logistics solutions. White-space opportunities exist in specialized areas including ESD-certified transportation, clean-room mobile solutions, and export control compliance automation, while emerging disruptors leverage blockchain technology for supply chain transparency and autonomous systems for warehouse operations. The competitive landscape increasingly reflects semiconductor industry dynamics, with logistics providers establishing trusted-partner relationships aligned with government incentive programs and national security considerations, fundamentally altering traditional competitive dynamics based purely on cost and service metrics.

Semiconductor Logistics Industry Leaders

-

DHL Supply Chain & Global Forwarding

-

Kuehne + Nagel

-

Nippon Express

-

DSV

-

Yusen Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TSMC unveiled its next-generation A14 process technology at the North America DHL Global Forwarding inaugurated a 24,500 m² air-freight hub at Frankfurt Airport, expanding annual capacity to 300,000 tons with advanced ULD handling technology

- April 2025: DHL Group announced EUR 2 billion (USD 2.20 billion) investment by 2030 in DHL TSMC unveiled A14 process technology, targeting mass-production readiness by 2028 for AI accelerators.

- April 2025: DHL Group committed EUR 2 billion (USD 2.20 billion) through 2030 to scale health-logistics and cold-chain infrastructure, a capability leveraged for EUV chemical flows.

- December 2024: Nippon Express Holdings signed a strategic partnership with Tive to offer real-time monitoring services for semiconductor cargo requiring temperature, humidity, and shock control, leveraging Solo 5G IoT devices.

Global Semiconductor Logistics Market Report Scope

Semiconductor Manufacturing refers to any process or operation that produces semiconductor material, such as slicing or polishing semiconductor material, using photoresists to make intermediate products, or producing semiconductor devices or related solid-state devices. Logistics refers to the process of lifting coal from mines and bulk transportation, which includes loading and unloading at various points as required to complete the transportation. A complete background analysis of the Semiconductor Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Semiconductor Logistics Market is segmented By Function (Transportation, Warehousing and Distribution, and Value-added Services), By Destination (Domestic and International). The report offers market size and forecast values (USD billion) for all the above segments.

| Transportation | Roadways |

| Railways | |

| Water and Seaways | |

| Airways | |

| Warehousing and Distribution | |

| Value-Added Services (Packaging, Customs, Brokerage, Others) |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Domestic |

| International |

| Raw Materials and Chemicals |

| Wafers (Bare and Processed) |

| Packaging Materials |

| Finished Semiconductor Products |

| Others (Photo masks and reticles, Specialty consumables, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Function | Transportation | Roadways |

| Railways | ||

| Water and Seaways | ||

| Airways | ||

| Warehousing and Distribution | ||

| Value-Added Services (Packaging, Customs, Brokerage, Others) | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Destination | Domestic | |

| International | ||

| By Product type | Raw Materials and Chemicals | |

| Wafers (Bare and Processed) | ||

| Packaging Materials | ||

| Finished Semiconductor Products | ||

| Others (Photo masks and reticles, Specialty consumables, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current value of the semiconductor logistics market?

The semiconductor logistics market size stands at USD 86.55 billion in 2026.

How fast is demand for cold-chain services growing?

Cold-chain logistics for semiconductor chemicals is advancing at a 4.78% CAGR through 2031.

Which region captures the largest share of semiconductor logistics activity?

Asia-Pacific leads with 43.10% share, thanks to its integrated manufacturing ecosystem.

Why are AI-based routing platforms important to semiconductor logistics?

AI tools cut planning cycles, predict ETA within minutes, and provide real-time cargo monitoring, raising supply-chain resilience.

How do government incentives affect logistics flows?

Programs like the CHIPS Act channel production toward the United States and Europe, creating new domestic corridors and trusted-partner requirements.

Which segment of logistics is growing quickest?

Value-added services, including packaging and export-control compliance, are expanding at a 4.08% CAGR to 2031.

Page last updated on: