Selective Catalytic Reduction Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

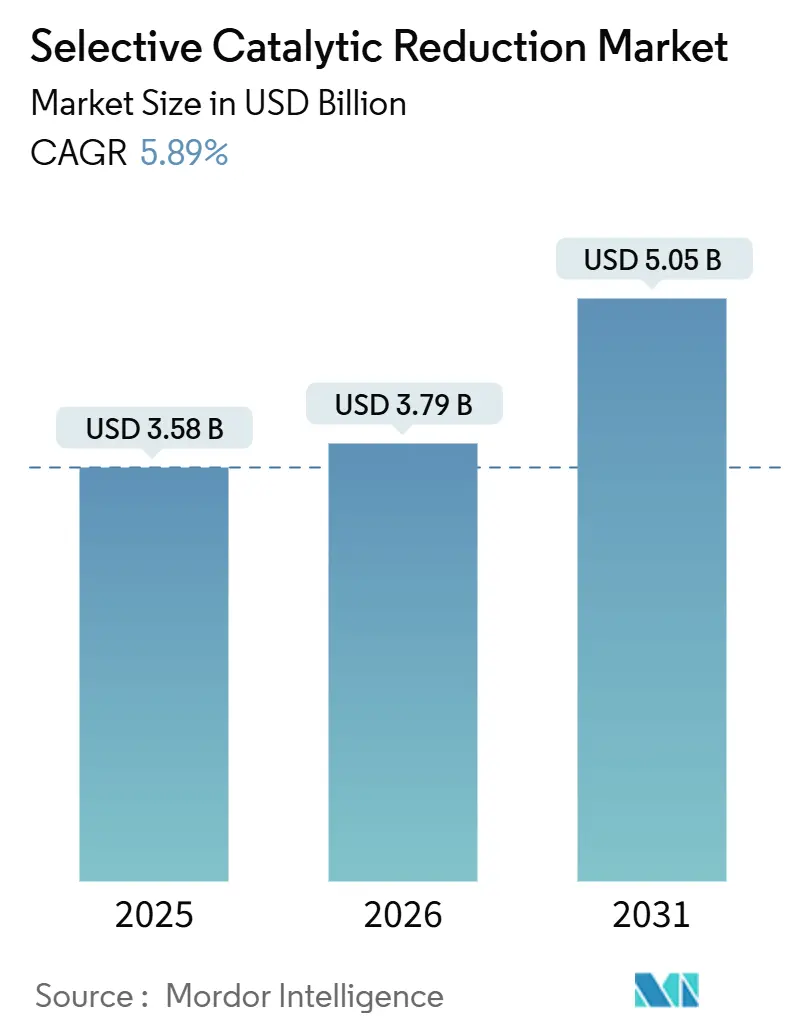

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 5.05 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

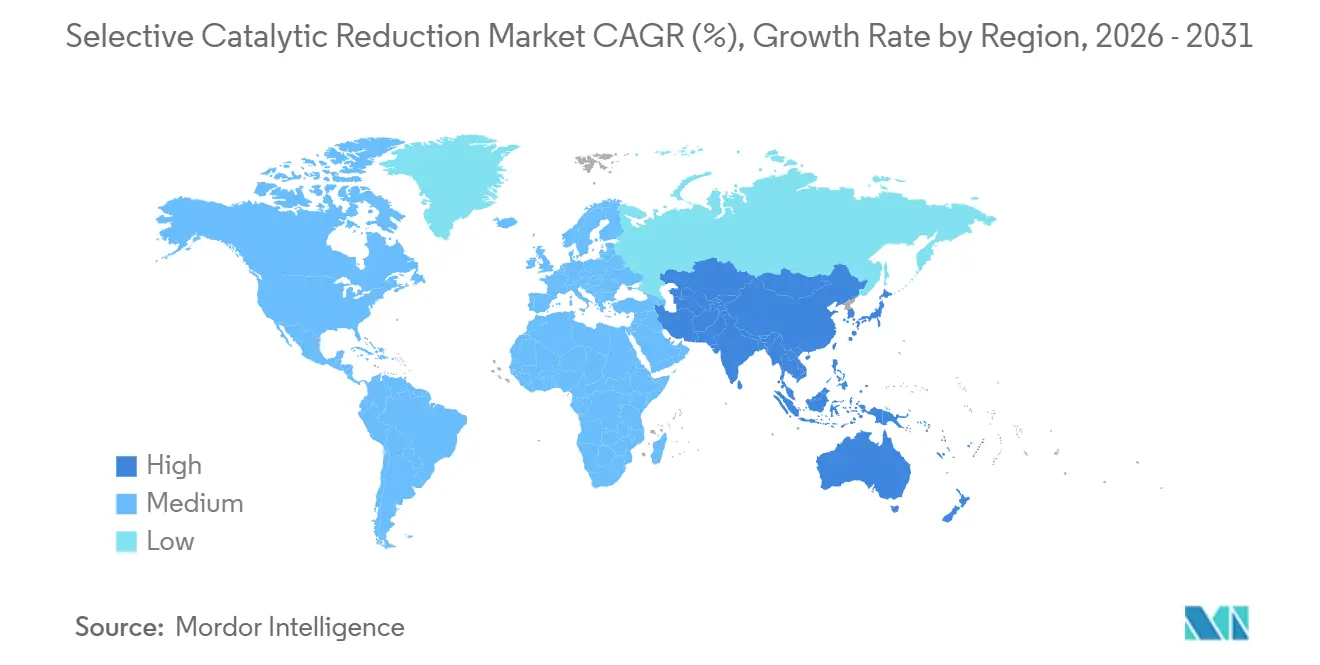

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Selective Catalytic Reduction Market Analysis by Mordor Intelligence

The Selective Catalytic Reduction Market size is expected to grow from USD 3.58 billion in 2025 to USD 3.79 billion in 2026 and is forecast to reach USD 5.05 billion by 2031 at 5.89% CAGR over 2026-2031. Demand is shifting from coal-fired power toward marine propulsion, heavy-duty road transport, and coal-to-chemicals complexes that view NOx compliance as non-negotiable. The International Maritime Organization’s 2025 expansion of Emission Control Areas sparked a surge of retrofit projects, while China’s 50 mg/Nm³ industrial limit has locked SCR into the design basis of major coal-to-chemicals plants. Catalyst suppliers now focus on lengthening service life under sulfur-rich gas streams and lowering precious-metal loadings to curb cost escalation. Consolidation, illustrated by Honeywell’s purchase of Johnson Matthey’s catalyst division, underlines an industry race for scale and lifecycle services.

Key Report Takeaways

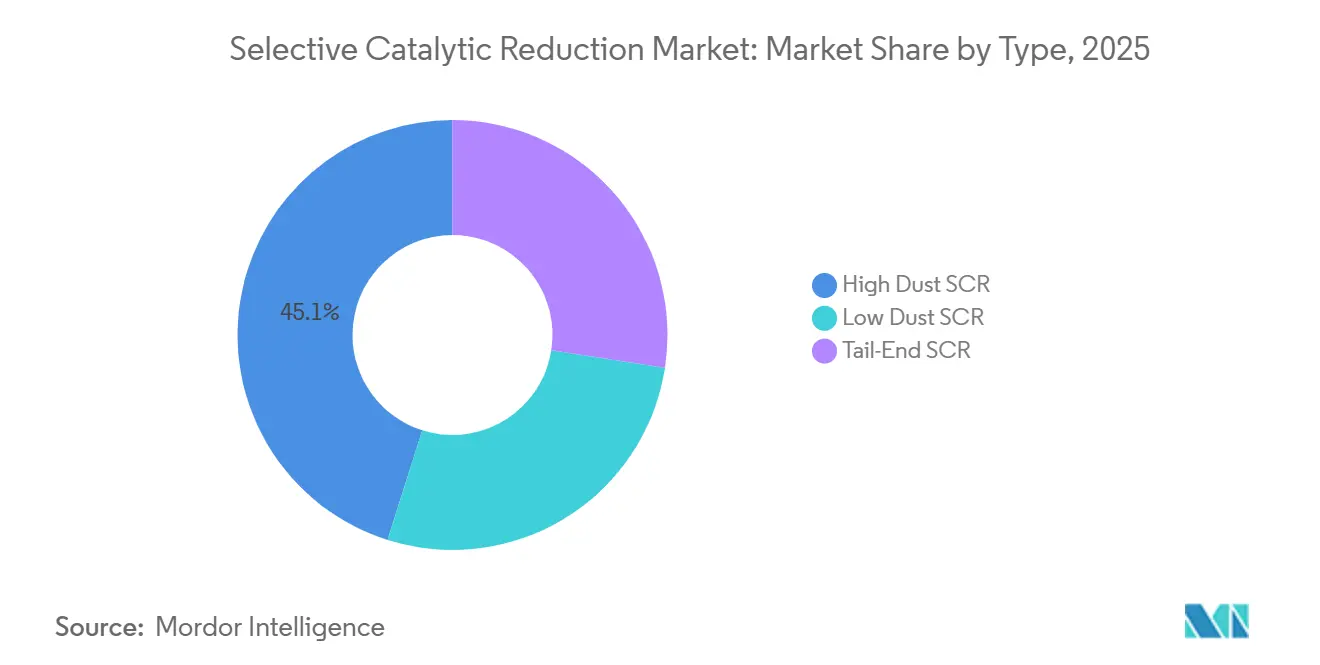

- By type, High Dust SCR commanded a 45.12% of the Selective Catalytic Reduction market share in 2025; Tail-End SCR is projected to expand at a 6.18% CAGR through 2031.

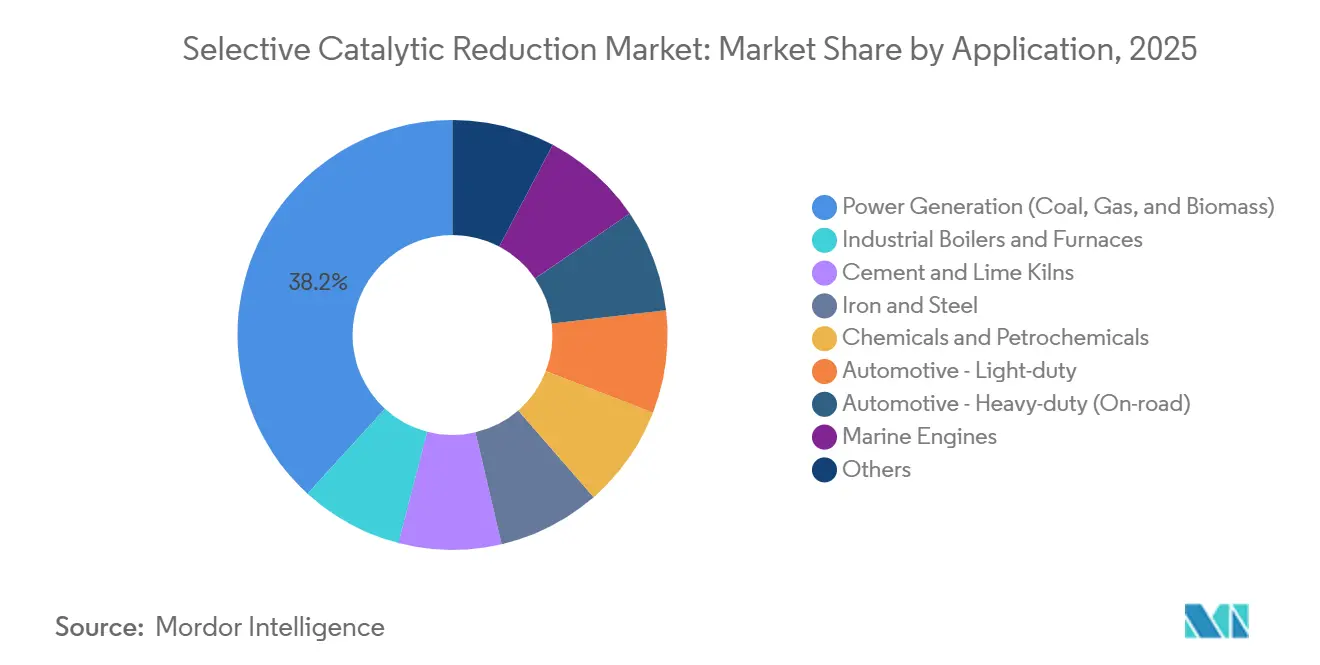

- By application, Power Generation (Coal, Gas, and Biomass) held a 38.22% share of the Selective Catalytic Reduction market size in 2025, while Automotive - Heavy-duty (On-road) is advancing at a 6.33% CAGR to 2031.

- By geography, Asia-Pacific accounted for 51.25% of the Selective Catalytic Reduction market share in 2025 and is moving ahead at a 6.29% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Selective Catalytic Reduction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in marine SCR retrofits ahead of IMO Tier III | +1.2% | Global, concentrated in North Europe, North America ECAs, expanding to Asia-Pacific coastal routes | Medium term (2-4 years) |

| Rapid build-out of coal-to-chemicals plants in Asia-Pacific | +0.9% | Asia-Pacific core (China, India), spillover to Southeast Asia | Long term (≥ 4 years) |

| Adoption of low-temperature vanadium-ceria catalysts in cement kilns | +0.6% | Global, early adoption in EU and China cement sectors | Medium term (2-4 years) |

| OEM validation of SCR for hydrogen-fuelled engines | +0.4% | North America, EU, Japan (hydrogen infrastructure corridors) | Long term (≥ 4 years) |

| AI-driven adaptive ammonia injection controls | +0.7% | Global, initial deployment in large coal/gas power plants (>500 MW) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Marine SCR Retrofits Ahead of IMO Tier III

Tier III rules require an 80% NOx cut, driving owners to retrofit SCR on vessels that enter Emission Control Areas. The 2025 designation of the Norwegian Sea and Canadian Arctic widened compliance zones and generated a backlog exceeding 3,000 vessels. Cruise operators moved fastest, fitting 81 ships with SCR by 2025, up from 7 in 2018[1]International Maritime Organization, “Emission Control Areas Expansion,” imo.org. Retrofit costs run USD 1.5-4 million per ship, but new engines such as WinGD’s X-DF-HP integrate SCR from the factory, trimming total cost of ownership by 15%. As more Tier III-ready tonnage is delivered post-2028, retrofit demand will cool, yet catalyst replacement will stay resilient through the 2030s.

Rapid Build-Out of Coal-to-Chemicals Plants in Asia-Pacific

China’s Shaanxi Coal Yulin complex embeds SCR to meet the 50 mg/Nm³ NOx cap, a precedent for other mega-projects. India’s 100-ton coal-gasification mission follows suit, but higher sulfur coal accelerates catalyst poisoning, inflating lifecycle cost. The public-health imperative remains clear, with studies showing SCR deployment could avert up to 210,000 premature deaths over a decade.

Adoption of Low-Temperature Vanadium-Ceria Catalysts in Cement Kilns

Cerium-doped vanadium catalysts now achieve greater than or equal to 70% NOx removal at less than 200°C, cutting reheating fuel expense and CO₂. CERI’s 2025 pilot recorded more than 90% abatement at 120-140°C, slicing annual operating cost by up to 40% for a 360 m² sintering line. Commercial uptake still hinges on evidence of 3-5 year service life under alkali and sulfate attack.

OEM Validation of SCR for Hydrogen-Fuelled Engines

Hydrogen ICE (internal combustion engine) platforms from Cummins and others need passive or urea-fed SCR to curb NOx. Early trials show a 60-70% reduction at 150°C, yet N₂O formation and hydrothermal aging remain hurdles. Commercial impact will appear from 2028 onward along advanced hydrogen corridors in the EU and Japan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating electrification of light-duty vehicles | -0.8% | Global, most pronounced in EU, China, North America | Short term (≤ 2 years) |

| SO₂/SO₃ poisoning shortening catalyst life | -0.5% | Asia-Pacific (high-sulfur coal regions), India, Southeast Asia, South America | Medium term (2-4 years) |

| Regulatory ambiguity around blue-ammonia bunkering | -0.3% | Global maritime, regulatory gaps in bunkering infrastructure and safety standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Electrification of Light-Duty Vehicles

Global BEV (battery electric vehicle) sales topped 14 million in 2025, displacing diesel engines that drove aftermarket SCR catalyst sales[2]European Commission, “Euro 7 Passenger Car Standards,” europa.eu. Euro 7 rules, effective 2027, tighten limits further but favor zero-tailpipe options, prompting Johnson Matthey to cut Platinum Group Metal (PGM) loadings 20% to defend share. Heavy-duty regulations in the U.S. will cushion demand until fuel-cell and battery trucks scale after 2030.

SO₂/SO₃ Poisoning Shortening Catalyst Life

SO₃ forms stable sulfates on active sites, forcing earlier replacement. Plants burning Indian coal with 0.4-0.8% sulfur report 40-50% faster deactivation than design, driving SCR life down to 3-4 years. Flue Gas Desulphurization (FGD) units can mitigate risk but add USD 50-80 per kW in capex and 1-2% parasitic load.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: High Dust Configurations Dominate Coal Applications

High-Dust systems captured 45.12% of the Selective Catalytic Reduction market share in 2025. Operating upstream of particulate filters lets these units stay within 300-420°C, avoiding reheating but demanding erosion-resistant channels. CORMETECH’s Dustbuster modules highlight such design features. Tail-End SCR, favored by gas turbines and marine engines, is expected to grow at the fastest CAGR of 6.18% during the forecast period (2026-2031) as low-temperature catalysts mature. The Selective catalytic reduction market size for Tail-End installations is projected to exceed USD 1 billion by 2031.

Continued catalyst advances will decide growth tempo. Trials of 3% V₂O₅-10 % MoO₃/TiO₂ show more than 67% average removal at 160-180°C over two years, while CERI’s heat-free design achieved more than 90% removal at 120-140°C. Yet ammonium bisulfate fouling below 200°C remains a constraint for operators.

By Application: Heavy-Duty Automotive Outpaces Power Generation

Power Generation (Coal, Gas, and Biomass) held 38.22% of the 2025 revenue of the Selective Catalytic Reduction market. Automotive - Heavy-duty (On-road) leads with 6.33% CAGR for the forecast period (2026-2031), driven by the US 2027 standard mandating 0.02 g/bhp-hr NOx and dual-stage SCR plus electric heating. The Selective catalytic reduction market size tied to heavy-duty vehicles could reach USD 1.5 billion by 2031.

Marine retrofits remain pivotal. Cruise and offshore segments show retrofits can deliver 85-95% NOx cuts without fuel-economy loss. Industrial boilers, cement, and petrochemicals together contribute roughly 30% of demand, with the strict 50 mg/Nm³ Chinese limit keeping Asia-Pacific ahead.

Geography Analysis

Asia-Pacific accounted for 51.25% of the Selective Catalytic Reduction market share in 2025 and is set to expand at 6.29% CAGR to 2031. China’s 50 mg/Nm³ industrial cap embeds SCR in every new coal-to-chemicals line, while India’s 100-ton gasification mission mirrors this pathway. Higher sulfur coal in India raises catalyst cost but also cements FGD retrofits. Japan’s 800,000 tons per year low-carbon ammonia contracts point to early deployment of ammonia-fired turbines that will need to be tailored.

In North America, the EPA 2027 heavy-duty rule propels on-road demand, and combined-cycle retrofits keep utility orders flowing. Kentucky regulators highlighted a finished SCR project that closed under budget, informing cost expectations for new gas units. Canadian Arctic ECA status pushes vessel retrofits, but cold climate imposes urea-handling challenges.

In Europe, coal retirements dampen utility orders, yet the Industrial Emissions Directive’s 200 mg/Nm³ limit for new cement kilns underpins low-temperature catalyst uptake. The 2025 Norwegian Sea ECA extended marine compliance northward, driving ferry and cruise retrofits. Honeywell’s bid for Johnson Matthey reflects a consolidating regional supplier base.

Competitive Landscape

The Selective Catalytic Reduction market is moderately concentrated. Chinese firms such as CERI disrupt with ultra-low-temperature systems that erase reheating cost, a strong lure for hard-to-abate industries. AI-enhanced dosing platforms are emerging as a wedge for differentiation. Honeywell and Emerson ship edge controllers that promise 5-10% reagent savings, matching utility cost-cutting goals. Future white space lies in ammonia-fuel engines, hydrogen ICEs, and Asian coal-chemicals, domains where catalyst design for N₂O control and sulfur tolerance remains underserved.

Selective Catalytic Reduction Industry Leaders

Johnson Matthey

BASF

Topsoe A/S

CORMETECH

Tenneco Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: YANMAR Marine International unveiled its SCR system. This system aims to drastically reduce NOx emissions from commercial vessels equipped with engines over 130 kW, especially in Emission Control Areas (ECAs). YANMAR's SCR system aligns with the International Maritime Organization's (IMO) Tier III emission standards.

- July 2025: Northwestern University developed a method to integrate metal-sulfur active sites into metal-organic frameworks, significantly enhancing catalytic efficiency in hydrogenation reactions and providing new strategies for designing advanced SCR catalysts.

Global Selective Catalytic Reduction Market Report Scope

Selective Catalytic Reduction (SCR) is an advanced emissions control technology that converts harmful nitrogen oxides in exhaust gas into nitrogen and water. It uses a catalyst and a reducing agent to achieve up to 90%+ nitrogen oxides reduction efficiency, commonly in diesel engines and industrial plants.

The Selective Catalytic Reduction market is segmented by type, application, and geography. By type, the market is segmented into high dust SCR, low dust SCR, and tail-end SCR. By application, the market is segmented into power generation (coal, gas, and biomass), industrial boilers and furnaces, cement and lime kilns, iron and steel, chemicals and petrochemicals, automotive - light-duty, automotive - heavy-duty (on-road), marine engines, and others. The report also covers the market size and forecasts for Selective Catalytic Reduction in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| High Dust SCR |

| Low Dust SCR |

| Tail-End SCR |

| Power Generation (Coal, Gas, and Biomass) |

| Industrial Boilers and Furnaces |

| Cement and Lime Kilns |

| Iron and Steel |

| Chemicals and Petrochemicals |

| Automotive - Light-duty |

| Automotive - Heavy-duty (On-road) |

| Marine Engines |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | High Dust SCR | |

| Low Dust SCR | ||

| Tail-End SCR | ||

| By Application | Power Generation (Coal, Gas, and Biomass) | |

| Industrial Boilers and Furnaces | ||

| Cement and Lime Kilns | ||

| Iron and Steel | ||

| Chemicals and Petrochemicals | ||

| Automotive - Light-duty | ||

| Automotive - Heavy-duty (On-road) | ||

| Marine Engines | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Selective catalytic reduction market in 2031?

Selective Catalytic Reduction market is projected to reach USD 5.05 billion by 2031, growing at a 5.89% CAGR from 2026.

Which region leads demand for Selective catalytic reduction technology?

Asia-Pacific accounted for 51.25% of 2025 revenue and is expanding at a 6.29% CAGR through 2031.

Which application segment is growing fastest?

Automotive Heavy-duty on-road engines are advancing at 6.33% CAGR due to the U.S. 2027 NOx rule.

Why are Tail-End SCR systems gaining popularity?

Advances in low-temperature catalysts allow installation after desulfurization, avoiding costly reheating and enabling use on gas turbines and marine engines.

Page last updated on: