Phase Transfer Catalyst Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

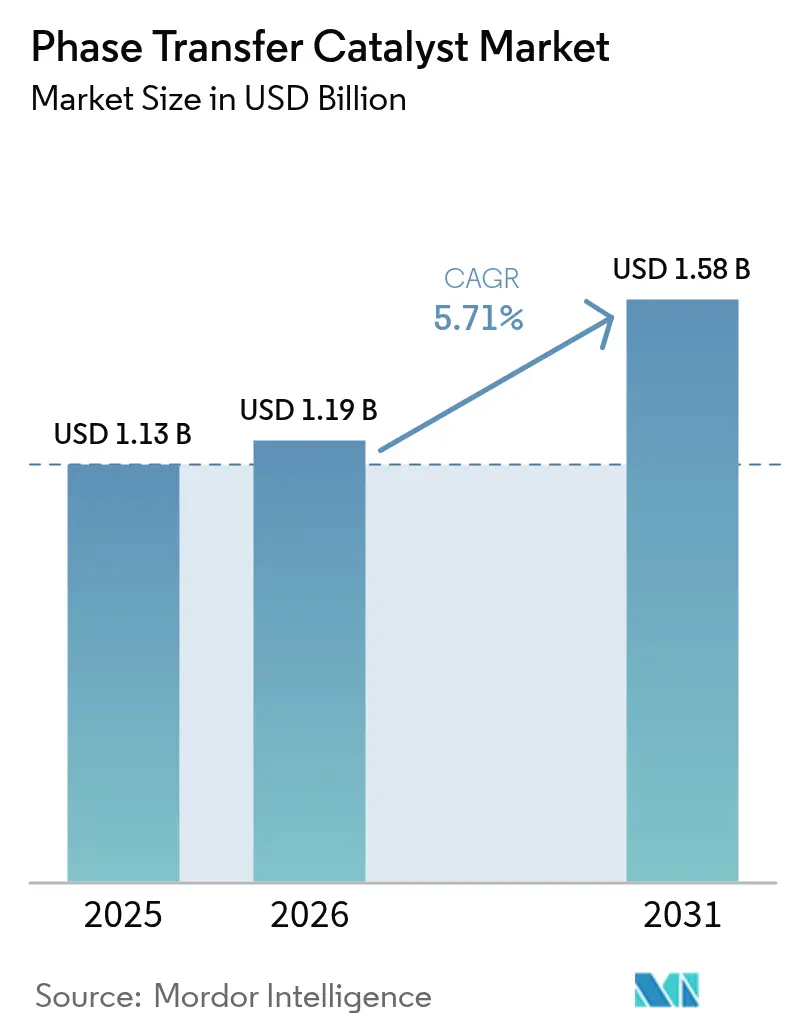

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phase Transfer Catalyst Market Analysis by Mordor Intelligence

The Phase Transfer Catalyst market size is expected to grow from USD 1.13 billion in 2025 to USD 1.19 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at 5.71% CAGR over 2026-2031. Robust demand stems from pharmaceutical green-chemistry adoption, expanding lithium-ion battery production, and the cost advantages of heterogeneous catalysis. Battery electrolyte additives present a rapidly growing niche that offsets pricing pressure in traditional drug synthesis. Intensifying competition from ionic-liquid and enzymatic systems is prompting incumbents to invest in supported catalysts and vertical integration to contain feedstock volatility. Integrated producers that control bromine, caustic soda, and quaternary ammonium capacity remain better shielded from 2025’s raw-material price swings, enabling them to safeguard margins while meeting tightening environmental norms.

Key Report Takeaways

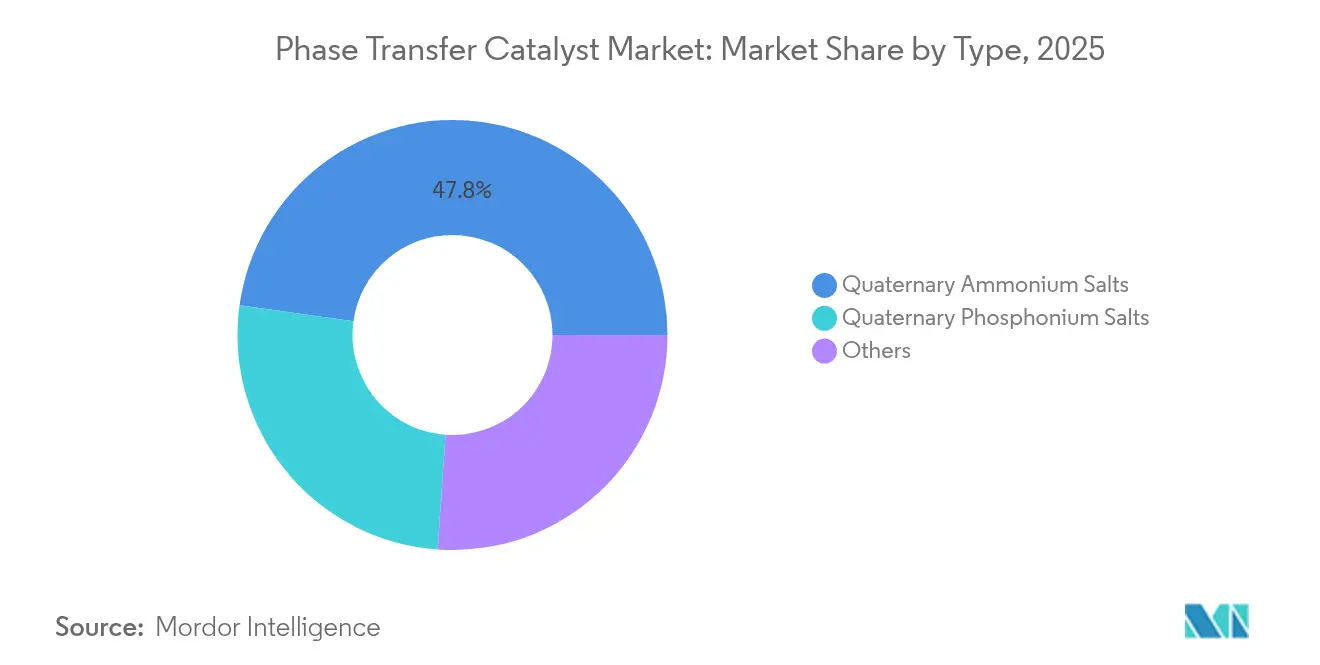

- By type, Quaternary Ammonium Salts held 47.79% of the Phase Transfer Catalysts market share in 2025 and are expanding at a 5.89% CAGR through 2031.

- By form, Liquid PTC accounted for 52.05% of the Phase Transfer Catalysts market size in 2025, while Supported/Immobilised PTC leads future growth at 6.02% CAGR to 2031.

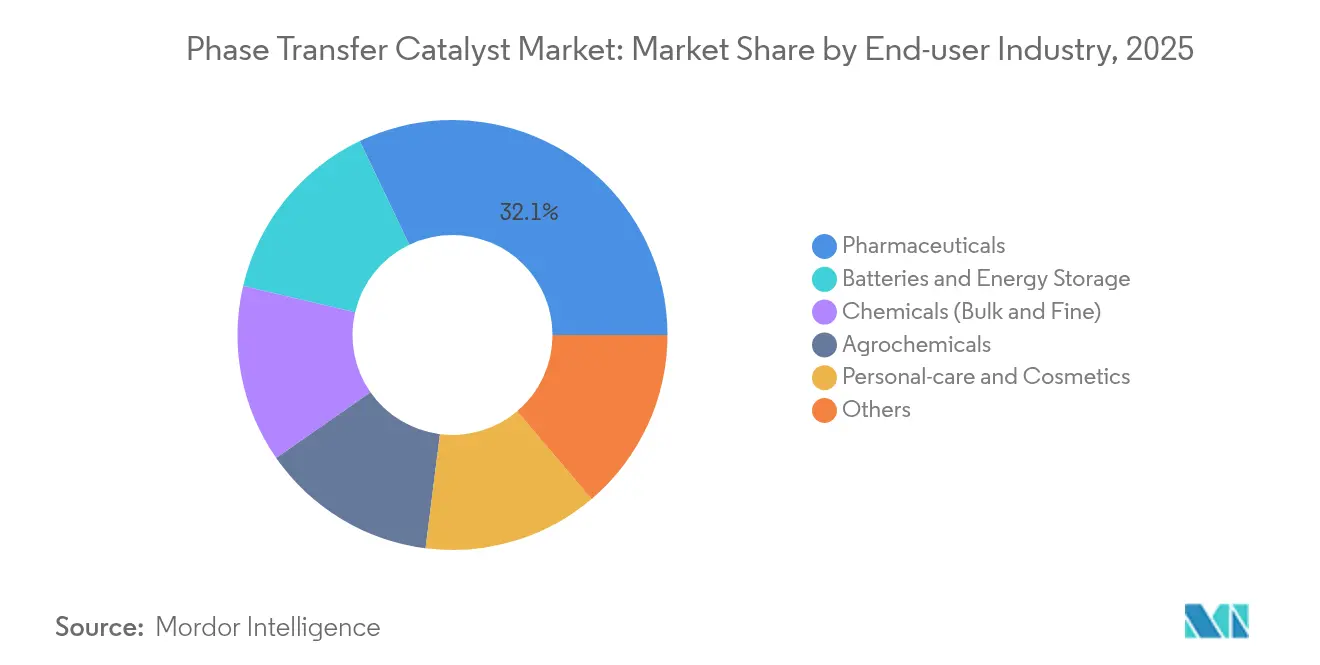

- By end-user industry, the pharmaceutical segment captured 32.10% revenue share in 2025 in the phase transfer catalyst market; Batteries and Energy Storage is advancing at the fastest 6.88% CAGR through 2031 in the phase transfer catalyst market.

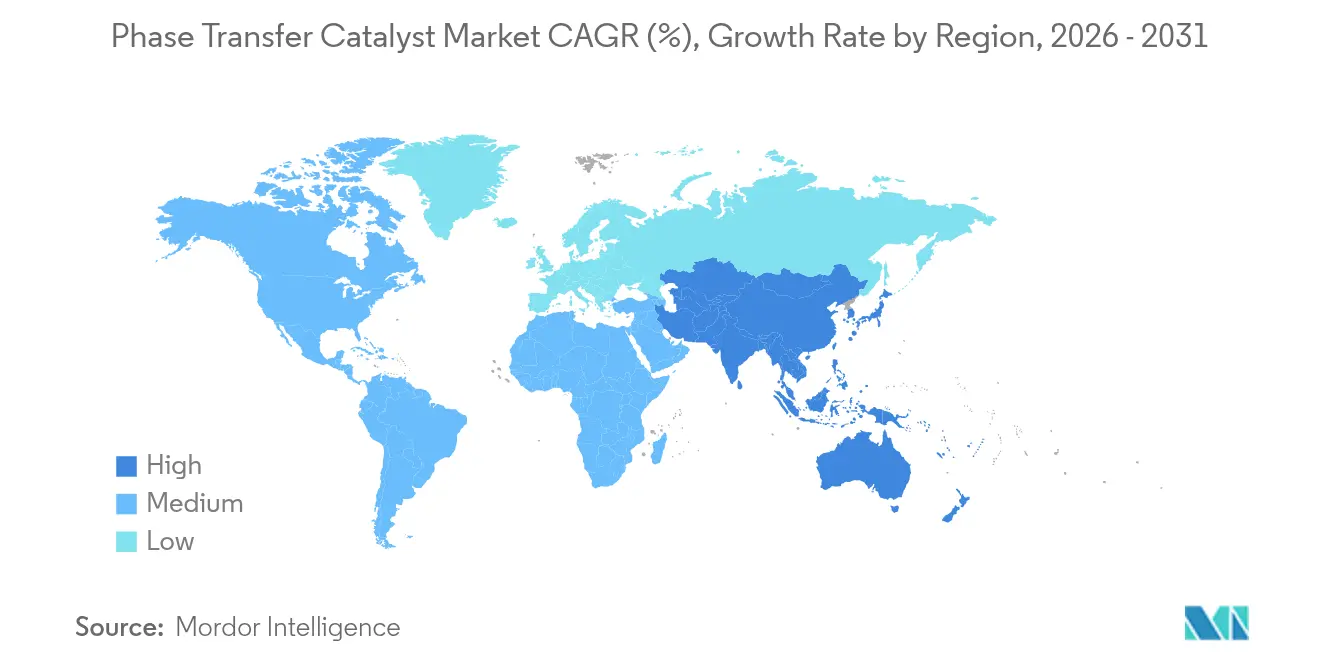

- By geography, Asia Pacific commanded 37.55% share of the Phase Transfer Catalysts market in 2025 and is on track for a 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phase Transfer Catalyst Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing application in pharmaceutical APIs | +1.8% | Asia Pacific, North America | Medium term (2–4 years) |

| Demand-side pull from green chemistry compliance | +1.5% | EU, North America | Long term (≥ 4 years) |

| Expansion of agrochemical active production | +1.2% | Asia Pacific, Latin America | Medium term (2–4 years) |

| Process-cost advantage over homogeneous catalysts | +0.9% | Global | Short term (≤ 2 years) |

| Use in Li-ion battery electrolyte additives | +1.1% | Asia Pacific, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Application in Pharmaceutical APIs

Pharmaceutical manufacturers rely on phase transfer catalysis to meet green-chemistry mandates while controlling costs, highlighting trends in the phase transfer catalyst industry. Mild reaction conditions lower energy input, and catalyst recyclability reduces waste disposal. Evonik’s reorganization around lipid specialties for mRNA therapies illustrates how large suppliers are refocusing on higher-value drug intermediates. Continuous-manufacturing adoption in the United States and Europe increases demand for supported systems that simplify catalyst recovery. Reshoring programs in both regions add extra pull for local, sustainable PTC solutions that compete with historic Asian low-cost supply.

Demand-side Pull from Green Chemistry Compliance

Environmental regulation underpins the steady uptake of PTC in the phase transfer catalyst industry. The EPA now targets a 65% reduction in hazardous-air-pollutant use, steering chemical plants toward aqueous or solvent-free routes that PTC enables[1]U.S. Environmental Protection Agency, “Pollution prevention update 2025,” epa.gov. California’s consumer-products rule imposes stringent VOC caps, encouraging waterborne reactions. The EU Chemicals Strategy further rewards circular-economy catalysts with low emissions. Compliance-driven buying supports PTC volumes even during macro-slowdowns, giving early adopters a competitive edge in eco-sensitive markets.

Expansion of Agrochemical Actives Production

Asia Pacific agrochemical makers adopt PTC to raise selectivity and curb by-product formation, reflecting trends in the phase transfer catalyst market. Inverse-PTC synthesis of 2,4-D acid yields cleaner product streams, trimming effluent treatment costs. Emerging multi-site catalysts raise turnover numbers, boosting productivity for herbicide and fungicide lines. Patent literature from Dow Agrosciences evidences industry-wide migration toward PTC in next-generation crop-protection molecules. Rising demand for precision pesticides and growing food-security investments sustain this driver.

Process-cost Advantage over Homogeneous Catalysts

PTC slashes solvent volumes, eliminates phase-separation hardware, and allows catalyst reuse, benefiting the phase transfer catalyst market. Fiber-supported quaternary ammonium systems remain active across 15 cycles with negligible yield loss, lowering variable costs. Continuous PTC reactors cut VOC emissions compared with batch operations, trimming permitting expenses. Supported ionic-liquid phases add selectivity gains without sacrificing throughput, giving manufacturers tangible operating-expenditure relief.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of quaternary ammonium feedstocks | –1.3% | Asia Pacific | Short term (≤ 2 years) |

| Competition from ionic liquid/enzymatic catalysts | –0.8% | North America, EU | Medium term (2–4 years) |

| Aquatic-toxicity scrutiny of phosphonium salts | –0.6% | EU, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Quaternary Ammonium Feedstocks

Bromine prices surged more than 40% in early 2025 amid logistics disruptions on Chinese and Jordanian routes, impacting the phase transfer catalyst market. Concurrent caustic-soda tightness, fueled by construction-sector rebound, threatens supply stability. European chlor-alkali plants grapple with energy inflation, passing higher costs to PTC buyers. Producers with captive chlorine and bromine resources or long-term contracts mitigate these shocks and maintain competitive pricing.

Competition from Ionic-liquid/Enzymatic Catalysts

Protic ionic liquids deliver greater substrate compatibility and superior sustainability metrics in the phase transfer catalyst market, particularly in biodiesel and CO₂-conversion reactions. Enzymes in deep-eutectic solvents enhance pharmaceutical intermediate yields while lowering toxicity footprints. Hybrid supported systems merge ionic-liquid selectivity with PTC mass-transfer efficiency, challenging traditional quaternary ammonium formats. As regulatory scrutiny tightens, these alternatives will capture share in high-value segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ammonium Salts Drive Market Leadership

Quaternary Ammonium Salts hold a commanding 47.79% share. Wide deployment in drug and agrochemical synthesis, supported supply chains, and well-documented reaction mechanisms keep them at the forefront. The segment is forecast to grow at 5.89% CAGR to 2031 as demand rises for efficient, environmentally compliant processes. Quaternary Phosphonium Salts occupy the next tier, appealing to battery electrolyte formulators seeking higher thermal durability. The niche “Others” category, spanning chiral and multi-site catalysts, addresses asymmetric synthesis for specialty APIs where single-enantiomer purity commands premium pricing.

By Form: Supported Systems Gain Momentum

Liquid formulations led the phase transfer catalyst market in 2025 with a 52.05% share. Familiar handling protocols and compatibility with legacy reactors sustain demand across fine chemicals. Supported/Immobilised systems, however, are set to outpace other forms with a 6.02% CAGR, reflecting industry preference for catalysts that simplify separation, minimize quaternary ammonium discharge, and reduce total solvent footprints.

By End-user Industry: Battery Applications Accelerate

The pharmaceutical sector retained 32.10% of the phase transfer catalyst market share in 2025, driven by green-chemistry compliance and continuous-manufacturing initiatives. Meanwhile, Batteries and Energy Storage displays the strongest 6.88% CAGR, propelled by global electric-vehicle adoption and grid-scale storage programs. Quaternary ammonium additives mitigate interfacial resistance and extend cycle life, attributes prized by cell makers targeting longer warranties.

Chemical producers leverage PTC to reduce cost in commodity lines in the phase transfer catalyst market, while agrochemical formulators exploit higher selectivity for pesticide intermediates. Personal-care applications move steadily despite scrutiny of quaternary ammonium safety profiles in rinse-off products. Battery-focused innovation rounds out the value proposition: multifunctional electrolyte additives employing PTC principles are under development to solve dendrite formation and thermal-runaway risks, potentially unlocking next-generation solid-state batteries.

Geography Analysis

Asia Pacific holds a 37.55% share in the phase transfer catalyst market and is projected to post a 6.18% CAGR to 2031. China’s pivot toward complex APIs and India’s specialty-chemical capacity build-out underpin regional dominance. Multinational expansions, such as Evonik’s specialty amine capacity in Nanjing, further consolidate the supply base. Regional lithium-ion gigafactories add demand for electrolyte additives, reinforcing a self-sustaining PTC ecosystem.

North America remains a pivotal buyer in the phase transfer catalyst market, supported by reshoring incentives and heightened environmental scrutiny. The EPA’s 2025 hazardous-pollutant thresholds push chemical firms toward PTC routes with lower solvent loads, locking in resilient baseline demand. Europe prioritizes sustainability and circular-economy alignment, driving uptake of recyclable catalysts and hybrid ionic-liquid systems. The EU Chemicals Strategy stipulates safe-and-sustainable-by-design criteria, positioning supported PTC as a favored alternative over legacy homogeneous halide processes.

Regulatory Landscape

Chemical regulation affecting phase transfer catalysts is tightening in the two most compliance-driven import markets, the United States and the European Union. This is increasing the documentation burden for quaternary ammonium and related catalyst chemistries used across pharma, agrochemical, and battery value chains. In the United States, the EPA finalized updates to the TSCA new-chemicals regulations in December 2024, aligning reviews more closely with Lautenberg Act requirements and narrowing pathways such as Low Volume Exemptions and Low Release and Exposure Exemptions for certain persistent, bioaccumulative, and toxic chemistries. That can slow commercialization of new PTC variants.

In 2026, the EPA also advanced the use of Significant New Use Rules (SNURs), which require advance notification (typically 90 days) before starting designated new uses. In Europe, compliance is shaped by REACH restriction planning and a rolling restriction roadmap updated in late June 2025, reinforcing the need for early hazard and exposure data packages and substance stewardship for suppliers serving regulated end users. Alongside US and EU regimes, OECD chemical safety work (progress reporting in 2025) continues to influence global test methods and dossier expectations, pushing multinational PTC suppliers toward more harmonized data generation and safer-by-design product positioning.

Value Chain Analysis

The phase transfer catalyst value chain starts with feedstocks linked to chlor-alkali and bromine chains (and related alkylation inputs used for quaternization), then moves through synthesis of catalyst families such as quaternary ammonium salts, quaternary phosphonium salts, quaternary ammonium bases, and specialty catalysts such as crown ethers. Upstream integration into bromine and basic chemicals is strategically important because raw-material volatility directly affects the economics of mainstream quaternary ammonium products. Supported and immobilized systems also add additional inputs (carriers, resins, or solid supports) and processing steps to improve recovery and reduce discharge.

Midstream production is concentrated among specialty manufacturers with strong footprints in Asia. This includes India-based suppliers such as Pacific Organics, Prabhat Chemiorganics, Delta Finochem, and Element Chemilink, as well as China-based producers such as Zibo Koyon Chemical Technology and Kente Catalysts. Downstream, PTCs are sold via direct contracts and distributors into pharmaceuticals, agrochemicals, bulk and fine chemicals, personal care, and the emerging battery and energy storage additive chain. Qualification and batch-to-batch consistency are critical, and compliance gates shape procurement, including the EPA’s December 2024 TSCA updates for new chemical reviews, which can raise pre-market workload for new catalyst chemistries. As a result, suppliers serving US and EU customers tend to prioritize well-characterized chemistries, robust quality systems, and defensible safety documentation.

Competitive Landscape

The Phase Transfer Catalysts market features moderate fragmentation. Evonik Industries, Solvay, and Dishman Carbogen Amcis anchor the high-end segment through vertically integrated feedstocks and global technical-service footprints. Competitive pressure intensifies as ionic-liquid and enzymatic alternatives vie for share in regulated markets. Incumbents respond by expanding supported-catalyst lines and sourcing renewable quaternary ammonium precursors.

Phase Transfer Catalyst Industry Leaders

Solvay

Merck KGaA

SACHEM Inc.

Tatva Chintan Pharma Chem Ltd

Dishman Carbogen Amcis Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Higher-value and easier-to-handle catalyst formats are gaining traction where manufacturers want reduced waste and simpler separation. This aligns with the market shift toward supported and immobilized systems in regulated manufacturing. Continuous processing is another opportunity area, particularly where PTCs can be paired with flow platforms to lower solvent use and improve mass transfer, as reflected by 2026 peer-reviewed work demonstrating a continuous-flow concept using solid NaOH particles and phase-transfer catalysts to reduce chemical waste in organic synthesis.

On the supply side, capacity and capability additions in specialty catalysts and closely adjacent chemistries create routes for suppliers to capture incremental demand from pharmaceuticals, agrochemicals, and emerging electronics-grade applications. In India, Tatva Chintan Pharma Chem’s Dahej investments in 2026, including commissioning activity tied to quaternary ammonium and phosphonium phase transfer catalysts and a subsequent greenfield expansion plan at Dahej-III with substantial new reactor capacity, point to active capacity build-out targeted at specialty chemical volumes. In Europe, BASF’s scheduled 2026 operational start of a new catalyst production facility in Ludwigshafen, focused on high-performance and application-specific catalysts, underlines continued investment in application-driven catalyst manufacturing infrastructure, supporting customer-specific formulations and qualification-driven supply chains.

Recent Industry Developments

- July 2026: Tatva Chintan Pharma Chem Ltd approved a greenfield expansion at Dahej-III (Gujarat, India) with an announced investment of INR 200 crore and plans to add 344 KL of aggregate reactor capacity. The project increases the company’s manufacturing headroom for specialty chemistries that include quaternary ammonium and phosphonium phase transfer catalyst products. This adds competitive pressure in global supply chains where large-volume, consistent PTC supply and documentation are differentiators.

- May 2026: Tatva Chintan Pharma Chem Ltd reported the start of full commercial production from its phase-3 Dahej expansion, taking its total licensed capacity to 48,000 TPA. The ramp-up improves near-term availability of specialty chemical output relevant to PTC and adjacent product lines while strengthening responsiveness to qualification-driven customer demand. Increased domestic capacity also supports export-oriented supply to pharmaceutical and agrochemical customers that prefer multi-site sourcing.

- July 2025: Dishman Carbogen Amcis Ltd highlighted Ethyl Triphenyl Phosphonium Bromide (ETPPB) as a phase transfer catalyst offering at Specialty and Agro Chemicals America 2025. The visibility given to phosphonium-based PTCs underscores continued commercialization focus beyond quaternary ammonium salts, particularly for applications needing different performance or handling profiles. Such product positioning can influence buyer switching decisions in agrochemical and fine-chemical process development.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue earned from phase transfer catalyst products sold for industrial use to enable reactions between immiscible phases, across key chemical manufacturing value chains.

Scope exclusions: We exclude in-house captive catalysts that are not sold commercially, as well as unrelated reaction aids and solvents that may be used in the same processes.

Segmentation Overview

- By Type

- Quaternary Ammonium Salts

- Quaternary Phosphonium Salts

- Others

- By Form

- Liquid PTC

- Solid PTC

- Supported / Immobilised PTC

- By End-user Industry

- Pharmaceuticals

- Chemicals (Bulk and Fine)

- Agrochemicals

- Personal-care and Cosmetics

- Batteries and Energy Storage

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping where phase transfer catalysts are used and what demand signals can be tracked consistently by geography and end-use. We refer to public sources such as the US International Trade Commission trade data, UN Comtrade, the US EPA Chemical Data Reporting context for chemical production patterns, Eurostat industrial production series, and national statistics releases that report chemical output indices.

To ground end-use pull, we also use sources such as FDA public manufacturing and product information context, European Chemicals Agency public pages on regulated substances, and peer reviewed chemistry journals that discuss catalyst families and typical use rates. Company filings, investor presentations, and reputable press releases help validate capacity expansions, product positioning, and pricing commentary. Where available, we complement this with paid subscriptions for company financials and intelligence, patent databases, and shipment level import export data to fill gaps in product mapping and cross border flows. These are illustrative examples, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the demand pool and to confirm what is actually purchased as a phase transfer catalyst, rather than adjacent additives used in the same batches. We speak with a mix of catalyst producers, distributors, and downstream users in pharmaceuticals, agrochemicals, and specialty chemicals. We then validate assumptions on pricing, substitution, and procurement cycles across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 43% |

| Mid tier: 56% | Functional/Unit leaders: 29% | EMEA: 37% |

| Smaller Players: 15% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where chemical production and trade indicators are used to reconstruct the demand pool for reactions that commonly require phase transfer catalysts, then the spend is derived using adoption and use-rate assumptions. To keep this practical, we rely on a small set of inputs that can be explained and rechecked, such as output trends in pharmaceuticals and agrochemicals, specialty chemical production indices, import export movements for relevant intermediates, observed shifts toward green-chemistry process routes, and the split between liquid, solid, and supported forms.

The total is corroborated with selective bottom-up approximations, mainly sampled volume by end-use multiplied by an average selling price range gathered from channel checks, along with supplier revenue sanity checks where disclosures allow it. When a full bottom-up roll-up is not possible for fragmented countries, we bridge gaps using proxy relationships, such as chemical output growth and the local mix of end-use industries, and then we adjust after expert feedback.

For forecasting, scenario analysis is applied around a central case, since pricing and adoption can move differently depending on regulatory pressure and process optimization cycles. The forward view is then refined using expert consensus on expected ASP progression, substitution risk between catalyst families, and planned capacity additions in key producing regions.

Data Validation & Update Cycle

Validation is done in steps, starting with consistency checks across regions so the implied volumes and prices do not move in unrealistic ways year to year. We compare outputs against independent signals like chemical output indices, trade direction changes, and major end-use capacity announcements, and then anomalies are reviewed before sign-off.

If a variance cannot be explained, assumptions are revisited and selected respondents are re-contacted to confirm what changed, such as pricing terms, grade shifts, or procurement timing. Reports are refreshed annually, with interim updates when material events occur, and before delivery an analyst completes a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Phase Transfer Catalyst Market Size Compared Against Other Published Estimates

Published market values for phase transfer catalysts can look far apart because scope and timing choices are not always the same, and small differences compound quickly in a chemistry inputs market. The year used as "current," the currency conversion date, and how average selling prices are carried forward are common reasons the totals do not match.

In this study, refresh cadence is tied to recent price and mix checks, and currency timing is kept consistent across regions so the implied ASP trend does not drift after large FX moves. This is the main reason the 2026 value shown by Mordor Intelligence does not line up with some 2024 snapshots that use a different price base.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.19 B (2026) | |

| Industry Distributor Brief A | USD 1.25 B (2024) | Uses an earlier year snapshot that can embed temporary pricing and mix effects, and it may include a wider set of reaction aids used in organic synthesis beyond commercial PTC products. |

| Trade News Note B | USD 1.23 B (2024) | Stops at a near-term endpoint and often applies a single blended growth rate, which can understate shifts between liquid, solid, and supported forms and the resulting ASP differences by end-use. |

Taken together, the spread is mostly explained by year alignment and what is counted as a phase transfer catalyst sale versus adjacent process chemicals. By keeping inputs tied to repeatable demand indicators and then rechecking price logic through interviews, we arrive at a balanced number that can be updated cleanly when conditions change.

Key Questions Answered in the Report

What is the current size of the Phase Transfer Catalysts market?

The market is valued at USD 1.19 billion in 2026.

What CAGR is forecast for the Phase Transfer Catalysts market through 2031?

The market is projected to expand at a 5.71% CAGR from 2026 to 2031.

Which end-user segment is growing fastest?

Batteries and Energy Storage leads with a 6.88% CAGR through 2031.

Which region holds the largest market share?

Asia Pacific commands 37.55% revenue share as of 2025.

Why are supported or immobilised PTC systems gaining popularity?

They simplify catalyst recovery, cut wastewater discharge, and are expected to grow at a 6.02% CAGR to 2031.

Page last updated on: