Catalyst Regeneration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 6.15 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

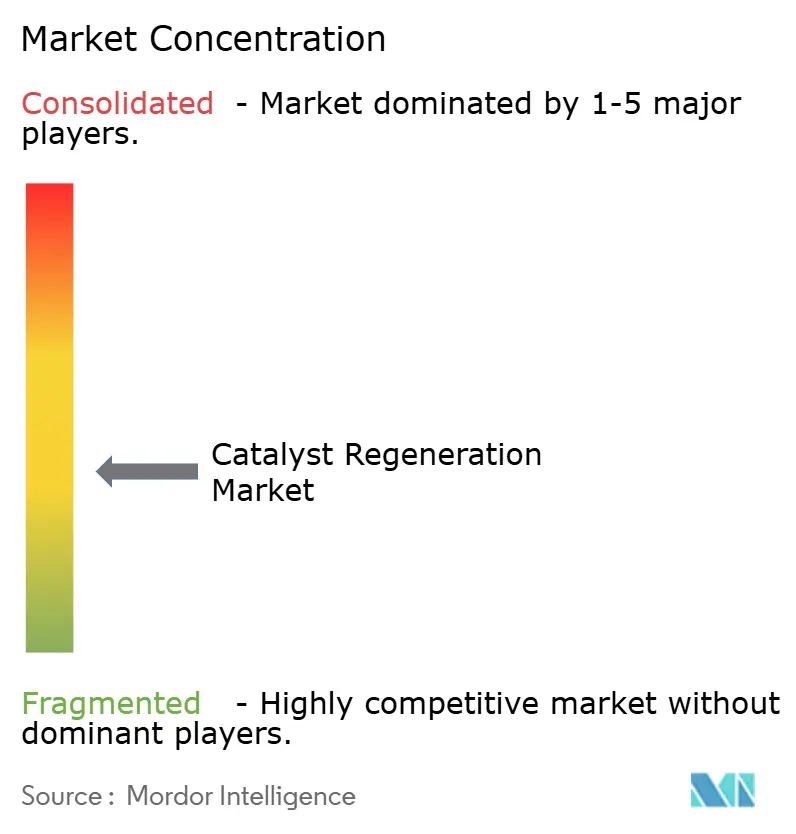

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catalyst Regeneration Market Analysis by Mordor Intelligence

The Catalyst Regeneration Market size was valued at USD 4.59 billion in 2025 and estimated to grow from USD 4.82 billion in 2026 to reach USD 6.15 billion by 2031, at a CAGR of 4.98% during the forecast period (2026-2031). This steady trajectory is underpinned by increasingly stringent emission norms, the escalating cost of fresh catalysts, and expanding circular-economy mandates that reward lower-carbon production routes. In practice, refineries and petrochemical complexes are sharpening focus on end-of-life catalyst handling, while emerging applications in plastics pyrolysis and volatile organic compound (VOC) abatement broaden the customer base. Technology advances such as low-temperature ozone oxidation and predictive analytics further reduce downtime and enhance cost efficiency, reinforcing the momentum of the catalyst regeneration market across both mature and developing economies.

Key Report Takeaways

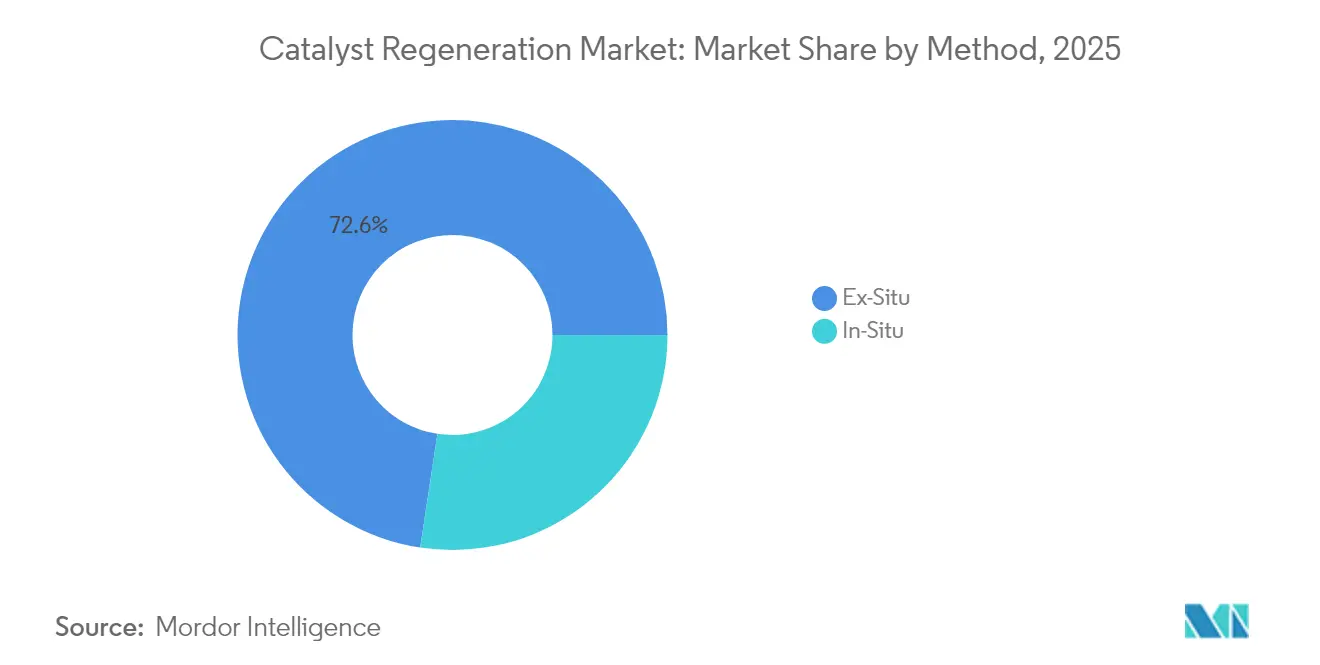

- By method, ex-situ processing held 72.60% of the catalyst regeneration market share in 2025, while in-situ systems are projected to grow at a 5.72% CAGR to 2031.

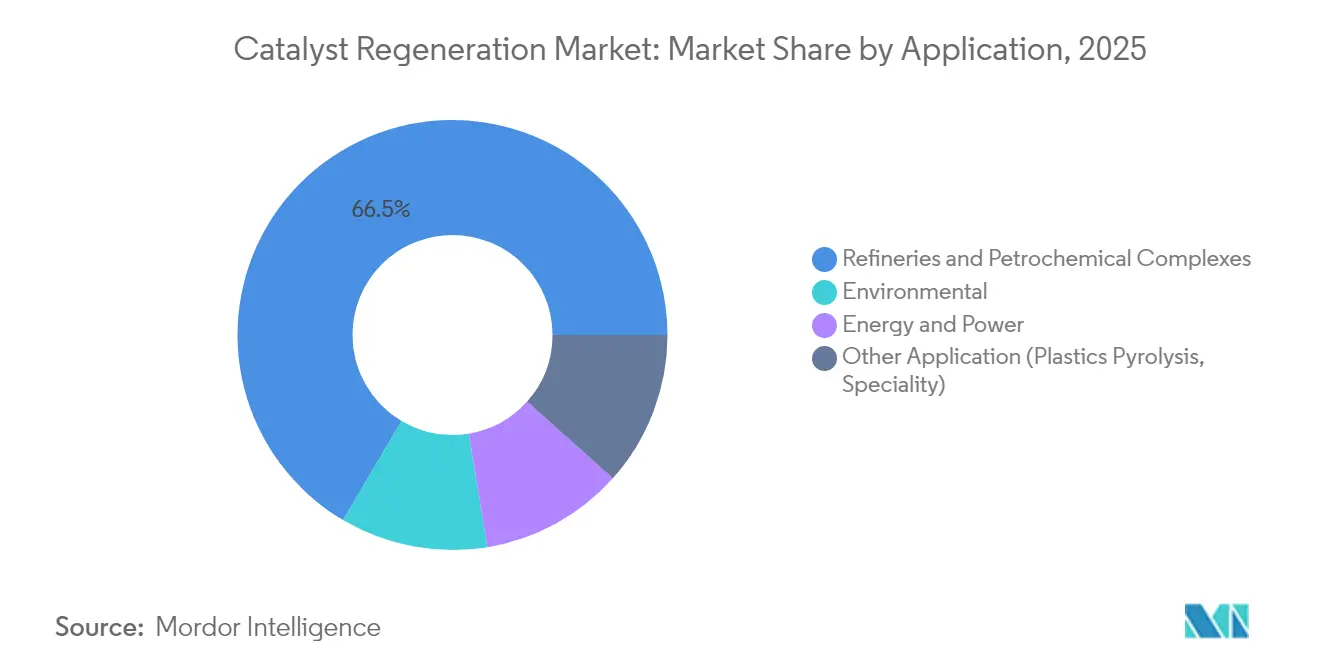

- By application, refineries and petrochemical complexes accounted for 66.50% share of the catalyst regeneration market size in 2025; other applications are set to register the fastest 5.89% CAGR through 2031.

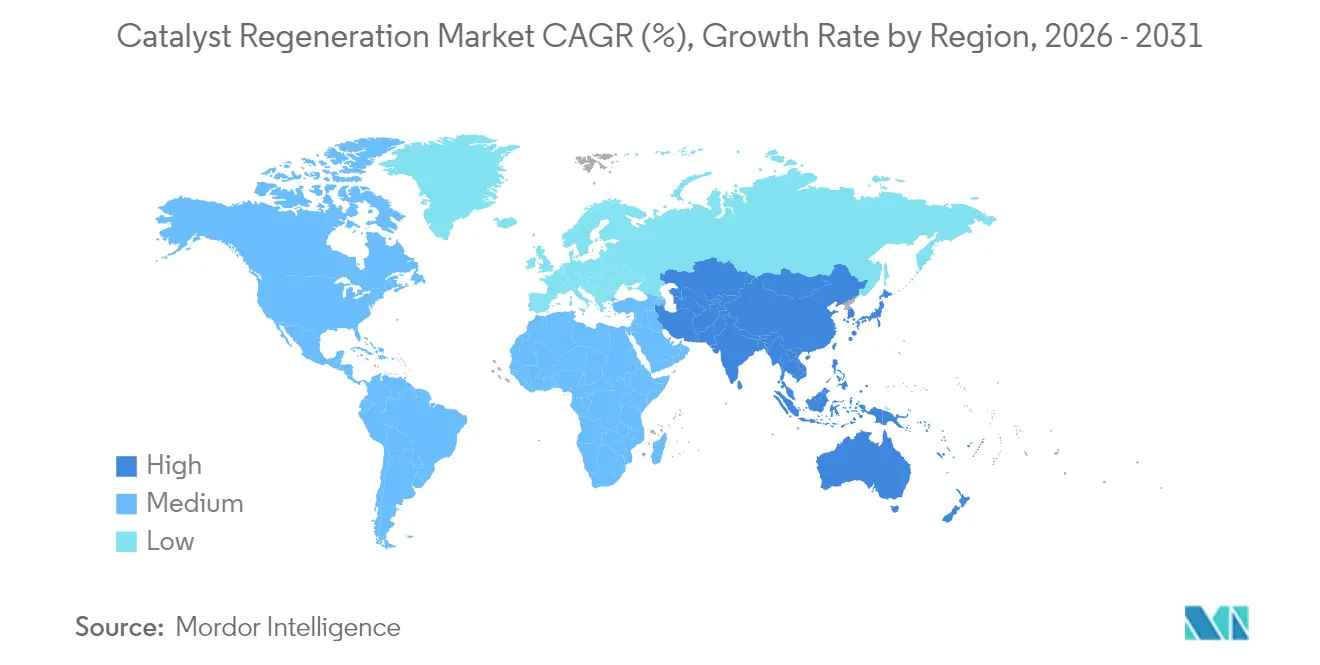

- By geography, Asia-Pacific led with 42.10% of the catalyst regeneration market share in 2025 and is forecast to expand at a 5.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Catalyst Regeneration Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict environmental regulations on refinery and petrochemical emissions | +1.8% | Global, early adoption in North America and the EU | Short term (≤ 2 years) |

| Rising cost pressure of fresh catalysts | +1.2% | Global, acute in APAC manufacturing hubs | Medium term (2-4 years) |

| Carbon-intensity mandates favouring regenerated catalysts | +0.9% | North America and the EU leading, expanding to APAC | Medium term (2-4 years) |

| On-site ozone-oxidation breakthroughs cut downtime | +0.7% | Global, faster adoption in developed markets | Long term (≥ 4 years) |

| Predictive analytics enabling condition-based regeneration | +0.5% | North America and EU early adopters, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Environmental Regulations on Refinery and Petrochemical Emissions

National and regional regulators are tightening allowable emission limits, changing the economics of catalyst reuse. The U.S. Environmental Protection Agency’s updated hazardous-air-pollutant standards will cut toxic releases by 2,200 short tons a year and deliver monetized health benefits exceeding USD 100 million annually[1]U.S. Environmental Protection Agency, “Final National Emission Standards for Hazardous Air Pollutants: Miscellaneous Organic Chemical Manufacturing,” epa.gov. California’s Low Carbon Fuel Standard requires a 30% reduction in fuel-cycle carbon intensity by 2030 and 90% by 2045, elevating demand for regenerated catalysts to comply with lifecycle accounting rules. The EU’s Industrial Emissions Directive embeds catalyst regeneration in Best Available Techniques for waste treatment, reinforcing a compliance-driven preference for regeneration over landfill. Across Asia, similar limits are being drafted, ensuring the driver’s influence spreads rapidly.

Rising Cost Pressure of Fresh Catalysts

Volatile prices for palladium, platinum, and rhodium have turned fresh catalyst procurement into a high-risk budget item. Academic assessments show that regenerating lightly fouled hydroprocessing catalysts recovers more than 80% of baseline activity at less than half the cost of a new supply. Metal-recovery facilities operated by Gulf Chemical and Metallurgical Corporation routinely convert 99% of spent catalyst into sellable molybdenum and nickel streams, illustrating the circular-value upside for refiners. In volume-heavy APAC hubs, the savings multiply, prompting facility managers to lock in multi-year regeneration contracts.

Carbon-Intensity Mandates Favouring Regenerated Catalysts

Lifecycle carbon accounting is becoming compulsory. The average global refining carbon intensity is 40.7 kg CO₂ eq per barrel, yet a regenerated hydroprocessing catalyst requires only a fraction of the embedded energy of a freshly manufactured equivalent, earning valuable compliance credits[2]International Energy Agency, “Global Refining CO₂ Intensity Tracker,” iea.org. Johnson Matthey’s selection to supply e-methanol technology at Europe’s largest planned facility underscores how regenerated catalysts underpin low-carbon fuels of the future. Crediting schemes from North America to Europe scale demand even in regions without firm carbon prices.

On-Site Ozone-Oxidation Breakthroughs Cut Downtime

Research proves that ozone treatment at 125 °C strips coke deposits that once demanded 500 °C regeneration cycles. Pilot installations show a 60% cut in energy use and a 30% reduction in turnaround time relative to traditional ex-situ burn-offs. Extended catalyst life, lower thermal stress, and minimal unit disruption appeal to process operators seeking incremental production uptime.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower recovery on metal-poisoned catalysts | -0.8% | Global, acute in heavy crude processing regions | Medium term (2-4 years) |

| Lack of global lab test method standards | -0.6% | Global, fragmented standards across regions | Long term (≥ 4 years) |

| Rise of single-use nano-catalysts in select processes | -0.4% | Developed markets with advanced manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lower Recovery on Metal-Poisoned Catalysts

Vanadium, nickel, and iron from heavy crudes bind irreversibly to active sites, curtailing regeneration yields. Laboratory work shows vanadium loads above 5 wt.% slash hydrodesulfurization activity by more than half because of pore blockage and phase changes. Although modified demetallization treatments strip up to 89.2% of nickel, they often damage framework stability, limiting reuse cycles. Operators running resid feeds therefore weigh the cost of partial recovery against fresh catalyst outlay, sometimes opting for disposal.

Lack of Global Lab Test-Method Standards

ASTM, IUPAC, and regional bodies have progressed toward unified protocols, yet disparities remain in coke quantification, surface-area measurement, and activity testing. Variability complicates cross-border tenders and challenges multi-site companies trying to benchmark regeneration quality. An industry-wide working group is now harmonising SCR and hydroprocessing test norms to reduce these transaction frictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: Ex-Situ Dominance Drives Market Leadership

Ex-situ facilities captured 72.60% of the catalyst regeneration market share in 2025 on the strength of robust thermal and chemical treatment trains capable of restoring 80-90% of fresh activity. Leading service providers remove hydrocarbons, carbon, and sulfur in staged kilns before metal extraction, delivering regenerated volumes back to the site in road-approved drums that slot seamlessly into refining units.

In-situ regeneration, applied directly inside process equipment, is gaining 5.72% CAGR momentum as ozone-oxidation technology matures. Continuous catalytic reformer operators appreciate that low-temperature oxidation curbs metallurgical stress on reactors, extending vessel life while slashing downtime. Early adopters report 10-day turnaround savings compared with sending material off-site and cutting the catalyst regeneration market cost per tonne by nearly 15%.

By Application: Refineries Lead While Specialty Segments Accelerate

Refineries and petrochemical plants consumed 66.50% of regeneration services in 2025, reflecting hydroprocessing, catalytic cracking, and reforming cycles that account for most spent volume. Environmental rules such as the EPA’s MACT standards reinforce the business case for routine regeneration rather than disposal.

Plastics pyrolysis, VOC abatement, and renewable-fuel synthesis comprise the fastest-growing “Other Applications” cohort, charting a 5.89% CAGR. Zeolite catalysts used to crack polyethylene waste retain conversion efficiency after 10-14 oxidative cycles, underpinning economic viability for circular-polymer projects. As chemical recyclers scale demonstration plants, demand for custom regeneration runs will broaden the catalyst regeneration market beyond its traditional hydrocarbon core.

Geography Analysis

Asia-Pacific carried 42.10% of global demand in 2025 thanks to high refining capacity, deep petrochemical integration, and progressive recycling regulations. Regional growth of 5.45% CAGR through 2031 keeps the catalyst regeneration market firmly centered on APAC. Japanese recyclers run integrated facilities that convert fouled catalyst, spent batteries, and electronic scrap into high-purity palladium and vanadium, ensuring secure domestic raw-material flows. In India, greenfield integrated refineries earmark capex for on-site regeneration trains to avoid cross-border waste shipments.

North America benefits from regulatory certainty and digital leadership. Refineries on the U.S. Gulf Coast stream operating-data feeds to cloud-based algorithms that recommend optimal burn times, while Canadian hydrocrackers receive recycled Co-Mo systems delivered under closed-loop contracts that guarantee metals buy-back pricing. Carbon-tax credits add a second revenue line, nudging mid-continental independent refiners to schedule regeneration just before compliance reconciliation dates.

Europe balances stringent environmental oversight with process-technology exports. French and German licensors bundle supply-and-regeneration packages, allowing clients in the Middle East to receive cradle-to-cradle service routed through European hubs. EU funding for green hydrogen and e-fuels further boosts regional demand as specialty reactors switch to tailored catalyst grades that require precise regeneration cycles to maintain selectivity.

Competitive Landscape

The catalyst regeneration market exhibits moderate fragmentation. The catalyst regeneration market exhibits moderate fragmentation. Honeywell’s USD 2.4 billion agreement to acquire Johnson Matthey’s Catalyst Technologies unit in May 2025 creates a vertical platform spanning catalyst synthesis, licensing, and regeneration. Independent specialists such as Eurecat maintain technological edge in hydroprocessing catalyst treatment, using proprietary caustic roasting to lift vanadium and molybdenum for resale. Start-ups in Europe and Asia race to commercialise similar chemistries, attracted by early mover sustainability premiums.

Catalyst Regeneration Industry Leaders

Eurecat

Albemarle Corporation

Axens

BASF

Johnson Matthey

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business for USD 2.4 billion, integrating regeneration, metals recovery, and process licensing into a single platform.

- April 2025: : Clariant launched the StyroMax UL-100 catalyst, achieving benchmark styrene yields at a steam-to-oil ratio of 0.76 wt, cutting energy demand for SM producers.

Global Catalyst Regeneration Market Report Scope

The catalyst regeneration process renews catalysts, making them reusable. Regenerated catalysts are used in several processes such as steam and naphtha reforming. Apart from these, these catalysts are also used in various processes including hydrogenation, alkylation, hydrocracking, hydro-desulfurization, and hydro-treatment, among others. The catalyst regeneration market is segmented by method, application, and geography, By the method, the market is segmented into Ex Situ and In Situ. By application, the market is segmented into Refineries and Petrochemical Complexes, Environmental, Energy & Power, and Other Applications. The report also covers the market sizes and forecasts for the Catalyst Regeneration market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Ex-Situ |

| In-Situ |

| Refineries and Petrochemical Complexes |

| Environmental |

| Energy and Power |

| Other Application (Plastics Pyrolysis, Speciality) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Method | Ex-Situ | |

| In-Situ | ||

| By Application | Refineries and Petrochemical Complexes | |

| Environmental | ||

| Energy and Power | ||

| Other Application (Plastics Pyrolysis, Speciality) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the catalyst regeneration market?

The catalyst regeneration market size is USD 4.82 billion in 2026 and is projected to reach USD 6.15 billion by 2031.

Which region dominates the catalyst regeneration market?

Asia-Pacific leads with 42.10% market share in 2025, supported by extensive refining capacity and advanced recycling systems.

Why is catalyst regeneration preferred over fresh catalyst replacement?

Regeneration cuts procurement costs by up to 50%, lowers embodied carbon, and helps refiners comply with tightening emission regulations.

What technological trends are shaping catalyst regeneration?

Low-temperature ozone oxidation, predictive analytics for condition-based maintenance, and on-site skid units are the key innovations improving efficiency.

Which application segment is growing the fastest?

Plastics pyrolysis and other specialty processes are expanding at a 5.89% CAGR as circular-economy projects scale globally.

Page last updated on: