Emission Control Catalysts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 53.82 Billion |

| Market Size (2031) | USD 68.62 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

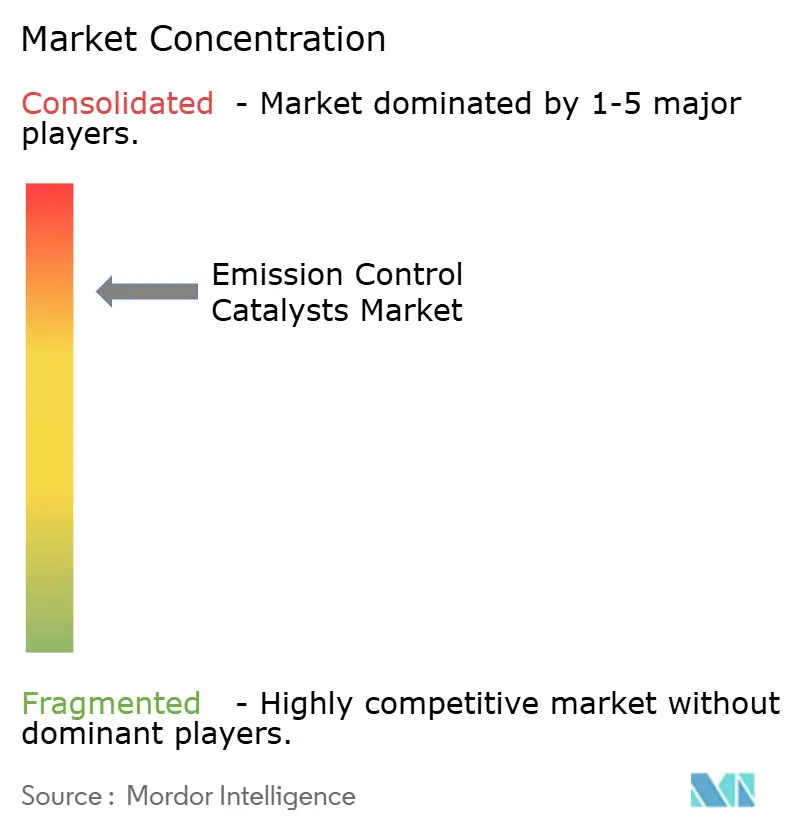

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emission Control Catalysts Market Analysis by Mordor Intelligence

The emission control catalysts market size was valued at USD 51.27 billion in 2025 and estimated to grow from USD 53.82 billion in 2026 to reach USD 68.62 billion by 2031, at a CAGR of 4.98% during the forecast period (2026-2031). Heightened global emission standards, resilient internal-combustion demand in emerging economies, and continuous catalyst innovation sustain this expansion. Regulatory bodies in the EU, the US, China, and India have tightened particulate and NOx limits, spurring near-universal adoption of advanced after-treatment technologies in new vehicles. Automakers are simultaneously refining catalyst formulations to lower precious-metal loadings, offset price volatility, and accelerate platinum substitution without compromising performance. Industrial and power-generation customers are also adopting similar technologies as air-quality rules broaden to cover stationary sources. The emission control catalysts market therefore benefits from a dual growth engine—persistent automotive volumes and widening industrial uptake—underpinning its robust outlook.

Key Report Takeaways

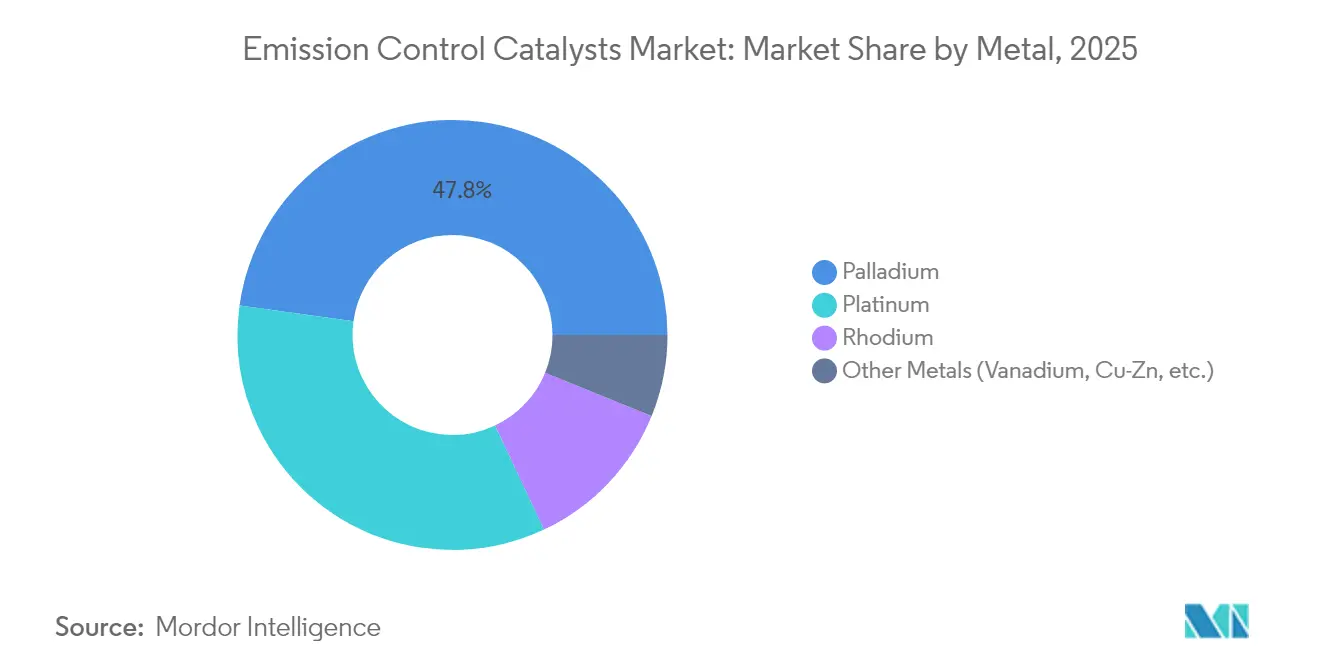

- By metal, palladium led with 47.80% of emission control catalysts market share in 2025; platinum is projected to post the fastest 6.41% CAGR to 2031.

- By technology, Three-Way Catalysts held 54.62% revenue share in 2025, while emerging nano-structured catalysts are forecast to expand at a 6.62% CAGR through 2031.

- By application, mobile emission control accounted for 81.48% of the emission control catalysts market size in 2025; stationary systems are expected to grow at 6.23% CAGR to 2031.

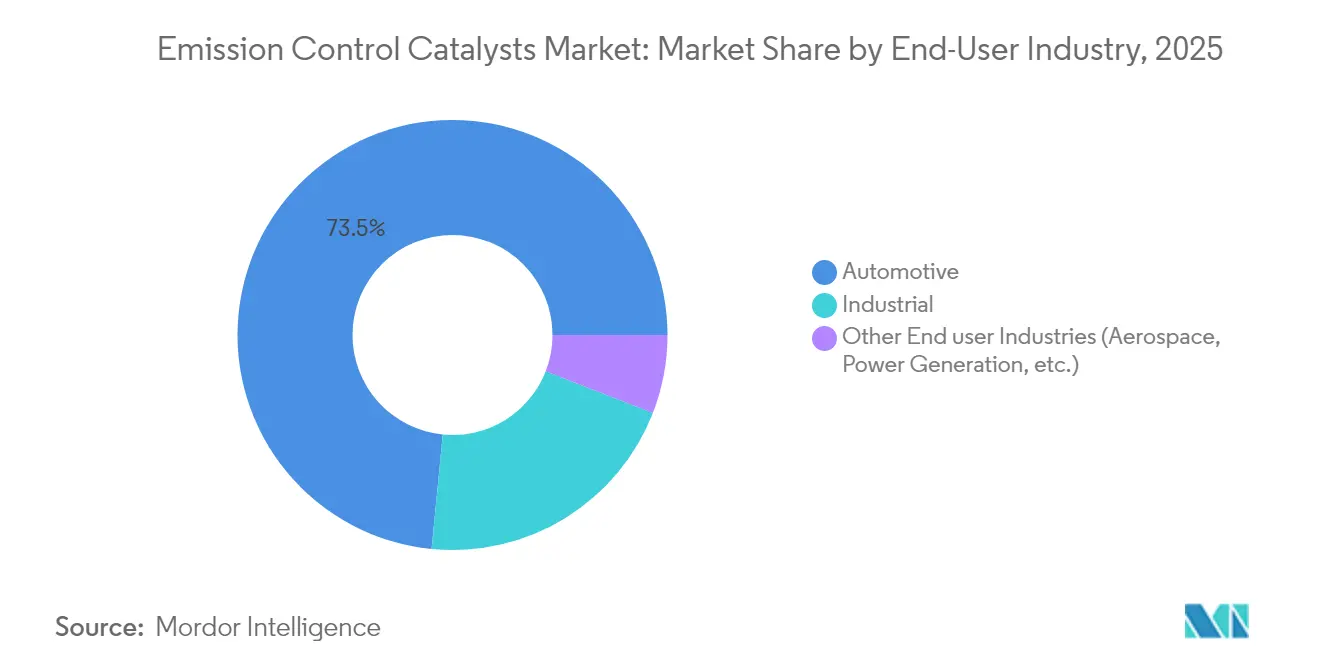

- By end-user industry, automotive and transportation represented 73.45% of demand in 2025; other niche industries—including aerospace—show the highest 6.49% CAGR outlook.

- By geography, Asia-Pacific captured 36.18% share of the emission control catalysts market in 2025 and is projected to register a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emission Control Catalysts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent tightening of on-road & off-road emission norms | +1.8% | Global, with early adoption in EU, North America, China | Medium term (2-4 years) |

| Rapid rebound of light-duty & heavy-duty vehicle production | +1.2% | Global, particularly APAC and emerging markets | Short term (≤ 2 years) |

| Growing concern for air quality and public health | +0.9% | Global, with emphasis on urban centers in China, India, EU | Long term (≥ 4 years) |

| Increasing adoption by industrial and power sector | +0.7% | North America, EU, China, with spillover to emerging markets | Medium term (2-4 years) |

| Expansion of the automotive sector | +0.6% | APAC core, Latin America, MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent tightening of on-road & off-road emission norms

Euro 7 rules lower permissible particulate levels and require real-world driving tests, compelling universal use of gasoline particulate filters and upgraded Three-Way Catalysts[1]European Council, “Council Agrees on Euro 7 Regulation,” consilium.europa.eu. Similar ambitions shape China VI and India BS VI regulations, which drive widespread SCR and GPF deployment across Asia’s vehicle fleets[2]International Council on Clean Transportation, “Global Progress Toward Soot-Free Transport,” theicct.org. Tier 4 off-road standards in North America extend comparable stringency to construction and agricultural machinery, broadening catalyst demand. Together, these frameworks ensure the emission control catalysts market maintains growth momentum, especially as developing economies replicate best-practice legislation.

Rapid rebound of light-duty & heavy-duty vehicle production

Global light-vehicle output climbed 8% in 2024, while commercial-vehicle production recovered strongly in infrastructure-focused economies, translating directly into higher catalyst unit shipments. The upturn coincides with new regulatory phases, forcing OEMs to install more sophisticated after-treatment even as production volumes rise. Electrification progress in heavy-duty fleets remains modest, meaning diesel SCR and DOC solutions will stay essential through 2030. This interplay between volume rebound and tightening standards supports a healthy order pipeline for catalyst suppliers.

Growing concern for air quality and public health

Megacities in China and India now cite PM2.5 exceedances as critical health risks, prompting municipal low-emission zones and accelerated enforcement of vehicle-inspection regimes. Government health-cost studies, valuing pollution impacts at USD 2.9 trillion annually, have strengthened political resolve to mandate best-available control technology across transport and industry. Catalysts capable of 99% pollutant conversion thus transition from compliance tools to public-health safeguards, embedding long-term demand for the emission control catalysts market.

Increasing adoption by industrial and power sector

Stationary systems post the fastest 6.54% CAGR as coal-fired plants retrofit SCR units and gas turbines add oxidation catalysts to satisfy stricter NOx and CO thresholds. Data-center backup generators require similar treatments to secure local permits. Industrial uptake already prevents an estimated 35 million t of CO₂-equivalent emissions annually, demonstrating measurable climate co-benefits that reinforce policy support. This diversification cushions the market against future automotive volume erosion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility & looming surplus of palladium depressing OEM purchasing | -0.8% | Global, particularly impacting automotive OEMs | Short term (≤ 2 years) |

| Accelerated BEV penetration eroding autocatalyst demand growth | -1.1% | EU, North America, China leading adoption | Medium term (2-4 years) |

| Catalyst poisoning from higher-sulfur alternative fuels in developing regions | -0.4% | Developing regions in APAC, Latin America, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price volatility & looming surplus of palladium depressing OEM purchasing

World Platinum Investment Council forecasts a swing from deficit to a surplus of nearly 900 koz of palladium by 2025 as recycling expands and mining supply stays firm. Automakers respond by intensifying platinum substitution and lowering overall PGM loadings through nano-engineered surfaces, trimming catalyst costs. Short-term volatility still complicates procurement, nudging OEMs toward long-term contracts and diversified sourcing strategies.

Accelerated BEV penetration eroding autocatalyst demand growth

Battery EV sales are on course to reach 30% of global light-vehicle demand by 2030, directly removing future exhaust-after-treatment volumes. Europe and China lead the shift, though hybrids and plug-in hybrids retain Three-Way Catalysts, partly offsetting unit losses. Commercial-vehicle electrification lags given payload and charging constraints, safeguarding SCR demand in long-haul trucking. Net impact stays moderate through 2027 but deepens thereafter as total cost of ownership parity expands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal: Palladium dominance amid supply transition

Palladium held 47.80% of the emission control catalysts market in 2025, underpinning its primacy in gasoline Three-Way Catalysts. Platinum followed at nearly 34.20% on the back of rising substitution, while rhodium’s unique NOx selectivity kept its 11.85% niche. The combined segment represented roughly USD 48.06 billion of emission control catalysts market size in 2025. Looking ahead, platinum’s 6.41% CAGR makes it the fastest riser as OEMs rebalance metal mixes to mitigate palladium surplus risk. Emerging applications such as liquid-gallium palladium alloys and nano-structured clusters promise equivalent conversion at far lower loadings, widening cost headroom.

Manufacturers increasingly deploy closed-loop recycling to reclaim PGMs, smoothing supply and lowering cash exposure. South African miners reevaluate capex, yet long-term catalyst research indicates continued palladium relevance in lean-burn and methanol engines. The emission control catalysts market therefore retains a multi-metal foundation even as relative shares shift through the decade.

By Technology: TWC leadership challenged by emerging innovations

Three-Way Catalysts controlled 54.62% revenue in 2025, reflecting their near-universal fitment on global gasoline vehicles. Diesel Oxidation Catalysts, Diesel/GPF filters, and SCR systems collectively equaled about one-third of revenues, their growth tied to heavy-duty and off-road sectors. Emerging nano-structured designs now grow at 6.62% CAGR, reaching critical commercial scale in petrochemical and low-temperature applications. Within this mix, emission control catalysts market share is expected to tilt progressively toward hybrid-optimized TWCs integrating gasoline particulate filters in response to Euro 7 and China VII legislation.

Additive manufacturing is another inflection point: BASF’s X3D printing enables complex channel geometries that raise surface area and cut back-pressure, improving efficiency by 1% in commercial trials. AI-driven copper-zeolite formulations enhance low-temperature SCR conversion, a crucial requirement for Euro 7 compliance in urban delivery trucks. Such advances safeguard the emission control catalysts market from commoditization, as performance differentiation continues to command pricing power.

By Application: Mobile primacy with stationary surge

Mobile sources represented 81.48% of 2025 demand, translating to over USD 41.77 billion in emission control catalysts market size. Passenger cars, commercial trucks, and off-highway machinery together exhaust the majority of global PGM output. The segment outlook remains positive through 2031 because hybrids and range-extender vehicles still require full after-treatment suites, even as pure-battery volumes grow. Stationary systems, although only 18.52% of current revenues, advance at 6.23% CAGR on the strength of industrial decarbonization mandates.

Coal plants in China and the US retrofit SCR units to meet 90% NOx reduction targets, while gas turbines add oxidation beds to curb CO and unburnt hydrocarbon slip aaqr.org. Marine engines adopt IMO-compliant solutions, further lifting stationary demand. The widening customer base diversifies risk and amplifies lifetime sales, given longer duty cycles and periodic replacement needs of industrial catalysts.

By End-user Industry: Automotive concentration with industrial diversification

Automotive and transportation consumed 73.45% of catalysts in 2025, a testament to the sector’s regulatory exposure and sheer production scale. The share equaled nearly USD 37.66 billion of emission control catalysts market size at year-end. Industrial customers—power generation, chemical processing, oil & gas—comprised roughly 20.65%, but will outpace automotive growth at 6.49% CAGR as nations impose plant-specific NOx and VOC caps. Aerospace, marine, and other niches round out the final 5.90%.

Hybrid proliferation, higher exhaust-gas temperatures from turbo-downsizing, and ultra-low-sulfur fuel availability collectively extend catalyst relevance in cars. In parallel, industrial users adopt high-temperature variants capable of 99% conversion in flue-gas streams of up to 600 °C, tapping expertise from top catalyst vendors. This industrial diversification buffers the market against an eventual automotive downturn, anchoring a stable forward revenue mix.

Geography Analysis

Asia-Pacific led the emission control catalysts market with 36.18% share in 2025, exceeding USD 18.55 billion in sales. The region’s 6.74% CAGR is propelled by robust vehicle production, rapid industrialization, and the implementation of China VI-B norms that demand low-temperature SCR and universal GPF usage. India’s BS VI regime similarly boosts catalyst loading per vehicle, while fuel-quality upgrades reduce sulfur-related poisoning. Japan and South Korea contribute research leadership, backing breakthrough nano-catalyst projects with academic-industry consortia. ASEAN nations, following UN-level equivalence, represent an incremental volume tailwind as their standards tighten toward Euro 6 parity.

North America and Europe together held 53.34% of 2025 revenues, their markets defined by advanced technology rather than raw unit growth. The US EPA’s 2027-plus light-vehicle rules target a 50% fleet-average GHG cut, compelling widespread hybridization and elevated PGM use in cold-start scenarios. Euro 7’s real-world testing extension to brake and tire wear triggers R&D for secondary filtration systems, broadening supplier portfolios. Both regions also lead industrial catalyst replacement cycles, with utilities retrofitting aged coal assets to curb NOx peaks and petrochemical outfits trialing additive-manufactured lattice catalysts. South America and the Middle East & Africa combined accounted for 10.48% of the emission control catalysts market in 2025 but present the highest catch-up potential. Brazil’s ethanol-diesel blends cut particulate output by 44%, yet still require oxidation catalysts to manage aldehyde slip. Gulf Cooperation Council states move to align fuel standards with Euro 5, prompting fresh demand for high-sulfur-resistant formulations. Diesel genset adoption across Sub-Saharan Africa adds incremental stationary catalyst volumes once local air-quality legislation matures. Overall, rising regulatory convergence guides steady long-term uptake across developing regions.

Value Chain Analysis

The value chain starts with upstream extraction and refining of platinum group metals (PGMs), along with sourcing ceramic or metallic substrates and washcoat chemicals, then moves through catalyst formulation, coating, canning, and validation to meet OEM and regulatory durability requirements. PGM availability and pricing are the most sensitive upstream dependencies, with supply concentration in regions such as South Africa increasing exposure to energy and labor disruptions. That volatility then feeds into catalyst pricing and contracting structures, especially where large catalyst programs are supplied under long-term OEM agreements with pass-through mechanisms for precious-metal costs.

Midstream manufacturers (for example, Johnson Matthey, BASF Environmental Catalyst and Metal Solutions, Umicore, Cataler Corporation, and regional suppliers such as Wuxi Weifu Lida) convert PGMs into technology-specific products (TWC, DOC, DPF/GPF, and SCR) and supply vehicle OEMs, engine OEMs, and industrial integrators. Downstream, distribution splits between OEM fitment and the automotive aftermarket, while stationary demand is handled through EPCs, turbine and engine packagers, and industrial service channels that rely on periodic catalyst replacement cycles. Bottlenecks typically arise from PGM supply concentration, trade policies and tariffs affecting substrates and metallic components, and qualification lead times for new formulations, which in turn encourage localization strategies and higher end-of-life catalyst recycling to stabilize supply and reduce cost exposure.

Competitive Landscape

The emission control catalysts market exhibits high concentration. R&D remains the prime differentiator. BASF’s X3D additive-manufacturing pilot in Ludwigshafen prints monolithic structures with 20% greater catalytic surface area at identical footprint, delivering measurable fuel-efficiency gains. Umicore invests in AI-guided material discovery to speed lab-to-line translation, cutting development cycles by 30%. Regional specialists, such as Tenneco’s Walker and India-based Sharda Motors, capture niche OEM programs through flexible local production and government policy alignment. Market entry barriers center on intellectual property, regulatory approval timelines, and precious-metal sourcing, limiting disruptive newcomer potential.

Strategic alliances focus on next-generation materials and digital twins for predictive catalyst aging models, crucial for extended warranty compliance. Suppliers increasingly bundle hardware with lifetime data-analytics services, creating recurring revenue beyond initial part sales. As industrial applications rise, multi-sector portfolios and tailored engineering support become decisive, favoring diversified players over single-segment firms.

Emission Control Catalysts Industry Leaders

Clariant

Umicore

Johnson Matthey

Haldor Topsoe A/S

BASF

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Stationary and industrial emission-control catalysts are where demand growth looks most actionable, since procurement is tied to plant permitting, retrofit cycles, and longer-duration service agreements rather than vehicle production volumes alone. Supplier investment is already pointing in this direction, including Johnson Matthey's agreement to acquire Cormetech (a US-based SCR catalyst manufacturer for stationary power generation), which signals ongoing focus on utility and industrial NOx control. Similar stationary-oriented moves show up in capacity additions and portfolio tailoring for sulfur and tail-gas treatment, including Axens completing an expansion at Axens Catalyst Arabia Limited in Saudi Arabia to manufacture tail gas treatment catalysts aimed at reducing SOx emissions and improving sulfur recovery.

In mobile emission control, opportunities center on compliance-driven upgrades such as low-temperature conversion, integrated particulate filtration, and catalyst architectures designed to reduce precious-metal loading volatility, along with supply-chain adjacency products that support after-treatment operation. In the United States, EPA activity in 2026 around Model Year 2027 and later heavy-duty highway engines, including proposed changes touching SCR system reliability and inducement provisions, keeps technical requirements in focus for catalyst and system suppliers. For the consumables layer, AdvanSix entered a process design and licensing agreement with Stamicarbon in May 2026 to assess expanding its ammonia platform in Hopewell, Virginia, to supply diesel exhaust fluid (DEF), which supports vertical integration around the urea-ammonia value chain and can help sustain SCR utilization across heavy-duty fleets and off-road equipment.

Recent Industry Developments

- July 2026: BM Catalysts launched 25 new part references covering 287 fitments for the European automotive aftermarket, including catalytic converters, DPFs, and GPFs. The broadened catalog increases coverage for late-model emissions systems and supports faster service replacement cycles as particulate filtration penetration rises.

- May 2026: Johnson Matthey announced an agreement to acquire Cormetech, a US-based manufacturer of selective catalytic reduction (SCR) catalysts for stationary power generation, for an enterprise value of USD 360 million. The deal expands scale in stationary emissions control and strengthens exposure to utility and industrial retrofit demand alongside longer service-driven replacement cycles.

- August 2024: BASF Catalysts India inaugurated a new Research, Development and Application laboratory in Chennai focused on automotive emissions control solutions for the Indian market. The facility supports localized formulation and validation work aligned with tightening regional standards and fuel-mix realities, shortening development-to-customer timelines.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers catalysts used in exhaust and flue-gas systems to cut harmful emissions, mainly by converting CO, hydrocarbons, and NOx into less harmful compounds. It includes catalysts used in mobile sources (on-road and off-road) and in stationary sources such as industrial plants and power generation units.

Scope exclusions: The sizing excludes non-catalyst emission-control hardware and services, and it does not count broader air-pollution equipment that does not rely on catalytic reactions.

Segmentation Overview

- By Metal

- Platinum

- Palladium

- Rhodium

- Other Metals (Vanadium, Cu-Zn, etc.)

- By Technology

- Three-Way Catalysts (TWC)

- Diesel Oxidation Catalysts (DOC)

- Diesel/GPF Particulate Filters (DPF/GPF)

- Selective Catalytic Reduction (SCR)

- Lean NOx Traps & NSC

- Emerging Nano-Structured Catalysts

- By Application

- Mobile Emission Control

- Stationary Emission Control

- By End-user Industry

- Automotive

- Industrial

- Other End user Industries (Aerospace, Power Generation, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

We start by building a fact base from emissions rules, vehicle and industrial activity, and precious metal trends, since these inputs shape catalyst demand and pricing. Public sources such as the US EPA, the European Commission publications on Euro standards, the International Energy Agency, and the International Organization of Motor Vehicle Manufacturers are used to anchor regulation timelines and production context.

We then add details from company filings and investor presentations, association pages, and reputable press coverage to track technology shifts like SCR adoption, gasoline particulate filter usage, and PGM thrifting direction. For hard-to-find cross-border signals, an import-export shipment-level database is selectively used to sense trade flows for catalyst-related materials and assemblies, and a patent database is used to track new formulations and coating approaches. These examples are not exhaustive, and many other public documents and datasets were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

To stress-test assumptions, we spoke with a mix of catalyst supply chain participants and downstream users, including manufacturing, compliance, procurement, and product teams. Since demand is global, inputs were validated across APAC, EMEA, and the Americas so our unit assumptions, pricing direction, and adoption timing reflect conditions in major producing and consuming regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 39% |

| Mid tier: 61% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 14% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where emissions-regulation coverage and activity indicators are used to reconstruct the demand pool, and then it is translated into catalyst value using typical loadings and price bands. In practice, vehicle production by powertrain type, penetration of after-treatment technologies (such as TWC, DOC, SCR, and particulate filters), replacement rates in mature fleets, and industrial NOx control adoption are treated as core inputs, because they explain most of the volume movement.

We then corroborate totals with selective bottom-up checks, where sampled ASP x volume logic is applied for major application buckets and adjusted based on channel feedback. Where direct data is thin, gaps are handled by using proxy series such as regional vehicle output mix, the installed base of regulated stationary units, and observed PGM price movements, followed by analyst review to ensure no single proxy dominates the outcome. For forecasting, scenario analysis is used around emissions-rule tightening, vehicle mix shifts, and PGM price direction, and the final trajectory is aligned to the most consistent consensus signals heard in expert calls.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as changes in vehicle production mix, public policy timelines, and directional PGM pricing, and then variances are investigated before sign-off. When the model shows a sharp step-change that does not match these external signals, we revisit adoption rates, pricing logic, and regional weights, and we follow up with selected respondents to confirm what changed.

Each report is refreshed annually, and interim adjustments are made when material events occur, such as major emissions-rule updates or sudden shifts in PGM pricing. Before delivery, an analyst runs a fresh review pass so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Emission Control Catalysts Market Size Compared Against Other Published Estimates

Published values for emission control catalysts often do not match because teams may not agree on what to include, which year to anchor, and how to treat pricing for precious-metal-heavy products. Differences also come from how mobile versus stationary demand is weighted, and whether replacement demand is modeled as a steady stream or a faster cycle.

The benchmark table shows a tight 2026 value versus some sources that anchor on 2024 or 2025, and in Mordor Intelligence's model the market is counted only for catalyst products used in emission-control systems across mobile and stationary sources, rather than bundling wider exhaust hardware or non-catalyst abatement solutions. Gaps also show up when other estimates apply a more aggressive ASP progression tied to spot PGM swings, or when emissions-rule timing is assumed to move faster than OEM and industrial compliance plans indicate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.82 B (2026) | |

| Industry Publisher A | USD 55.13 B (2025) | Uses a different base year and a steeper growth profile, and the pricing path can be more sensitive to near-term PGM movements, which lifts the value when metal prices are elevated. |

| Research Desk B | USD 51.95 B (2024) | Anchors the model earlier and can apply broader end-use allocation assumptions for industrial demand, which shifts totals when stationary adoption and replacement cycles are not validated region by region. |

Overall, the spread is explained mostly by base-year selection, what is counted as a catalyst-only market versus adjacent exhaust items, and how fast pricing is allowed to move with metals. By tying the value to regulation coverage, technology penetration, and repeatable unit checks, the estimate stays traceable to clear variables that can be revisited each update cycle.

Key Questions Answered in the Report

What is the current Emission Control Catalysts Market size?

The market is valued at USD 53.82 billion in 2026 and is forecast to reach USD 68.62 billion by 2031.

Which metal dominates catalyst formulations today?

Palladium leads with 47.80% share because of its high efficiency in gasoline Three-Way Catalysts.

What segment is expanding fastest outside automotive uses?

Stationary industrial and power-sector applications show a 6.23% CAGR as plants retrofit SCR and oxidation catalysts to meet tightening NOx and CO regulations.

How is electrification affecting the emission control catalysts market?

Battery EV penetration reduces long-term exhaust-after-treatment volumes, yet hybrids, commercial vehicles, and industrial sources will sustain meaningful demand through at least 2031.

Page last updated on: