South Korea Access Control Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

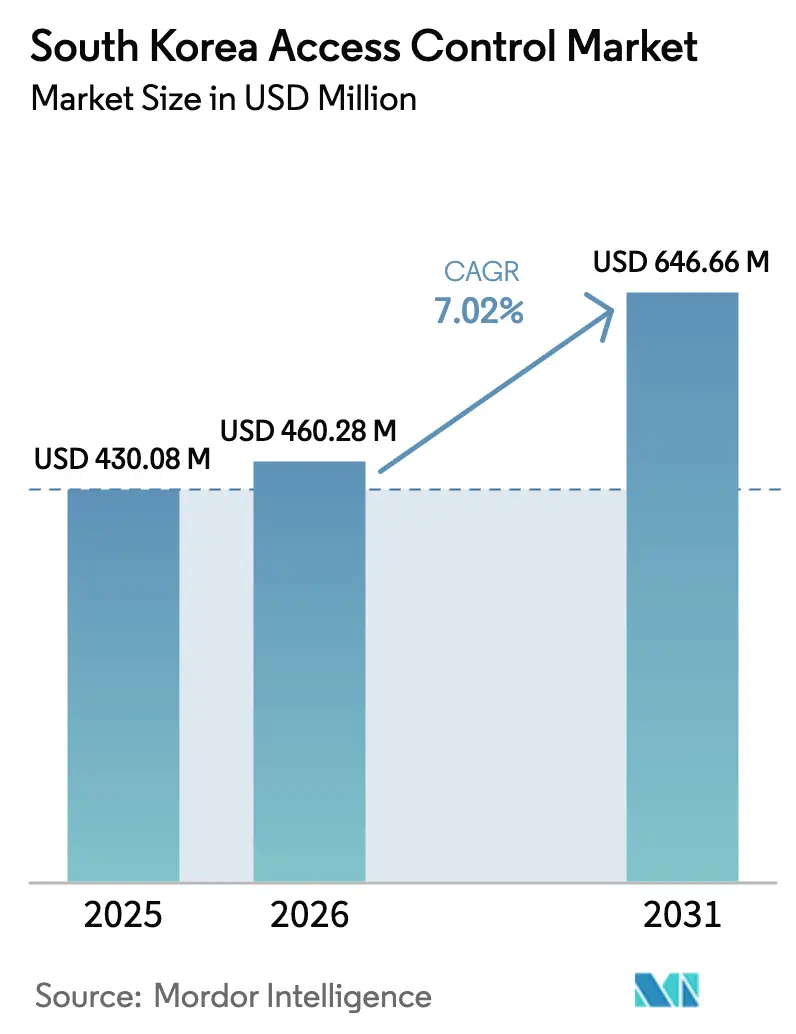

| Base Year Market Size (2025) | USD 430.08 Million |

| Market Size (2026) | USD 460.28 Million |

| Market Size (2031) | USD 646.66 Million |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

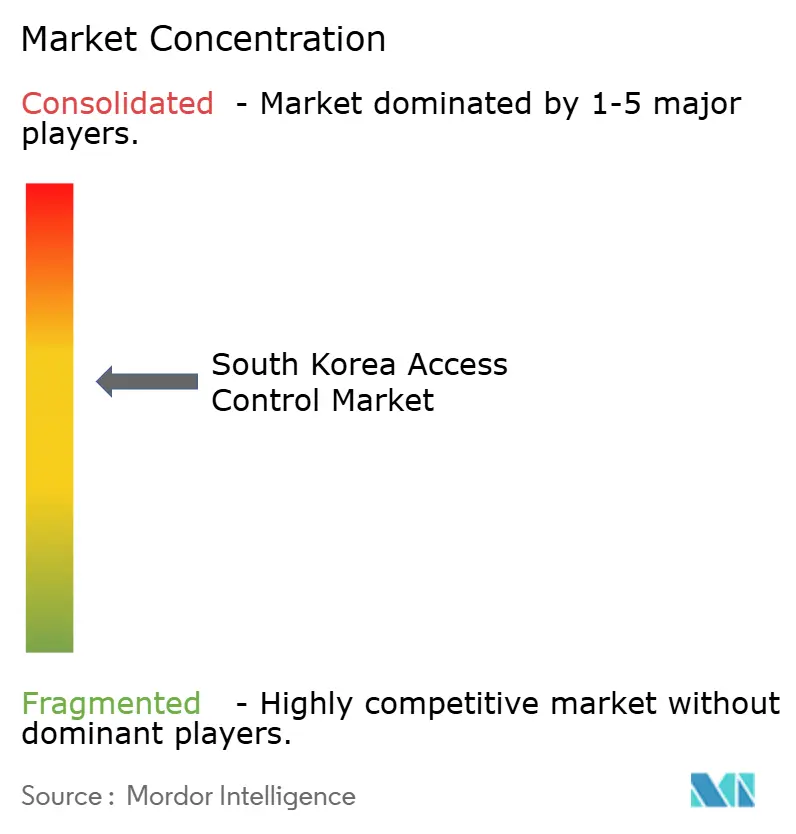

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Access Control Market Analysis by Mordor Intelligence

The South Korea access control market size was valued at USD 430.08 million in 2025 and estimated to grow from USD 460.28 million in 2026 to reach USD 646.66 million by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). Rapid digitization of national identity, stringent building‐security mandates, and smart-city investments collectively underpin demand momentum.[1]NFCW: NFCW, “Korean Government Completes Rollout of Digital ID Cards,” nfcw.comThe Zero-Energy & High-Security Building Code, effective since December 2023, has hard-wired electronic logs into new construction requirements.[2]Korea Legislation Research Institute: Enforcement Decree of the Green Buildings Construction Support Act, elaw.klri.re.kr Parallel execution of digital ID cards gives 52 million citizens friction-free mobile credentials that integrate directly into workplace, healthcare, and public-service checkpoints. Smart-city mega-projects such as Songdo and Busan Eco Delta City embed access control nodes inside broader IoT layers, elevating the strategic relevance of interoperable, cyber-hardened platforms. [3]Charter Cities Institute : Joey Jung, “Songdo City: Blueprint or Black Sheep?,” chartercitiesinstitute.org At the same time, chaebol conglomerates are upgrading to cloud-based Access Control as a Service to manage hybrid work and geographically distributed campuses.

Key Report Takeaways

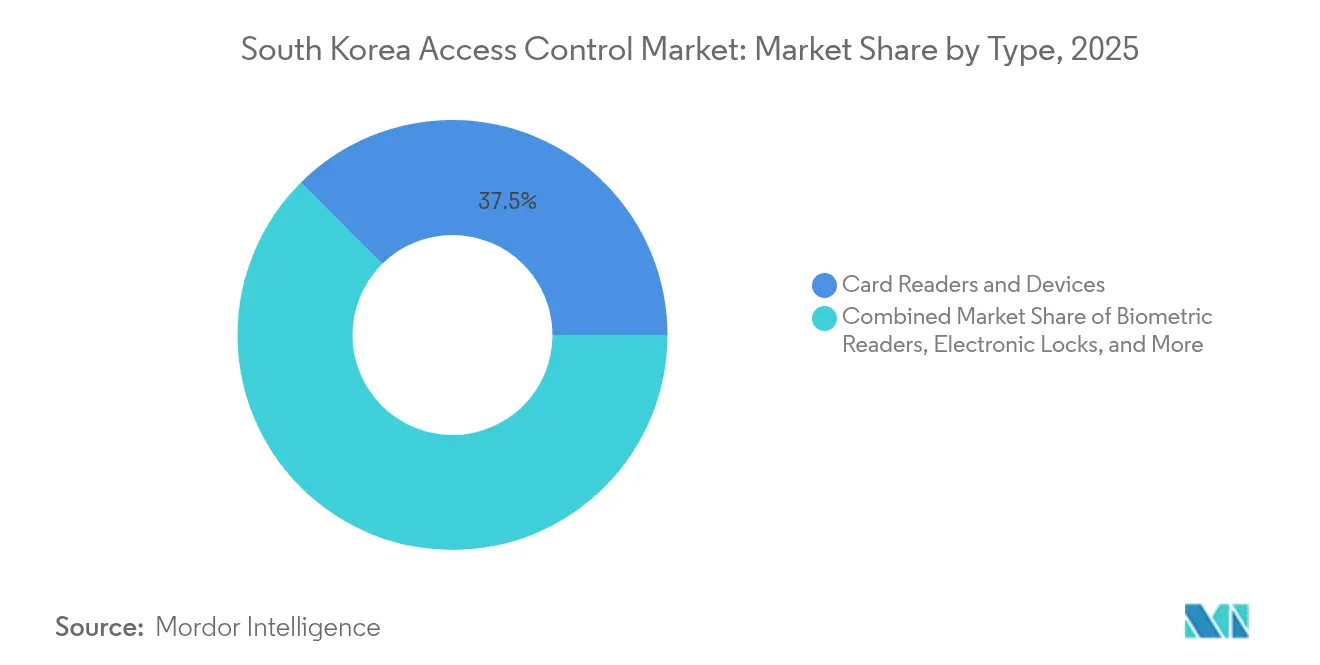

- By product type, Card Readers & Devices led with 37.45% revenue share in 2025, while Biometric Readers are projected to expand at an 8.22% CAGR through 2031.

- By end-user vertical, Commercial settings held 41.30% of the South Korea access control market share in 2025; Healthcare facilities are forecast to grow fastest at a 9.4% CAGR to 2031.

- By architecture, on-premise deployments retained 63.20% of the 2025 base, whereas cloud-based ACaaS solutions are tracking a 8.61% CAGR over 2026-2031.

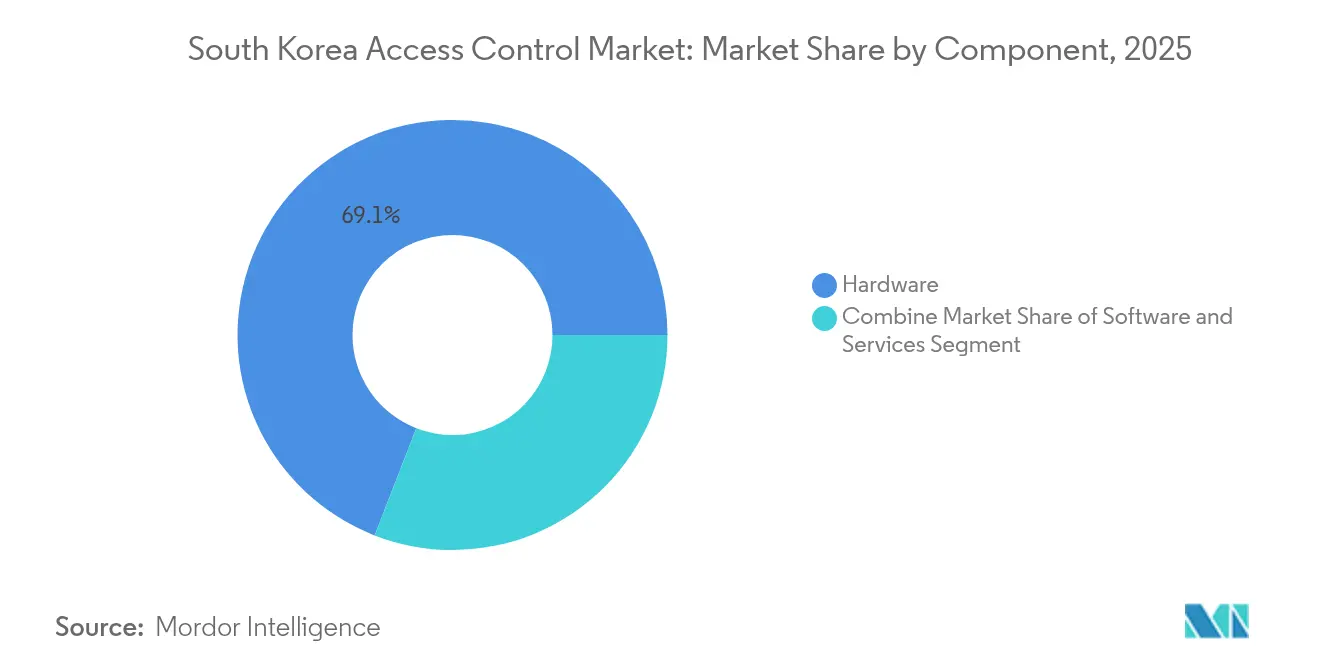

- By component, Hardware captured 69.10% of 2025 revenues; Services represent the quickest climber with an 10.35% CAGR over the outlook period.

- By authentication mode, Single-factor methods accounted for 59.25% of the South Korea access control market size in 2025, yet Multi-factor solutions are accelerating at a 9.74% CAGR.

- Suprema, ASSA ABLOY and Johnson Controls collectively command the largest combined footprint, with Suprema ranked within the global top five access control vendors in 2025

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Access Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city mega-projects | +2.10% | Incheon, Busan | Long term (≥ 4 years) |

| Zero-Energy & High-Security Building Code | +1.80% | Nationwide; early uptake in Seoul, Busan, Incheon | Medium term (2-4 years) |

| ACaaS uptake across chaebol campuses | +1.50% | Seoul metro | Medium term (2-4 years) |

| National Mobile-ID (PASS) rollout | +1.30% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-city mega-projects driving integrated physical-logical security

Songdo and Busan Eco Delta City exemplify how integrated urban planning is scaling the South Korea access control market. Songdo’s USD 40 billion conversion from tidal flats to connected metropolis and the government’s USD 77 billion future investment target signal long-run, infrastructure-backed demand. These cities deploy sensor-laden gateways, AI video analytics and interoperable card-to-biometric devices that feed real-time situational dashboards. KISA steers interoperability certification so that physical edges align with national cyber frameworks, allowing city planners to unify surveillance, traffic and building access on one governance stack.

Zero-Energy & High-Security Building Code mandating electronic logs

Effective December 2023, every new build or significant retrofit must log entry events electronically, pushing developers toward networked readers and audit-ready software. Suppliers differentiate by embedding low-power chipsets and data encryption at the edge, supporting compliance without breaching aggressive net-zero energy targets. Facility operators now treat access control as both a sustainability lever and a compliance cost hedge, accelerating platform refresh cycles across offices, hotels and residential towers.

Surge in ACaaS adoption by chaebol campuses to support hybrid work

Chaebol facilities have high badge volumes and fluid occupancy. Cloud-native platforms reduce server sprawl, shift capital outlays to subscription opex, and deliver rapid policy changes across nationwide estates. Device-to-cloud APIs enable real-time monitoring of thousands of doors from a single console, while mobile credentials replace plastic cards. Vendors leverage this migration to cross‐sell analytics packs, threat-intel feeds, and automatic firmware patches, positioning ACaaS as a continuous-improvement tool rather than a static asset.

National Mobile-ID (PASS) rollout accelerating multi-factor authentication

PASS binds decentralized IDs to smartphone secure elements, issuing QR tokens that harmonize with facility entrance kiosks. Over 10 million active IDs create a mass-market ecosystem that de-risks mobile credential pilots for enterprises. K-FIDO further layers cryptographic PKI onto FIDO biometrics, enabling password-less yet regulation-ready authenticationg. As a result, multi-factor suites that fuse mobile ID, face recognition and PIN checkpoints are migrating from bank branches into hospitals, data centers and co-working spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter PIPA biometric clauses | -0.80% | Nationwide | Medium term (2-4 years) |

| Interoperability gaps (domestic vs OSDP/Wiegand) | -0.60% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter PIPA biometric clauses raising compliance costs

September 2023 amendments to the Personal Information Protection Act mandate explicit opt-in, encrypted storage and recurring privacy impact reviews for biometric. Penalties are material, as PIPC probes have imposed sizeable fines for mis-configuration. SMEs defer biometric rollouts whereas larger enterprises ring-fence budgets for compliant tokenization, driving a consulting services upswing but trimming near-term device shipments.

Interoperability gaps between domestic protocols and global standards

Local vendors often enhance proprietary protocols for speed and custom encryption, yet these choices complicate integration with multinational tenants that standardize on OSDP-secure channels. PSIA’s ratified PKOC-over-OSDP standard offers a bridge, but adoption lags in local manufacturing pipelines. The resulting patchwork elevates engineering costs and slows multi-site rollouts, reinforcing buyer appetite for middleware or cloud translation layers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biometrics redefine authentication paradigms

Card Readers & Devices controlled 37.45% of the South Korea access control market in 2025. Biometric Readers, propelled by AI vision and on-device neural processing, are forecast at an 8.22% CAGR, eclipsing growth in legacy cards. Suprema’s Template-on-Mobile model stores encrypted face vectors on user phones, easing PIPA compliance. Meanwhile, hybrid card-plus-mobile devices protect sunk investments while giving property managers a pathway to contactless upgrades.

Contactless trends reshape risk postures. Facial recognition throughput suits transit hubs and hospitals, while capacitive fingerprint remains preferred for industrial sites with gloves. Software & Analytics platforms mine door events for anomalous patterns and SLA reporting, embedding business intelligence into what was once a cost center.

By End-user Vertical: Healthcare sector embraces advanced security

Commercial complexes such as BFSI branches, retail chains and data centers delivered 41.30% of South Korea access control market revenue in 2025. Hospitals are scaling at a 9.4% CAGR as cyber-physical breaches threaten patient confidentiality and controlled-substance inventories. Yongin Severance Hospital’s PASS-based workflow illustrates how mobile ID cuts queue times while bolstering compliance.

Data centers represent a high-growth Commercial micro-segment. Microsoft’s build program, generating 858 peak construction jobs, requires concentric circles of biometric, card and mantrap barriers. Such facilities favor multi-factor suites with automatic high-availability failover. The South Korea access control market share linked to Healthcare and data centers will expand as digital-transformation budgets prioritize uptime and personal-data stewardship.

By Access-Control Architecture: Cloud migration reshapes deployment models

On-premise controllers governed 63.20% of deployments in 2025. Yet cloud ACaaS subscriptions are compounding at 8.61%, a trend that positions platform vendors as managed-service allies rather than box shippers. Hybrid topologies dominate transition roadmaps: peripheral doors route to local panels for fail-safe continuity, while policy sets reside in regional data centers. Chaebol IT teams cite rapid badge revocation and API hooks into HR suites as pivotal benefits, underscoring the evolving role of identity orchestration inside corporate resilience strategies.

The transition to cloud-based architectures is particularly pronounced among chaebol conglomerates implementing hybrid work models, as these organizations require flexible security solutions that can accommodate dynamic workforce distributions.

By Component: Services growth outpaces hardware dominance

Hardware preserved a 69.10% share in 2025. Still, Services—spanning design, installation, and ongoing compliance audits—clock an 10.35% CAGR as buyers outsource complexity. AI-enabled edge readers such as Anviz’s SAC921 and C2KA-OSDP keypad fuse local intelligence with protocol openness. The South Korea access control market is mirroring the skills gap in non-metro regions and rising PIPA risk assessments.

The emergence of AI-powered solutions is transforming the component landscape, with intelligent edge devices capable of performing advanced authentication and decision-making functions without constant connectivity to central servers.

By Authentication Mode: Multi-factor solutions address evolving threats

Single-factor authentication still underpins 59.25% of installed endpoints, but 9.74% CAGR in multi-factor uptake highlights risk recalibration. PASS and K-FIDO convert citizen smartphones into federated ID tokens tied to biometric capture. Anviz’s OSDP reader layers RFID with PIN and optional face scan, epitomizing modular defense-in-depth. Policy engines increasingly weigh location, daypart, and user risk to grant adaptive access, aligning with zero-trust doctrines.

The shift toward multi-factor authentication is particularly pronounced in high-security environments such as financial institutions, government facilities, and data centers, where the consequences of unauthorized access are most severe. Anviz's C2KA-OSDP reader, which supports multi-factor authentication combining RFID credentials with PIN codes, illustrates the industry's response to these requirements.

Geography Analysis

The Seoul metropolitan area accounts for the largest slice of the South Korea access control market, owing to dense headquarters clusters and multi-tower residential estates. The city’s metaverse pilot under the national Smart City plan requires secure avatar-to-building credential bridges. Incheon’s Songdo leverages marine-climate sensors to calibrate reader environmental tolerances, demonstrating region-specific product tweaks.

Busan hosts the Eco Delta Smart City, an 11.77 km² showcase blending waterfront commerce and AI-managed public services. Its target of 97,000 residents configures a living lab for cloud-native ACaaS across residential, retail, and leisure zones. The South Korea access control market benefits from provincial subsidies that reward vendors co-locating assembly lines in Busan’s high-tech corridor.

Rural districts trail due to installer shortages and bandwidth limitations. Managed service providers now bundle LTE fallback units with cloud doors to serve logistics depots and renewable-energy sites. Government rail expansions, such as Eco Delta City Station, due in 2029, will progressively close the urban-rural security gap

Competitive Landscape

Domestic incumbent Suprema anchors innovation through AI facial models and cloud connectors, earning a spot in the global top 50 security leaderboard for 14 consecutive years. Global conglomerates ASSA ABLOY and Johnson Controls complement portfolios with open-protocol controllers, while Honeywell focuses on OT-IT convergence for industrial clients.

Strategic alliances intensify: hardware OEMs white-label cloud dashboards from SaaS specialists, and integrators consolidate card issuance, surveillance, and visitor management under outcome-based contracts. ProMart’s EasyMart unmanned retail blueprint showcases how RFID entry can converge with inventory management to unlock new revenue pools turck.us. PSIA’s PKOC standard introduction incentivizes ecosystem partners to abandon proprietary lock-ins, anticipating a mid-term reshuffling of end-to-end runnings.

South Korea Access Control Industry Leaders

Thales Group

Bosch Security System Inc.

Honeywell International Inc

Tyco International PLC (Johnson Controls)

Allegion PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Government completes nationwide digital ID card rollout, enabling 52 million citizens to adopt mobile credentials.

- March 2025: 260 MW hyperscale data center proposal signals sustained demand for high-security, multi-factor entry layer.

- February 2025: HID Global previews Amico facial readers to tap growth in contactless corporate lobbies.

- January 2025: Suprema secures global top-50 ranking for 14th straight year, underscoring brand equity in biometrics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea access control market as all revenue earned from physical credentials, readers, electronic locks, controllers, management software, and associated installation or monitoring services that permit or deny entry to buildings, parking lots, elevators, and critical zones after verifying a person or vehicle through card, biometric, mobile, or keypad credentials.

Scope exclusion: Network-only identity or privileged-access software that never actuates a physical barrier is outside this scope.

Segmentation Overview

- By Type

- Card Readers and Devices

- Card-based Readers

- Proximity Readers

- Smart-card (Contact / Contactless) Readers

- Mobile-credential (NFC / BLE) Readers

- Biometric Readers

- Fingerprint

- Face Recognition

- Iris Scan

- Vein / Palm

- Electronic Locks

- Electromagnetic

- Electric-strike

- Smart Locks

- Controllers and Panels

- Software and Analytics

- Services

- Card Readers and Devices

- By Authentication Mode

- Single-Factor

- Multi-Factor

- By Component

- Hardware

- Software

- Services (Installation, Maintenance, Consulting)

- By Application Area

- Building Entry/Exit

- Parking and Vehicle Access

- Elevator Control

- Critical Infrastructure Zones

- Turnstiles and Visitor Management

- By End-user Vertical

- Commercial (BFSI, Offices, Retail, Data centres, Hotels)

- Residential

- Government and Public Facilities

- Industrial and Manufacturing

- Transport and Logistics

- Healthcare

- Military and Defence

- Education

Detailed Research Methodology and Data Validation

Primary Research

We spoke with facility managers, system integrators, hardware suppliers, and cloud ACaaS providers across Seoul, Busan, and Gyeonggi. Their insights confirmed penetration ratios, service mark-ups, and the price premium now commanded by multi-factor kits, letting us close data gaps that secondary sources could not address.

Desk Research

We began by pairing Korea Customs Service import codes for card readers and biometric panels with MOLIT building-completion statistics, which signal fresh hardware demand. We then traced export flows through Volza to capture domestic manufacturing footprints. Next, Bank of Korea capital-goods accounts and Korea Smart City Association project trackers offered macro filters, while IEEE journal articles on facial-recognition uptake and IITP security surveys clarified technology mix shifts. Paid pulls from D&B Hoovers supplied vendor revenue splits that grounded average selling prices. These sources are illustrative; many additional public datasets, filings, and news archives were reviewed to verify and enrich every figure.

Market-Sizing & Forecasting

A top-down build started with 2024 commercial floor area and new dwelling units, was converted to potential access points, and multiplied by installation ratios drawn from interviews. We then cross-checked totals through a partial bottom-up roll-up of the fifteen largest vendors identified in customs data. Key drivers in our model include biometric share of new readers, smart-city capital spending, NFC-enabled smartphone penetration, building starts, and typical three-year replacement intervals. Forecasts to 2030 use multivariate regression blended with ARIMA smoothing, and results are stress-tested through expert scenario reviews before finalization.

Data Validation & Update Cycle

Outputs pass variance checks against crime statistics and insurance loss data, with anomalies escalated to senior analysts for peer review. Mordor Intelligence refreshes each file annually and issues interim updates whenever material events, such as a change to PIPA biometric clauses, significantly alter demand.

Why Mordor's South Korea Access Control Baseline Is Dependable

Estimates across publishers diverge because scopes, variables, and update cadences differ. We standardize each element before modeling.

Key gap drivers include whether residential DIY locks are counted, how cloud subscription revenue is annualized, currency conversion dates, and the share of bundled perimeter hardware folded into totals, all calibrated within Mordor's baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 430.08 M (2025) | Mordor Intelligence | |

| USD 472.65 M (2024) | Global Consultancy A | Includes logical identity software and video surveillance revenue |

| USD 171.7 M (2024) | Industry Journal B | Uses replacement-value only, excludes services and SaaS fees |

| USD 320.05 M (2024) | Regional Analyst C | Applies uniform ASPs, omits mobile-credential upgrades |

The comparison shows that by aligning scope with real hardware plus service cash flows, sampling current price ladders, and updating every year, Mordor Intelligence delivers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

How large is the South Korea access control market in 2026?

The South Korea access control market is valued at USD 460.28 million in 2026.

What is the forecast CAGR for the South Korea access control market from 2026-2031?

The market is projected to grow at 7.02% annually during 2026-2031.

Which product segment is expanding fastest?

Biometric Readers are forecast at an 8.22% CAGR on the back of AI-driven facial and fingerprint solutions.

Why are multi-factor authentication systems gaining traction?

National Mobile-ID (PASS) infrastructure and K-FIDO standards simplify mobile-based biometric credentials, driving 9.74% CAGR in multi-factor adoption.

What regulatory change most affects biometric deployment costs?

The 2023 PIPA amendments impose stricter consent and encryption rules, adding compliance overhead for biometric data processing.

How is cloud adoption influencing market structure?

ACaaS platforms grow at 8.61% CAGR as enterprises seek subscription models, centralized policy control and rapid scaling across distributed sites.

Page last updated on: