Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

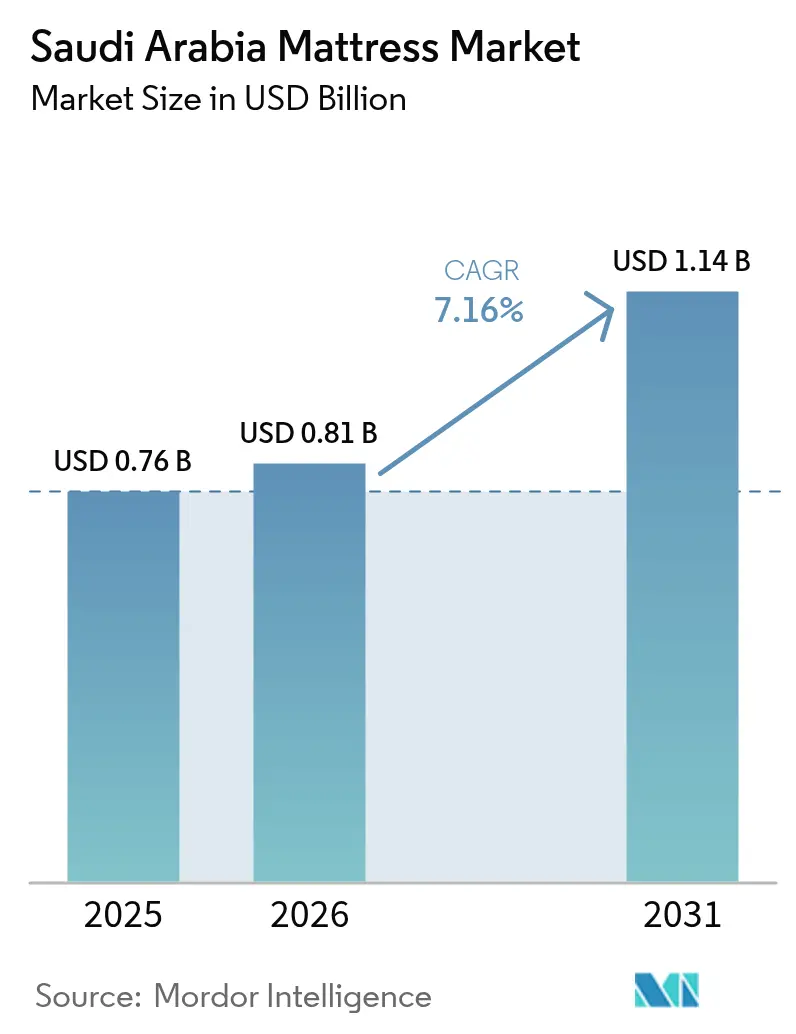

| Base Year Market Size (2025) | USD 0.76 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Mattress Market Analysis by Mordor Intelligence

The Saudi Arabia mattress market size stood at USD 0.81 billion in 2026, up from USD 0.76 billion in 2025, and is projected to reach USD 1.14 billion by 2031 at a 7.16% CAGR during the forecast period (2026-2031). Momentum is sustained by Vision 2030 execution, with rising homeownership and government-backed delivery of new housing that continues to seed first-time and replacement purchases across the Saudi Arabia mattress market. Standards enforcement and product-safety regulation through SASO tighten quality baselines and nudge households and projects to refresh inventory as non-compliant stock exits, which supports value-accretive upgrades in the Saudi Arabia mattress market. Local manufacturing and assembly reduce import exposure to duties and lead times, improving responsiveness to specification-led B2B demand and regional tastes that shape the Saudi Arabia mattress market. Omnichannel adoption and wider acceptance of digital payments lower purchase friction, which benefits mid-market and premium placements, as online discovery resets the consideration journey in the Saudi Arabia mattress market.

Key Report Takeaways

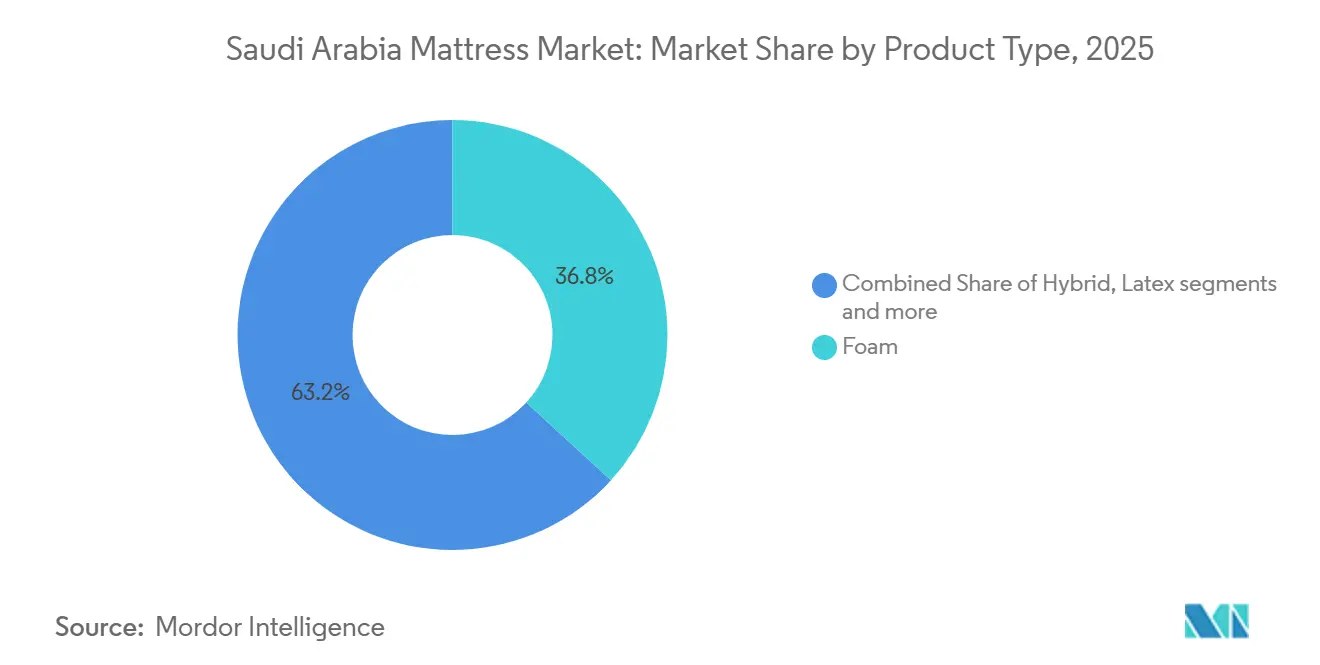

- By product type, foam led with 36.81% of the Saudi Arabia mattress market share in 2025, while hybrid is projected to record the fastest 7.85% CAGR to 2031.

- By mattress size, queen held 33.94% of the Saudi Arabia mattress market share in 2025, while king is forecast to expand at a 7.92% CAGR through 2031.

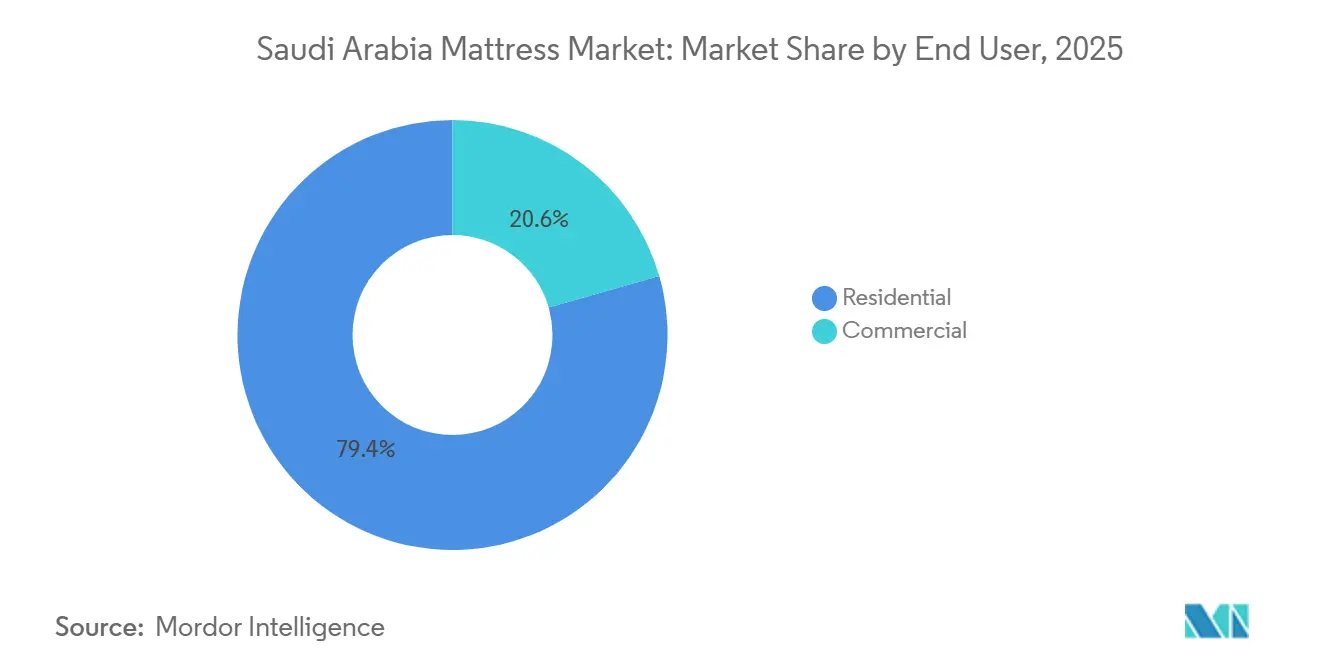

- By end user, the residential segment accounted for 79.42% of the Saudi Arabia mattress market share in 2025, while the commercial segment is set to advance at a 7.23% CAGR to 2031.

- By distribution channel, B2C retail captured 74.61% of the Saudi Arabia mattress market share in 2025, while the online channel is the fastest growing at 8.21% CAGR through 2031.

- By geography, the Eastern Region led with 34.74% of the Saudi Arabia mattress market share in 2025, while the Northern Region is projected to grow the fastest at an 8.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Housing Push and Rising Homeownership | 2.5% | National, strongest in Riyadh, Eastern Region | Medium term (2-4 years) |

| Hospitality Pipeline and Room Additions Elevate B2B Demand | 2.1% | Western (Makkah, Jeddah), Northern (NEOM), Southern (Aseer) | Long term (≥ 4 years) |

| E-Commerce And Omnichannel Adoption in Mattress Retail | 1.4% | Urban cores (Riyadh, Jeddah, Dammam) with spillover to mid-tier cities | Short term (≤ 2 years) |

| Premiumization And Wellness-Led Sleep Upgrades | 1.2% | Riyadh and Jeddah high-income clusters, early gains in the Eastern Region | Medium term (2-4 years) |

| Localization Of Manufacturing Shortens Lead Times and Customization | 1.0% | National, concentrated in the Central Region industrial zones | Medium term (2-4 years) |

| SASO Standards Enforcement Accelerates Replacement and Formalization | 0.8% | National, faster compliance in the import-heavy Western Region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Housing Push and Rising Homeownership

The Housing Program confirmed that Saudi homeownership reached 65.4% by the end of 2024 and that more than 122,000 families received housing support during 2024, which raised household formation and accelerated move-ins, thereby directly lifting demand for first-time bedroom furnishings, including mattresses[1]https://momah.gov.sa/en/node/15202?pageNumber=8. The Ministry also documented continued momentum in 2025 through large off-plan launches, which sustain a pipeline of unit handovers that translate to steady retail traffic for sleep products and related essentials. Master-planned communities under Vision 2030, including large-scale projects led by national developers, provide multi-year visibility into new-housing supply, keeping bedroom and bedding categories on a firm footing. As these households stabilize, replacement cycles begin to govern repeat purchases, supporting a gradual shift toward higher-performance foam and hybrid formats with clearer quality signaling. The result is a durable residential backbone for the Saudi Arabia mattress market that carries through the forecast horizon as the mix evolves from first-time outfitting to wellness-led upgrades.

E-Commerce and Omnichannel Adoption in Mattress Retail

Clear customs guidance for e-store buyers and sellers has increased confidence in bulky goods transactions, supporting category growth in mattresses as more purchases blend online discovery with controlled delivery and returns. Payment adoption across local schemes and digital wallets has reduced checkout friction, thereby improving conversion for high-consideration products like mattresses when paired with installment options and secure authentication flows. Within the category, the online route is the fastest-growing channel, supported by better content, AR-guided selection, and click-and-collect models that shorten the path to purchase. Standards and conformity workflows add credibility to online listings by formalizing material and safety claims that buyers can verify before completing checkout. Together, these factors drive greater value through omnichannel journeys, reinforcing steady share gains for digital routes in the Saudi Arabia mattress market while preserving the role of in-store validation for premium purchases.

Localization of Manufacturing Shortens Lead Times and Customization

Saudi Arabia’s policy environment supports local production and assembly, reducing exposure to cross-border frictions and duties, making it easier for suppliers to deliver specification-led projects and region-specific comfort preferences on reliable schedules. Domestic capacity also enables shorter production runs and custom sizes requested by large hospitality or corporate clients, improving responsiveness and controlling inventory risk for complex assortments. Integrating SASO and SABER conformity processes into local quality systems streamlines certification and reduces rework, thereby lowering working-capital drag and preserving delivery dates for time-sensitive channels. This setup favors suppliers that can consistently validate inputs and finished goods, a prerequisite for stable frame agreements in B2B categories such as hospitality and serviced apartments. The net effect is better supply resilience and improved lead times in the Saudi Arabia mattress market, as local and licensed players align on quality, cost, and service to sustain demand.

SASO Standards Enforcement Accelerates Replacement and Formalization

The Technical Regulation for Furniture Products, issued by SASO, tightened rules on hazardous substances, flammability, labeling, and traceability for mattresses, raising baseline safety standards and encouraging formal channels for certifying compliance across assortments. The 2025 standards plan includes adopting ISO 16502 methods for ignitability assessments and children’s mattress safety, based on EN 16890, to enhance testing rigor and support consumer confidence at retail and in projects[2]A https://saso.gov.sa/ar/sectors/specs/ProjectPlansEN/Specifications-projects-plan-en.pdf. Complementary regional standards for flexible urethane foam and mechanical safety provide reference methods that align material chemistries and bed stability with recognized norms. Conformity processes managed through SABER and third-party partners create clear documentation trails for both imported and locally produced goods, which streamlines customs clearance and post-market surveillance. These measures encourage upgrade cycles as non-compliant inventory clears, while also formalizing competition around verified safety and durability in the Saudi Arabia mattress market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PU Foam/Isocyanate Price Volatility Pressures Margins | -1.0% | National, acute for import-dependent converters in Western and Northern corridors | Short term (≤ 2 years) |

| 15% VAT and Import Duties Elevate Retail Price Points | -0.5% | National, disproportionate, where imports are a larger share | Medium term (2-4 years) |

| Compliance Costs and Certification Timelines (SASO/SABER) | -0.24% | National, greater impact on smaller import-reliant players | Medium term (2-4 years) |

| Project Delivery Timing Uncertainty Creates Demand Lumpiness | -0.1% | Western and Central hubs with large project pipelines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

15% VAT and Import Duties Elevate Retail Price Points

Saudi Arabia applies a 15% VAT to most goods and services, which increases the final outlay for big-ticket home products such as mattresses at the point of sale. Import processing and customs obligations add further cost layers for finished goods entering the Kingdom, and these charges are embedded in clearance workflows that all cross-border shipments must complete. In a competitive category with generous trials and promotional calendars, these fiscal elements tighten retailer margins and can deter discretionary upgrades when household budgets are stretched[3]https://www.mof.gov.sa/en/budget/2025/Documents/Bud-E%202025-251124-V8-Fin.pdf. Localization and assembly strategies mitigate some of the duty exposure and reduce lead times, but VAT still applies to the final transaction value paid by consumers. Efficient customs clearance and accurate labeling, in accordance with applicable rules, help formal players manage stock and maintain pricing discipline despite tax-related headwinds in the Saudi Arabia mattress market.

Compliance Costs and Certification Timelines Under SASO and SABER

The Technical Regulation for Furniture Products requires manufacturers and importers to meet rules for hazardous substances, flammability, labeling, and traceability, which adds recurring compliance and testing costs to mattress assortments. SABER-managed conformity, including product and shipment certificates, sets documentation standards for market entry that new or small-scale importers may find resource-intensive to maintain across multiple SKUs. Regional references such as GSO 2672 for flexible urethane foam and harmonized methods for adult-bed mechanical safety also introduce explicit test regimes that raise quality baselines while increasing pre-market lead times. The 2025 standards plan to align with ISO 16502 ignitability tests and EN 16890 for cot mattresses to provide additional safety assurance, increasing compliance overhead for suppliers without integrated labs or established certification partners. These requirements favor organized, vertically integrated players while pushing smaller, import-reliant distributors to rationalize assortments or exit slower-moving models in the Saudi Arabia mattress market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Mattresses Capture Premiumization Wave, Foam Holds Volume

Foam mattresses led the category with 36.81% in 2025, and hybrid designs are forecast to grow the fastest at a 7.85% CAGR through 2031 as shoppers look for cooling comfort and edge support that suit local living patterns. Foam commanded 36.81% of the Saudi Arabia mattress market share in 2025 due to broad retail availability, value price points, and continued improvements in breathability for hot climates. Hybrid formats that blend coils with foam or latex address motion isolation and perimeter stability, making them appealing for larger bed sizes that are gaining popularity in multi-bedroom homes. As standards take hold, safety and durability signaling on labels and in-store displays matters more, which supports better differentiation across good, better, and best tiers. Organized players that can consistently certify inputs and finished goods through SABER and related conformity schemes are positioned to consolidate market share as the Saudi Arabia mattress market matures around features and verified performance[2].

By Mattress Size: King-Size Aspirations Drive Premium Growth

Queen models delivered 33.94% of shipments in 2025 due to efficient room fit and mid-tier pricing that suits urban apartments. King units, though lower in volume, advance at a 7.92% CAGR as affluent households upgrade their master suites and hospitality venues mimic international luxury benchmarks. Architects specify spacious sleeping areas in new villa designs, reinforcing king adoption and lifting input demand for extra-wide pocket-coil cores. Retail spaces highlight aspirational bedroom vignettes, and financing plans normalize larger outlays, expanding the addressable swing-up pool. Packaging innovations reduce king-size freight surcharges, granting online sellers parity in shipping costs that spur incremental uptake inside the Saudi Arabia mattress market.

Smaller single and double formats retain importance for children’s rooms, staff housing, and furnished rental apartments, although replacement pacing trails the wider average. Custom orders arise in boutique hotels and high-net-worth residences where non-standard dimensions or adjustable bases dictate bespoke builds. Manufacturers manage SKU complexity through modular layer systems that resize easily, cutting inventory risk while still serving niche sizes profitably. Sales data confirm life-stage progression, with first-home buyers moving from double to queen within five years, then shifting to king once space permits. That predictable migration guides merchandising strategies and supports stable growth across all sizes inside the Saudi Arabia mattress market.

By End User: Residential Dominance with Commercial Acceleration

The residential segment commands 79.42% market share in 2025 while growing at 7.23% CAGR, reflecting the Kingdom's housing boom and homeownership initiatives that have supported over 1 million families through programs like Sakani, creating sustained demand for home furnishing, including mattresses. Mortgage subsidies and rising household formation sustain annual replacement and new-household purchases, while influencer-driven marketing lifts acceptance of higher-priced comfort technologies. Online search trends show that mattresses are among the top five furniture keywords nationwide, indicating heightened consumer mindfulness about sleep welfare. Retail showrooms concentrate in malls to capture weekend family traffic, and loyalty apps encourage routine rotation and eventual replacement. Upselling adjustable bases and complementary bedding lifts ticket sizes without eroding conversion rates.

Commercial demand increases at a faster clip due to hospitality development and public-sector dormitory projects. Institutional buyers favor standardized SKUs with reinforced edges, high-cycle compression ratings, and flame-retardant barriers that meet global brand manuals. Suppliers win tenders by combining local manufacturing capacity with international warranty backing, mitigating currency swing risks, and ensuring consistent after-sales service. Healthcare and senior-care facilities join hotels in requiring pressure-relief surfaces and antimicrobial covers, diversifying commercial order books. The cyclical refurbishment of hotel stock every four to six years creates predictable repeat business that stabilizes the Saudi Arabia mattress market’s commercial stream.

By Distribution Channel: Retail Transformation Through Digital Integration

B2C retail channels dominate with 74.61% market share in 2025 while accelerating at 8.21% CAGR, reflecting the consumer preference for physical mattress evaluation combined with emerging digital shopping behaviors that enable omnichannel purchasing experiences. In-store experiences focus on guided comfort trials, sleep profiling kiosks, and staged bedroom settings to convert floor traffic into premium purchases. Online channels grow swiftly thanks to zero-interest payment schedules and extended return policies that alleviate fit concerns. Compressed-roll packaging and same-day fulfillment in Riyadh and Jeddah ease delivery friction and amplify word-of-mouth recommendations. Hybrid retailers adopting a “click-and-collect” model achieve higher attachment rates for accessories like mattress protectors and sheets.

Suppliers cultivate relationships with contractors and project-management firms to secure early specifications and lock in order pipelines. Warehouse clubs and department stores carry limited assortments aimed at promotional price points, complementing but not cannibalizing specialty shop revenue. The expected rise of omnichannel will repose physical stores as experiential hubs rather than pure inventory points. Robust Saber compliance processes at warehouse entry guarantee quality assurance across all sales routes in the Saudi Arabia mattress market.

Geography Analysis

The Eastern Region led with 34.74% in 2025, and the Northern Region is projected to grow the fastest at an 8.18% CAGR through 2031, as major developments and new communities expand the base for residential and hospitality demand. The Eastern Region benefits from diversified employment, infrastructure, and logistics capacity that improve the availability and service levels of formal retail. Northern Region’s growth prospects reflect the Vision 2030 development momentum, which introduces new residential and lodging assets that, over time, lift baseline demand for compliant bedding. Central Region remains a premium anchor given its concentration of high-income households and corporate demand, which sustains both retail traffic and B2B tender activity in the Saudi Arabia mattress market.

The Western Region enjoys enduring religious tourism, and formal hospitality projects depend on validated flammability and durability specifications that align with SASO and regional standards. Southern Region builds on domestic tourism draws and growing retail footprints that cater to mainstream price points and family formats. These geographic dynamics reward suppliers that tailor assortments to income bands, climate, and room sizes that vary across city clusters in the Saudi Arabia mattress market. As infrastructure and compliance maturity deepen outside the top metros, visibility into deliveries and post-sale service improves, strengthening formal channels.

Across regions, local manufacturing and assembly hubs near demand centers support faster delivery and more adaptable production runs. Standards adoption across ignition, materials, and mechanical safety is uniform, creating consistent compliance expectations across regions. Eastern and Central regions often set the pace on premium features and hybrid formats, while Northern and Southern regions follow with value tiers that move up over subsequent replacement cycles. This progression shapes assortment and pricing ladders while preserving room for specialty and custom sizes in hospitality and luxury residential projects across the Saudi Arabia mattress market.

Competitive Landscape

Competition features a blend of domestic manufacturers, regional licensees of global brands, and diversified home retailers that operate national store networks and e-commerce platforms. Organized players leverage compliance, warranties, and delivery capabilities to capture demand in both retail and project channels, while import-reliant distributors concentrate on niche and luxury assortments. Local conversion and assembly compress lead times, reduce duty exposure, and enable custom specifications common in hospitality and corporate housing. These capabilities align well with SASO's regulatory expectations for labeling, traceability, and fire safety, which formalize product claims and quality controls across the Saudi Arabia mattress market.

Retailers with strong omnichannel execution are strengthening the bridge between online discovery and in-store validation. Payment readiness, installment options, and secure checkout experiences increase consideration for premium foam and hybrid models, especially among younger buyers who value convenience and service. Category leaders deploy curated assortments at graduated price points, pair them with trial policies, and emphasize certified materials and tested performance. This approach helps reduce return rates and strengthen brand trust, both crucial in higher-priced segments of the Saudi Arabia mattress market.

International licensees maintain quality alignment with parent brands while investing in regional supply to match local service requirements. Domestic champions scale manufacturing and compliance capabilities to meet SABER and shipment-conformity needs that intensive project work demands. Partnerships between retailers and producers emphasize stable pricing on contracted volumes and reliable replenishment, which serve as differentiators during peak demand periods. As the market formalizes, players that integrate compliance, omnichannel experience, and local production are best placed to defend and grow share in the Saudi Arabia mattress market over the forecast period.

Saudi Arabia Mattress Industry Leaders

Sleep High

IKEA Saudi Arabia

Home Centre Saudi Arabia

Sealy Middle East

King Koil Saudi Arabia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bed Quarter, the exclusive Eclipse International licensee in Saudi Arabia and a division of MAZ Holding Group, opened the first flagship Eclipse Exclusive mattress store in Riyadh, showcasing the Royal collection with over 6,000 springs and tufting technology developed specifically for the Middle East market.

- September 2024: Eight Sleep, a U.S.-based sleep technology company, officially launched its AI-powered Pod 5 system in Saudi Arabia at SAR 11,999.

- October 2025: Spring Air International expanded its Sleep Copper collection internationally for the first time through Saudi Arabia licensee BedHouse (MAZHOLDING GROUP), making it available across the Middle East, including Saudi Arabia, UAE, Bahrain, Kuwait, Oman, and Qatar.

- June 2024: Bedding Industries of America (BIA), parent company of Eclipse International, partnered with Saudi Arabia's Bed Quarter Company (MAZ Holding Group) via a licensing deal to produce and distribute Eclipse mattresses across Saudi Arabia, GCC countries, Jordan, Syria, Lebanon, and North Africa.

Saudi Arabia Mattress Market Report Scope

A mattress, a sizable and flat pad, typically has a durable covering filled with straw, foam rubber, cotton, hair, feathers, and sometimes coiled springs. Mattresses are often quilted or tufted at regular intervals. They are the primary sleeping surface, standalone or placed on a bedstead.

The report comprehensively analyzes the Saudi Arabian mattress market, delving into emerging trends, notable market dynamics, and a market overview. The Saudi Arabian mattress market is segmented by type, application, and distribution channel. The market types include innerspring, memory foam, latex, and others. Applications span residential and commercial sectors. Distribution channels are segmented into online and offline. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| Eastern Region (Dammam, Khobar) |

| Northern Region |

| Southern Region |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | Eastern Region (Dammam, Khobar) | |

| Northern Region | ||

| Southern Region | ||

Key Questions Answered in the Report

What is the Saudi Arabia mattress market size and growth outlook to 2031?

The Saudi Arabia mattress market size stood at USD 0.81 billion in 2026, up from USD 0.76 billion in 2025, and is projected to reach USD 1.14 billion by 2031 at a 7.16% CAGR

Which product types lead demand within Saudi Arabia?

Foam leads by volume with a 36.81% share in 2025, driven by its value and availability, while hybrids are the fastest-growing segment as shoppers seek cooling and support benefits in layered designs.

How are regulations affecting mattress buying and supply in Saudi Arabia?

SASO’s updated rules raise flammability, hazardous-substance, and traceability requirements, remove non-compliant stock, improve safety signaling, and steer demand toward formal, warranty-backed channels.

Which channels are growing the fastest for mattresses in Saudi Arabia?

B2C retail remains dominant at 74.61% in 2025, while the online channel is the fastest-growing, with an 8.21% CAGR through 2031 as payments, logistics, and click-and-collect improve.

What regions should suppliers prioritize in Saudi Arabia?

Eastern Region holds the largest 2025 share at 34.74%, and Northern Region shows the fastest expected growth at an 8.18% CAGR through 2031 as new communities and hospitality assets scale.

Page last updated on: