Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

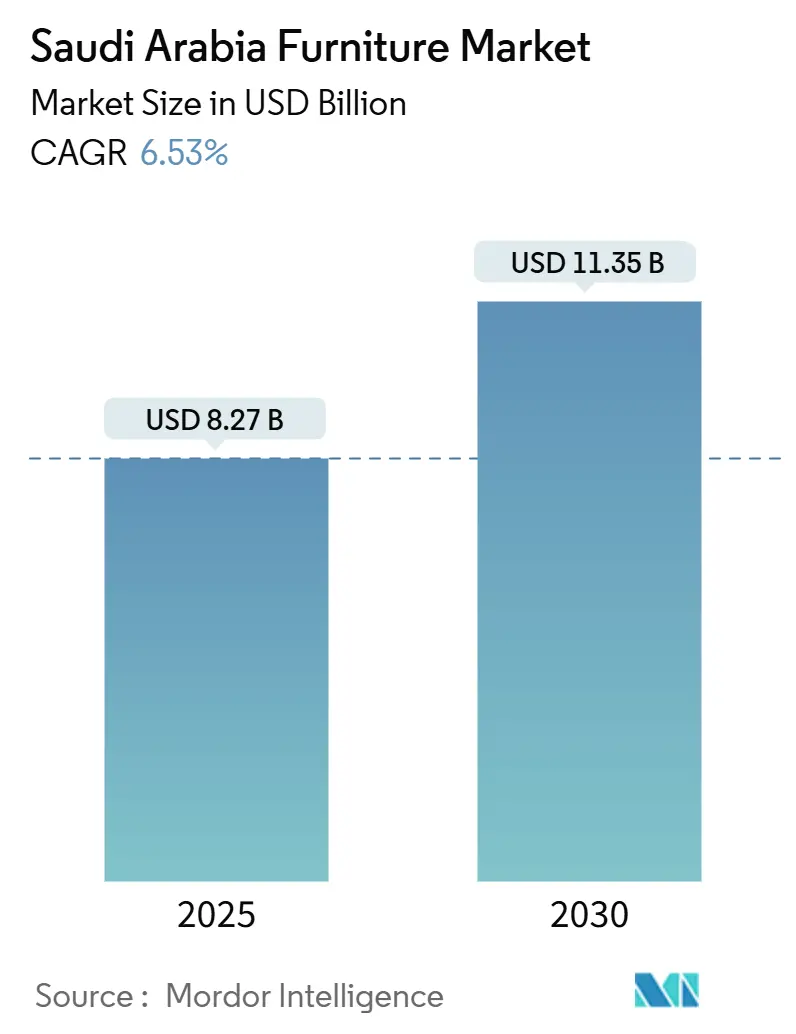

| Market Size (2025) | USD 8.27 Billion |

| Market Size (2030) | USD 11.35 Billion |

| Growth Rate (2025 - 2030) | 6.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Furniture Market Analysis by Mordor Intelligence

The Saudi Arabia furniture market size is valued at USD 8.27 billion in 2025 and is expected to advance to USD 11.35 billion by 2030 at a 6.53% CAGR. Vision 2030’s residential build-out, the rapid rollout of giga-tourism projects, and the booming digital economy are reshaping demand patterns and channel strategies. Developers’ shift toward large, master-planned communities sustains bulk orders for integrated home-furniture packages, while hospitality investors require bespoke contract pieces that meet five-star brand standards. Government procurement reforms are unifying technical specifications across ministries, tightening quality oversight, and elevating local-content thresholds. At the same time, e-commerce adoption, buoyed by buy-now-pay-later (BNPL) services, is pulling a rising share of discretionary purchases online. Against this backdrop, manufacturers are diversifying raw-material mixes, wood, metal, and advanced polymers, to align with stricter sustainability requirements and Saudi climate conditions.

Key Report Takeaways

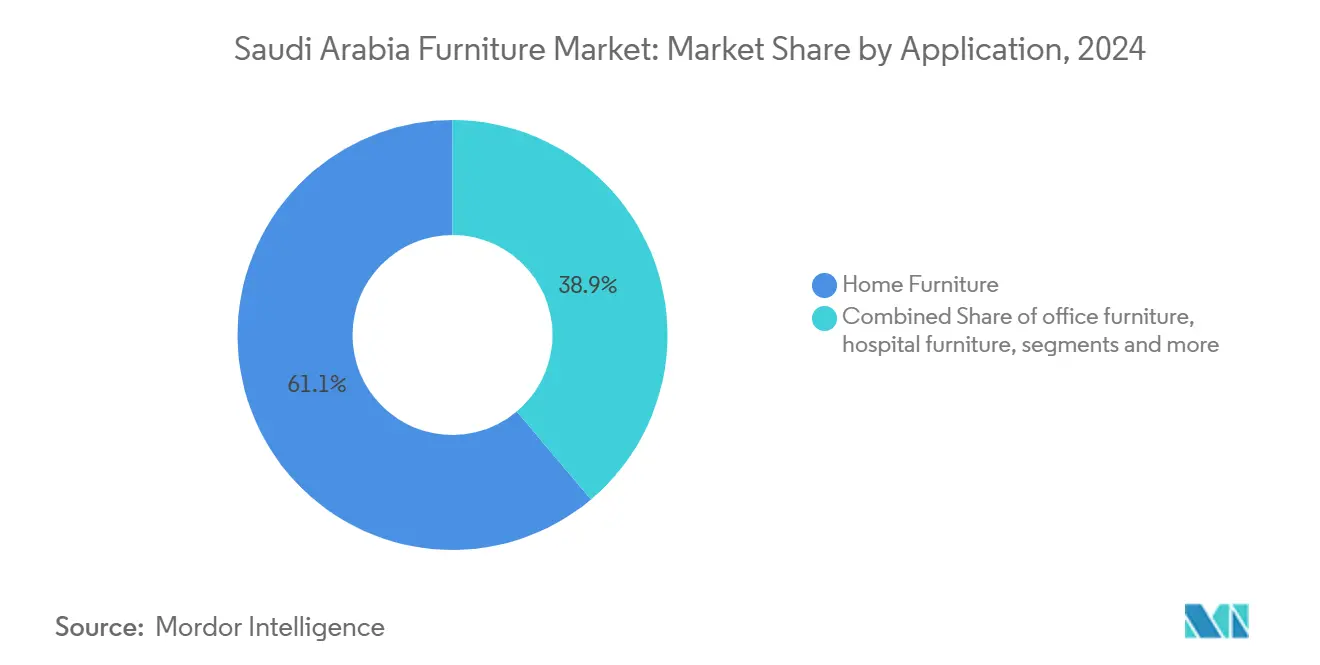

- By application, home furniture led with 61.13% of the Saudi Arabia furniture market share in 2024; hospitality furniture is projected to expand at a 7.10% CAGR through 2030.

- By material, wood captured 55.13% of the Saudi Arabia furniture market size in 2024, while plastic & polymers are on track to grow at a 6.50% CAGR.

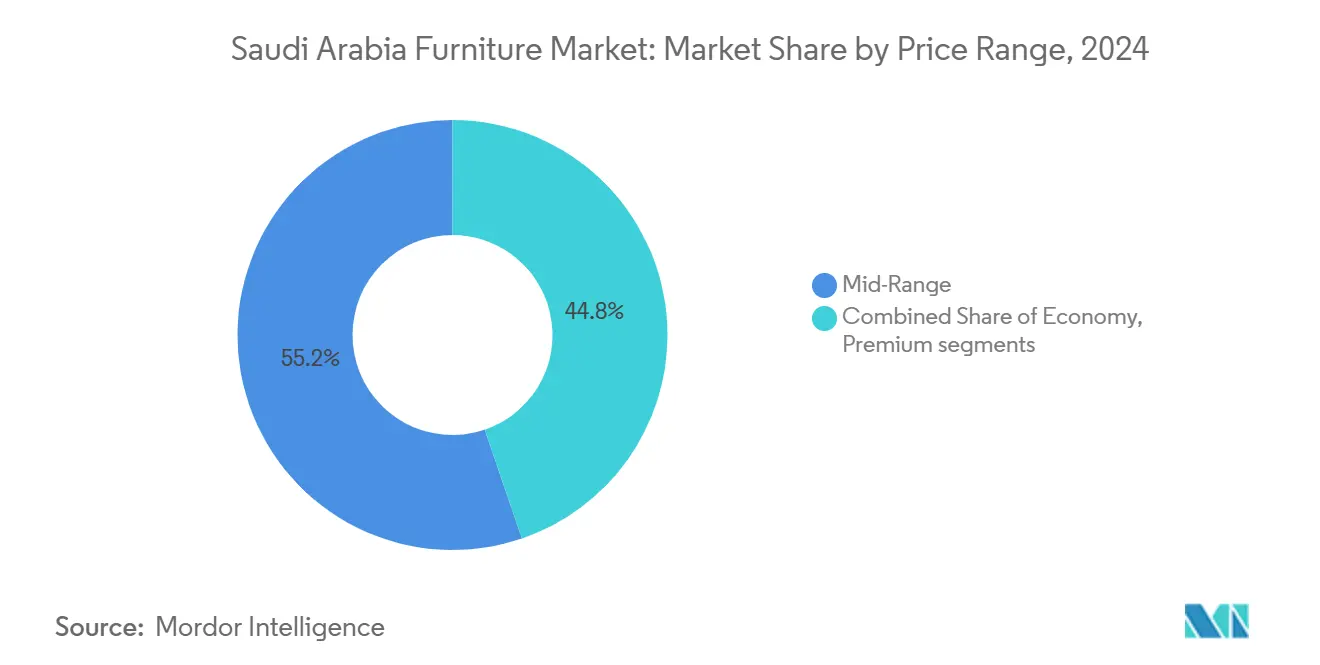

- By price range, the mid-range segment held 55.24% of the Saudi Arabia furniture market share in 2024; premium furniture is forecast to rise at a 6.36% CAGR through 2030.

- By distribution channel, B2C/retail controlled 62.65% of the Saudi Arabia furniture market size in 2024 and is advancing at a 7.40% CAGR.

- By region, the central region accounted for 36.51% share of the Saudi Arabia furniture market in 2024 and the western region is climbing at a 7.53% CAGR over the same period.

Saudi Arabia Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 residential build-out | +1.8% | Central & western provinces | Medium term (2–4 years) |

| Hospitality giga-projects | +1.5% | Western tourist corridors (NEOM, Red Sea) | Long term (≥ 4 years) |

| Rapid e-commerce and BNPL uptake | +1.2% | Riyadh, Jeddah, other large urban centers | Short term (≤ 2 years) |

| ESG-linked government tenders | +0.8% | Nationwide, public-sector procurement | Medium term (2–4 years) |

| Saudization spurring ergonomic office-furniture upgrades | +1.0% | Corporate hubs, government offices | Short to Medium term (1–3 years) |

| Panel-board localisation amid Red Sea shipping risk | +0.9% | Coastal industrial zones, domestic supply chains | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 residential build-out is accelerating home-furniture demand

Saudi Arabia's USD 1.6 trillion construction pipeline under Vision 2030 is creating systematic furniture demand across residential developments, with the government targeting one million new housing units. Knight Frank estimates the Kingdom needs approximately 115,000 homes annually over the next six years to meet youth-driven demographic demand, translating to sustained home furniture procurement. Developers like Reportage KSA, which achieved SAR 350 million (USD 93.33 million) sales in 2024, are launching integrated residential communities that require comprehensive furniture packages from kitchen cabinets to bedroom sets. The Saudi Industrial Development Fund has provided 89 loans totaling SAR 636 million (USD 169.60 million) to wooden furniture manufacturers, indicating government commitment to supporting domestic supply capabilities[1]Source: SaudiPedia, “Logging in Saudi Arabia,” saudipedia.com. .

Hospitality Giga-Projects Fuelling Contract & Luxury Segments

NEOM's hospitality division has partnered with 20+ global hotel brands, including Four Seasons, Marriott, and Hyatt, to develop innovative hotel concepts across Trojena, Sindalah, and Oxagon zones[2]NEOM, “Hospitality Partnerships,” neom.com.. Diriyah Company awarded a USD 2.13 billion contract to construct four luxury hotels (Aman, Six Senses, The Chedi, Faena) requiring bespoke furniture and fixtures. The Red Sea Development and Rua Al Madinah projects collectively target 149,000 visitors by 2030, necessitating 47,000+ hospitality units with specialized contract furniture. These mega-projects are driving the Hospitality Furniture segment's 7.10% CAGR, the fastest among all application segments. NEOM's Sindalah Yacht Club, designed by Stefano Ricci with Carrara marble and hand-woven Florentine fabrics, exemplifies the luxury positioning that's elevating furniture specifications and pricing power across the contract segment.

Rapid E-Commerce & BNPL Adoption Boosting Online Furniture

Saudi Arabia's e-commerce market ranks 26th globally on BMI's E-Commerce Maturity Index, with household online spending projected to grow at 10.60% CAGR to USD 24.5 billion by 2029. The Kingdom's 85.40% urbanization rate and 47.40% of households earning above USD 50,000 create ideal conditions for online furniture adoption, particularly among the young demographic. ABYAT's loyalty program offering tiered cashback (2-5% based on purchase volume) and companies like Al Rugaib Furniture launching mobile apps with 10,000+ downloads demonstrate retailers' digital transformation. Buy-now-pay-later services through Tabby and Tamara are reducing purchase barriers for high-ticket furniture items, while free delivery thresholds encourage larger basket sizes.

ESG-Linked Public Tenders Favoring Certified Wood Furniture

The Saudi Standards, Metrology and Quality Organization (SASO) has implemented comprehensive technical regulations through the SABER platform, requiring a Certificate of Conformity for all consumer goods, including furniture[3]SABER, “Technical Regulations for Furniture,” saber.sa.. Government procurement exceeding USD 1 billion annually increasingly emphasizes sustainability credentials, with the Local Content and Government Procurement Authority adding 11 furniture products worth USD 910 million to mandatory local-content lists. The Kingdom's USD 180 billion decarbonization commitment and net-zero-by-2060 target are driving preference for certified wood products and sustainable materials. Environmental regulations under the Environmental Law impose penalties up to SAR 30 million (USD 8 million) for unauthorized logging, forcing furniture manufacturers to source certified timber or face compliance risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics costs & import duties | –1.1% | Eastern ports, long-haul domestic distribution | Short term (≤ 2 years) |

| Volatile timber & foam input prices | –0.9% | Import-dependent manufacturing hubs | Short term (≤ 2 years) |

| Permitting delays postponing fit-out schedules | –0.7% | Urban commercial development zones | Short term (≤ 2 years) |

| Skilled labour shortages in upholstery & joinery | –1.0% | Industrial furniture manufacturing clusters | Short to Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

High logistics & import duties are squeezing margins

Port congestion, Red Sea rerouting, and customs fee hikes are lifting landed costs by 15-20%, while Red Sea shipping disruptions and elevated import duties are compressing furniture retailer margins, particularly for the 70% of products that rely on international supply chains. The Kingdom's furniture import dependence, evidenced by tripled plywood imports to Dubai and Riyadh ports over the past year, exposes manufacturers to volatile freight costs and currency fluctuations. Dammam Port's SAR 300 million (USD 80 million) vehicle logistics park development by Mawani and Alissa Group signals infrastructure improvements, but current bottlenecks inflate landed costs by 15-20% compared to pre-2024 levels. The SAL Logistics Zone's SAR 4 billion (USD 1.07 billion) investment in Riyadh, featuring 1.5 million square meters of automated warehousing, aims to address supply chain inefficiencies but won't reach full capacity until 2027.

Volatile Timber & Foam Input Prices

Global timber price volatility, exacerbated by environmental restrictions on domestic logging, is creating margin pressure across the Saudi furniture manufacturing base of 363 factories. The Environmental Law's absolute ban on local firewood/charcoal exports and customs duty exemptions for imported alternatives indicate structural dependence on international timber markets. Foam input costs remain elevated due to petrochemical price cycles, affecting upholstery and bedding segments that represent significant portions of home furniture demand. Companies like Areen Holding Group, operating five manufacturing plants totalling 75,000 square meters, are investing in vertical integration to mitigate input cost volatility. The Saudi Modern Factory for Steel & Wooden Furniture emphasizes global specifications compliance to maintain quality standards despite input price pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Contract segments drive premium growth

Home furniture dominates the Saudi Arabia furniture market share at 61.13% in 2024, thanks to continuous villa and apartment deliveries. Demand clusters around bedroom suites, modular wardrobes, and kitchen cabinetry. Contract channels, however, are the main growth story. The hospitality sub-segment, propelled by giga-project tenders, is forecast to record a 7.10% CAGR, the fastest across applications. Office furniture benefits from Saudization mandates for ergonomic upgrades, while education and healthcare orders track public-sector capital-spending plans. Makers capable of customizing to brand standards or hospital-grade hygiene requirements secure higher margins.

Saudi Arabia's furniture market size for hospitality applications is projected to expand from USD 1.14 billion in 2025 to USD 1.62 billion by 2030, underscoring the shift toward experience-driven tourism. In contrast, the Saudi Arabia furniture market size for home use rises steadily but at a slower pace as household penetration starts from a higher base.

By Material: Sustainability drives polymer innovation

Wood maintains the largest material share at 55.13% in 2024, supported by the Kingdom's embrace of timber construction and sustainable building practices. Traditional wood furniture benefits from ESG-linked procurement policies favoring certified materials, though domestic logging restrictions force reliance on imported timber from sustainable sources. Metal furniture serves industrial and office applications, with companies like Eastern Aluminium Extrusion in Dammam providing aluminium profiles for furniture frames and architectural applications.

Plastic and Polymer segments show the fastest growth at 6.50% CAGR, driven by climate-adapted outdoor furniture demand and innovative materials meeting SASO biodegradable plastic requirements. The National Center for Vegetation Cover's 10-billion-tree initiative creates long-term domestic wood supply potential, while polymer innovation addresses durability requirements in the Kingdom's harsh climate conditions. Other Materials, including composites and engineered products, gain traction in specialized applications, particularly for hospitality projects requiring custom specifications and fire-retardant properties mandated by SASO technical regulations.

By Price Range: Premium segment accelerates

Mid-Range furniture dominates with 55.24% market share in 2024, reflecting the Kingdom's expanding middle class and preference for quality-value positioning across home and office categories. This segment benefits from retailers like IKEA Saudi Arabia's franchise expansion to 30 locations by 2028 and Ashley HomeStore's six-store network offering accessible luxury positioning. Economy furniture serves price-sensitive consumers and bulk institutional buyers, with government tenders frequently specifying basic functionality requirements for educational and healthcare facilities.

Premium furniture emerges as the fastest-growing segment at 6.36% CAGR through 2030, driven by luxury hospitality projects like NEOM's Sindalah Yacht Club featuring Stefano Ricci interiors and Carrara marble finishes. High-net-worth individuals and luxury hotel developments increasingly demand bespoke furniture solutions, with companies like RIS Store KSA offering products up to SAR 34,210 (USD 9,122) for premium sofas and tables. The premium segment's growth reflects the Kingdom's economic diversification and rising disposable incomes among urban professionals, with luxury positioning becoming increasingly viable as consumer sophistication advances.

By Distribution Channel: Digital transformation accelerates

B2C/Retail channels command 62.65% market share in 2024 while simultaneously achieving the fastest growth at 7.40% CAGR, indicating both market dominance and digital transformation momentum. Home-Improvement Centers benefit from the residential construction boom, with retailers expanding physical footprints across major cities. Specialty Furniture Stores like ABYAT operate comprehensive showrooms while developing loyalty programs offering 2-5% cashback to encourage repeat purchases.

Online channels experience rapid adoption supported by BNPL services through Tabby and Tamara, with household e-commerce spending projected to reach USD 24.5 billion by 2029. B2B/Project channels serve the growing contract furniture market, with government procurement exceeding USD 1 billion annually through standardized tender processes. The convergence of online and offline retail, evidenced by companies like Al Rugaib Furniture launching mobile apps while maintaining physical showrooms, reflects omnichannel strategies capturing both convenience-seeking consumers and experience-driven shoppers requiring tactile product evaluation before purchase.

Geography Analysis

The Central Region dominates with 36.51% market share in 2024, driven by Riyadh's concentration of government institutions, corporate headquarters, and mega-developments like Diriyah's USD 2.13 billion luxury hotel projects. The region benefits from the SAL Logistics Zone's SAR 4 billion (USD 1.07 billion) investment, creating 1.5 million square meters of automated warehousing, improving furniture distribution efficiency across the Kingdom. Government procurement exceeding USD 1 billion annually concentrates in Riyadh through ministries and agencies, while Saudisation policies drive ergonomic office furniture upgrades across corporate districts.

The Western Region achieves the fastest growth at 7.53% CAGR through 2030, propelled by tourism infrastructure investments and luxury hospitality developments across Makkah, Madinah, and coastal areas. NEOM's hospitality division has partnered with 20+ global hotel brands requiring specialized contract furniture, while the Red Sea Development targets premium tourism markets with bespoke interior specifications. Jeddah Central's USD 3.2 billion investment includes 17,000 residential units and luxury amenities, creating sustained furniture demand through 2027. The region's retail expansion includes LuLu Group's 200,000 square foot Makkah hypermarket and furniture retailers establishing showrooms to serve the growing affluent population.

The Eastern Region leverages its industrial heritage and port infrastructure to capture furniture manufacturing and logistics opportunities, with Dammam's 2.4 million square meter industrial city project creating space for furniture production facilities. Companies like Arfad International Industry operate 20,000 square meters of manufacturing serving Saudi Aramco and government clients, while Eastern Aluminum Extrusion provides metal components for furniture frames. The region's strategic location enables furniture exports to GCC markets, supported by Dammam Port's SAR 300 million (USD 80 million) logistics park development, improving cargo handling efficiency. Northern and Southern Regions benefit from IKEA's retail expansion to Jazan and Abha, demonstrating furniture retailers' confidence in regional purchasing power and infrastructure development.

Competitive Landscape

The Saudi Arabia furniture market is moderately concentrated, with the top five players commanding a significant market share in 2024, suggesting ample white-space opportunities for both expansion and new market entrants. IKEA Saudi Arabia leads the market, operating under a franchise agreement with Alsulaiman Group, which aims to increase its presence from 10 to 30 customer meeting points by 2028. The group is also adopting Lean Management practices to enhance operational efficiency. As international brands form local partnerships and domestic manufacturers scale up, competition is intensifying. Key players like Almutlaq Group are leveraging diversified investments, while Al-Rugaib Furniture focuses on digital growth through mobile app-driven channels.

Strategic growth in the sector revolves around omnichannel retail expansion, vertical integration, and digital transformation to cater to both consumer and contract markets. Ashley HomeStore’s franchise agreement with Hamad M. Alrugaib & Sons showcases this model, with six store openings, including a 35,090-square-foot showroom in Buraydah, signalling a strong regional focus. ABYAT exemplifies a platform-driven approach with a wide-ranging catalog and tiered cashback loyalty program, capturing customers across the furniture and home improvement spectrum. Vertically integrated manufacturers such as Areen Holding Group, which operates five production facilities and 18 showrooms, benefit from cost control and tailored offerings.

White-space growth opportunities are emerging in premium hospitality furniture, sustainable material offerings, and regional expansion outside major urban centers. Mega-projects under Vision 2030 are driving demand for specialized contract furniture, necessitating local manufacturing capabilities and SASO regulatory compliance. Players with expertise in localized production and project-based fulfillment are increasingly valuable. Sustainable design and eco-certified materials also present a competitive edge as consumer preferences shift.

Saudi Arabia Furniture Industry Leaders

IKEA Saudi Arabia

Almutlaq Furniture

Al-Rugaib Furniture

Home Centre (Landmark Group)

Ashley HomeStore Saudi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MEED confirms USD 25 billion in giga-project contracts awarded in 2024, including hotel and mixed-use schemes that boost future contract-furniture orders.

- March 2025: Riyadh municipality releases 20 new investment plots totalling 175,000 m² for retail and manufacturing, opening fresh opportunities for furniture factories.

- March 2025: SAL Logistics Zone launches a SAR 4 billion (USD 1.07 billion) automated warehouse hub in Riyadh, enhancing last-mile capabilities for bulky goods.

- December 2024: Ashley HomeStore opens a 35,090 ft² showroom in Buraydah, its sixth domestic outlet.

Saudi Arabia Furniture Market Report Scope

Furniture is essential for homes and businesses, providing comfort and style. The demand for modern furniture has increased, leading to a wide selection of items like tables, chairs, beds, and cabinets. Different materials like plastic, wood, and metal are used to meet various preferences. The Saudi Arabian furniture market is segmented by type, application, and distribution channel. By type, the market is segmented into wood, metal, plastic, and other furniture. By application, the market is segmented into home furniture, office furniture, hospitality furniture, and other furniture, and by distribution channel, the market is segmented into supermarkets and hypermarkets, specialty stores, online, and other distribution channels. The report offers market size and forecasts for the Saudi Arabian furniture market in value (USD) for all the above segments.

By Application

| Home Furniture | Chairs |

| Tables | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (bathroom furniture, outdoor furniture, etc.) | |

| Office Furniture | Chairs |

| Desks & Workstations | |

| Storage Cabinets | |

| Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| B2C / Retail | Home-Improvement Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

By Region

| Central Region (Riyadh, Al-Qassim) |

| Western Region (Makkah, Madinah) |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Application | Home Furniture | Chairs |

| Tables | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (bathroom furniture, outdoor furniture, etc.) | ||

| Office Furniture | Chairs | |

| Desks & Workstations | ||

| Storage Cabinets | ||

| Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C / Retail | Home-Improvement Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Region | Central Region (Riyadh, Al-Qassim) | |

| Western Region (Makkah, Madinah) | ||

| Eastern Region | ||

| Northern Region | ||

| Southern Region | ||

Key Questions Answered in the Report

How large is household spending on online furniture purchases in Saudi Arabia?

Household e-commerce spending on furniture contributes to a broader USD 24.5 billion online retail pool projected for 2029, supporting a 7.40% CAGR in B2C furniture sales.

What segments are expanding fastest within the Saudi furniture landscape?

Hospitality and premium-priced furniture lines lead with 7.10% and 6.36% CAGRs respectively owing to luxury tourism projects and rising affluent demand.

Which raw materials face the greatest price volatility for Saudi manufacturers?

Imported timber and polyurethane foam experience the widest swings, prompting factories to explore engineered-wood substitutes and forward-purchase contracts.

Why is the western region outpacing other areas in furniture growth?

Massive tourism ventures such as NEOM and Red Sea Global, plus Jeddah Central’s mixed-use plan, are accelerating hospitality and residential furniture demand at a 7.53% CAGR.

How are retailers adapting to Saudi consumers’ digital preferences?

Stores deploy omnichannel models mobile apps, VR room planners and BNPL options to blend online convenience with showroom experiences, boosting conversion and basket sizes.

Page last updated on: