Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.37 Billion |

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Home Textile Market Analysis by Mordor Intelligence

Saudi Arabia home textiles market size in 2026 is estimated at USD 1.42 billion, growing from 2025 value of USD 1.37 billion with 2031 projections showing USD 1.72 billion, growing at 3.88% CAGR over 2026-2031. Robust spending under Vision 2030, large-scale residential completions, and hospitality giga-projects underpin growth momentum. Demand is amplified by ROSHN Group’s annual delivery of 115,000 housing units, the Red Sea Project’s 50 resort destinations, and retail modernization that lifts discretionary outlays. Competitive strategies revolve around localization incentives, digital-first retail, and sustainable material differentiation. Opportunities arise from premium linen specifications in luxury hotels, while risks stem from cotton-price volatility and Saudization-driven labor-cost pressures.

Key Report Takeaways

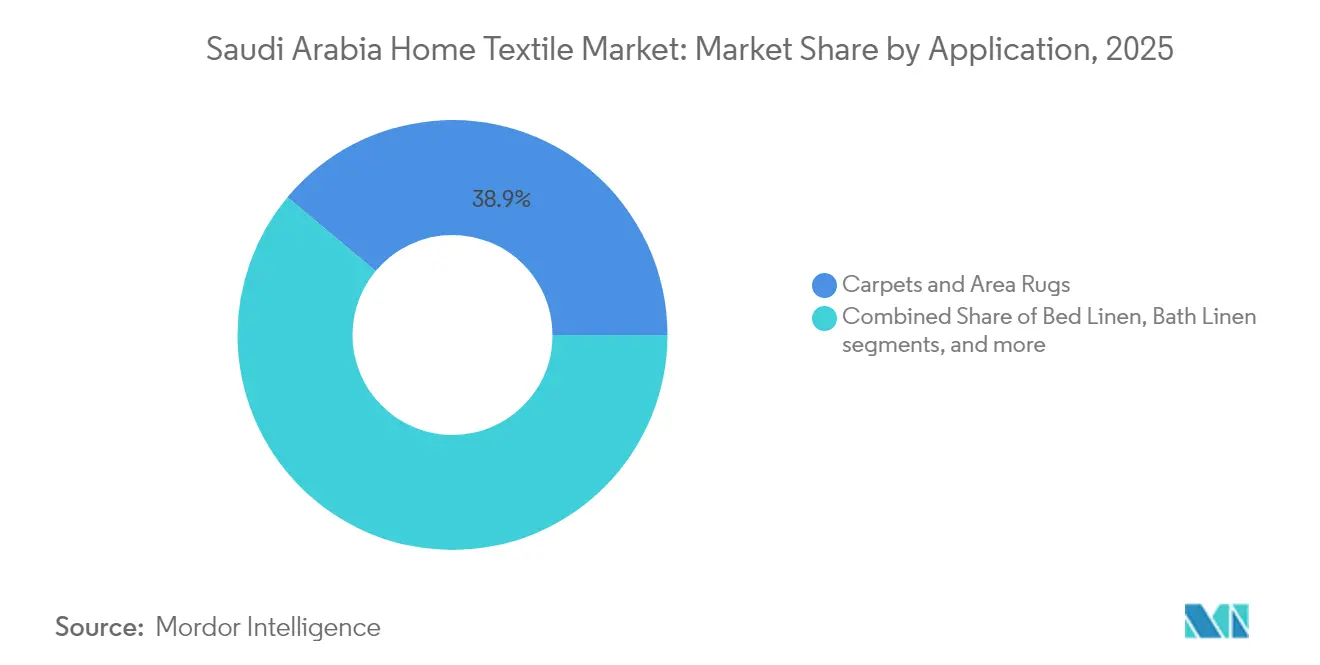

- By application, carpets and area rugs led with 38.94% revenue share in 2025; upholstery is poised for the fastest 6.12% CAGR to 2031.

- By material, synthetic fibers commanded 51.05% share of the Saudi Arabia home textiles market size in 2025, while wool, hemp, and bamboo are projected to grow at a 5.19% CAGR through 2031.

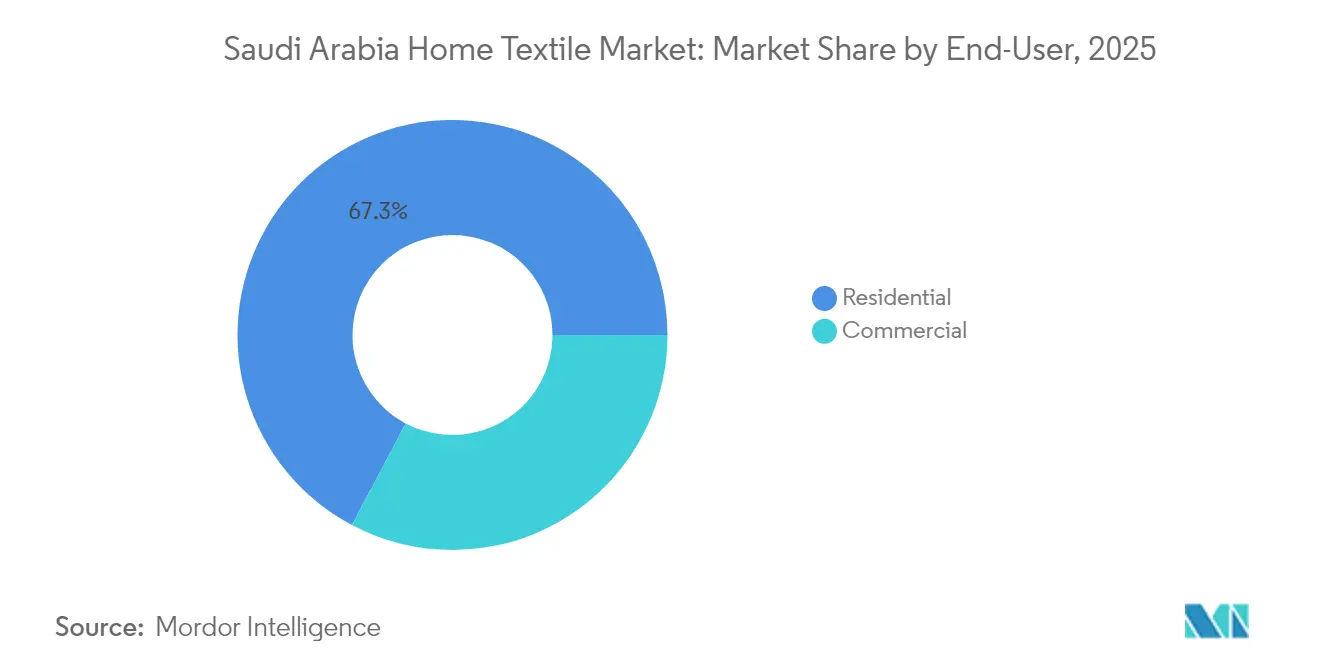

- By end-user, residential captured 67.25% of the Saudi Arabian home textiles market share in 2025; commercial is advancing at a 5.48% CAGR through 2031.

- By distribution channel, B2C retail channels dominate with 75.82% market share in 2025, and B2B direct sales from manufacturers demonstrate the strongest growth at 5.39% CAGR through 2031.

- By geography, the Central Region accounted for 30.85% of 2025 revenue; the Western Region is expected to register the fastest 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential real-estate completions and government housing programs | +1.2% | Central and Western regions, with spillover to Eastern | Medium term (2-4 years) |

| Expansion of hospitality & tourism giga-projects driving premium linen demand | +0.8% | Western and Northern regions, concentrated in NEOM and Red Sea corridors | Long term (≥ 4 years) |

| Accelerating e-commerce adoption and omnichannel retail integration | +0.6% | National, with early gains in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| High consumer preference for cotton and natural-fiber comfort in arid climate | +0.4% | National, with stronger preference in Central and Eastern regions | Medium term (2-4 years) |

| Localization incentives and SEZ benefits encouraging domestic textile manufacturing | +0.5% | Eastern and Central regions, focused on KAEC and industrial zones | Long term (≥ 4 years) |

| Growing demand for sustainable & OEKO-TEX-certified home textiles among young consumers | +0.3% | Urban centers in Central and Western regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Real-Estate Completions and Government Housing Programs

Government-backed initiatives such as ROSHN’s 115,000-unit annual pipeline generate predictable procurement cycles for carpets, upholstery, and bed-linen packages PIF.GOV.SA. [1]Zawya, “Landmark Group BCI Cotton Procurement,” zawya.com. Standardized design specifications allow mills to optimize batch production for Saudi climate requirements. Integrated community developments combine housing, retail, and leisure, expanding textile needs beyond pure residential. Quality-oriented build standards drive demand for high-durability fabrics that withstand harsh heat and sand exposure. The Sakani program’s home-ownership incentives to further lift consumer spending on interior refurbishment.

Expansion of Hospitality & Tourism Giga-Projects Driving Premium Linen Demand

NEOM’s luxury resorts and the Red Sea Project create unprecedented premium-linen volumes, prompting suppliers to establish Saudi finishing lines. Design mandates emphasize environmental credentials, encouraging climate-adaptive, low-water fabrics. Hotel operators seek bespoke patterns that reflect local heritage, stimulating demand for custom weaving. Tourism infrastructure extends textile use to airports, museums, and entertainment venues. Procurement scale provides predictability that de-risks capital investment in localized production.

Accelerating E-Commerce Adoption and Omnichannel Retail Integration

Mada card online transactions expanded 25% y/y, while 30% of regional shoppers rely on on-demand delivery each week. IKEA’s partnership with Tamara lifted conversion by 15% and average order value by 40%. Digital channels let brands bypass wholesalers and capture margin, aided by Landmark Group’s Logistiq, which handles 20,000 daily shipments. Same-day fulfillment extends reach into secondary cities, raising overall market penetration. Social-commerce integration with localized content enhances shopper engagement in Arabic-language platforms.

High Consumer Preference for Cotton and Natural-Fiber Comfort in Arid Climate

Cotton’s breathability suits 45 °C summers, leading 45% of Middle Eastern consumers to pay more for eco-friendly options. Moisture-wicking properties enhance indoor comfort during prolonged air-conditioner use. Younger Saudis link natural fibers to wellness, reinforcing premium-positioning strategies. Water-soft finishing improves hand-feel and extends product life in hard-water laundering. Climate-specific UV inhibitors maintain fabric colorfastness despite intense solar radiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global cotton prices and import dependency | -0.7% | National, with higher impact on manufacturers in Eastern and Central regions | Short term (≤ 2 years) |

| Stringent SASO conformity and lab-testing requirements raising compliance costs | -0.5% | National, affecting all importers and manufacturers | Medium term (2-4 years) |

| Rising labor costs due to Saudization quotas impacting margins | -0.4% | National, with concentrated impact on manufacturing facilities | Medium term (2-4 years) |

| Water-scarcity-driven environmental regulations on processing & finishing plants | -0.3% | Eastern and Central regions, affecting textile processing facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Global Cotton Prices and Import Dependency

Projected global output of 26 million tons versus 25.7 million tons consumption tightens supply and elevates price risk for Saudi buyers. Imports face currency and freight swings that compress margins in price-sensitive carpet lines. Manufacturers diversify into blends and man-made cellulosic to mitigate exposure. Hedging via futures markets remains limited due to low regional liquidity. Cost pass-through is constrained by promotional pricing in hypermarkets, squeezing retailer profits.

Stringent SASO Conformity and Lab-Testing Requirements Raising Compliance Costs

SABER certification costs SAR 402.50 (USD 108) per shipment and must be renewed annually [2]Public Investment Fund, “ROSHN Annual Residential Delivery Targets,” pif.gov.sa. SMEs allocate higher revenue shares to testing than global peers, impeding product-refresh cycles. Laboratory bottlenecks during Ramadan and back-to-school peaks elongate lead times. Non-compliance incurs port demurrage charges and potential re-export penalties, raising landed costs. Alignment with EU REACH eases dual-market exports yet adds chemical-reporting overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Carpet Dominance Drives Volume Growth

Carpets and area rugs generated 38.94% of 2025 revenue, reflecting cultural preferences for floor coverings and air-conditioned indoor lifestyles. Upholstery is forecast to compound at 6.12% through 2031 as Saudi consumers shift toward sofas and armchairs in open-plan living areas. Commercial hotel corridors require high-traffic tufted carpets with soil-resistant treatments, creating volume opportunities. Bed-linen sales track the Saudi Arabia home textiles market size projection, supported by affordable housing handovers. Kitchen-linen demand stabilizes as restaurant expansion moderates after pandemic recovery. The Saudi Arabia home textiles market remains volume-led in carpet grades but value-led in premium upholstery SKUs.

Consumer migration from majlis floor seating to sectional sofas elevates per-home textile spend. NEOM resorts specify wool-rich Wilton carpets with marine-grade backings to combat coastal humidity . Bulk orders smooth factory utilization for regional power-loom clusters. E-commerce promotions leverage augmented-reality floor planners, raising online conversion in rug categories. Local weavers explore recycled-polyester yarns to secure public-sector green-procurement wins.

By Material: Synthetic Fibers Lead Despite Natural Growth

Synthetic fibers held a 51.05% share in 2025, buoyed by price and stain-resistance demanded by family households. Natural alternatives like wool, hemp, and bamboo are set for a 5.19% CAGR, outpacing the total market but from a lower base. Cotton remains the climate-comfort benchmark and underpins the Saudi Arabia home textiles market size for bed and bath segments. Polyester microfiber dominates budget duvet sales in value retailers; viscose-linen blends gain traction in aspirational loft-living concepts.

Landmark Group’s Better Cotton uptake anchors supply-chain sustainability, enabling green-label storytelling . Man-made staple fiber producers in Jubail evaluate downstream spinning to localize feedstock. Linen’s thermo-regulation appeals to penthouse buyers in Riyadh’s King Abdullah Financial District, supporting premium pricing. SASO compliance assures toxin-free azo-dye use across both natural and synthetic streams, maintaining consumer trust.

By End-User: Commercial Segment Accelerates Growth

Residential retained a 67.25% share in 2025, fueled by home-ownership incentives under Sakani. Commercial demand is projected to rise at a 5.48% CAGR through 2031, benefiting from hotel pipelines and Grade-A office towers in Riyadh, Jeddah, and NEOM. Healthcare infrastructure adds antimicrobial curtain and bedding requirements, widening product scope.

ROSHN’s master-planned communities include neighborhood malls that specify flame-retardant drapery, expanding the Saudi Arabian home textiles market share for contract-grade suppliers. Corporate workspace re-design post-pandemic prioritizes acoustical soft panels and modular rugs, deepening value per square meter. Government grants on tourism assets under the Tourism Development Fund accelerate linen turnover cycles in beach resorts.

By Distribution Channel: Digital Transformation Reshapes Retail

B2C retail—including hypermarkets, specialty stores, and pure-play e-commerce—captured 75.82% revenue in 2025. Direct B2B sales from mills to hospitality chains are set to grow 5.39% annually as suppliers pursue higher margins. Click-and-collect models flourish in Arabian Centres’ SAR 1.8 billion Jawharat Al-Riyadh mall, linking online orders to in-store pickup.

IKEA’s BNPL integration lifted conversion, signaling the Saudi Arabia home textiles market’s readiness for alternative payments. Marketplace sellers leverage Fulfilled-by-Noon hubs to reach Tier-2 towns in the Southern Region. Specialty boutiques curate heritage-pattern cushions for Hajj visitors in Makkah, preserving cultural motifs. B2B portals integrate SASO e-document uploads to accelerate customs clearance, shortening project lead times for hotel pre-opening teams.

Geography Analysis

The Central Region generated 30.85% of 2025 revenue, anchored by Riyadh’s government spending and headquarters-relocation program. Diriyah Gate’s mixed-use upscale district boosts linen demand for boutique hotels and serviced apartments. ROSHN’s SEDRA community phases increase carpet volumes as each tranche is handed over. Retail modernization, supported by Riyadh Front’s expansion, positions the city as a distribution hub for the broader Saudi Arabia home textiles market.

The Western Region is projected to record a 6.74% CAGR to 2031, underpinned by Red Sea coastal resort openings and Jeddah’s port-enabled import logistics. NEOM’s Desert Rock eco-lodge requires high-specification organic cotton, catalyzing niche suppliers. Makkah’s religious pilgrim traffic demands rapid-turnover bedding and bath linen in budget hotels, lifting unit volumes. Jeddah Central redevelopment includes retail promenades that favor lifestyle-oriented textile storefronts.

The Eastern, Northern, and Southern regions collectively contribute the remaining share but hold strategic value. Jubail’s petrochemical base supports polyester feedstock, promoting localized fiber production. King Abdullah Economic City’s SEZ framework lures weaving and finishing investors with duty-free re-export incentives. The Northern Region benefits from NEOM spillover, requiring worker-camp bedding for 100,000 laborers during peak construction. The Southern Region leverages cross-border trade with Yemen, sustaining traditional patterned fabric sales.

Competitive Landscape

The Saudi Arabian home textiles market is moderately fragmented. Landmark Group’s Home Centre operates 61 domestic stores and plans 40 additional outlets by 2028, backed by a USD 1 billion capex plan. Alsulaiman Group aims to triple IKEA locations to 30 and expand Circle K convenience stores to 300, deepening omnichannel reach.

Localization strategies gain traction as Al-Ahsa-based Arabian Home Textiles installs a 2-million-meter dyeing line financed by the National Development Fund. International entrants partner with local distributors to navigate SASO compliance; Zara Home leverages Fawaz Alhokair’s retail infrastructure for rapid rollouts. Technology adoption centers on RFID inventory tracking and AI-driven demand planning, improving on-shelf availability by 8% for leading chains.

Sustainability is emerging as a key differentiator. IKEA targets 100% renewable-energy sourcing for its Saudi operations by 2027, while Home Centre introduces a recycled-polyester sofa range made from 400 million PET bottles. Competitive intensity is further heightened by BNPL providers funding consumer purchases, effectively expanding addressable demand without retailer margin dilution.

Saudi Arabia Home Textile Industry Leaders

Al Abdullatif Industrial Investment Co.

IKEA – Ghassan Ahmed Al Sulaiman Furniture Co.

Home Centre (Landmark Group)

Al Sorayai Group

Al Mutlaq Furniture (Homeworks, Ethan Allen franchise)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: National Water Company completed SAR 1.6 billion infrastructure upgrades in Makkah, enhancing industrial water security for textile processors.

- June 2025: The Public Investment Fund unveiled the Accelerated Manufacturing Program to scale domestic textile capacity, offering low-interest financing to machinery buyers.

- March 2025: Diriyah Company partnered with Alshaya Group to allocate 566,000 m² of lifestyle-retail GLA, including multiple home-furnishing flagships.

- November 2024: Landmark Group announced a USD 1 billion investment plan spanning three years. The plan aims to launch 400 new stores across the GCC, India, and Southeast Asia. Notably, the VIVA grocery brand will debut in Saudi Arabia in 2025, alongside an expansion of Home Centre operations.

Saudi Arabia Home Textile Market Report Scope

Home textiles are fabrics and clothes used specifically for furnishing a residence. The materials and design of each are defined by the functional and aesthetic uses of each. A complete background analysis of the Saudi Arabia Home Textile Market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and logistics spending by the end-user industries, is covered in the report. Saudi Arabia Home Textile Market is Segmented By Product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery and Floor Covering), and By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online and Other Distribution Channels). The report offers market size and forecasts for Saudi Arabia Home Textile Market (In USD Million) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Local Mom and Pop Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct from the Manufacturers |

By Region

| Central Region (Riyadh & Surroundings) |

| Western Region (Makkah & Jeddah Corridor) |

| Eastern Region (Dammam & Khobar) |

| Northern Region |

| Southern Region |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Local Mom and Pop Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct from the Manufacturers | ||

| By Region | Central Region (Riyadh & Surroundings) | |

| Western Region (Makkah & Jeddah Corridor) | ||

| Eastern Region (Dammam & Khobar) | ||

| Northern Region | ||

| Southern Region | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia home textiles market?

It is USD 1.42 billion in 2026.

How fast is demand for carpets and rugs growing?

Carpets already lead with 38.94% share and continue steady volume gains from housing deliveries.

Which region is expanding quickest?

The Western Region is projected to grow at a 6.74% CAGR through 2031 thanks to tourism mega-projects.

How will localization policies affect sourcing?

SEZ incentives and local-content quotas encourage mills to establish domestic production lines for higher bid preference.

What is the major compliance hurdle for importers?

All textile SKUs must obtain annual SABER certification under SASO's Technical Regulation, adding testing fees and lead-time.

Are consumers willing to pay premiums for sustainable fabrics?

Yes; 45% of Middle Eastern shoppers would pay more for eco-friendly products, driving uptake of OEKO-TEX-certified lines.

Page last updated on: