Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

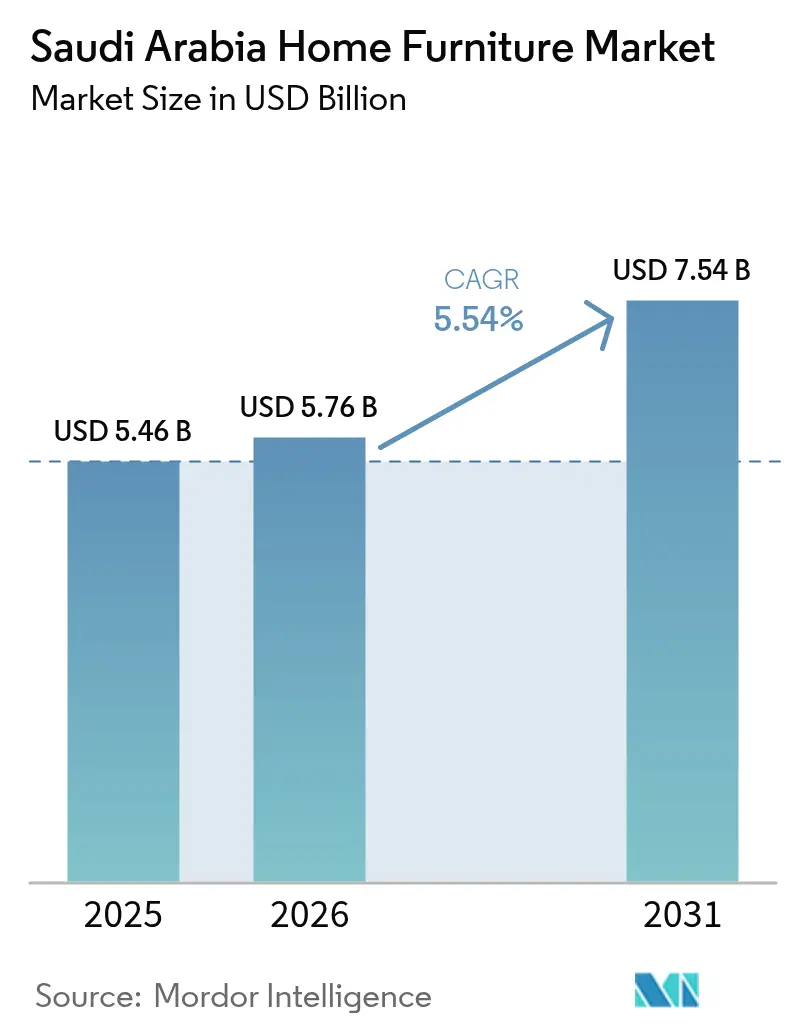

| Base Year Market Size (2025) | USD 5.46 Billion |

| Market Size (2026) | USD 5.76 Billion |

| Market Size (2031) | USD 7.54 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

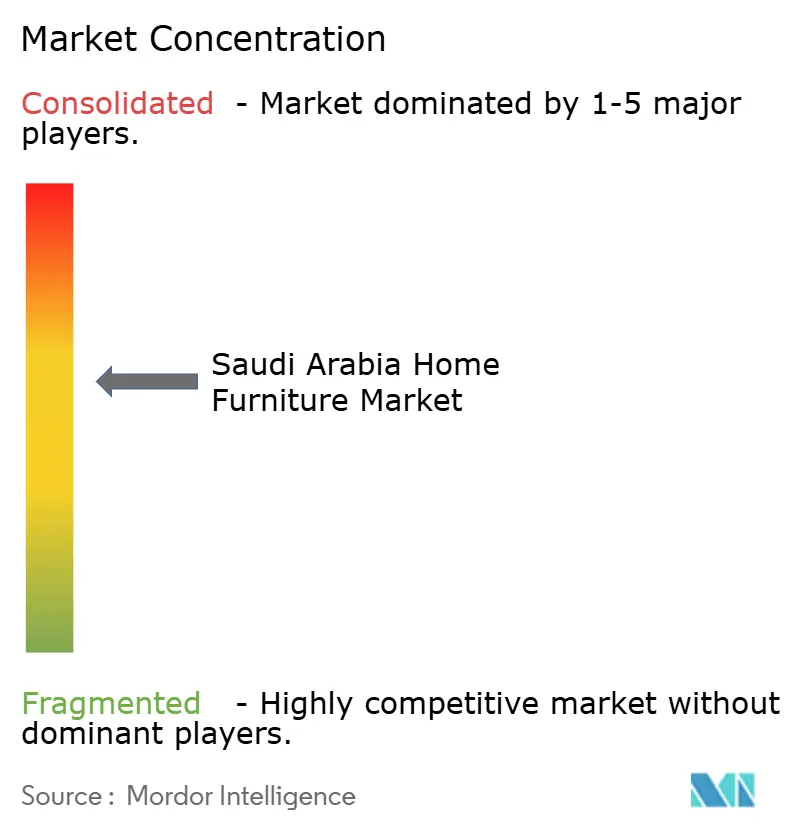

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Home Furniture Market Analysis by Mordor Intelligence

The Saudi Arabia home furniture market size is expected to grow from USD 5.46 billion in 2025 to USD 5.76 billion in 2026 and is forecast to reach USD 7.54 billion by 2031 at 5.54% CAGR over 2026-2031. Sustained residential construction linked to Vision 2030 is triggering bulk purchases of complete room sets, while premiumization trends accelerate as disposable incomes rise. Specialty retail dominates today’s sales but digital channels are expanding quickly, encouraged by 99% internet penetration and mobile-centric shopping habits. Material innovation is gathering pace because extreme summer heat forces suppliers to develop UV-resistant outdoor furniture and climate-robust plastics. Competitive intensity is heightened by localization incentives that reward domestic production through financing and procurement preferences.

Key Report Takeaways

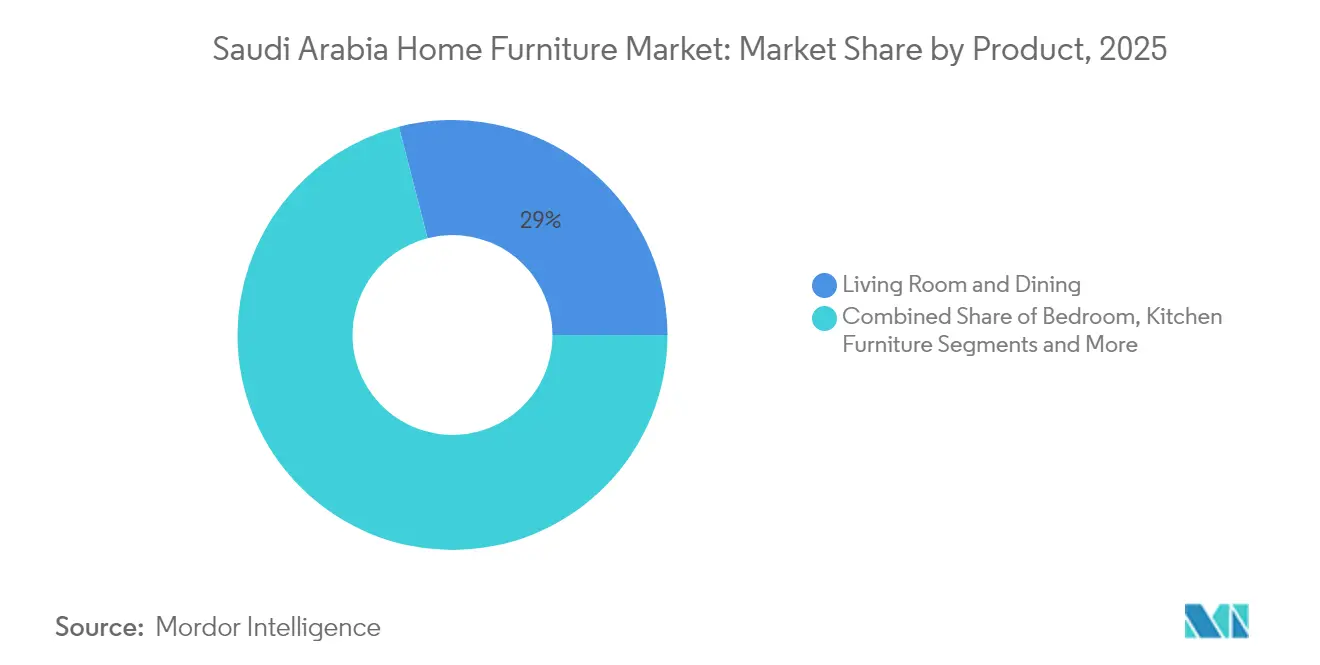

- By product category, Living Room and Dining Room Furniture held 29.01% of Saudi Arabia home furniture market share in 2025, whereas Kitchen Furniture is forecast to expand at a 6.39% CAGR through 2031.

- By material, wood products captured 66.02% share of the Saudi Arabia home furniture market size in 2025, while plastic & polymer furniture is poised for 5.74% CAGR to 2031.

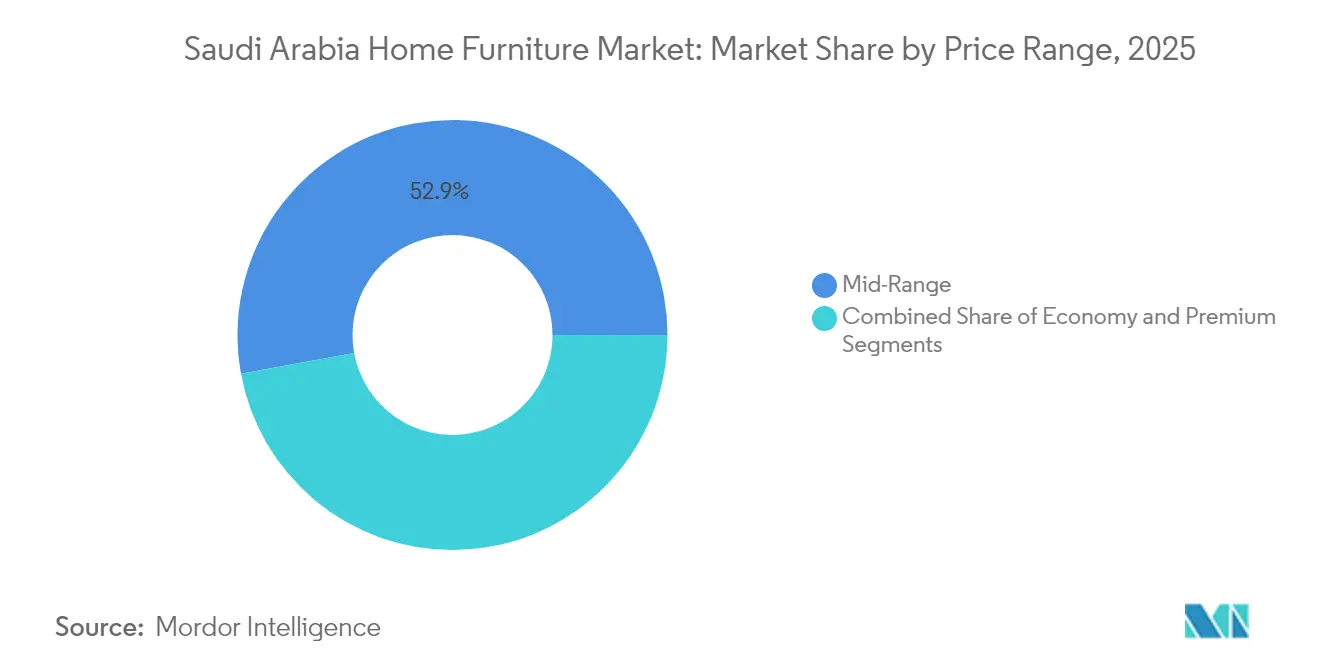

- By price range, the mid-range segment commanded 52.88% share of the Saudi Arabia home furniture market size in 2025; premium furniture is projected to grow at 6.03% CAGR to 2031.

- By distribution channel, specialty furniture stores led with 44.92% revenue share in 2025, yet online sales represent the fastest trajectory with a 7.05% CAGR through 2031.

- By geography, the Western Region accounted for 27.31% of Saudi Arabia home furniture market share in 2025, whereas the Central Region is advancing at the highest 6.61% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030-driven residential real-estate boom | +1.8% | National, concentrated in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| Rising disposable income and shifting lifestyle preferences | +1.2% | Urban centers, Western and Central regions | Medium term (2-4 years) |

| Expansion of e-commerce and last-mile delivery networks | +0.9% | National, with early gains in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| Hospitality build-out for tourism and religious pilgrimages | +0.7% | Western Region (Makkah, Madinah), Red Sea coastal areas | Medium term (2-4 years) |

| Modular, multi-functional designs suiting high expat churn | +0.5% | Eastern Province, Riyadh business districts | Short term (≤ 2 years) |

| "Made-in-Saudi" localization incentives for furniture plants | +0.4% | Industrial zones in Central and Eastern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030-Driven Residential Real Estate Boom

Housing commitments underpin the Saudi Arabia home furniture market, with one million new homes scheduled before 2030 and ROSHN alone targeting 400,000 units. Transaction data show Riyadh villas representing 53.3% of residential sales, creating outsized demand for large living-room sets and bespoke interiors. The New Murabba downtown plan adds 104,000 apartments, while NEOM’s The Line anticipates nine million occupants whose initial fit-outs will be phased over a decade. New homeowners typically furnish entire dwellings within 12-18 months, locking in several spending waves for sofas, beds, cabinets, and kitchen systems. Mega-project timetables thus act as reliable demand indicators for manufacturers and retailers.

Rising Disposable Income and Shifting Lifestyle Preferences

Consumer spending is growing at a 6.4% compound pace to 2028, and millennials 27% of the population, display strong preferences for both traditional majlis-style pieces and sleek modern lines[1]Source: Saudi Central Bank, “Household Consumption Data 2024,” sama.gov.sa. Luxury demand is moving beyond Riyadh into secondary cities, supported by 85% smartphone-based research and widespread buy-now-pay-later adoption. Multi-functional living arrangements are commonplace, with 80% of households expecting furniture to accommodate work, study, and entertainment. Local brands now integrate wireless chargers, USB ports, and app-enabled lighting into tables and wardrobes, bridging technology and décor. These shifts enlarge margins for suppliers that can meet quality aspirations without abandoning heritage design cues.

Expansion of E-Commerce and Last-Mile Delivery Networks

Digital furniture revenue tripled for IKEA Saudi Arabia between 2021 and 2024 after stores were re-engineered as fulfillment hubs[2]Source: IKEA Saudi Arabia, “Digital Commerce Growth Report,” ikea.com. National e-retail penetration could reach 46% by 2030 as logistics partners introduce temperature-controlled warehousing and AI route optimization. Tamara’s “Split in 6” option has removed sticker-shock for mid-range buyers and lifted average order value by double digits. Augmented-reality room planners have cut product return rates because shoppers preview scale and color before checkout. Persistent challenges include 40% delivery failure in remote zones, yet drone pilot programs and parcel lockers are showing early promise in shrinking last-mile costs.

Hospitality Build-Out for Tourism and Religious Pilgrimages

Saudi Arabia plans 362,000 additional hotel keys by 2030, underpinning more than USD 110 billion in hospitality investment[3]Source: Hospitality Net, “Saudi Arabia Hotel Pipeline Update 2025,” hospitalitynet.org. Hotel room revenue climbed 3.5% year-on-year to USD 5.6 billion during the first ten months of 2024, with weekday occupancy in Riyadh averaging 70%. Religious tourism remains pivotal: Makkah and Madinah together welcome over 17 million pilgrims annually, demanding resilient, easy-to-clean furniture for high-turnover accommodations. Mega-resort projects such as the Red Sea Development will require marine-grade outdoor pieces and premium beachfront suites. Supplier showings at the 2024 Riyadh Hotel and Hospitality Expo doubled compared with 2023, signaling broad procurement cycles ahead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive mid-income consumer segment | -0.8% | National, pronounced in secondary cities | Medium term (2-4 years) |

| Import-linked logistics cost volatility | -0.6% | National, affecting port cities primarily | Short term (≤ 2 years) |

| Limited professional interior-design penetration beyond Tier-1 cities | -0.4% | Secondary and tertiary cities | Long term (≥ 4 years) |

| Extreme-heat durability challenges for outdoor SKUs | -0.3% | National, intensified in central desert regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Mid-Income Consumer Segment

Half of Saudi shoppers have trimmed discretionary expenditure and frequently delay furniture purchases until discounts emerge. The tendency is sharper in smaller cities where household budgets are tighter and upscale showrooms rare. Ready-to-assemble items built from particle board now out-sell solid wood within the economy tier because they halve upfront price. Retailers offset margin erosion through value engineering, payment plans, and bundled delivery services. Over the medium term, modest wage growth may temper this restraint but cost transparency will remain central to conversion.

Import-Linked Logistics Cost Volatility

Furniture imports still dominate supply, and tariffs raised in 2020 raised landed costs, while fuel price fluctuations pushed shipping charges up 20% between 2022 and 2024. Port congestion can add three weeks to customs clearance, complicating project timelines for hotels and residential towers. Businesses holding minimal inventory face stock-outs whenever container availability contracts, forcing emergency airfreight that erodes profit. Currency swings against the U.S. dollar further muddy budgeting for Italian and Chinese furnishings. Government efforts to scale domestic capacity through the Saudi Industrial Development Fund are aimed at reducing this volatility but will take years to mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Social Spaces Sustain Largest Slice of Demand

Living Room and Dining Room Furniture retained 29.01% of Saudi Arabia home furniture market share in 2025, anchored by cultural traditions of extended family gatherings. Premium sofas, sectional seating, and carved wood tables dominate villa purchases, while compact apartment layouts in Jeddah spur interest in modular dining sets that double as work desks. Kitchen Furniture is projected to post the highest 6.39% CAGR through 2031, reflecting Vision 2030 standards that promote modern cooking and entertaining spaces. Suppliers such as IKEA have deployed mobile design studios so shoppers in peripheral cities can configure cabinets on-site, accelerating penetration. Bedroom and home-office pieces also advance steadily as hospitality projects and remote-work patterns reorder consumer priorities.

Kitchen Furniture continues to surge because mass-market chains now bundle appliances with cabinetry, making one-invoice packages attractive to new homeowners. Outdoor furniture remains a niche yet fast-emerging segment, with demand rising from resort projects lining the Red Sea coast and municipal greening initiatives that add public seating. Suppliers are experimenting with powder-coated aluminium and weather-proof wicker to counter 120°F summer peaks. Bathroom vanities and storage gain less publicity but underpin replacement cycles whenever households upgrade plumbing fixtures. Together, these categories illustrate the breadth of Saudi Arabia home furniture market requirements.

By Material: Wood Dominance Faces Climate-Driven Substitution

Wood products represented 66.02% of Saudi Arabia home furniture market size in 2025 thanks to perceived durability, warm aesthetics, and easy customization. Yet supply chains lean heavily on imported oak, beech, and teak because domestic forests are sparse; this reliance magnifies exposure to shipping delays and FX shifts. Plastic and polymer furniture is gaining 5.74% CAGR because UV-stable resins offer longevity on balconies and patios that experience relentless sun exposure. Metal frames appear in commercial offices and hospitality back-of-house areas where strength and hygiene trump visual softness. Engineered wood boards such as MDF support the booming ready-to-assemble niche by reducing weight and freight expense.

Innovations are growing at the junction of sustainability and performance: composite boards infused with recycled plastics now tolerate extreme heat better than raw plywood. Luxury resorts experiment with bamboo and rattan to showcase eco-branding, though these materials remain supply-constrained. Fire-safety regulations embedded in the Saudi Building Code have nudged high-rise developers toward flame-retardant laminates and powder-coated steel. Suppliers that certify products under GREENGUARD or FSC standards secure bidding advantages on government projects that prioritize low-VOC finishes. As sourcing diversifies, transparency about origin and testing becomes a decisive purchase factor for institutional buyers.

By Price Range: Mid-Market Dominance, Premium Upswing

Mid-range collections absorbed 52.88% share of Saudi Arabia home furniture market size in 2025, reflecting mainstream budgets backed by subsidized mortgages and government homeowner loans. Retailers position these lines as durable yet affordable, using rubber-wood cores with veneer finishes to balance longevity with price. Premium furniture is expected to grow 6.03% CAGR as wealthy millennials pursue heritage-inspired designs and resort operators commission luxury suites across the Kingdom. At the top end, imported Italian leather sofas and Scandinavian minimalist pieces fetch 30-50% higher margins than mass-produced equivalents. Economy pieces, often flat-packed, retain loyal buyers in student and expatriate segments that value portability.

Financial innovation underpins wider affordability: instalment plans and BNPL services smooth cash-flow, cutting cart abandonment online by up to 15%. Promotional bundles that include delivery, assembly, and extended warranty reduce total cost-of-ownership concerns for cautious households. Growth in co-living and serviced-apartment models pushes landlords toward durable premium SKUs that lower lifecycle costs despite higher initial outlay. Meanwhile, public-sector housing initiatives specify mid-range quality benchmarks to ensure livability without inflating project budgets. The resulting three-tier price ladder sustains healthy inventory turnover across retailer formats.

By Distribution Channel: Showrooms Refocus as Omnichannel Hubs

Specialty furniture stores delivered 44.92% of 2025 sales and continue to anchor discovery, tactile evaluation, and personalized design consultations. Operators now overlay digital appointment scheduling and VR walk-throughs that shorten in-store dwell time while boosting conversion. Online marketplaces are sprinting ahead at 7.05% CAGR and could command one-third of sales by decade-end as mobile checkout becomes frictionless. Home-improvement hypermarkets serve a convenience niche, especially for self-install bookcases, closet systems, and outdoor chairs. Department stores and mass discounters contribute supplementary volume in secondary towns where standalone showrooms are scarce.

Partnerships blur former channel boundaries: Livspace collaborates with big-box retailers so consumers can obtain design, materials, and furniture under one roof. Warehouses adjacent to major highways now double as click-and-collect points, slashing last-mile costs for bulky items. Influencer-led live-shopping events on social media unleash flash sales that liquidate inventory within hours. Saudi Building Code compliance pushes commercial buyers toward distributors that maintain certified documentation on flame-spread ratings and structural loads. As consumer expectations converge around speed, transparency, and service, every channel races to perfect an integrated experience.

Geography Analysis

The Western Region, encompassing Makkah and Madinah, controlled 27.31% of Saudi Arabia home furniture market share in 2025 as religious tourism accelerated hotel construction and apartment refurbishments. Average daily room rates climbed 5% in Madinah, which translated into bulk orders for bedroom suites and lobby seating tailored to rapid guest turnover. The Red Sea Project also stimulates upscale outdoor and marine-grade furnishing demand as beachfront villas break ground. Coastal humidity shapes material choices toward stainless steel and treated hardwoods that resist corrosion. Retailers allocate Ramadan promotions to this region because pilgrim footfall peaks translate into spill-over residential purchases.

The Central Region, led by Riyadh and Qassim, is forecast to post the fastest 6.61% CAGR owing to New Murabba’s 104,000 planned homes and a doubling of Riyadh’s population by 2030. Villa layouts dominate Riyadh, driving sales of large U-shaped sectional sofas and eight-seat dining tables. Qassim benefits from agricultural diversification programs that lift disposable income and retail penetration. Logistics corridors radiating from Riyadh diminish delivery lead-times, supporting same-week installation services demanded by upmarket consumers. Government greening projects that will plant 7.5 million trees also kindle public-space furniture opportunities across parks and boulevards.

Eastern, Southern, and Northern regions combined account for the remaining share but present distinct nuances. Industrial cities in the Eastern Province, such as Dammam, buy durable office furniture for petrochemical and logistics companies, while expatriate compounds opt for modular furnishings that facilitate frequent moves. The Southern highlands of Asir and Jazan are emerging as tourism magnets; IKEA’s 2024 store debuts in Abha and Jazan recorded double-digit first-quarter footfall, evidence of latent demand. NEOM spill-over boosts Tabuk and Al-Jawf, though infrastructure gaps still hinder rapid fulfillment. Climate extremes, dry desert interiors versus humid coasts, require suppliers to segment SKUs carefully by region, reinforcing the complexity but also the resilience of Saudi Arabia home furniture market dynamics.

Competitive Landscape

International, regional, and domestic manufacturers shape a moderately concentrated arena in which the top five players hold roughly half the revenue share. IKEA Saudi Arabia, franchised by Alsulaiman Group, retains category leadership after re-configuring showrooms into omnichannel experience centers and applying Lean Management to cut delivery lead-times by 30%. Home Centre, anchored by Landmark Group, intensifies store upgrades featuring digital kiosks and private-label assortment expansions. Pottery Barn leverages Alshaya’s retail muscle to position premium California coastal aesthetics toward affluent Saudis in Riyadh’s Diplomatic Quarter. Local champion Saudi Modern Factory uses SIDF loans to scale capacity for metal office desks and hospitality wardrobes meeting ISO 9001 standards.

Competitive differentiation increasingly hinges on technology. Retailers deploy AR visualization that overlays furniture scale in a customer’s room using a smartphone, reducing product returns and increasing basket size. Inventory algorithms forecast demand surges tied to public-sector salary disbursement dates, allowing dynamic pricing and promotion. Sustainability remains white space; few brands can certify cradle-to-grave traceability, yet Vision 2030 environmental pillars are pushing tenders to add eco-score weightings. Localization provides both shield and sword: the Made in Saudi emblem attracts patriotic shoppers, but meeting local content thresholds can be capital-intensive for smaller importers. Mergers and distribution alliances are expected as firms chase economies of scale and geographic fill-in.

High-profile corporate actions illustrate momentum. Bentley Home inaugurated flagship boutiques in Riyadh and Jeddah in December 2024, signaling confidence in Saudi luxury appetite. Ashley Furniture entered Buraydah the same month, evidencing penetration of secondary cities. Sedar Global Interiors forged alliances with Armani/Casa and Versace Home to supply turnkey packages for Red Sea resorts. Meanwhile, online pure-play Noon.com enhanced its furniture catalogue by onboarding local manufacturers under fulfilled-by-Noon logistics, promising one-day delivery in Riyadh. Collectively, these moves underscore the relentless evolution of Saudi Arabia home furniture market competition.

Saudi Arabia Home Furniture Industry Leaders

IKEA Saudi

Home Centre

Almutlaq Furniture

Al-Rugaib Furniture

Pottery Barn KSA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Bentley Home opened new stores in Riyadh and Jeddah, emphasizing its luxury interiors expansion in Saudi Arabia.

- December 2024: Hamad M. Alrugaib and Sons Trading Co. added an Ashley Furniture HomeStore in Buraydah, widening branded access in secondary cities.

- September 2024: IKEA Alsulaiman launched outlets in Jazan and Abha and confirmed a Madinah store by year-end as part of its 30-location strategy.

- May 2024: Sedar Global Interiors showcased pergola collections and smart living solutions at Index Saudi, aligning with hospitality megaproject demand.

Saudi Arabia Home Furniture Market Report Scope

Furniture refers to movable objects intended to support various human activities such as seating, eating, and sleeping, to hold objects at a convenient height for work, or to store things. Furniture can be a product of design and is considered a form of decorative art made up of many materials, including metal, plastic, and wood.

The Saudi Arabian furniture market is segmented by type (living room furniture, dining room furniture, bedroom furniture, kitchen furniture, and other types) and by distribution channel (home centers, flagship stores, specialty stores, online stores, and other distribution channels).

The report offers market size and forecasts for the Saudi Arabia furniture market in value (USD) for all the above segments.

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector) |

| Online |

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.) |

By Geography

| Central Region (Riyadh & Qassim) |

| Western Region (Makkah & Madinah) |

| Eastern Region (Dammam, Khobar) |

| Southern Region (Asir, Jazan, Najran) |

| Northern Region (Tabuk, Al-Jawf, Hail) |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector) | |

| Online | |

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.) | |

| By Geography | Central Region (Riyadh & Qassim) |

| Western Region (Makkah & Madinah) | |

| Eastern Region (Dammam, Khobar) | |

| Southern Region (Asir, Jazan, Najran) | |

| Northern Region (Tabuk, Al-Jawf, Hail) |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia home furniture market?

The market is valued at USD 5.76 billion in 2026 and is set to reach USD 7.54 billion by 2031.

Which product category holds the largest share in Saudi Arabia?

Living Room and Dining Room Furniture leads with 29.01% share owing to cultural focus on hospitality spaces.

How fast are online furniture sales growing in the Kingdom?

Online channels are expanding at a 7.05% CAGR, supported by near-universal internet access and BNPL services.

Which region is witnessing the quickest market growth?

The Central Region, anchored by Riyadh, shows the fastest 6.61% CAGR driven by mega-projects like New Murabba.

What is driving premium furniture demand?

Rising disposable income, lifestyle upgrades, and luxury resort developments are pushing premium segment growth at 6.03% CAGR.

Page last updated on: