Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

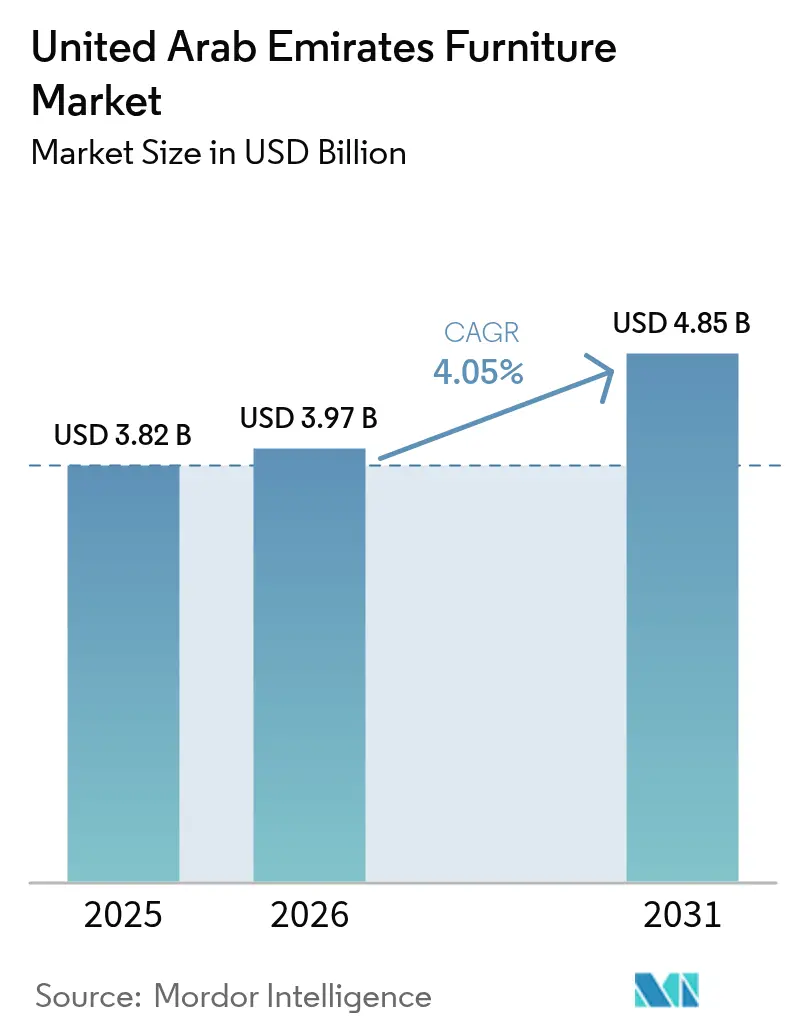

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

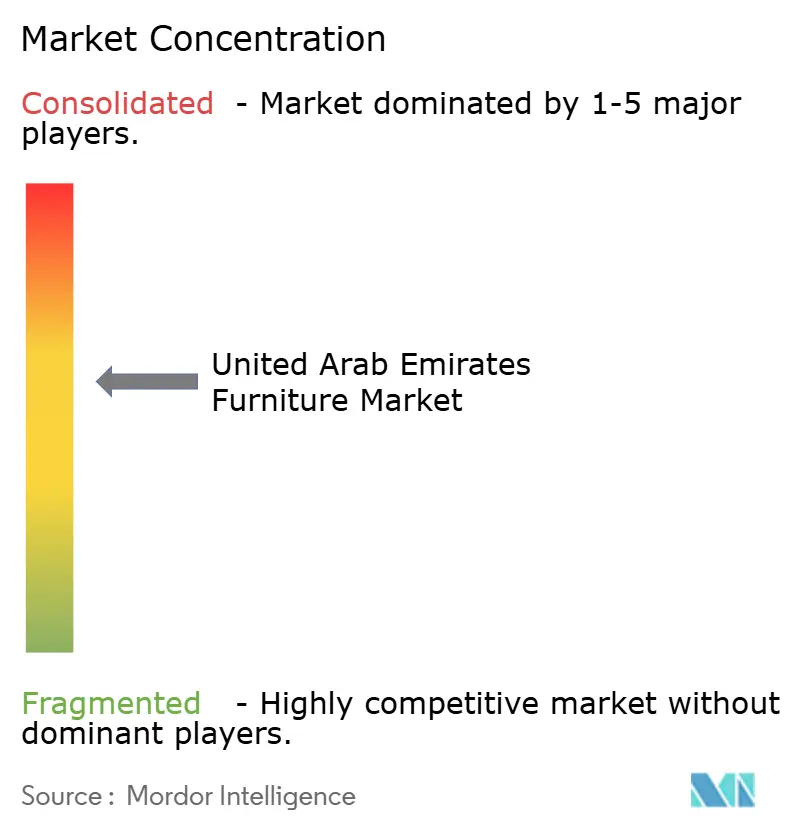

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Furniture Market Analysis by Mordor Intelligence

The UAE furniture market size was valued at USD 3.82 billion in 2025 and estimated to grow from USD 3.97 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). Steady household formation, resilient commercial real-estate activity, and a policy environment that channels disposable income toward home improvements underpin this trajectory. Sustained tourism spending lifts demand for premium hospitality fit-outs, while post-Expo infrastructure keeps renovation pipelines active. Digital retail platforms extend nationwide reach for brands that historically relied on destination showrooms, enabling faster inventory turns and richer consumer data capture. In parallel, “Made in UAE” manufacturing programs nurture local capacity for sustainable furniture and shorten lead times when global supply chains tighten[1]TECOM Group, “Andreu World Unveils UAE’s First Flagship Showroom at Dubai Design District,” tecomgroup.ae. Competitive positioning now revolves around omnichannel convenience, financing partnerships, and circular-economy credentials, with leading retailers investing in smart-home compatible product lines to differentiate.

Key Report Takeaways

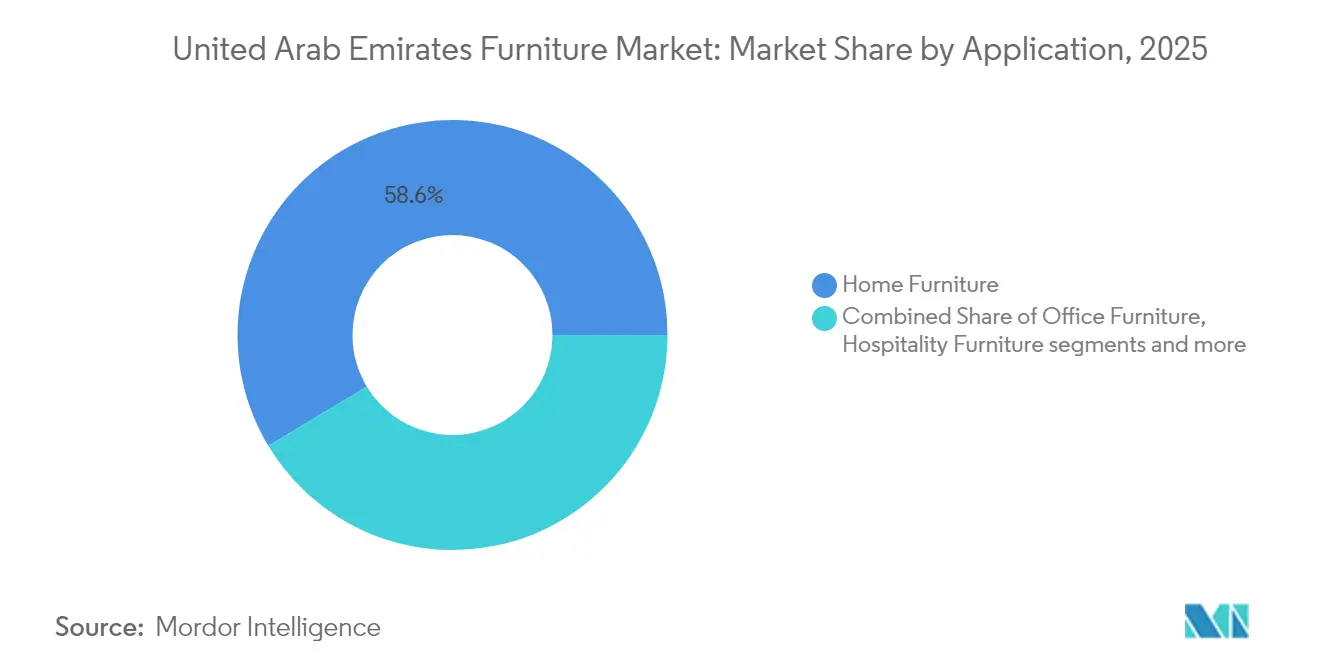

- By application, Home Furniture held 58.62% of the UAE furniture market share in 2025; Hospitality Furniture is forecast to grow at a 5.20% CAGR through 2031.

- By material, Wood captured 47.68% share of the UAE furniture market size in 2025, while Plastic & Polymer is advancing at a 4.65% CAGR to 2031.

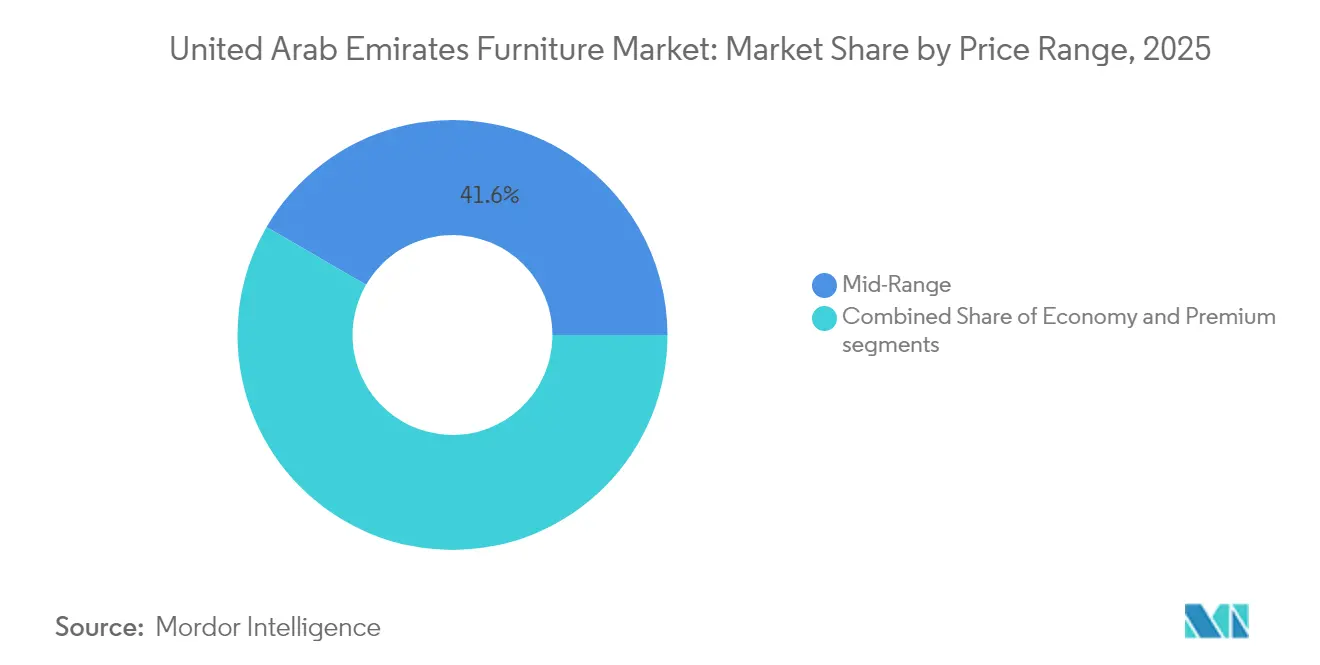

- By price range, the Mid-Range segment commanded 41.63% of the UAE furniture market size in 2025, whereas Premium offerings are projected to expand at a 5.00% CAGR through 2031.

- By distribution channel, B2C/Retail accounted for 66.95% of the UAE furniture market size in 2025 and is pacing the channel growth outlook with a 5.85% CAGR to 2031.

- By geography, Dubai led with a 39.74% UAE furniture market share in 2025; Abu Dhabi is predicted to record the fastest growth at 5.60% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expo 2020 legacy boosts residential & hospitality fit-outs | +0.8% | Dubai primary, spillover to Abu Dhabi | Medium term (2-4 years) |

| Rising mortgage penetration and expat homeownership | +0.6% | Dubai and Abu Dhabi core markets | Long term (≥ 4 years) |

| Government housing grants for Emiratis | +0.5% | Abu Dhabi and Dubai focus | Short term (≤ 2 years) |

| Dubai Design District “Made in UAE” initiatives | +0.4% | Dubai Design District, regional expansion | Medium term (2-4 years) |

| Smart-home adoption is driving modular furniture demand | +0.4% | Urban centers across UAE | Medium term (2-4 years) |

| Circular-economy mandates for hospitality refurbishments | +0.3% | Dubai and Abu Dhabi hospitality zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expo 2020 legacy boosts residential & hospitality fit outs

Expo 2020 converted vast tracts of temporary infrastructure into mixed-use districts that still require continuous furnishing cycles. Developers racing to populate these districts prefer turnkey solutions that meet stringent fit-out timelines and align with Dubai Municipality design approvals. International hotel chains entering the post-Expo pipeline specify bespoke, high-durability pieces to differentiate guest experiences in a competitive hospitality scene. Furniture makers able to demonstrate prior Expo accreditation enjoy shorter vendor-qualification lead times and higher order values. The ripple effect extends to residential buildings that flank legacy sites, where owners upgrade interiors to match the district’s elevated aesthetic. Collectively, these requisitions sustain volume growth for premium and modular lines within the UAE furniture market.

Rising mortgage penetration and expat homeownership

Expanded freehold zones and lender competition have widened mortgage access for expatriates, shifting the consumer psyche from transient rental furnishing to longer-horizon investments. Banks now offer tenors up to 25 years at competitive fixed rates, prompting buyers to prioritize durability, warranty coverage, and smart-home compatibility. Retailers answer with 0% instalment plans bundled with loyalty rewards, reducing out-of-pocket hurdles for big-ticket living-room and bedroom sets[2]Emirates NBD, “0% EPP at Home Centre,” emiratesnbd.com. The move toward ready-to-move-in units accelerates immediate demand for complete furnishing packages rather than staggered purchases. Developers also integrate furniture vouchers into handover promotions, further cementing early-stage procurement. These dynamics keep the UAE furniture market on an upward consumer spending curve as ownership deepens.

Government housing grants for Emiratis

Housing-benefit disbursements act as predictable demand pulses because grants are earmarked for furniture purchases at approved suppliers. The most recent AED 6.75 billion allocation in Abu Dhabi covered 4,356 beneficiaries, each mandated to furnish new homes within a preset window. Retailers holding vendor codes with the Housing Authority see guaranteed order flows and lower receivables risk. Grant rules require itemized quotations, steering beneficiaries toward organized retail formats with transparent pricing rather than informal vendors. Consequently, the grants stabilize quarterly revenue trajectories and provide volume visibility that supports inventory planning across the UAE furniture market.

Dubai Design District “Made in UAE” initiatives

Dubai Design District (d3) positions local manufacturers alongside international designers, reducing reliance on imported finished goods and framing “Made in UAE” as a premium narrative. Flagship showrooms from brands such as Andreu World showcase recycled materials and modular designs, amplifying sustainability awareness. Access to shared prototyping labs lowers entry costs for start-ups experimenting with biodegradable composites and 3D-printed joinery. Government export incentives tied to d3 further motivate capacity expansions that can serve Gulf neighbours. As local production scales, lead times shrink and customization options expand, elevating the value proposition for domestic buyers across both residential and contract markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported timber price volatility | -0.7% | UAE-wide, supply chain dependent | Short term (≤ 2 years) |

| High reliance on expatriate labour amid visa reforms | -0.5% | Manufacturing and retail operations | Medium term (2-4 years) |

| Grey-market e-commerce undercutting branded retailers | -0.4% | Online retail channels nationwide | Short term (≤ 2 years) |

| Limited domestic forestry base restricting backward integration | -0.3% | Manufacturing sector concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported timber price volatility

Two-thirds of the UAE’s fibreboard enters through Thai suppliers, making the cost base sensitive to freight spikes, baht swings, and regional disruptions[3]Vervo Logistics, “Fiberboard: The Most Imported Timber into the UAE,” vervologistics.com. Spot container rates from Laem Chabang to Jebel Ali rose nearly 18% during 2024, eroding gross margins for wood-heavy product lines. Inventory hedging can buffer shocks but inflates working-capital requirements and warehouse overhead. Projects quoting fixed prices months ahead risk negative spreads when shipments are delayed. Some manufacturers swap to fast-growing eucalyptus veneers or engineered bamboo panels, yet these alternatives still rely on imports. Until domestic agroforestry matures, timber volatility will continue to cap near-term price aggressiveness across the UAE furniture market.

High reliance on expatriate labor amid visa reforms

The 2025 labour law revision increased penalties for documentation lapses up to AED 1 million per incident, doubling compliance budgets for firms dependent on foreign carpenters and upholsterers[4]Fragomen, “Stricter Penalties Introduced for Labor Law Violations,” fragomen.com. Sharper audits push employers to invest in digital HR systems and worker accommodation upgrades. Emiratization quotas add a parallel training burden because local talent pipelines for joinery trades remain thin. Wage escalation—driven by competition for limited skilled craft workers—compresses margins, forcing some SMEs to outsource components to lower-cost neighbouring countries. Automation offsets part of the burden, yet high-touch finishing work still demands human expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Furniture anchors consumption while hospitality accelerates

Home Furniture represents 58.62% of the UAE furniture market size in 2025, providing the foundational revenue stream for retailers who continue to expand same-day delivery capabilities in Dubai and Abu Dhabi. Stable household formation and mortgage uptake ensure recurring demand for bedroom sets, sofas, and storage solutions. The segment benefits from structured government grants that funnel orders to registered suppliers, insulating volumes from discretionary cutbacks. Hospitality Furniture, meanwhile, charts a forecast-beating 5.20% CAGR as hotel pipelines revive and refurbishment cycles compress to maintain brand competitiveness. High-touch design briefs that call for modular headboards, acoustic wall panels, and smart-lighting integration reinforce premium pricing leverage in project tenders.

Retailers cross-pollinate learnings between residential and hospitality clients, repurposing modular cabinetry initially developed for hotel suites into urban micro-apartments. Manufacturers prioritize stain-resistant textiles and antimicrobial surface coatings that serve both health-conscious households and high-occupancy hotels. The convergence of residential and hospitality aesthetics manifests in open-plan furniture designs that emphasize space efficiency and multi-functionality, strengthening portfolio coherence across the UAE furniture market.

By Material: Wood leads yet polymers define future flexibility.

Wood holds a 47.68% UAE furniture market share in 2025, anchored by cultural affinity for solid-wood statement pieces and artisanal joinery. Walnut and oak finishes command premium sub-segments, especially in majlis seating and executive desks. Despite wood’s dominance, Plastic & Polymer categories advance at a 4.65% CAGR through 2031, buoyed by the modular-furniture boom and growing demand for moisture-resistant outdoor pieces. Polymer frames accommodate embedded LED strips and wireless chargers, making them ideal for technology-centric households.

Cost volatility in imported lumber motivates producers to substitute engineered polymers where load-bearing requirements allow. Brands market these pieces under sustainability narratives, using recycled ocean plastics and bio-resins to appeal to eco-conscious buyers. Metal continues to serve niche requirements for outdoor dining and commercial lobbies, leveraging powder-coating technologies that extend lifecycle in Gulf climates. Composite materials combining bamboo fibres with polypropylene are in early commercialization, promising strength-to-weight ratios that could disrupt both traditional wood and pure-polymer categories over the next decade.

By Price Range: Premium momentum signals maturing tastes

The Mid-Range band controls 41.63% of the UAE furniture market share, yet the Premium tier posts the strongest outlook at 5.00% CAGR, reflecting willingness to pay for branded craftsmanship and integrated technology. Emirati housing grants alleviate upfront costs, enabling beneficiaries to channel disposable income into higher-grade finishes and custom upholstery. Expatriates drawn into long-term mortgages mirror this behaviour, viewing premium furniture as an asset that tracks property value appreciation.

Retailers showcase aspirational lifestyle vignettes inside experiential zones that let shoppers test smart recliners and adjustable standing desks. Financing options—often interest-free for 12-24 months—reduce sticker shock and expand the addressable audience. Meanwhile, economy lines protect volume by targeting landlords who furnish rental stock on tight budgets. Price-tier migration within the UAE furniture market thus reflects demographic stratification, but shared omni-channel journeys allow retailers to nudge customers upward through targeted promotions.

By Distribution Channel: Digital ecosystems redefine customer journeys

B2C/Retail captured 66.95% of the UAE furniture market size in 2025 and will drive incremental gains through a 5.85% CAGR to 2031 as app-centric discovery supplements showroom footfall. Augmented reality tools allow shoppers to visualize scale and colourways at home, reducing return rates and building purchase confidence. Click-and-collect models shorten delivery cycles for smaller accent items, while big-ticket pieces ship from automated regional fulfilment centres. B2B/Project channels sustain relevance for bulk orders tied to hospitality, office, and governmental projects but encounter elongated tender processes and rigid payment schedules.

Strategic partnerships with buy-now-pay-later providers Tabby and Tamara spur cart conversion among millennials and Gen Z early homeowners. Inventory data feeds into social-commerce integrations, enabling real-time stock visibility during livestream product demos. As e-commerce widens, retailers invest in reverse-logistics capabilities that streamline returns and refurbishment, aligning with circular-economy goals and customer expectations of hassle-free after-sales support across the UAE furniture market.

Geography Analysis

Dubai retains leadership at 39.74% of the UAE furniture market share thanks to its status as a commercial and tourism nexus that continually spawns residential and hospitality fit-out opportunities. Post-Expo precincts such as District 2020 sustain renovation pipelines, while high-net-worth foreign buyers furnish waterfront penthouses with bespoke European collections. The emirate’s design-led ecosystem, anchored by Dubai Design District, nurtures local talent and shortens concept-to-showroom cycles, sustaining product novelty that reinforces consumer engagement.

Abu Dhabi follows with the fastest projected growth of 5.60% CAGR as its housing authority allocates multibillion-dirham benefit packages that translate into immediate furniture procurement. Large-scale mixed-use developments in Al Maryah and Yas islands pair retail promenades with high-density residences, broadening footfall for furniture showrooms. Government partnerships that attract smart-home technology providers shape demand for connectivity-ready furnishings, positioning Abu Dhabi as a test bed for tech-integrated living concepts.

Sharjah, Ajman, and the northern emirates collectively account for a smaller share but register steady gains as industrial land and labour costs encourage manufacturing clusters. IKEA’s Fujairah outlet exemplifies a hub-and-spoke strategy that shortens last-mile delivery to underserved coastal areas. Free-zone incentives lure component suppliers and small-batch producers, gradually building an ecosystem that could offset import dependency. In aggregate, regional diversification balances the UAE furniture market, mitigating concentration risk and spreading economic spillovers beyond the primary emirates.

Regulatory Landscape

Furniture placed on the UAE market is governed by federal product safety and conformity requirements, with the Ministry of Industry and Advanced Technology (MoIAT) acting as the main authority for conformity services and national conformity marks. Federal Law No. (10) of 2018 on Product Safety sets supplier obligations to place safe products on the market, and MoIAT-administered conformity pathways (including certificates for regulated products and licensing for national conformity marks such as the Emirates Quality Mark) apply to manufacturers and importers where the relevant technical requirements cover their product categories.

For cross-border trade, importers also manage customs and indirect taxation under the GCC customs framework, where a commonly applied 5% customs duty on many furniture lines (HS 9403) and a 5% VAT are relevant. Emirate-level schemes can add additional layers, for example through Abu Dhabi Quality and Conformity Council (QCC) programs and product certification pathways used in Abu Dhabi, which can shape vendor qualification for institutional and project procurement.

Value Chain Analysis

The UAE furniture value chain is import-centric, with finished furniture and key inputs sourced overseas and consolidated through the countrys logistics and free-zone ecosystem. Upstream supply includes imported timber panels, fabrics, foams, and hardware, while conversion activities occur through local assembly, upholstery, finishing, and bespoke joinery for hospitality and premium residential projects. Port and logistics infrastructure, especially Jebel Ali, supports containerized inbound flows and re-exports to nearby markets, while duty deferral mechanisms in free zones affect inventory positioning and cash cycles.

Downstream, organized retailers and omnichannel specialists distribute via large-format showrooms, compact mall stores, and online channels supported by fulfillment, last-mile delivery, and installation services. On the project side, contractors, fit-out firms, designers, and procurement agents channel demand from hospitality, office, and government-linked developments, where compliance documentation and lead-time reliability affect supplier selection. In March 2026, the launch of the ADEED supply chain support platform by 7X with Abu Dhabi government entities pointed to deeper public-private coordination around trade facilitation and continuity, which can help improve availability of industrial inputs and reduce disruption risk for local production and project delivery.

Competitive Landscape

The UAE furniture market exhibits moderate fragmentation with established international retailers competing alongside regional players and emerging e-commerce specialists. Global giants such as IKEA leverage brand equity, vertically integrated supply chains, and data-rich loyalty ecosystems to defend market leadership. Recent compact-format stores in Fujairah and Dalma Mall demonstrate adaptive retail footprints that penetrate secondary catchments while keeping inventory optimized. Home Centre counters with an app surpassing 1 million downloads and AI-driven recommendation engines that lift conversion rates, underlining the centrality of digital engagement.

Regional players PAN Home and Danube Home scale through controlled real-estate expansion, large logistics campuses, and private-label product development, collectively pushing omnichannel price competitiveness. Danube Home’s 5 million sq. ft logistics park allows bulk procurement advantages that feed both retail and project divisions, enhancing bid aggressiveness in hospitality tenders. Disruptors tap circular-economy trends via rental and resale platforms; dubizzle reports growing listings in the gently used premium segment as sustainability and affordability converge.

Strategic differentiation now gravitates around sustainability certifications, smart-home compatibility, and value-added services such as 3D space planning. Partnerships with local fabric mills and metalwork ateliers support faster custom orders and fulfil Emiratization objectives. Exclusive distribution deals—exemplified by La-Z-Boy’s tie-up with Dubai Furniture Manufacturing Company—illustrate how foreign brands localize without direct brick-and-mortar investment. Collectively, these manoeuvres keep the competitive field dynamic yet moderately consolidated.

United Arab Emirates Furniture Industry Leaders

IKEA

Danube

Royal Furniture

Home Centre

PAN Emirates

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven product upgrades are creating room for brands that can provide safer, better-documented case goods and indoor-air-quality-aligned materials. Dubai Law No. (3) of 2026 on the Quality and Safety of Buildings codifies a shift toward more unified standards and structured maintenance and repair regimes, which supports demand for traceable specifications and durable, serviceable furniture in managed buildings and refurbishment cycles. Alongside building-led requirements, product safety and liability considerations also push for clearer labeling, Arabic instructions, and tighter attention to emissions performance for engineered wood and upholstered categories, supporting suppliers that can provide test reports, compliant component sourcing, and standardized installation and anchoring solutions for storage furniture.

Premiumization and personalization form a second opportunity band, especially where homeowners and hospitality operators are prioritizing bespoke, design-led interiors instead of generic catalog choices. This shift is visible in the luxury interiors narrative around personalization and long-term value, and in continued investment by organized players in curated store formats and digital tools that support guided selling. The market also offers space for Made in UAE capacity and quick-turn customization that reduces reliance on imported lead times, particularly for hospitality fit-outs and replacement demand where schedule adherence and repeatability matter alongside design.

Recent Industry Developments

- June 2026: IKEA UAE opened a 6,100 sq m expanded New Market Hall at Dubai Festival City and added interactive Ask IKEA digital tools to support assisted shopping. The larger footprint strengthens omnichannel conversion by linking in-store discovery with digital guidance and helps accelerate turnover of core home-furnishing categories in a high-traffic retail destination.

- May 2026: Danube Home unveiled a smart, curated 35,000 sq ft showroom at Festival Plaza, Jebel Ali. The expansion increases brand reach in a major mall corridor and reinforces competitive intensity in mid-range to premium assortments where guided selling, visualization, and faster delivery promises influence purchase decisions.

- December 2024: Abu Dhabi Investment Office signed five manufacturing-related deals spanning HVAC, lighting, and smart-home solutions that support the wider built-environment supply chain. These moves complement furniture demand in project-led developments by strengthening adjacent inputs and systems commonly bundled into residential and hospitality fit-outs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the UAE furniture market is measured as the value of finished furniture sold for residential and non-residential use across the UAE, covering locally made and imported products sold through offline and online channels.

Scope exclusions: We exclude home decor, appliances, building materials, and installation or interior design services even when bundled with fit-out projects.

Segmentation Overview

- By Application

- Home Furniture

- Chairs

- Tables (side, coffee, dressing, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom, outdoor, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas & Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, govt offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B / Project

- B2C / Retail

- By Geography

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and the supply flow before any interviews were run. We relied on public trade and macro series to understand how much furniture enters the country, how fast end markets expand, and how pricing moves across categories.

Sources used include, for example, UAE Federal Competitiveness and Statistics Centre population and household indicators, Dubai Statistics Center construction and hospitality activity data, UN Comtrade and ITC Trade Map import and export series, World Bank macro indicators, and UNIDO industrial statistics where applicable. To connect this with company behavior, we also reviewed annual reports, investor presentations, retailer announcements, and trusted press coverage, then checked selective company financials and import and export shipment-level databases for consistency. The sources listed are illustrative and not exhaustive, and additional public and paid references were consulted for cross-checks, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives buying in the UAE, and then stress testing the desk assumptions with real pricing and volume signals. We spoke with manufacturers, importers, distributors, retailers, project buyers, and fit-out stakeholders across the UAE so the model reflects channel mix shifts, project timing, and category-level price movement.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 45% | Functional/Unit leaders: 29% | |

| Smaller Players: 22% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where import and local production signals are reconciled with UAE demand drivers, then allocated to furniture consumption using category splits and channel shares gathered from public series and interviews. Once the totals were shaped, we used selective bottom-up checks, such as sampled average selling prices by major product groups multiplied by estimated units sold through key channel types, to confirm that the top-line value stays realistic.

Inputs that materially affect the model include new housing handovers and residential move-ins, hotel keys and occupancy trends that impact replacement cycles, office and education project activity, retail sales momentum for home goods, import value by key furniture HS codes, and observed price movement by material type and price range. Where bottom-up visibility is weaker, such as for small workshops and unorganized trading, we used informed share assumptions that were validated through distributor and retailer feedback.

For forecasting, scenario analysis was used because the UAE market is sensitive to project pipelines, tourism swings, and promotional pricing. Assumptions for the base case were anchored to expert views on construction and hospitality activity, expected e-commerce penetration changes, and steady but uneven price progression across categories.

Data Validation & Update Cycle

Outputs are checked in more than one way before sign-off so large jumps do not pass through without explanation. We compare the final market value against independent signals like import trends, construction activity, and channel-level pricing, then investigate variances by category and emirate before totals are finalized.

If an unexpected break is seen, such as a sharp change in import value or a sudden demand shock in hospitality, the team re-contacts sources and reruns the impacted assumptions. Reports are refreshed annually, with interim updates when material events occur, and a final analyst pass is completed close to delivery so clients receive the latest view.

Mordor Intelligence's United Arab Emirates Furniture Market Estimate Compared With Other Published Estimates

Published market sizes for UAE furniture often differ because the scope lines are not drawn the same way, and because pricing and channel mix are treated differently across models. Timing also matters since a study that uses older trade data or pre-update construction assumptions can land at a noticeably different value.

The biggest gaps usually come from whether mattresses, decor, or fit-out services are mixed into the furniture total, and whether values are counted at retail selling price or closer to import and ex-factory value. Another source of spread is how fast average selling prices are assumed to rise in premium categories, along with how online discounting and promotions are reflected, which is corrected through channel checks and current-year import value reconciliation before finalizing the 2025 total in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.82 B (2025) | |

| Trade Journal A | USD 3.40 B (2025) | Often closer to import value and may undercount locally assembled supply and retail markups, which pushes the total down even if unit demand is similar. |

| Regional Consultancy B | USD 4.30 B (2025) | May fold in fit-out scope and adjacent home categories, and may apply faster ASP growth for premium projects without consistent channel level validation. |

The spread in the table is mostly explained by what is counted as furniture and at what price point it is valued. By keeping inclusions clear, tying the total to trade, construction, and channel checks, and then adjusting only where interview feedback supports it, the result stays traceable and repeatable for planning.

Key Questions Answered in the Report

How large is the UAE furniture market in 2026?

It is valued at USD 3.97 billion and is projected to reach USD 4.85 billion by 2031 at a 4.05% CAGR.

Which emirate contributes the most to furniture demand?

Dubai leads with 39.74% share thanks to its tourism hub status and dense real-estate activity.

What segment is growing quickest?

Hospitality Furniture shows the fastest growth at 5.20% CAGR as hotels refurbish post-Expo.

Why are premium furniture sales rising?

Higher disposable incomes, accessible mortgages, and technology integration drive a 5.00% CAGR for premium pieces.

How are retailers tackling supply-chain risks?

They expand local manufacturing, diversify sourcing beyond Thai timber, and invest in automated fulfillment centers.

What role does e-commerce play?

B2C online channels now command 66.95% of spend, aided by mobile apps, AR visualization, and buy-now-pay-later schemes.

Page last updated on: