Home and Property Improvement

27th MayStrategic Expansion in the Russia Laundry Appliances Market

3 Min Read

The Saudi Arabia Kitchen Furniture Market Report is Segmented by Product (Kitchen Cabinets, Kitchen Chairs, Kitchen Tables, Other Products), Material (Wood, Metal, Plastic & Polymer, Other Materials), End-User (Residential, Commercial), Distribution Channel (B2C/Retail, B2B/Project), and Geography (Central, Western, Eastern, Southern, Northern Regions). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

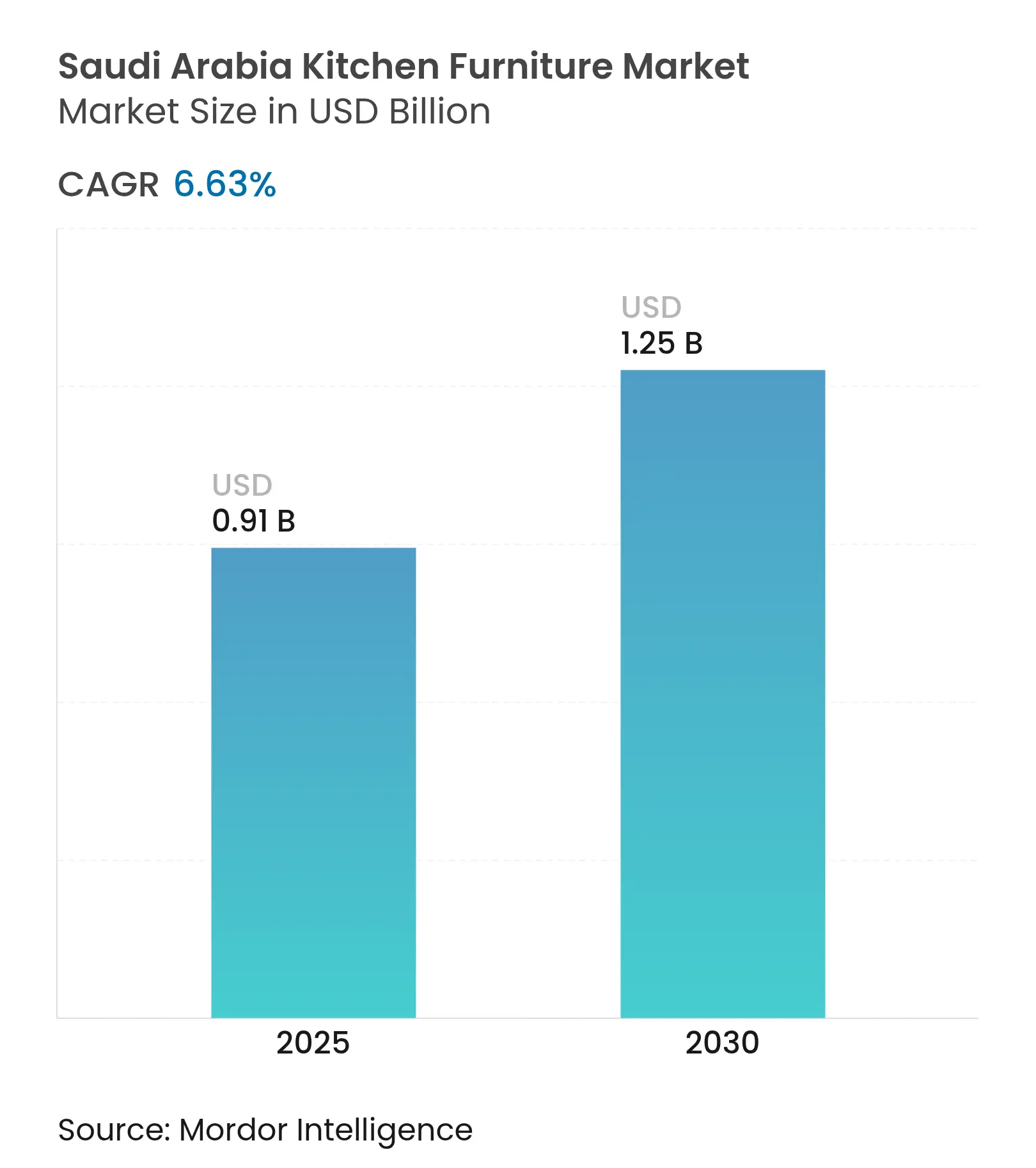

| Market Size (2025) | USD 0.91 Billion |

| Market Size (2030) | USD 1.25 Billion |

| Growth Rate (2025 - 2030) | 6.63 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Saudi Arabia kitchen furniture market size reached USD 903.70 million in 2025 and is projected to climb to USD 1,245.72 million by 2030, reflecting a 6.63% CAGR across the forecast horizon. Current demand is firmly linked to a surge in off-plan residential projects, a mortgage upswing that funded almost 89,000 new home‐financing contracts in 2024, and a hospitality construction spree that is adding 320,000 hotel keys under Vision 2030. Robust public-sector spending on infrastructure keeps contractor pipelines full, while municipal land reforms in Riyadh and Jeddah enlarge the pool of first-time owners who must fit out kitchens from scratch. Parallel to these macro factors, retail digitalization, BNPL adoption, and two-hour delivery commitments reshape buying journeys and reduce friction for big-ticket purchases. Suppliers that preload smart-appliance cut-outs, meet Saudi Building Code 2024 energy guidelines, and hold verifiable local-content certificates enjoy preferred-vendor status with both developers and government buyers, positioning them to capture an accelerating share in the Saudi Arabian kitchen furniture market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid urban-residential pipeline

Rapid urban-residential pipeline

| +1.8 | Nationwide, the highest in Riyadh and Jeddah | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8

|

Geographic Relevance

:

Nationwide, the highest in Riyadh and

Jeddah

|

Impact Timeline

:

Medium term (2-4 years)

|

Premiumization and modular adoption

Premiumization and modular adoption

| +1.2 | Central and Western regions | Medium term (2-4 years) | |||

Energy-efficient appliance integration

Energy-efficient appliance integration

| +0.9 | National | Long term (≥4 years) | |||

E-commerce and omni-channel retail

E-commerce and omni-channel retail

| +0.7 | Digitally enabled metro areas | Short term (≤2 years) | |||

Vision 2030 hospitality mega-projects

Vision 2030 hospitality mega-projects

| +1.1 | Western and Northern regions | Long term (≥4 years) | |||

Rise in female homeownership

Rise in female homeownership

| +0.6 | National | Short term (≤2 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Urban-Residential Pipeline

Over 205,000 off-plan units received licenses in 2024 as Riyadh’s northern corridors alone unlocked 81.48 km² for development with plots capped at SAR 1,500 per m²[1]Ministry of Municipal, Rural Affairs and Housing, “Updated Requirements for Construction of Residential Buildings,” momrah.gov.sa. Developers such as Roshn load procurement schedules with multi-phase orders that cover cabinets, countertops, and smart hood wiring, locking in multi-year demand for participants in the Saudi Arabia kitchen furniture market. The Real Estate Development Fund’s SAR 62.9 billion financing outlay in 2024 provided liquidity for thousands of middle-income households, transforming latent interest into contracted kitchen packages. Installers report cycle times of under five working days from measurement to handover, thanks to prefabricated modules that slot into standard footprints specified in master plans. These dynamics convert one-off retrofit purchases into repeatable new-build streams, strengthening volume predictability for factory planners and encouraging machinery upgrades that raise local value-add.

Premiumization and Modular Adoption

Trump-branded towers in Jeddah and villa clusters in AMAALA stipulate high-end finishes, while the cabinet carcasses must still arrive in synchronized batches to meet MMC build speeds that shorten schedules up to 30%[2]Frontiers in Sustainable Cities, “Sustainability Assessment of Modern Method of Construction,” frontiersin.org. Consumer tastes are also shifting upward as disposable incomes rise; buyers routinely ask for quartz worktops, integrated lighting strips, and concealed wireless chargers. Smart-home backbone wiring is becoming a de facto specification, prompting cabinetmakers to pre-drill conduit passages for data cables and to reinforce panels supporting motorized lift systems. Local manufacturers now offer “click-fit” box systems that allow late-stage customization of handles, color fronts, and corner accessories without disrupting the factory rhythm. The Saudi Arabia kitchen furniture market benefits as modularity lowers the cost of upgrades and creates a long tail of accessory demand after core installations.

Energy-Efficient Appliance Integration

Saudi Building Code 2024 (SBC 601/602) forces all new residential kitchens to meet tougher kWh benchmarks, steering buyers toward appliances that communicate data to smart meters. LG’s built-in line, launched in December 2024, is tailored to local voltage and ambient heat profiles and comes with IoT modules that pair with popular Saudi home-automation apps. Cabinet designers must guarantee proper vent clearances, reinforce frames for heavier insulation layers, and provide service hatches for in-wall monitoring devices. Lenders now evaluate energy-performance documentation during credit appraisal, creating a sales narrative that links efficient cabinetry layouts to lower household utility outgo. Manufacturers that issue certified U-value reports for door-panel assemblies see faster approvals from Vision Bank green-finance schemes, giving them a pricing edge in the Saudi Arabia kitchen furniture market.

E-Commerce and Omni-Channel Retail Boom

Household e-commerce spending is forecast to top USD 17 billion in 2025, with furniture and homeware taking a 12.2% slice. Retailers embed virtual-reality walkthroughs that let buyers visualize cabinet lines against developer floor-plan PDFs. Two-hour delivery promises in Riyadh relieve micro-fulfilment hubs that stock fast-moving widths and color fronts, allowing on-site teams to complete assembly the same evening. Payment friction has eased; BNPL services report kitchen basket conversions 35% higher than for cash-on-delivery. Social-commerce influences livestream unboxing of flat-packed pantries, triggering flash-order spikes that route to the nearest store for curbside pick-up. The omni-channel flywheel therefore widens reach, trims marketing costs, and compresses cash conversion cycles inside the Saudi Arabia kitchen furniture market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile timber and plywood prices

Volatile timber and plywood prices

| –0.8 | Nationwide—import-dependent factories are most exposed | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

–0.8

|

Geographic Relevance

:

Nationwide—import-dependent factories are most exposed

|

Impact Timeline

:

Short term (≤ 2 years)

|

Fragmented informal joinery

Fragmented informal joinery

| –0.6 | Dense metro neighborhoods | Medium term (2-4 years) | |||

Skilled cabinet-maker shortage

Skilled cabinet-maker shortage

| –0.5 | Kingdom-wide, acute in growth corridors | Medium term (2-4 years) | |||

Lengthy permits for remodels

Lengthy permits for remodels

| –0.3 | Select municipalities | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Timber and Plywood Prices

Landed plywood costs swung more than 25% within six months of 2024, even as import volumes rose, forcing weekly quotation updates by mid-sized plants. Hedging is costly because suppliers typically import mixed species of cargoes, making standardized futures contracts impractical. Manufacturers dilute risk by shifting toward melamine-faced MDF or by promoting aluminum-frame doors clad in thinner wood veneers. Sudden cost spikes ripple into retail shelves, causing booking deferrals and complicating project-budget approvals. Government reforestation programs will nurture domestic supply in the long run, yet immediate volatility remains a drag on margins within the Saudi Arabian kitchen furniture market.

Fragmented Informal Joinery

Home-garage shops and pop-up social-commerce sellers sidestep licensing, wage regulations, and tax reporting, enabling offer prices 15-25% below formal players[3]Balady Platform, “Commercial Registration Regulations,” balady.gov.sa. Customers attracted by low pricing often forego warranties, and inspectors report non-compliant glues exceeding VOC limits. Digitized inspection scheduling is tightening the net, but many micro-operators relocate quickly to avoid fines. Formal brands must invest in consumer-awareness campaigns stressing safety certificates and after-sales support, lifting overheads in a price-sensitive landscape. The unorganized footprint thus erodes volume potential for compliant suppliers in the Saudi Arabia kitchen furniture market until enforcement catches up.

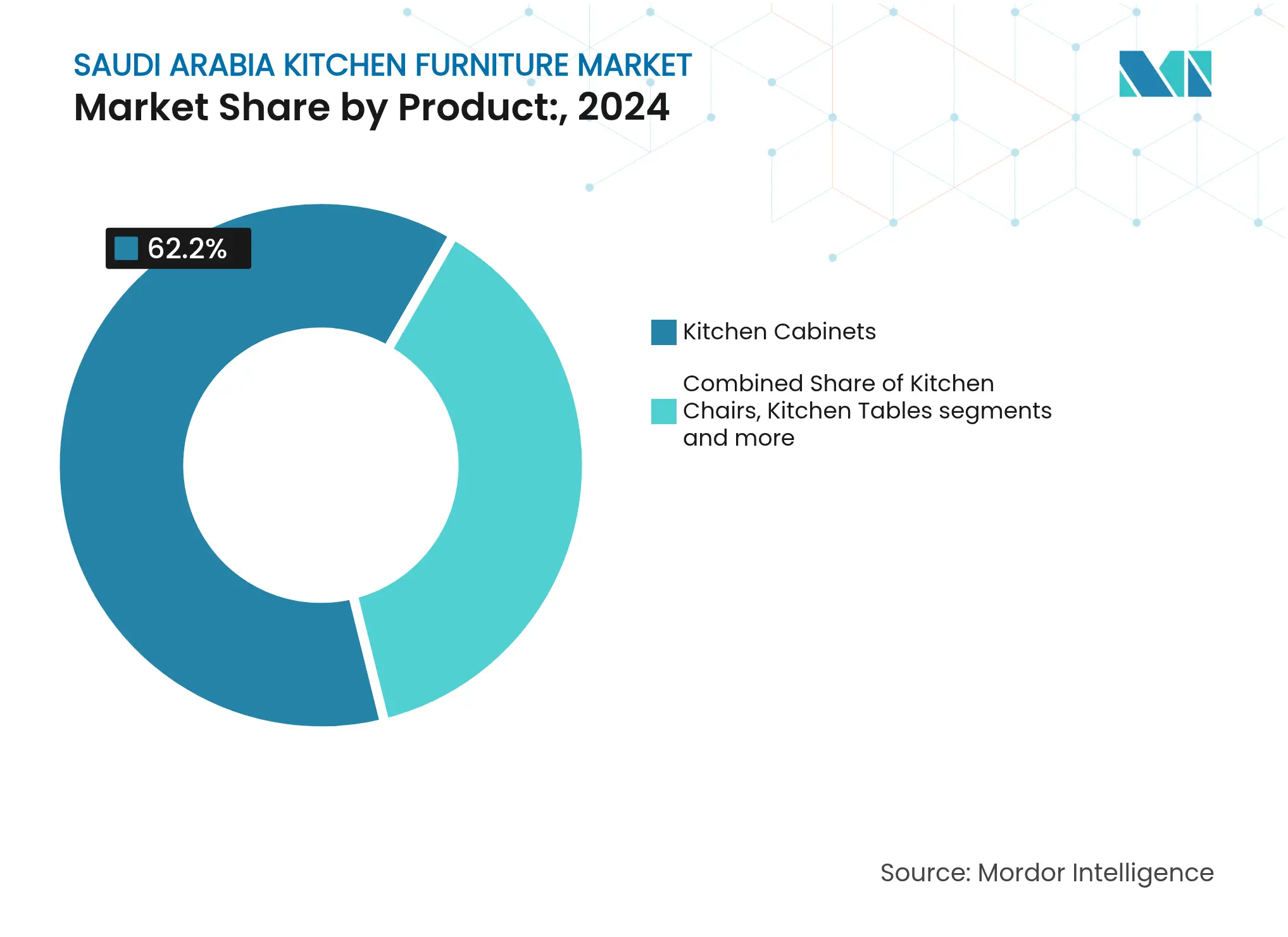

By Product: Cabinets Anchor Volume while Accessories Accelerate Upgrades

The Saudi Arabia kitchen furniture market generated 62.20% of 2024 revenue from cabinet lines, a level sustained by bulk orders from master-planned communities requiring uniform carcass dimensions to streamline installation. Developers procure flat-pack boxes in container lots, cutting logistic costs and reducing on-site waste. Meanwhile, the accessory subset—pantry pull-outs, corner carousels, and mobile trolleys—grew fastest at a 6.91% CAGR, fueled by urban apartments where space optimization is paramount. E-commerce platforms prominently feature video demos of hydraulic lift baskets and IoT-enabled spice racks, enticing buyers into incremental upgrades. Cabinet factories respond by coding SKU architecture so that add-ons snap into pre-drilled holes, allowing homeowners to refresh layouts without full replacements. The Saudi Arabia kitchen furniture market thereby achieves a dual revenue engine: high-volume cabinet shells at baseline and margin-rich accessories sold throughout the ownership cycle.

Oakcraft’s kiln-dried American oak carcasses withstand Saudi thermal swings, a claim supported by accelerated-aging tests conducted in the manufacturer’s Riyadh lab[4]Oakcraft, “Product Catalogue 2025,” oakcraft.com. Such durability credentials resonate with institutional buyers signing 15-year FM contracts. On the accessories front, Hafele’s soft-close hinge kits ship from a Jeddah DC that replenishes retailers every 48 hours, keeping stock-outs rare. Government tenders increasingly demand modular configurations so public-housing recipients can add pull-out trays when budgets permit, bridging the gap between upfront affordability and long-term functionality. These converging preferences reinforce the dominance of cabinets yet extend the revenue tail in the Saudi Arabia kitchen furniture market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Wood Retains Cultural Appeal but Metal Outpaces in Growth

Wood products captured 42.45% of the Saudi Arabia kitchen furniture market size in 2024, building on deep-rooted aesthetic preferences and the versatility of hardwoods when paired with desert-tolerant lacquers. Import substitution possibilities are improving as local sawmills trial heat-modified native species under Vision Forest initiatives. Nevertheless, metal units are projected to expand at a 7.12% CAGR through 2030, addressing hygiene mandates in hospitality kitchens and delivering moisture resilience along coastal resorts. Stainless 304-grade carcasses now ship with powder-coated RAL palettes that mimic timber grain, softening the industrial look and widening appeal to residential loft buyers. The Saudi Arabia kitchen furniture market is therefore poised for blended installations where aluminum frames carry MDF infills, allowing designers to balance cost, weight, and compliance.

Saudi Modern Factory’s Jeddah plant operates an automated powder-line that meets VOC thresholds in SBC 1001, letting it pitch for Green Building certified projects. Wood-centric brands counter by offering FSC-labeled birch cores and water-based varnish, satisfying lenders’ ESG screening. Material choice also intersects with lifecycle costing; hotel operators calculate ten-year TCO and increasingly find stainless steel superior due to reduced refinishing cycles. Suppliers flexible enough to swap facings late in the design calendar stand to capture orders from undecided architects, underscoring the agile dynamics within the Saudi Arabia kitchen furniture market.

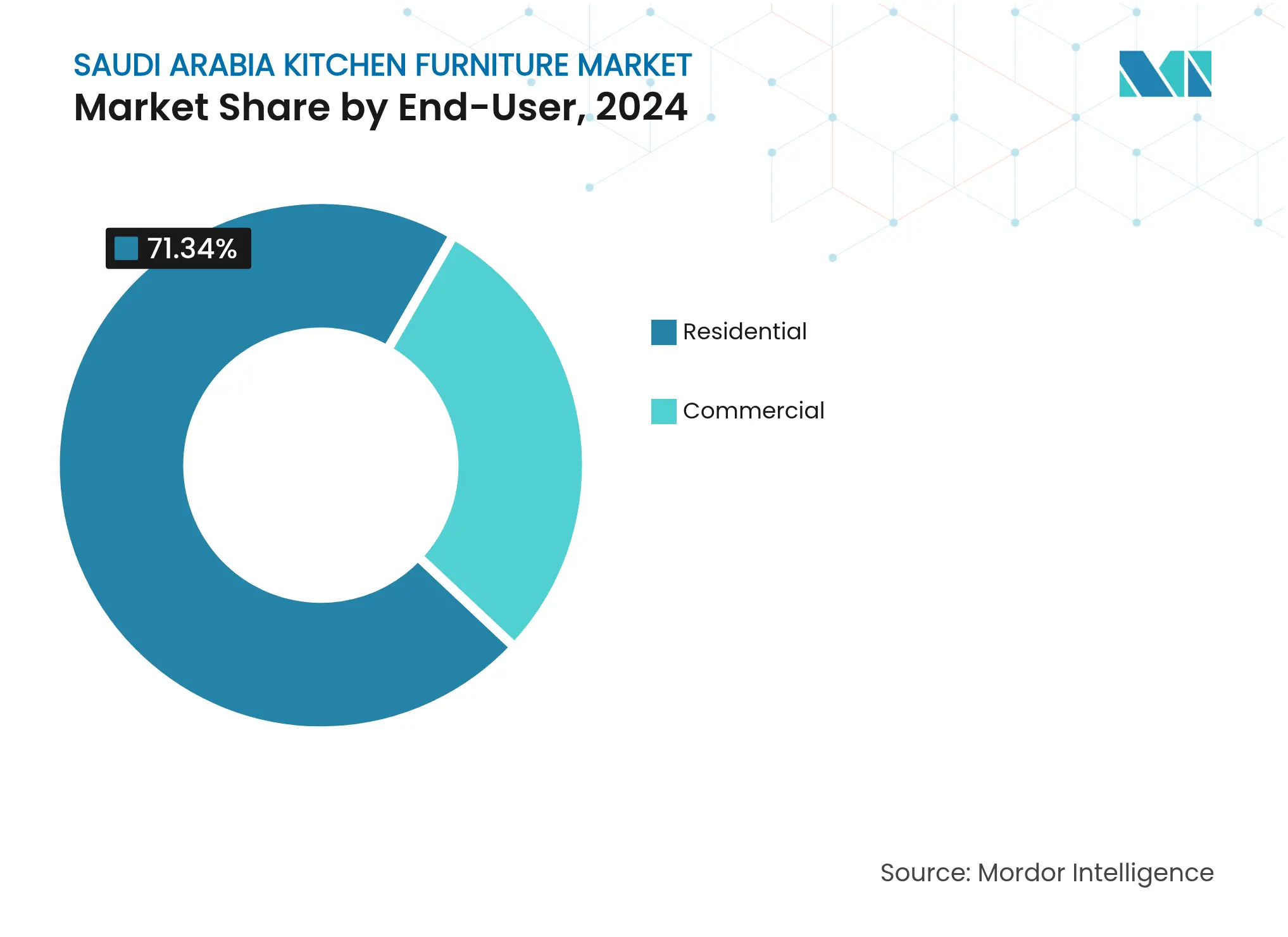

By End-User: Commercial Installations Race Ahead of Residential Base

Residential buyers generated 71.34% of 2024 turnover, supported by a 63.74% homeownership rate and record mortgage flows. Each handover triggers immediate kitchen fit-out, and householders often roll the cost into mortgage add-ons, smoothing cash impact. Commercial projects, however, chart the steeper growth at 7.43% CAGR, stemming from hospitality, education, and health-care programs baked into Vision 2030. Four Seasons Sindalah’s guest villas require concealed-appliance wardrobes and chef-grade prep enclaves, while staff cafeterias mandate bulk-service island benches. Ministry of Health hospital upgrades list antimicrobial solid-surface counters and negative-pressure storage rooms to contain pathogens. These highly specified contracts fetch higher average selling prices per running meter and elevate technical-service revenues in the Saudi Arabia kitchen furniture market.

Commercial buyers evaluate suppliers on BIM object libraries, stainless steel gauge conformity, and documentation of weld integrity. Residential buyers still prioritize style and payment flexibility. Brands catering to both segments establish dual business units: showrooms and e-commerce for homeowners, and tender desks staffed with QS engineers for contractors. Cross-learning flows as consumer-grade laminate colors influence hotel-suite pantry choices, while industrial design practices improve residential moisture-barrier techniques. Such synergy widens innovation bandwidth across the Saudi Arabia kitchen furniture market.

By Distribution Channel: Digital Convergence Redraws the Sales Map

Traditional B2C retail outlets captured 67.12% of 2024 revenue within the Saudi Arabia kitchen furniture market, their dominance propped up by 4,549 malls and a culture of family weekend outings. Showrooms invest in VR pods allowing couples to wander through life-size projections and tweak finishes in real time. Online order confirmation happens at the floor level, with stock shipped from regional hubs the same evening. The B2B project route is scaling at a 6.76% CAGR, powered by procurement portals run by Red Sea Global and large ministries that centralize tendering and favor pre-qualified vendors. Suppliers compliant with e-invoice frameworks and able to upload part numbers to SAP-based catalogs win preferential scoring.

Digital convergence blurs the two tracks: developers embed consumer-facing plug-ins on their off-plan portals so buyers can choose kitchen packages before construction starts, and the chosen SKU automatically feeds into the project ERP docket. Retailers, for their part, spin out “pro desks” inside big-box stores to woo small contractors. Brands that synchronize inventory across physical racks, click-and-collect, and framework-contract dashboards can redeploy stock to fluctuating pockets of demand, optimizing working capital. This fluidity becomes a competitive necessity as the Saudi Arabia kitchen furniture market migrates toward real-time visibility and just-in-time final-mile routing.

Riyadh-centric Central Region secured 37.54% of 2024 sales value, undergirded by dozens of mega-communities sprouting along newly zoned corridors. High white-collar income levels translate into above-average spending per kitchen, and proximity to head offices of major developers accelerates specification cycles. Retail chains cluster flagships around the capital ring road, creating an ecosystem of installers, accessories resellers, and after-sales contractors that lower service lead times. Government agencies located in Riyadh also issue large furniture RFPs, meaning many national tenders funnel through Central Region corporate hubs before deployment nationwide. This administrative gravity cements regional dominance inside the Saudi Arabia kitchen furniture market.

The Western Region is registering the highest growth at 6.87% CAGR, catalyzed by the Red Sea, AMAALA, and NEOM corridors. Resorts under construction specify industrial stainless carcasses, humidity-proof laminates, and anti-corrosive hardware, lifting average order values. Jeddah, as the Kingdom’s main maritime gateway, reduces import-to-dock cycle times, enabling shorter lead-time commitments for European hardware. Retailers leverage the rising disposable income among cruise-terminal employees and newly relocated management staff, opening omni-channel pick-up points along the coastal belt. Environmental regulations unique to marine conservation zones further encourage composite and aluminum products, helping metal-leaning manufacturers penetrate a traditional wooden landscape.

The Eastern Region grows steadily on the back of petrochemical city expansions and expatriate accommodation refurbishments. Southern Region demand received a lift when a global flat-pack brand opened new concept stores in Jazan and Abha in late 2024, eliminating the multi-hour drive residents previously endured to view catalogues in person. Northern Region volumes remain modest yet volatile, depending on the pace of NEOM worker-camp turnovers and site-office rotations. Collectively, balanced regional policy ensures no area remains supply-starved, reinforcing nationwide resiliency for the Saudi Arabia kitchen furniture market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

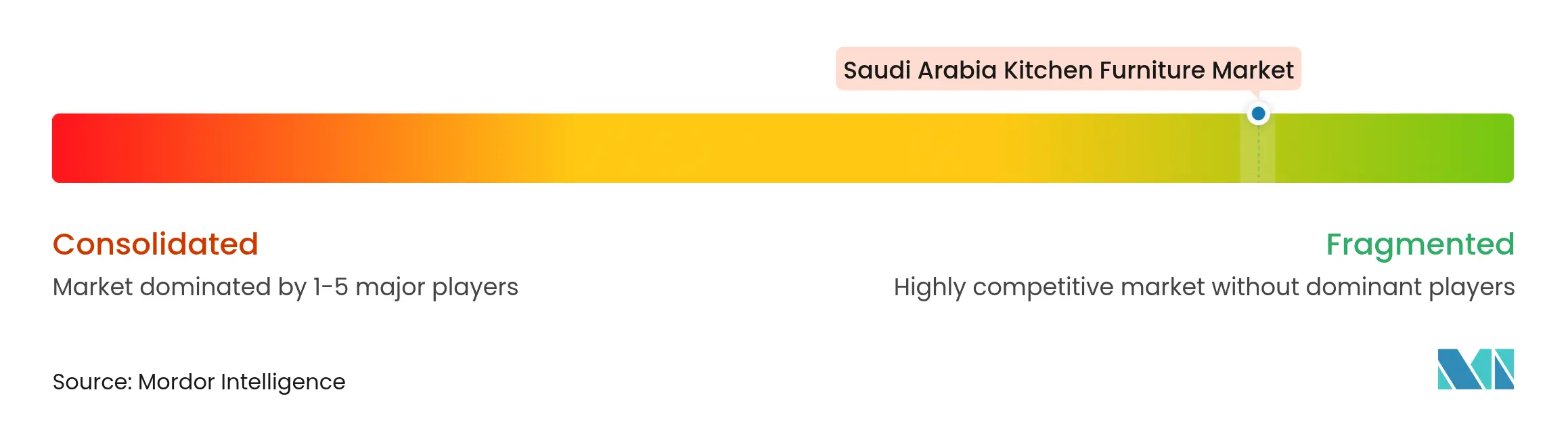

Market Concentration

The Saudi Arabia kitchen furniture market remains highly fragmented. A leading Scandinavian brand pursues a nationwide roll-out of additional “customer meeting points,” diversifying beyond top-tier cities and embedding 3D-design terminals in each smaller outlet. Domestic champion Saudi Modern Factory distinguishes itself through dual-material manufacturing, thereby bidding on packages that require both hardwood detail and stainless core carcasses. Roshn and other master developers deepen collaboration by issuing multi-year framework agreements, prompting suppliers to invest in automated panel-line upgrades and local component sourcing to safeguard continuity.

Technology has emerged as the sharpest differentiator. Appliance maker LG’s built-in range debuts factory-fitted IoT modules, and cabinet partners pre-align hinge holes for its standard mounts, enabling same-hour installation. Digital-first retailers run AI-enabled demand-forecast engines that relocate inventory across stores each night, lowering markdown pressure. Informal workshops, though nimble on pricing, struggle to comply with SBC documentation and therefore find doors closing to institutional contracts. At the same time, Saudization quotas push formal companies to expand training academies that upskill nationals in CAD-CAM woodworking, underscoring a strategic pivot toward human-capital depth in the Saudi Arabia kitchen furniture market.

Local-content scoring continues to reshape sourcing. Developers grant weightings to vendors proving 60% in-Kingdom value-add, leading international brands to sign OEM agreements with Saudi joineries. Access to 0% import duties on raw boards, as opposed to finished furniture, and further incentives for in-country assembly. As a result, global and local enterprises increasingly converge with foreign players contributing design IP and supply-chain governance, while Saudi firms supply workforce and last-mile logistics. The convergent model accelerates knowledge transfer and reduces foreign-currency leakage, all while heightening rivalry among incumbents and newcomers eyeing the Saudi Arabia kitchen furniture market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value in USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Kitchen furniture is the furniture that is installed in a kitchen to store food, cooking utensils, silverware, and utensils for table service, etc. Kitchen appliances such as Fridges, Dishwashers, and Ovens are often included in kitchen cabinetry. The Saudi Arabia Kitchen Furniture Market is segmented by Type (Kitchen Cabinets, Kitchen Chairs, Kitchen Tables, and Other Types) and Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, e-commerce, and Other Distribution Channels). The report offers Market size and forecasts for Saudi Arabia's Kitchen Furniture Market in value (USD) for all the above segments.

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.